Investigate how different economic systems developed based on access to resources, societal values, and human experiences, in order to address the problem of scarcity.

Investigating Economic Systems: How People Around the World Deal With Scarcity 🌍

Imagine you open your favorite game and see a message: “You are out of coins. Come back in 2 hours or buy more.” 😮 That message is actually about a big idea in economics: scarcity. In real life, we don’t have unlimited food, water, money, or time. Because of this, every society has to decide: Who gets what? How is it made? Who makes the decisions? The different ways societies answer these questions create different economic systems.

As shown in [Figure 1], people in different places with different resources and values build different kinds of economies to solve the same problem: how to deal with scarcity.

A world map with small icons showing different economic activities: farms, factories, open-air markets, government buildings, and tech offices in different regions, labeled with different economic systems

What Is Scarcity?

Scarcity means there are not enough resources to give everyone everything they want. Resources include things like:

Human resources: people’s skills, time, and energy

Capital resources: tools, machines, buildings, and technology

Our wants are almost unlimited. People want nice homes, fun trips, new clothes, good food, and more. But resources are limited. That conflict creates scarcity.

Because of scarcity, people and societies have to make choices. When you choose one thing, you usually give up something else. Economists call what you give up your opportunity cost. For example, if you spend your allowance on a game, your opportunity cost might be the snacks or toys you can’t buy now.

Why Economic Systems Exist

Every society needs to answer three basic economic questions:

What goods and services will be produced?

How will they be produced?

For whom will they be produced (who gets them)?

An economic system is the way a society organizes itself to answer these questions. Different societies answer in different ways based on:

Access to resources – What natural, human, and capital resources do they have?

Societal values – What do people in that society care about most (freedom, equality, tradition, security, profit)?

Human experiences – What has happened in their history (wars, colonization, revolutions, climate, inventions)?

Main Types of Economic Systems

Most real countries today are mixed (they blend different systems), but it helps to learn the main four “pure” types first:

Traditional economy

Market economy

Command economy

Mixed economy

[Figure 2] shows these four systems on a line from more government control to more individual freedom.

A horizontal spectrum labeled on the left “More government control (Command)” and on the right “More individual choice (Market)”, with markers for Traditional (below the line, separate), Command, Mixed, and Market

1. Traditional Economies: “We Do It the Way We Always Have” 🏹

In a traditional economy, people make economic decisions based on customs, beliefs, and traditions that are passed down from parents and grandparents.

Key features:

People often hunt, fish, farm, or herd animals.

Work roles are learned from family and community.

Trade is often done through barter (exchanging goods directly without money).

Change happens slowly; people value tradition and stability.

Example: In some Indigenous communities, people might fish in certain seasons, share the catch with elders, and use traditional methods. They do this not just because it’s practical, but because it matches their cultural values of sharing and respect for nature.

Scarcity in traditional economies:

If there is a drought and crops fail, there may not be enough food.

People deal with scarcity by sharing, saving food, or moving to new areas.

Resources and values: Traditional economies often develop in places where people rely heavily on local land and nature. Their values of community, respect for elders, and tradition shape how they use resources and share what they have.

2. Market Economies: “Buyers and Sellers Decide” 🛒

In a market economy, most economic decisions are made by individuals and businesses, not by the government. This is sometimes called capitalism or a free-market system.

Key features:

People can start businesses and choose their jobs.

Prices are set by supply and demand (how much is available and how much people want).

Businesses compete to attract customers.

Consumers (buyers) decide what to buy, which tells businesses what to make.

Example: Think about a popular new sneaker. A company decides to make it, hoping people will like it and buy it. If the sneakers sell out quickly, that shows high demand. Other companies might start making similar shoes to compete.

Scarcity in market economies:

When a product is scarce but many people want it, the price rises.

Higher prices push some people to buy less or not at all, and encourage companies to produce more.

Resources, values, and experiences:

Market economies often grow in places with strong trade and many kinds of businesses.

People value individual freedom, choice, and the chance to earn profit.

Past experiences with strict kings or rulers might make people prefer less government control over the economy.

3. Command Economies: “The Government Decides” 🏛️

In a command economy, the government makes most or all economic decisions. The government decides what will be produced, how it will be produced, and who will get it.

Key features:

The government owns major resources (like factories, land, and mines).

Leaders create plans for the whole economy.

There is little competition because the government controls most businesses.

Example: In the past, the Soviet Union had a command economy. The government would plan how many cars, shoes, and other goods should be made each year. People couldn’t easily start private companies.

Scarcity in command economies:

If the government guesses wrong, there might be shortages (not enough of something) or surpluses (too much of something nobody wants).

People might have to wait in long lines for basic items.

Resources, values, and experiences:

Some command economies developed after wars or revolutions, when leaders wanted equality and strong control to rebuild.

People may value security and fairness more than individual profit.

Leaders might believe that the government can make better choices than individuals and companies.

4. Mixed Economies: “A Blend of Market and Command” ⚖️

Most modern countries today, like the United States, Canada, and many in Europe, have a mixed economy. This means they mix parts of market and command systems.

Key features:

People and businesses make many decisions (like in a market economy).

The government sets rules, protects consumers and workers, and provides services (like in a command economy).

The government might pay for schools, roads, and hospitals.

Example: In the United States, people can start their own businesses and choose their jobs. But the government also makes laws about safety, protects the environment, and runs public schools.

Scarcity in mixed economies:

Prices still help to balance supply and demand.

Governments may help people when they don’t have enough money, food, or healthcare.

Resources, values, and experiences:

Countries with strong mixed economies often have a wide variety of natural and human resources.

They value both freedom and fairness.

Past events, like the Great Depression, taught people that completely free markets can sometimes fail, so they support some government involvement.

How Access to Resources Shapes Economic Systems

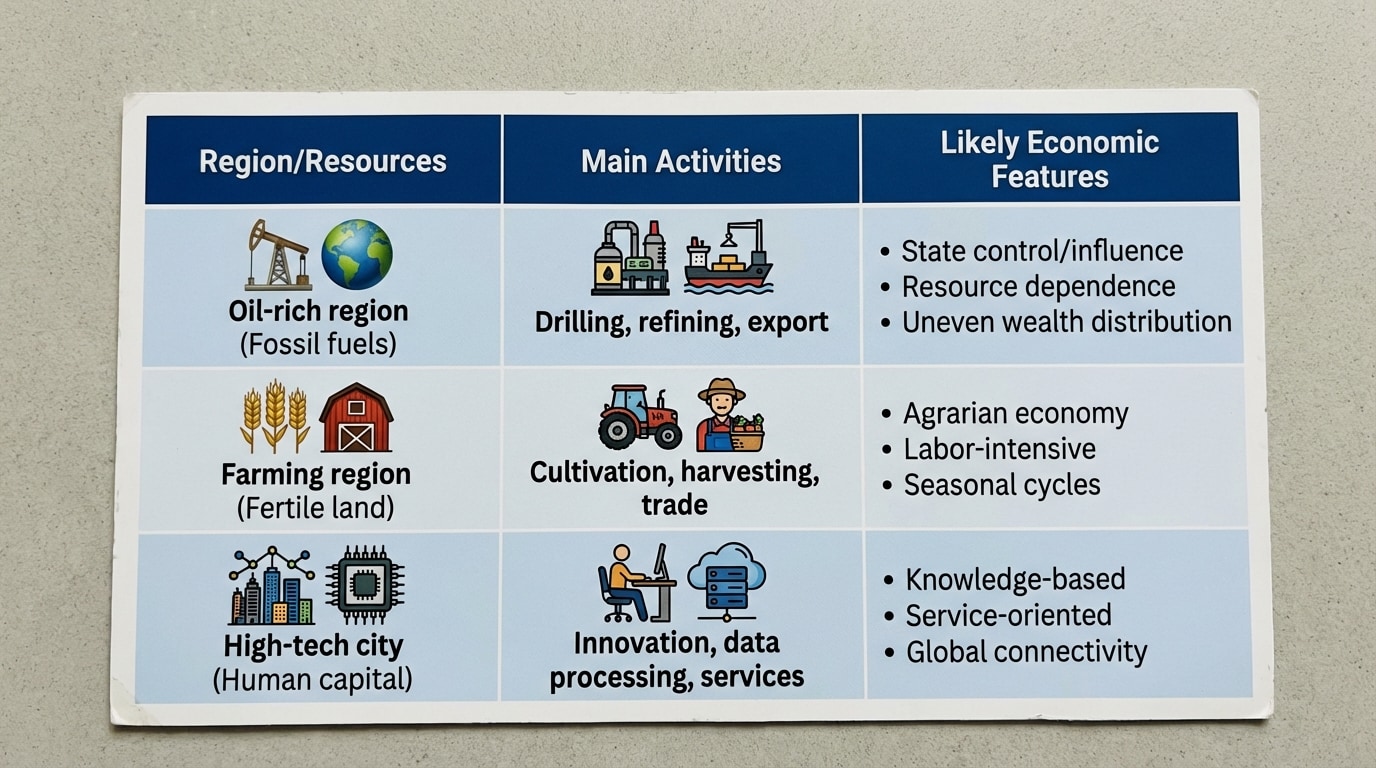

Different places on Earth have different resources. This strongly affects how their economic systems develop. [Figure 3] shows how resource distribution connects to different types of economic activities in a few regions.

A simple chart with three columns labeled “Region/Resources”, “Main Activities”, and “Likely Economic Features”, using examples like oil-rich region, farming region, and high-tech city

Examples:

Oil-rich countries: Some countries in the Middle East have a lot of oil but not much farmland. Their economies focus on drilling and selling oil. The government may control much of the oil industry (more command-like), or private companies may do it (more market-like).

Fertile farming areas: Places with rich soil and good rainfall may have many farms. If families farm the way their ancestors did, they may have more traditional systems. If there are large companies using machines, the system is more market-based.

High-tech cities: A city with many universities and tech workers might develop a strong market economy with lots of startups and innovation.

Did you know? 🌟 Some countries are called “resource-rich but income-poor”. They have valuable resources like diamonds or oil, but because of war, corruption, or weak government, most people still live in poverty. This shows that how a society organizes its economy matters as much as what resources it has.

How Societal Values Shape Economic Systems

Economic systems are not only about money and resources. They also show what a society cares about most.

Important values that affect economic systems:

Freedom: Do people want the freedom to choose their job, start businesses, and buy what they like?

Equality: Do people want wealth and resources to be shared more equally?

Security: Do people want to be sure they will have food, healthcare, and housing, even if they lose a job?

Tradition: Do people want to keep doing things the way their ancestors did?

Connections:

Societies that value individual freedom often lean toward market economies.

Societies that value equality and security may support more government involvement or command elements.

Societies that value tradition may keep traditional economies or mix them with modern systems.

How Human Experiences and History Shape Economic Systems 📜

History is full of events that changed how people thought about the economy. These human experiences include:

Wars: After wars, some countries want strong government control to rebuild; others want freedom and less control.

Revolutions: When people feel an old system is unfair, they may overthrow it and try a new economic system.

Colonization: Empires often forced colonies to produce certain goods (like sugar, cotton, or gold), shaping their economies for many years.

Economic crises: Big crashes or depressions push people to change their system to avoid the same problems again.

Technology changes: Inventions like machines, computers, and the internet change how we work and trade.

Example 1: The Great Depression

In the 1930s, many countries suffered a huge economic crisis. Millions lost jobs and homes. This experience led people in places like the United States to accept more government programs to help the poor and protect workers, moving toward a more mixed economy.

Example 2: After a Revolution

In some countries, like the former Soviet Union and China, revolutions in the 1900s led new leaders to set up command economies. They wanted to control resources and share them more equally, based on their belief that capitalism was unfair.

Comparing Economic Systems Using Scarcity

Let’s compare how each system tries to solve scarcity:

Traditional: Use customs to decide who gets what. Sharing and community help when resources are scarce.

Market: Use prices and competition. If something is scarce, price goes up, encouraging more production and less use.

Command: Use government planning. Leaders decide how to use resources to meet people’s needs.

Mixed: Use a combination. Markets handle many things, but government steps in for fairness and protection.

Every system has trade-offs:

Traditional: Strong community, but slow change and less technology.

Market: Lots of choices and innovation, but some people may be left out.

Command: Tries for fairness, but may waste resources or ignore what people want.

Mixed: Balances freedom and fairness, but can be complicated and political.

Economic Systems in Everyday Life 🎮

You might think economic systems are just for adults, but you see them around you all the time:

At school: The government usually pays for public schools (a command or mixed-economy feature). But you may have choices about clubs and activities (more like a market).

At the store: You choose what to buy, and businesses compete to offer better prices and products (market).

Online games and apps: Game companies decide how to price coins, skins, or upgrades. They respond to what players buy more often. This acts like a tiny market economy inside your game.

Family rules: Sometimes your family might have “command” rules (bedtime is at 9:00, no arguing!) and sometimes more “market-like” choices (you earn allowance by doing chores and decide how to spend it).

Investigating and Asking Good Questions

To really understand how economic systems developed in a country or community, you can ask questions like:

What natural resources are available here?

What jobs do most people do?

Who owns most of the businesses and land—individuals, companies, or the government?

What does this society value most: freedom, equality, tradition, profit, or something else?

What important events in history changed how people work and trade?

By looking at resources, values, and history, you can better understand why a place has a traditional, market, command, or mixed economy—or a combination of them.

Summary of Key Ideas 💡

Scarcity means there are not enough resources to meet all our wants, so societies must make choices. Economic systems are the different ways societies organize to answer the questions “What to produce?”, “How to produce?”, and “For whom?”. Traditional economies are guided by customs and ancestors; market economies are guided by individual choices, prices, and competition; command economies are guided by government plans; and mixed economies combine elements of market and command systems.

Access to resources shapes what countries produce and how their economies grow. Societal values like freedom, equality, security, and tradition influence whether a system is more market-like, command-like, or traditional. Human experiences—such as wars, revolutions, colonization, economic crises, and new technologies—also push societies to change or adjust their systems over time.

All economic systems try to solve the same problem of scarcity but make different trade-offs between freedom and control, change and stability, and profit and fairness. When you look at the resources, values, and history of any place, you can better understand why its economic system looks the way it does—and how people are working to meet their needs in a world where resources are limited. 🎯