What you do with your next paycheck or allowance can either move you closer to your goals or lock you into stress and debt for years. Teenagers sign phone contracts, use debit and credit cards, and take on student loans long before anyone hands them a "how-to" manual. This lesson is that manual — giving you the consumer skills to make money decisions that actually support the life you want.

Consumer skills are the habits and strategies you use when you earn, spend, save, and borrow money. They include how you:

These skills matter because:

Strong consumer skills help you answer questions like: "Can I really afford this?", "What am I giving up if I buy this now?", and "Is this borrowing decision worth the long-term cost?"

Before you can make smart decisions, you need a clear picture of money coming in and money going out.

Income is any money you receive, such as:

Your net income (also called "take-home pay") is what you actually get after taxes and other deductions. If your gross pay for a week is written as \(G\textrm{ (in dollars)}\) and your total deductions are \(D\textrm{ (in dollars)}\), then your net income \(N\textrm{ (in dollars)}\) is

\(N = G - D\)

Expenses are all the ways your money goes out. They usually fall into three key groups:

It also helps to separate needs (things necessary for basic living and responsibilities) from wants (things that are nice to have but not essential). Food, basic transportation, and required school supplies are needs. Concert tickets and premium streaming are wants.

Example: Categorizing expenses

Suppose you have these monthly expenses:

You could see them like this:

A budget is a plan that matches your income with your expenses and savings so that your money goes where you actually want it to go. It is not about perfection; it is about paying attention and adjusting.

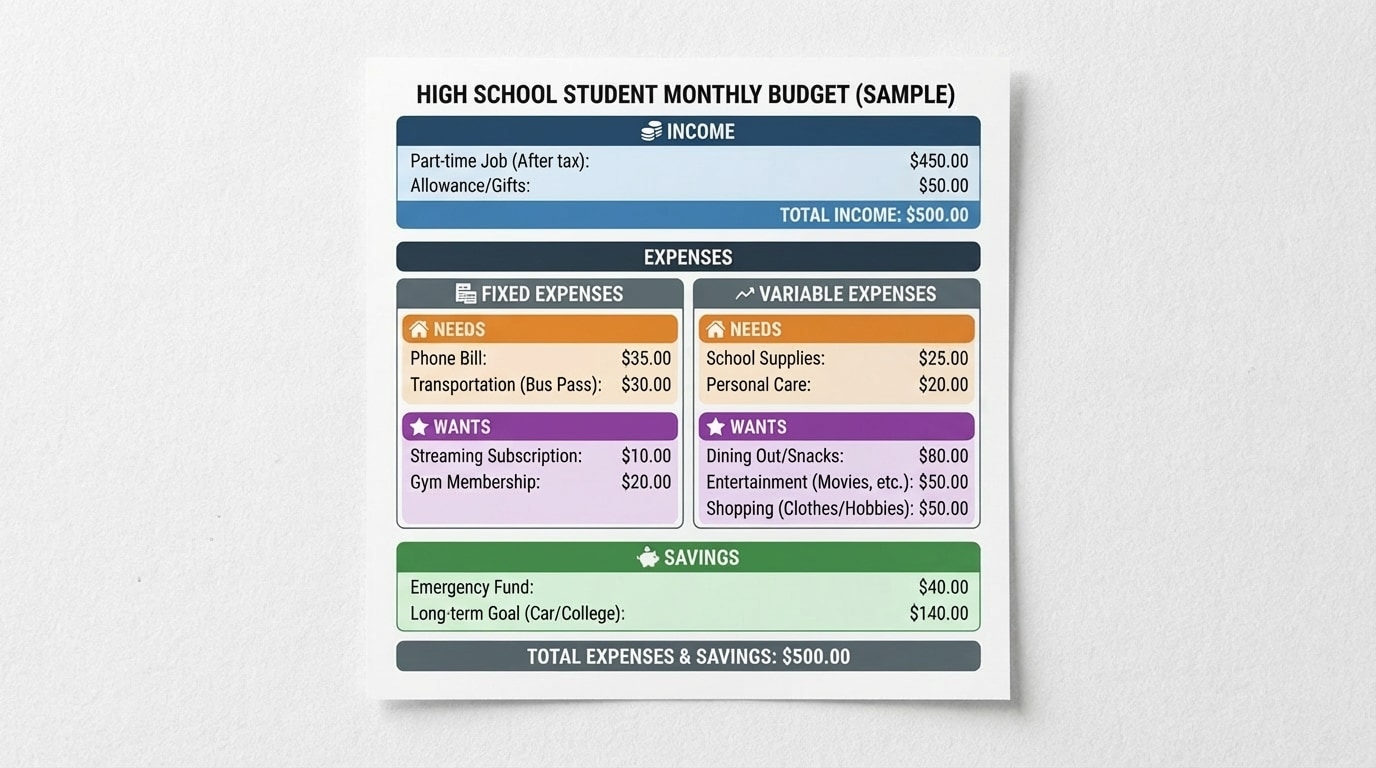

A simple budget usually includes the elements shown in [Figure 1]:

A budget organizes your income at the top and then spreads it across spending and saving categories. This layout helps you see whether your plan fits within your net income and whether you are prioritizing your goals.

Steps to create a basic monthly budget

Example: A teen monthly budget

Suppose you earn net income of $300 in a month from a part-time job. You plan:

Total planned expenses and savings is

\[40 + 60 + 50 + 40 + 30 + 80 = 300\]

Since this equals your income, the budget is balanced. If your total had come to more than $300, you would need to cut some wants or find extra income.

Needs vs wants vs savings

Many people use a simple rule of thumb such as:

The exact percentages can change, but your budget should always include some savings, even if it is small.

| Category | Type | Example |

|---|---|---|

| Rent or family contribution | Need, fixed | Agreed monthly amount to household |

| Phone bill | Need or want, fixed | Base plan cost |

| Streaming service | Want, fixed | Subscription fee |

| Gas or transit | Need, variable | Varies with travel |

| Eating out | Mostly want, variable | Cafes, fast food, deliveries |

| Savings | Future need | Emergency fund, college, car |

Spending is where your budget meets the real world. Smart spending protects your money from impulse, pressure, and clever marketing.

Comparison shopping and unit price

Stores often sell similar items in different sizes and packaging. To compare fairly, look at the unit price, which is the cost per unit (such as per ounce or per liter). If a bottle costs $3.60 for 12 ounces, the unit price is

\[\frac{3.60}{12} = 0.30\textrm{ dollars per ounce.}\]

Another brand might cost $4.80 for 20 ounces, giving a unit price of

\[\frac{4.80}{20} = 0.24\textrm{ dollars per ounce.}\]

Even though the second bottle costs more overall, it is cheaper per ounce.

Sales, discounts, and taxes

A sale sign does not always mean something is affordable or a good value. If a hoodie is originally $60 and is 25% off, the discount is

\[0.25 \times 60 = 15\textrm{ dollars,}\]

so the sale price before tax is

\[60 - 15 = 45\textrm{ dollars.}\]

If your local sales tax rate is 7%, the tax is

\[0.07 \times 45 = 3.15\textrm{ dollars,}\]

so the total cost is

\[45 + 3.15 = 48.15\textrm{ dollars.}\]

Knowing how to estimate total cost (including tax and any fees like shipping) helps you stay within your budget.

Total cost of ownership

A purchase can cost more than the price tag. For example, buying a used car means also paying for insurance, maintenance, repairs, parking, and gas. A slightly more expensive item that is durable and energy efficient can sometimes cost less in the long run than a cheap item that breaks quickly.

Marketing and impulse decisions

Companies use tactics like limited-time offers, "only 2 left", or "free shipping if you spend a little more" to push impulse buying. A simple consumer skill is to pause and ask:

Consumer rights and protections

Smart spending also means knowing you have rights, such as:

Keep receipts, take screenshots of online offers, and read reviews from reliable sources when making bigger purchases.

Saving is choosing to keep some of your money now so you have more options later. A strong consumer knows that future needs and goals are just as real as current wants.

Why save?

Many people treat saving as a bill they pay to themselves first, instead of waiting to save "whatever is left over."

Interest: your money working for you

Banks and credit unions may pay you interest on your savings. If your savings account pays a yearly interest rate of \(r\) (written as a decimal) and you keep a constant balance \(P\) for one year, the simple interest you earn is

\[I = P \times r\textrm{.}\]

For example, if you put $500 into savings at an annual rate of \(0.02\) (that is, 2%), your interest for one full year is

\[I = 500 \times 0.02 = 10\textrm{ dollars.}\]

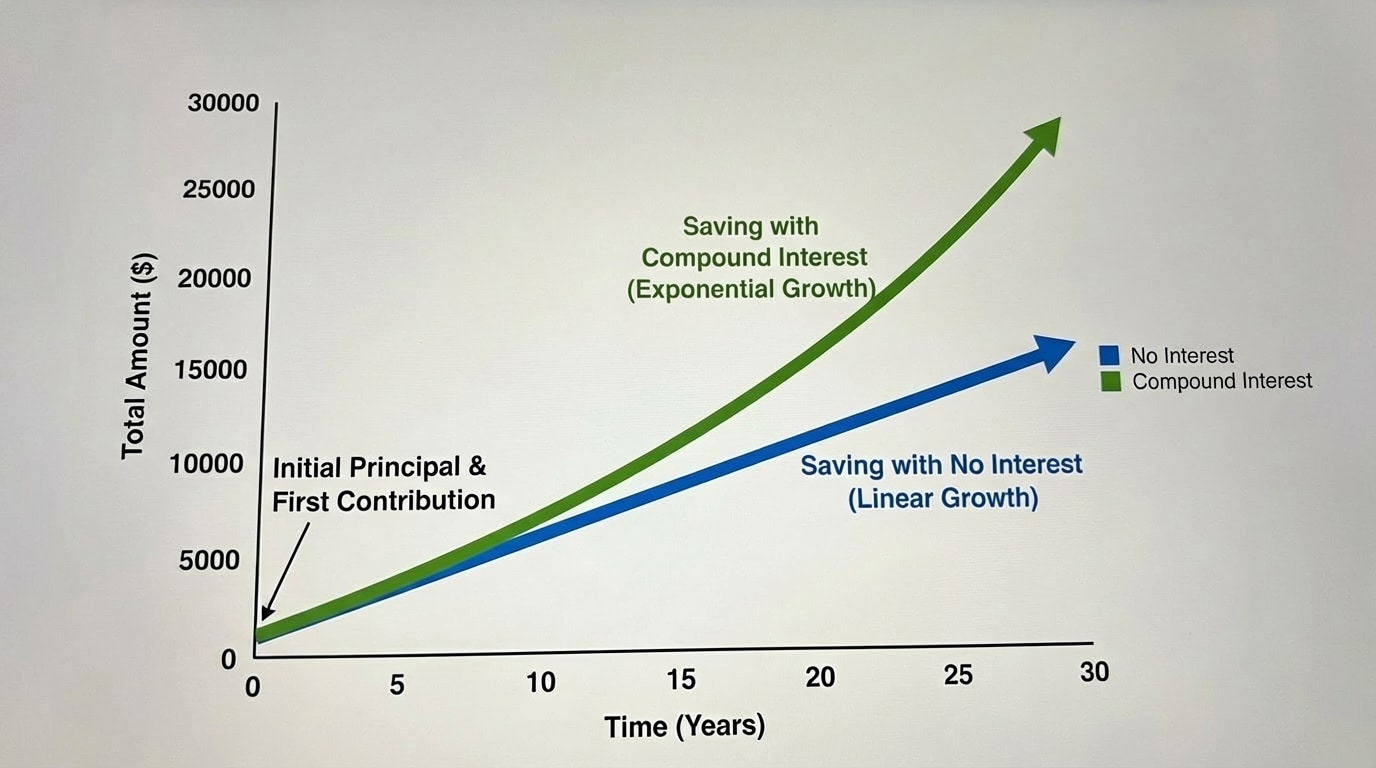

Compound interest

With compound interest, you earn interest on your original money and also on the interest you already earned. Over time, this makes a big difference. The general idea can be shown with

\[A = P(1 + r)^t\textrm{,}\]

where \(A\) is the amount after \(t\) years, \(P\) is the starting amount, and \(r\) is the annual interest rate. The way the curve bends upward over time is illustrated in [Figure 2], showing that the earlier you start, the more time interest has to grow on itself.

Quick compound interest example

If you save $1,000 at a 5% annual rate for 3 years without adding more money, then

\[A = 1000(1 + 0.05)^3 = 1000(1.05)^3\textrm{.}\]

Calculating step by step:

\[(1.05)^2 = 1.1025\]

\[(1.05)^3 = 1.157625\]

So

\[A \approx 1000 \times 1.157625 = 1157.63\textrm{ dollars (rounded).}\]

You earned about $157.63, which is more than you would have earned with simple interest at 5% for 3 years (which would be \(1000 \times 0.05 \times 3 = 150\) dollars).

Types of savings accounts and tools

| Option | Typical Features | Pros | Cons |

|---|---|---|---|

| Checking account | Very easy access, often low or no interest | Great for daily spending | Not ideal for growth |

| Basic savings account | Limited transactions, small interest rate | Simple, low risk, FDIC/NCUA insured | Interest may be low |

| Online savings account | Higher interest, online only | Better growth, convenient apps | May take time to transfer money out |

| Certificate of deposit (CD) | Fixed term (for example, 1 year), fixed rate | Usually higher rate than regular savings | Penalty if you withdraw early |

A strong consumer skill is matching the tool to your goal. Emergency funds belong in accounts you can access quickly; long-term savings you know you will not touch for years can sometimes go into higher-rate options.

Borrowing can help you reach major goals (like education or a car for work), but it also comes with risks and costs. Understanding how borrowing works is essential consumer knowledge.

Key vocabulary

Types of credit

How interest on debt adds up

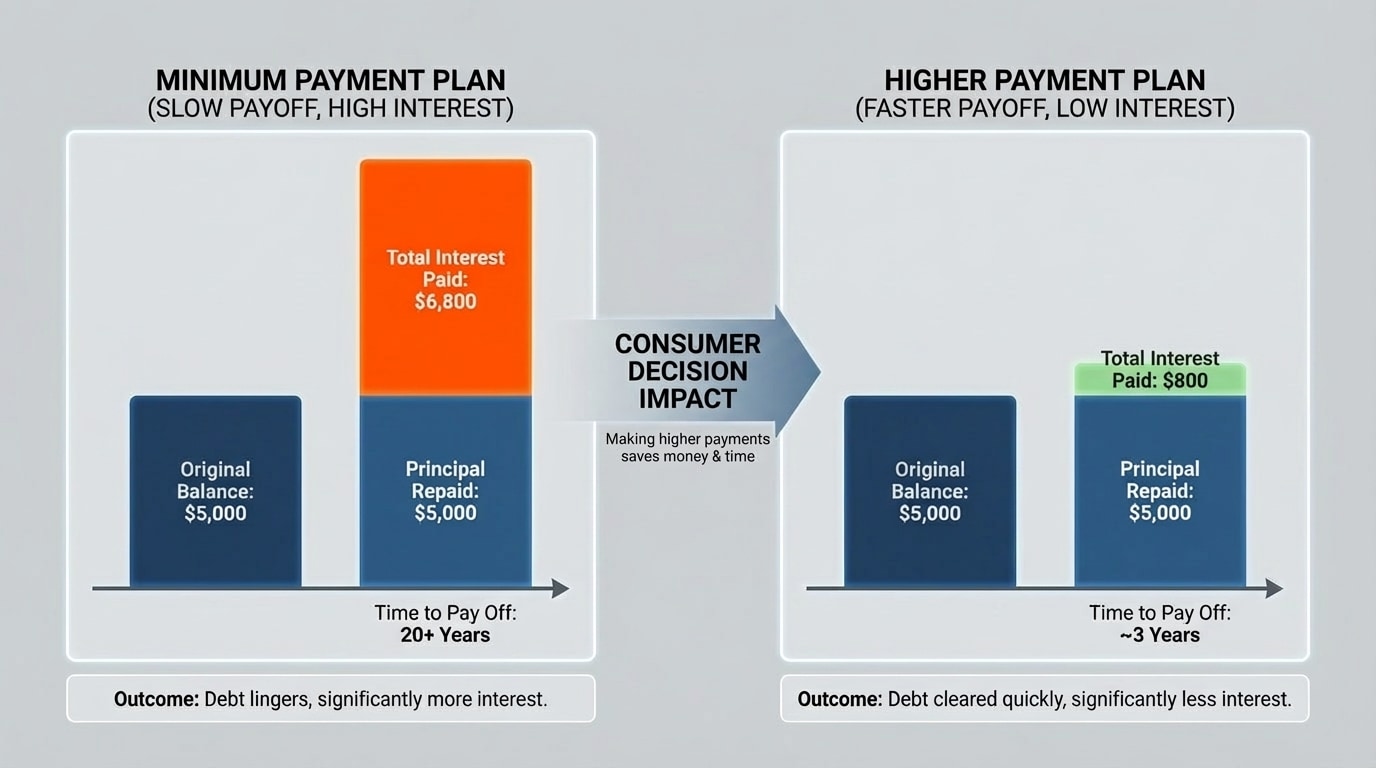

If you carry a balance on a credit card, interest is calculated on what you owe. Suppose you owe $600 on a credit card with an annual rate of 18%. If interest is roughly calculated monthly, the monthly rate would be, as illustrated in [Figure 3],

\[\frac{0.18}{12} = 0.015\textrm{ (that is, 1.5% per month).}\]

In one month, the interest charge on $600 would be about

\[600 \times 0.015 = 9\textrm{ dollars.}\]

If you pay only the minimum payment, you may barely reduce the principal, and you will pay interest again next month on almost the same amount. The way this drags out the payoff time and increases the total cost is similar to what is shown when comparing minimum payments with higher fixed payments.

Example: Minimum payment vs higher payment

Assume your credit card requires a minimum payment of $25 per month on a $600 balance, and you decide instead to pay $60 per month. If you ignore new charges and focus only on paying down the $600, then:

The exact time and interest depend on how your card calculates interest, but the pattern is always the same: higher payments = faster payoff and less total interest.

When borrowing can be reasonable

When borrowing is risky

Not all credit offers are created equal. Consumer skills help you separate useful tools from dangerous traps.

Reading the fine print

When you see an offer like "0% interest for 6 months" or "No payments until next year", check for:

Ask yourself: "If I cannot pay this off by the end of the promo period, what will it really cost me?"

Common high-cost options

Strategies to avoid debt traps

Budgeting, spending, saving, and borrowing are not separate islands; they constantly affect each other.

Scenario: Saving for a laptop and thinking about college

Jordan is a 16-year-old student who wants a $900 laptop and also plans to attend college in two years. Jordan earns $350 per month and currently has no savings.

Jordan makes a plan:

If Jordan consistently saves $80 per month for the laptop, the time needed is

\[\frac{900}{80} = 11.25\textrm{ months,}\]

so roughly 11 to 12 months, depending on any extra savings or sales. At the same time, the $30 per month college savings grows in a separate account, ideally earning interest over time, similar to the curve shown in [Figure 2].

Because Jordan has a clear plan, there is less pressure to use high-interest credit for the laptop. If Jordan did consider a store credit card to buy the laptop immediately, Jordan would compare:

This is what it looks like to apply consumer skills: using information, math, and planning to choose the option that best fits your long-term priorities, not just your short-term desires.

Strong consumer skills give you more control and less stress around money. The core ideas are:

These habits take practice, but every smart decision you make now builds skills and freedom that compound over time, just like interest.