What would happen if tomorrow your phone was stolen, you injured your knee in sports, and your part-time job cut your hours in half—all at once? 😬 Would you be able to pay your bills, get medical care, and replace what you lost, or would you be stuck with debt and stress? The way you prepare before things go wrong is called risk management, and it is one of the most important parts of personal financial literacy.

In everyday life, a risk is the chance that something bad or unexpected happens. In money terms, financial risk is the chance that an event causes you to lose money, owe more money, or miss out on income you expected to receive.

Risk is the possibility that an event will occur and affect your goals, plans, or resources. Financial risk is the chance of losing money or facing unexpected costs. Risk management is the process of identifying risks and choosing strategies to deal with them.

Four big areas of personal financial risk are especially important for teens and young adults:

Every risk has two key features: how likely it is to happen (its probability) and how big the damage is if it happens (its impact). A small, common risk—like losing cheap earbuds—has low impact but maybe higher probability. A rare but serious risk—like a major car accident—has low probability but very high impact. You can imagine a grid that places each risk according to its likelihood and impact, as shown in [Figure 1].

Once you understand likelihood and impact, there are four main ways to respond to a risk:

Good risk management is not about being scared of everything. It is about using a simple process to make smart choices with your time and money.

For example, losing a $15 water bottle is low impact. You probably just accept that risk. But a hospital bill of $5,000 could be a huge problem, so you would want stronger strategies, like health insurance and an emergency fund.

For many teens, income comes from part-time jobs, summer work, or gigs like babysitting. What if your hours are cut, the business closes, or you are injured and cannot work?

Common causes of income risk include:

Key strategies to protect against lost income include:

Example: Building an emergency fund for lost income

Suppose you work part-time and earn $400 per month. Your essential expenses (phone bill, transportation, basic personal items) total $200 per month. You decide your emergency fund should cover 3 months of essential expenses.

Step 1: Calculate the emergency fund target.

Your monthly essentials are $200, so your target is:

\[3 \times 200 = 600\]

You need $600 in your emergency fund.

Step 2: Plan your monthly savings.

If you decide to save $50 per month, the number of months needed is:

\[\frac{600}{50} = 12\]

It will take 12 months to reach your goal if you stay consistent.

This emergency fund could help you cover basic expenses if you get sick, lose your job, or have your hours cut unexpectedly.

For adults, disability insurance is a major way to transfer income risk, especially if they support a family. As a teen, you might mainly rely on emergency savings and developing valuable skills that let you find new work more easily.

Cars, phones, laptops, and even the contents of your room are at risk from theft, accidents, and disasters like fire or storms. Property risks vary in both cost and probability.

Different tools help manage property risk:

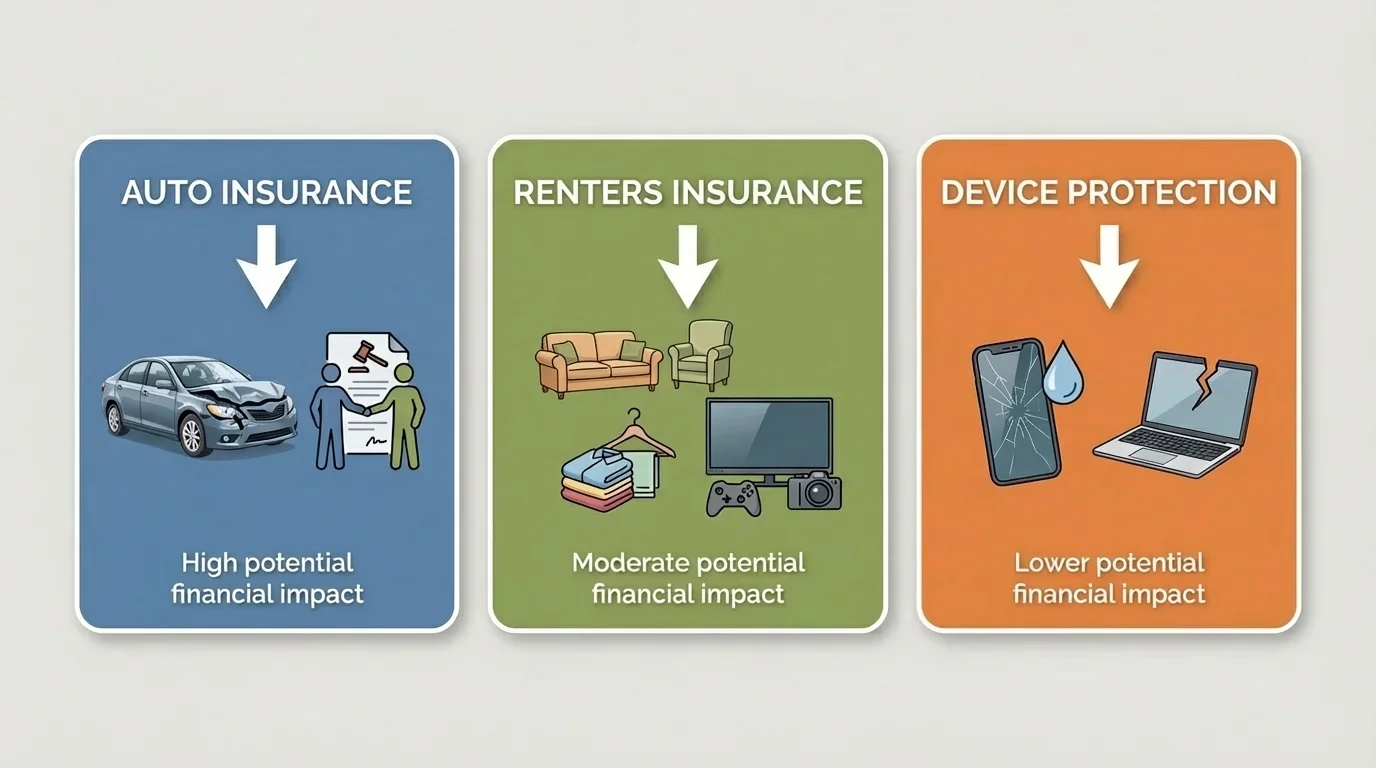

Three common types of insurance related to property are compared below, and their main features are illustrated in [Figure 2]:

| Type of insurance | What it mainly covers | Who usually buys it | Typical risk strategy |

|---|---|---|---|

| Auto insurance | Damage to cars, liability for injuries or damage you cause while driving | Licensed drivers who own or operate vehicles | Transfers high-impact risk of accidents |

| Renters insurance | Personal belongings in a rented home or apartment; sometimes liability | People who rent apartments or houses | Transfers risk of theft or damage to belongings |

| Device insurance | Accidental damage, loss, or theft of phones, laptops, or tablets | People with expensive electronics | Transfers risk of replacing the device, especially early in ownership |

Table 1. Summary of common property-related insurance types.

These policies protect different things and have different costs. Notice that high-value items and large potential losses are more often covered by insurance, while small, affordable items are often self-insured—you simply plan to replace them yourself if needed.

Every insurance policy involves two key money terms:

For example, if your phone insurance has a deductible of $150 and your repair costs $400, you pay $150 and the insurer pays $250. If you rarely damage your phone, the premium plus potential deductible might be more expensive than paying for a repair yourself. This is why you should compare the cost of protection with the size and likelihood of the loss.

Health risks include everything from a simple flu to a serious injury. These risks affect both your health and your finances. Even a short visit to an emergency room can cost hundreds or thousands of dollars.

Health risk strategies focus on both prevention and financial protection:

Common health insurance terms you should know:

Example: Comparing two health insurance plans

Suppose you are covered under a parent's plan and can choose between Plan A and Plan B for the year (imagine the parent makes the final choice, but you help analyze it).

You expect to have 2 doctor visits this year and no major emergencies.

Step 1: Calculate total annual premium for each plan.

Plan A premium per year:\[200 \times 12 = 2{,}400\]

Plan B premium per year:\[150 \times 12 = 1{,}800\]

Step 2: Add expected copays.

Plan A copays:\[2 \times 30 = 60\]

Plan B copays:\[2 \times 40 = 80\]

Step 3: Compare total expected cost for the year (ignoring deductibles because you do not expect to meet them).

Plan A expected cost: premium + copays is\[2{,}400 + 60 = 2{,}460\]

Plan B expected cost: premium + copays is\[1{,}800 + 80 = 1{,}880\]

Based on your expectations, Plan B is cheaper this year. But if you had a big medical event and needed to pay the deductible, the higher deductible in Plan B might make that year more expensive. This shows how risk management involves predicting your likely health needs and balancing regular costs against potential big emergencies.

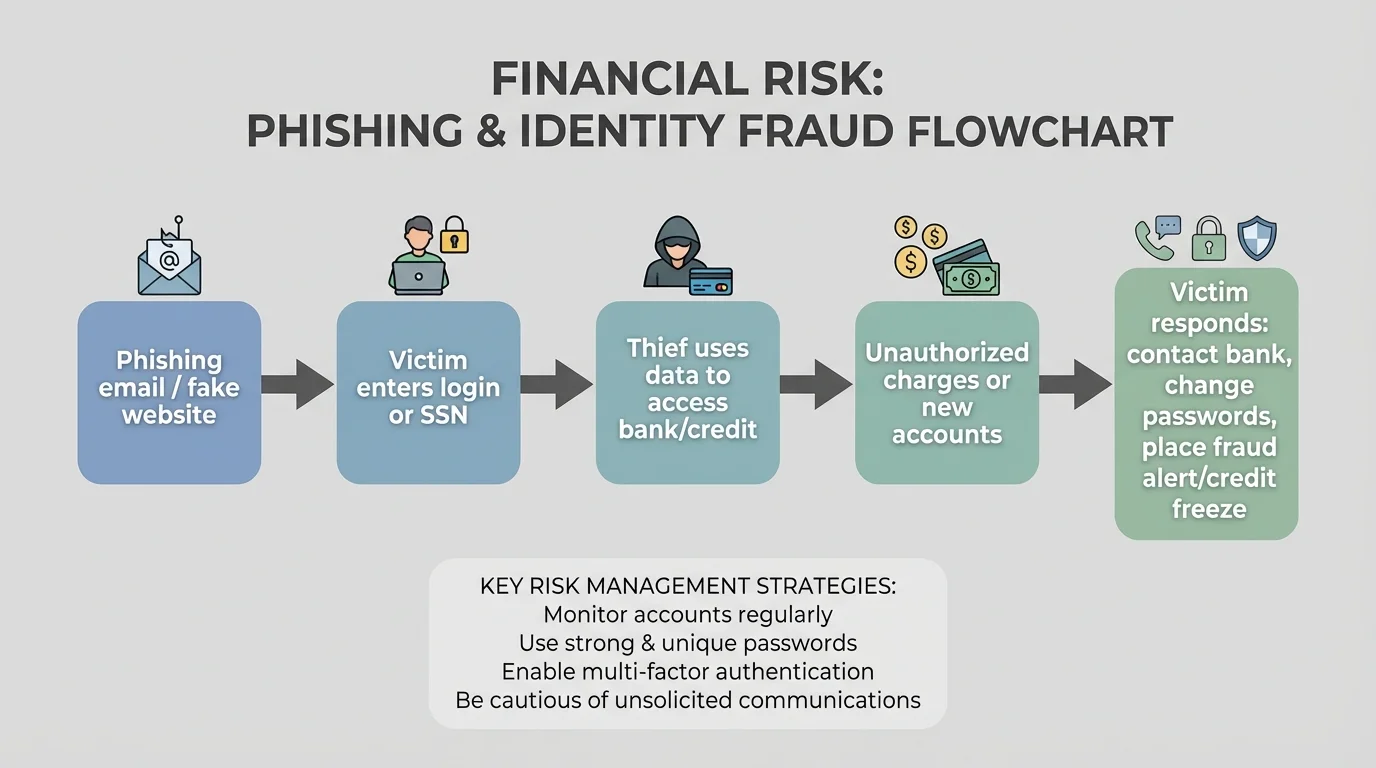

Identity theft happens when someone steals your personal information—like your Social Security number, bank details, or login passwords—and uses it to access your money or open new accounts in your name. With so much of life connected to phones and the internet, identity fraud is a major modern financial risk.

Large data breaches at companies and websites have exposed the personal information of hundreds of millions of people, meaning your data may already be circulating on illegal markets even if you have never personally shared it with a criminal.

Financial identity fraud often follows a pattern, as shown in [Figure 3]:

Key strategies to reduce the risk of identity theft include:

If identity theft still happens, you then need strategies to respond and limit financial damage:

These steps do not transfer risk like insurance, but they can greatly reduce the chance and impact of identity fraud in your financial life. 🔐

Every risk management strategy involves trade-offs. The main question is: Is the cost of protection worth the reduction in risk?

A useful idea for thinking about this is expected loss. If a bad event has probability \(p\) and would cost you \(C\) dollars, then the expected loss is:

\[\textrm{Expected loss} = p \times C\]

This is not a prediction of what will happen in a single year, but it helps you compare options over time.

Example: Should you buy phone insurance?

Suppose a new phone costs $800. A store offers insurance for $8 per month with a deductible of $100 if the phone is lost or damaged. You think there is a 10% chance (probability \(p = 0.10\)) that in the next year you will lose or badly damage the phone.

Step 1: Find the expected loss without insurance.

If you lose or ruin the phone, you have to pay the full $800. With probability \(0.10\), expected loss is:

\[0.10 \times 800 = 80\]

On average, you would expect to lose the equivalent of $80 per year from this risk.

Step 2: Find the expected cost with insurance.

You pay premiums of $8 per month:

\[8 \times 12 = 96\]

per year in premiums. If the phone is lost or damaged (probability \(0.10\)), you also pay the $100 deductible:

\[0.10 \times 100 = 10\]

So your expected total cost with insurance is approximately:

\[96 + 10 = 106\]

Using these numbers, the expected yearly cost with insurance ($106) is higher than the expected loss without insurance ($80). However, remember that without insurance, if the bad event actually happens, you must suddenly find $800, while with insurance, you only need $100 at once. If you do not have savings, you might still choose insurance because it protects you from a large sudden bill, even if it costs a bit more on average. This is the kind of trade-off real risk management involves.

The risk matrix in [Figure 1] is helpful here. You might decide to self-insure (accept the risk) for low-impact items, but transfer or strongly reduce risks that would be financially devastating.

As a high school student, your risk profile looks different from that of a 40-year-old parent, but the same principles apply. Here is a realistic scenario:

A simple risk management checklist for you might look like this:

By applying avoid, reduce, transfer, and accept strategies in each of these areas, you create a personal safety net that protects not only your money but also your future opportunities. You are not trying to eliminate all risk—that is impossible—but to make sure that when bad things happen, they do not destroy your financial stability. 🎯