A fixed monthly mortgage payment may look ordinary, but hidden inside it is one of the most elegant ideas in algebra: a long sum of terms connected by constant multiplication. The same structure appears in finance, population models, computer graphics, radioactive decay, and even the way sound intensity can fade. When a quantity changes by the same factor over and over, algebra lets us compress a long pattern into one useful formula.

If each term in a pattern is found by multiplying the previous term by the same number, the pattern is called a geometric sequence. For example, in the sequence \(3, 6, 12, 24, 48\), each term is multiplied by \(2\) to get the next term. The number \(2\) is called the common ratio.

When we add the terms of a geometric sequence, we get a geometric series. So the sum \(3 + 6 + 12 + 24 + 48\) is a geometric series. If the number of terms is limited, it is a finite geometric series.

Many real problems involve adding repeated changes. Suppose a machine loses \(15\%\) of its value each year. Its values form a geometric sequence. Or suppose a borrower makes equal monthly payments. When those future payments are translated back into present-day value, they form a geometric series. The structure may be hidden, but it is there.

From earlier algebra, remember that repeated multiplication is expressed with exponents. For example, multiplying by \(r\) repeatedly gives \(r^2, r^3, r^4\), and so on. This is why powers of \(r\) appear naturally in geometric sequences.

A geometric sequence with first term \(a\) and common ratio \(r\) looks like this:

\[a, ar, ar^2, ar^3, \dots, ar^{n-1}\]

The sum of the first \(n\) terms is usually written as

\[S_n = a + ar + ar^2 + ar^3 + \dots + ar^{n-1}\]

Here, \(a\) is the first term, \(r\) is the common ratio, and \(n\) is the number of terms.

Not every series is geometric. To check whether a series is geometric, divide each term by the one before it. If the quotient stays constant, the series is geometric. For example, in \(5 + 10 + 20 + 40\), the ratios are \(\dfrac{10}{5} = 2\), \(\dfrac{20}{10} = 2\), and \(\dfrac{40}{20} = 2\), so this is geometric with \(r = 2\).

In contrast, \(4 + 7 + 10 + 13\) is not geometric, because the ratios are not constant. That is an arithmetic pattern, not a geometric one.

Geometric series can have ratios that are fractions or even negative numbers. For example, \(8 + 4 + 2 + 1\) has ratio \(\dfrac{1}{2}\), and \(3 - 6 + 12 - 24\) has ratio \(-2\).

Geometric sequence: a sequence in which each term is found by multiplying the previous term by the same constant ratio.

Geometric series: the sum of the terms of a geometric sequence.

Finite geometric series: a geometric series with a limited number of terms.

Common ratio: the constant factor \(r\) used to move from one term to the next.

Once you identify the first term and common ratio, you can use structure instead of long addition. This is exactly the kind of expression rewriting that makes algebra powerful.

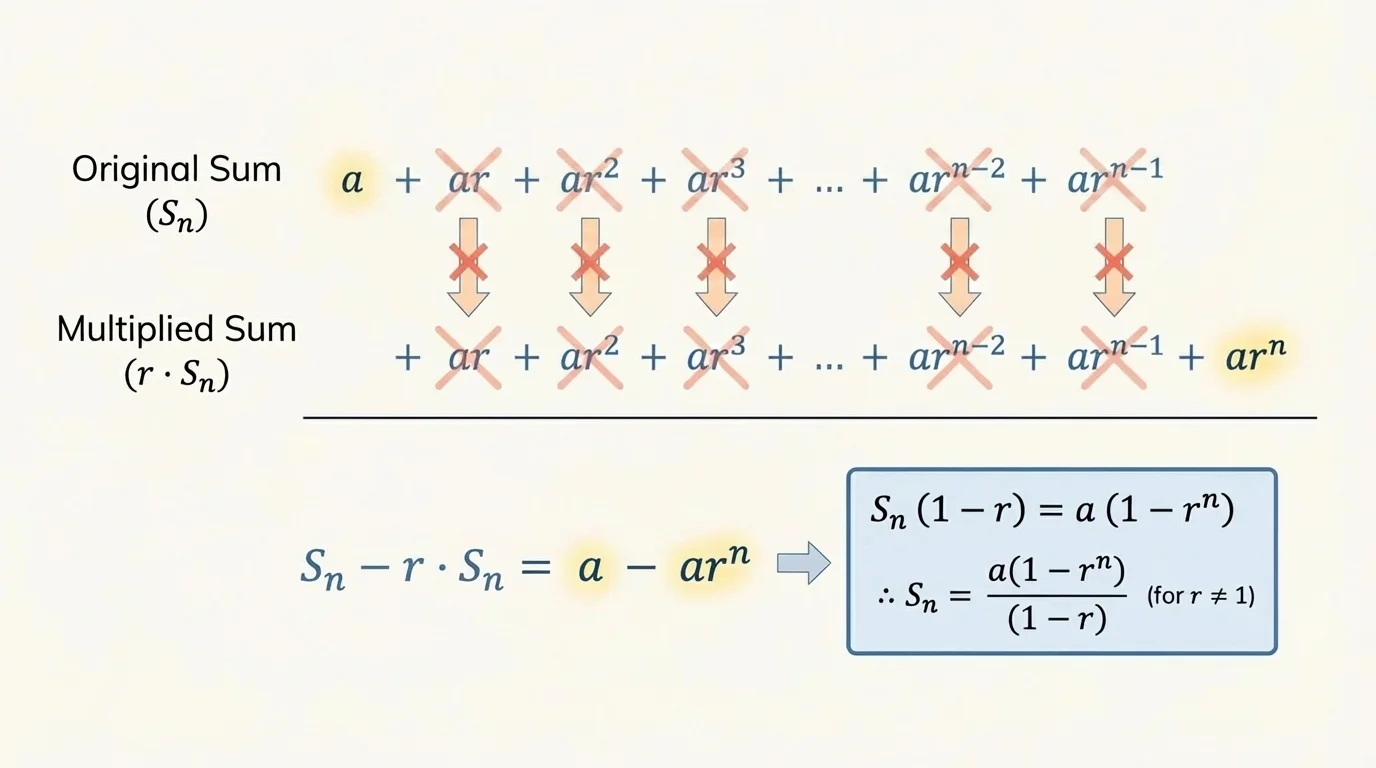

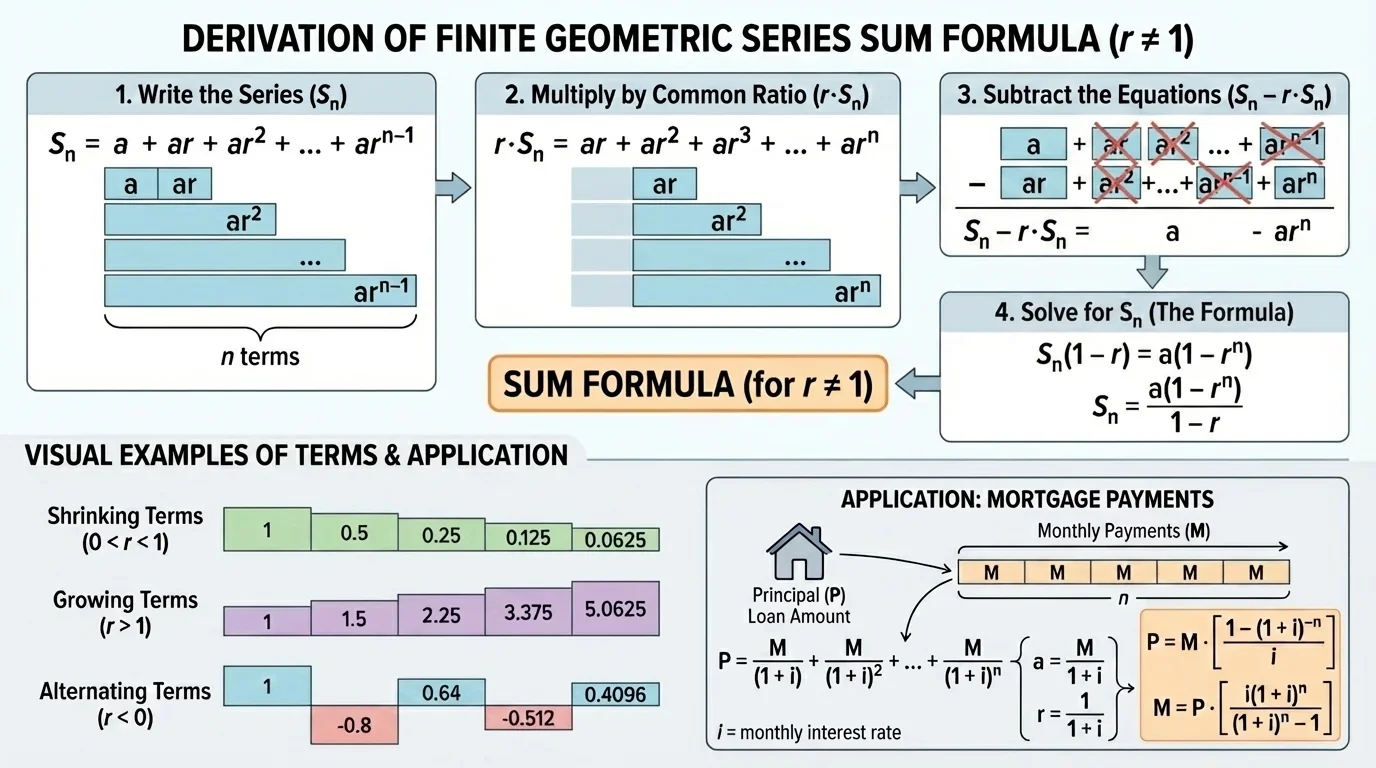

The formula for the sum is not magic. It comes from a clever subtraction pattern, and that pattern is easier to follow in [Figure 1], where the terms are lined up so most of them cancel. Start with the sum of the first \(n\) terms:

\[S_n = a + ar + ar^2 + ar^3 + \dots + ar^{n-1}\]

Now multiply both sides by \(r\):

\[rS_n = ar + ar^2 + ar^3 + \dots + ar^{n-1} + ar^n\]

Subtract the second equation from the first:

\[(S_n - rS_n) = (a + ar + ar^2 + \dots + ar^{n-1}) - (ar + ar^2 + \dots + ar^{n-1} + ar^n)\]

Almost every term cancels. What remains is

\[S_n - rS_n = a - ar^n\]

Factor both sides:

\[S_n(1-r) = a(1-r^n)\]

Now divide by \((1-r)\), as long as \(r \ne 1\):

\[S_n = \frac{a(1-r^n)}{1-r}\]

This is the standard formula for the sum of a finite geometric series when \(r \ne 1\). An equivalent form is

\[S_n = \frac{a(r^n-1)}{r-1}\]

These two formulas mean the same thing because multiplying numerator and denominator of the first by \(-1\) gives the second.

The derivation works because geometric expressions repeat in a highly organized way. That repeated structure is exactly what allows the subtraction to collapse a long sum into just two terms.

The formula \(S_n = \dfrac{a(1-r^n)}{1-r}\) depends on three values: the first term \(a\), the common ratio \(r\), and the number of terms \(n\).

As [Figure 2] shows, changing the value of \(r\) changes the whole behavior of the series. If \(0 < r < 1\), the terms get smaller. For example, \(16 + 8 + 4 + 2 + 1\) shrinks because the ratio is \(\dfrac{1}{2}\). If \(r > 1\), the terms grow. If \(r < 0\), the signs alternate, such as \(5 - 10 + 20 - 40\).

The condition \(r \ne 1\) matters. If \(r = 1\), every term is just \(a\), so the sum is simply \(na\). The derived formula would have a denominator of \(1-1=0\), which is undefined.

Students often mix up \(n\) and the highest exponent. In a geometric series with \(n\) terms, the last exponent is \(n-1\), not \(n\). That is why the subtraction step produces \(ar^n\).

Another common error is identifying the wrong first term. In the series \(12 + 6 + 3 + 1.5\), the first term is \(12\), not \(6\), and the ratio is \(\dfrac{1}{2}\). Accuracy at the start makes the formula work smoothly.

Credit cards, car loans, mortgages, and many investment accounts all rely on repeated multiplication factors. Finance often looks complicated because of vocabulary, but underneath it, much of the mathematics is geometric growth or geometric decay.

Later, when we return to mortgage payments, the same idea of repeated multiplication will reappear through repeated discounting of equal payments, just as the cancellation idea in [Figure 1] turned a long sum into a short expression.

Use the formula to find the sum

\[2 + 6 + 18 + 54 + 162\]

Worked example

Find the sum of the geometric series \(2 + 6 + 18 + 54 + 162\).

Step 1: Identify \(a\), \(r\), and \(n\).

The first term is \(a = 2\). The common ratio is \(r = 3\). There are \(n = 5\) terms.

Step 2: Substitute into the formula.

\(S_5 = \dfrac{2(1-3^5)}{1-3}\)

Since \(3^5 = 243\), this becomes \(S_5 = \dfrac{2(1-243)}{-2}\).

Step 3: Simplify.

\(S_5 = \dfrac{2(-242)}{-2} = 242\)

\(S_5 = 242\)

You can check by direct addition: \(2 + 6 + 18 + 54 + 162 = 242\). The formula matches the arithmetic, but it is much faster for longer series.

A sound system loses \(20\%\) of its value each year. If it is worth $2,000 now, then its values over the next four years are multiplied by \(0.8\) each year. Suppose we want the total of its values over those five years, including the current value. That is a geometric series.

Worked example

Find the sum of the values $2,000, $1,600, $1,280, $1,024, and $819.20 using a geometric-series formula.

Step 1: Identify the pattern.

The first term is \(a = 2000\), the common ratio is \(r = 0.8\), and the number of terms is \(n = 5\).

Step 2: Use the finite geometric sum formula.

\(S_5 = \dfrac{2000(1-0.8^5)}{1-0.8}\)

Step 3: Compute the power and simplify.

Since \(0.8^5 = 0.32768\), we get \(S_5 = \dfrac{2000(1-0.32768)}{0.2}\).

This gives \(S_5 = \dfrac{2000(0.67232)}{0.2} = \dfrac{1344.64}{0.2} = 6723.2\).

\[S_5 = 6723.2\]

The total value over the five years is $6,723.20.

This kind of model appears whenever a quantity repeatedly changes by the same percentage. The ratio is not found by subtracting the percent but by converting the percent change into a multiplier: a \(20\%\) decrease means multiplying by \(0.8\), while a \(5\%\) increase means multiplying by \(1.05\).

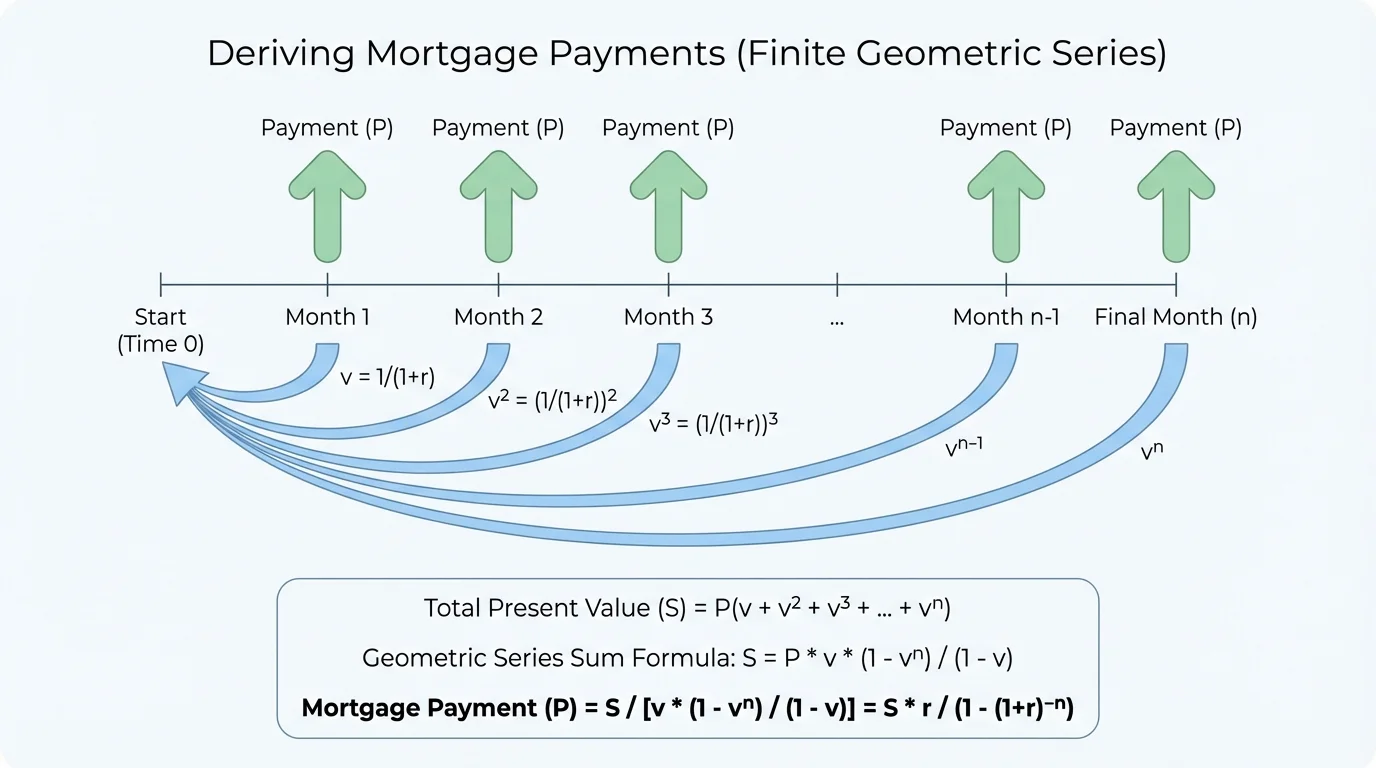

A mortgage is a loan used to buy property, usually repaid with equal monthly payments over many years. The surprising part is that equal payments do not mean equal portions of principal and interest every month. Early payments include more interest, while later payments reduce the principal more quickly.

To understand why geometric series appear, think in terms of present value, the value today of money paid in the future. A payment made one month from now is worth less today than the same payment made immediately, because money can earn interest. [Figure 3] illustrates how equal future payments, when discounted back to the present, form a geometric pattern.

Suppose the monthly interest rate is \(i\), the monthly payment is \(M\), and there are \(n\) payments. Then the present value of those payments is

\[\frac{M}{1+i} + \frac{M}{(1+i)^2} + \frac{M}{(1+i)^3} + \dots + \frac{M}{(1+i)^n}\]

This is a geometric series with first term \(\dfrac{M}{1+i}\) and common ratio \(\dfrac{1}{1+i}\).

If the amount borrowed is \(P\), then that present value must equal \(P\). So

\[P = \frac{M}{1+i} + \frac{M}{(1+i)^2} + \dots + \frac{M}{(1+i)^n}\]

Using the finite geometric series formula, this becomes

\[P = M\left(\frac{1-(1+i)^{-n}}{i}\right)\]

Now solve for \(M\):

\[M = \frac{Pi}{1-(1+i)^{-n}}\]

This is the standard mortgage payment formula. It is really a geometric-series formula in disguise.

The expression \((1+i)^{-n}\) appears because future payments are discounted back to the present. The farther away the payment is, the more times you divide by \((1+i)\). That repeated division creates the common ratio.

Suppose a borrower takes out a $250,000 mortgage at an annual interest rate of \(6\%\), to be repaid monthly over \(30\) years. We want the monthly payment.

Worked example

Calculate the monthly payment for a $250,000 mortgage at \(6\%\) annual interest for \(30\) years.

Step 1: Identify the loan values.

The principal is \(P = 250000\).

The monthly interest rate is \(i = \dfrac{0.06}{12} = 0.005\).

The total number of monthly payments is \(n = 30 \cdot 12 = 360\).

Step 2: Use the payment formula.

\(M = \dfrac{Pi}{1-(1+i)^{-n}}\)

Substitute: \(M = \dfrac{250000(0.005)}{1-(1.005)^{-360}}\).

Step 3: Evaluate the expression.

First compute the numerator: \(250000 \cdot 0.005 = 1250\).

Next, \((1.005)^{-360} \approx 0.16604\).

So the denominator is \(1 - 0.16604 = 0.83396\).

Then \(M \approx \dfrac{1250}{0.83396} \approx 1498.88\).

\[M \approx 1498.88\]

The monthly payment is approximately $1,498.88.

This number does not include property taxes, insurance, or fees. In real life, a monthly housing bill is often higher than the mortgage payment itself.

Notice how different this is from simply dividing the loan amount by the number of months. If there were no interest, then dividing $250,000 by \(360\) would give about $694.44 per month. Interest more than doubles that payment. The geometric-series model captures the effect of repeated monthly interest.

Just as the geometric pattern in [Figure 3] shows payments being discounted back to the present, the formula balances all future payments so their total present value exactly matches the amount borrowed.

Finite geometric series are useful far beyond mortgages. They model installment savings plans, machine depreciation over fixed periods, repeated rebounds of a ball, and total distance traveled when each bounce reaches a fixed fraction of the previous height.

For example, if a ball is dropped from \(10\) meters and rises to \(\dfrac{3}{4}\) of its previous height on each bounce, then the bounce heights form a geometric sequence: \(7.5, 5.625, 4.21875, \dots\). If you want the total upward distance over the first \(6\) bounces, you are summing a finite geometric series.

Why equivalent forms matter

The power of this topic is not just memorizing a formula. It is seeing a long expression as a structured object that can be rewritten in a simpler equivalent form. The geometric sum formula is a perfect example: one expression with many terms becomes one compact formula that is easier to evaluate and apply.

That idea is central to algebra. When you rewrite an expression without changing its value, you often reveal a hidden pattern or make a real-world problem solvable.

One common mistake is using addition instead of multiplication to find the pattern. Geometric series depend on a constant ratio, not a constant difference.

Another mistake is substituting the annual interest rate directly into a monthly mortgage formula. If payments are monthly, the rate must be monthly too. That means dividing the annual rate by \(12\).

A third mistake is using the wrong number of periods. A \(30\)-year mortgage with monthly payments has \(360\) periods, not \(30\).

Students also sometimes reverse the geometric sum formula incorrectly. Both forms \(\dfrac{a(1-r^n)}{1-r}\) and \(\dfrac{a(r^n-1)}{r-1}\) are correct, but you must keep numerator and denominator consistent.

Finally, do not forget that finance formulas often depend on interpretation. In the mortgage formula, \(P\) is the amount borrowed, \(i\) is the periodic interest rate, \(n\) is the total number of payments, and \(M\) is the payment each period. If even one of these is misread, the answer will be wrong.

| Situation | First term | Common ratio | Number of terms |

|---|---|---|---|

| Simple series \(2 + 6 + 18 + 54 + 162\) | \(2\) | \(3\) | \(5\) |

| Depreciation by \(20\%\) | \(2000\) | \(0.8\) | \(5\) |

| Discounted mortgage payments | \(\dfrac{M}{1+i}\) | \(\dfrac{1}{1+i}\) | \(n\) |

Table 1. Examples of how the first term, common ratio, and number of terms appear in different geometric-series situations.

Once you become comfortable identifying the repeated multiplier, many problems that first seem unrelated begin to look alike. That is one of the best parts of algebra: different stories can share the same mathematical structure.