Many people do not run out of money because they buy one very expensive item. They run out of money because of many small choices that seem harmless at the time: a game add-on here, snacks there, a free trial that turns into a monthly charge, or a "great deal" that was not actually needed. Smart money habits are less about being rich and more about making thoughtful decisions.

Every time you spend money, you are making a consumer choice. A consumer is a person who buys goods or services. Goods are physical items, like shoes or a backpack. Services are things people or companies do for you, like a streaming plan, phone service, or a haircut.

Good consumer choices help you get value, stay on budget, and reach future goals. Poor choices can leave you short on money, stuck with something low-quality, or unable to afford something more important later. That is why it helps to slow down and ask, "Is this the best use of my money right now?"

Comparison shopping means looking at different options before buying so you can compare price, quality, features, and other important details.

Budget means a plan for how you will use your money.

Financial goal means a financial target you want to reach, such as saving for new headphones, a trip, or emergency savings.

One of the most useful ways to think about spending is the difference between a need and a want. A need is something important for daily life, health, safety, or basic functioning. A want is something you would enjoy but could live without. Sometimes the line is not perfectly clear. For example, shoes are a need, but a specific expensive brand may be a want.

Knowing that difference does not mean you can never buy wants. It means you should make those choices on purpose instead of automatically.

When you are deciding whether to buy something, three tools work together: comparison shopping, budgeting, and goals. Comparison shopping helps you choose the best option. Budgeting helps you decide whether you can afford it. Goals help you decide whether buying it fits your bigger plans.

Think of these tools like a three-part filter. First, ask which choice gives the best value. Second, ask whether the purchase fits your spending plan. Third, ask whether spending now helps or hurts something you care about later.

Value is more than price. The cheapest option is not always the smartest option, and the most expensive option is not always the best. Real value means what you get for the money you spend. That includes quality, how long the item lasts, whether you will really use it, and any extra costs attached to it.

If you skip one of these tools, your decision gets weaker. For example, you might compare products carefully but forget that your budget is already tight. Or you might have money available now but forget that you are saving for something more important next month.

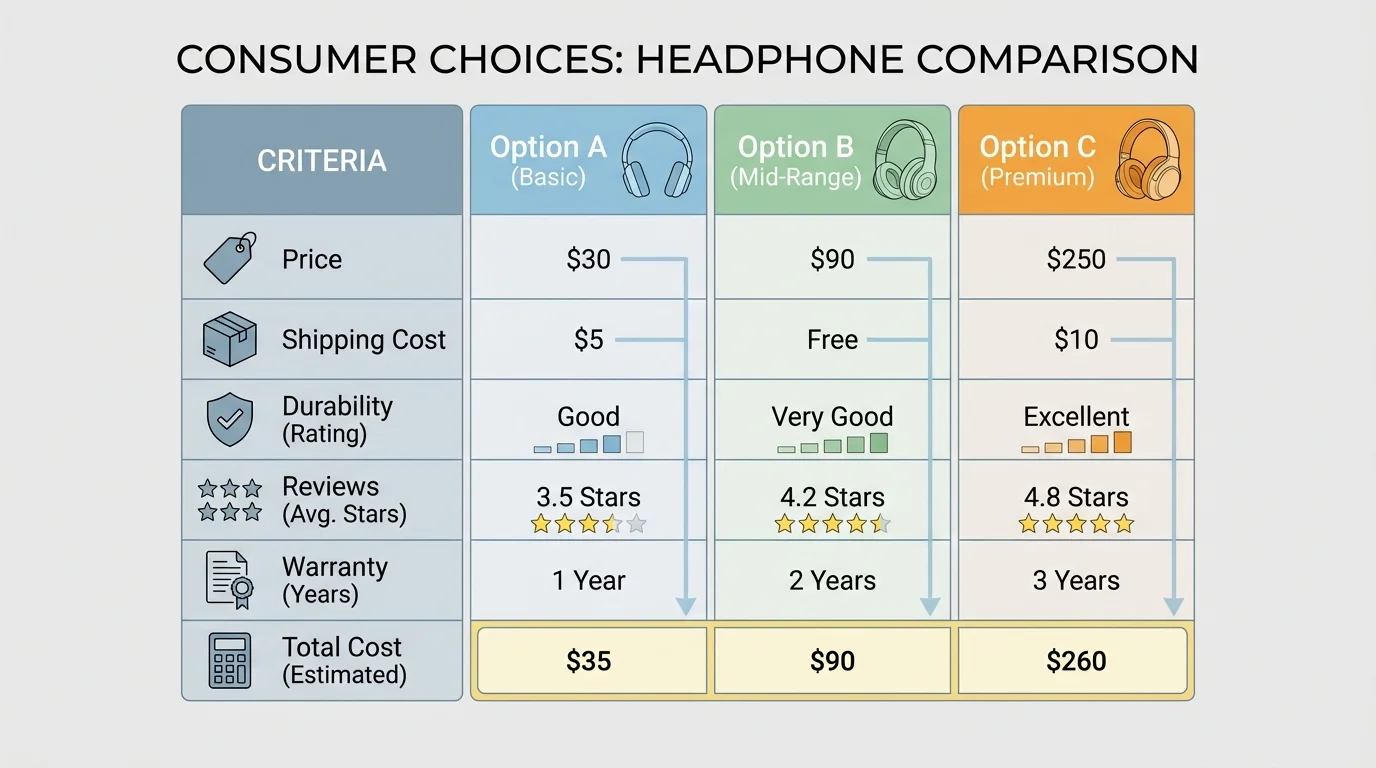

A smart comparison shopping process looks at several factors at once, as shown in [Figure 1]. Price matters, but so do quality, features, shipping cost, return rules, reviews, and how long the product is likely to last.

For example, suppose you want wireless earbuds. One pair costs $20, another costs $32, and another costs $40. If the $20 pair breaks after two months, while the $32 pair lasts a year and includes a case and warranty, the $32 option may actually be the better value.

Another smart move is checking the unit price. Unit price tells you the cost per one item, ounce, pound, or similar amount. It helps when products come in different sizes.

Suppose one snack pack costs $3 for 6 bars. Another costs $4.50 for 10 bars. To compare fairly, divide the total cost by the number of bars. For the first pack, the unit price is \(3 \div 6 = 0.50\), so each bar costs $0.50. For the second pack, the unit price is \(4.50 \div 10 = 0.45\), so each bar costs $0.45. Even though the second pack costs more overall, each bar costs less.

Be careful with hidden costs. A product might look cheaper until you notice shipping fees, taxes, add-ons, accessories, or subscription charges. A video game may cost $15 at first, but if it strongly pushes in-game purchases, your total spending can climb fast.

Reviews can help, but they are not perfect. Look for patterns instead of one dramatic opinion. If dozens of people mention weak battery life, that matters more than one angry comment. Also, be cautious on unfamiliar websites. If a deal looks unbelievably cheap, the site has no clear contact information, and the reviews seem fake, step back.

Comparing three hoodie options

You want a hoodie for cooler weather and find three choices online.

Step 1: List the total cost of each option.

Option A: hoodie is $18 and shipping is $7, so total cost is \(18 + 7 = 25\), which is $25.

Option B: hoodie is $24 with free shipping, so total cost is $24.

Option C: hoodie is $28 with free shipping, so total cost is $28.

Step 2: Compare quality and return policy.

Option A has mixed reviews and no returns. Option B has strong reviews and a 30-day return window. Option C has excellent reviews but costs more than your limit.

Step 3: Choose the best value, not just the lowest sticker price.

Even though Option A looks cheap at first, its total cost is actually higher than Option B once shipping is added. Option B is cheaper overall than Option A and has better reviews.

Best choice: Option B gives the best balance of cost and quality.

As you saw earlier in [Figure 1], comparing several categories at once helps you avoid focusing on only one detail. That is how thoughtful consumers make stronger decisions.

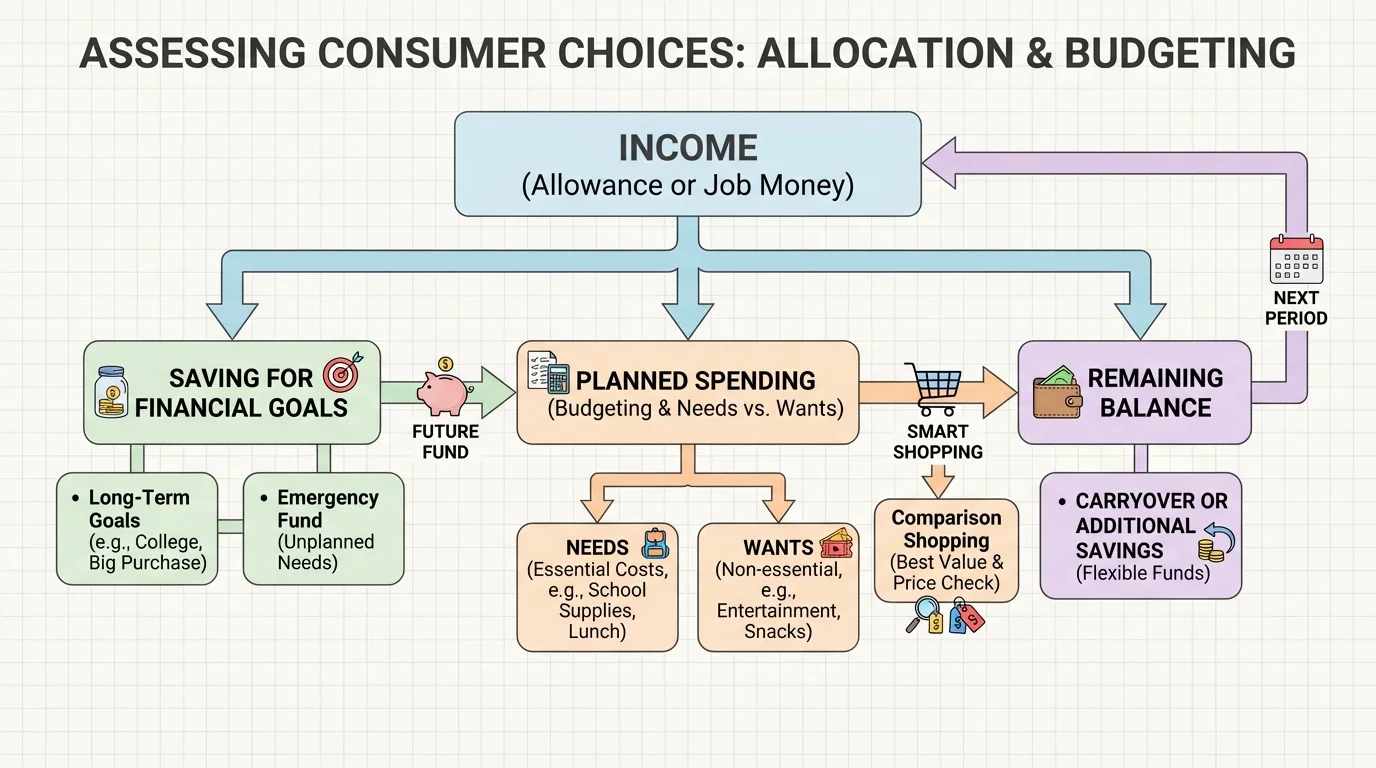

A budget gives each dollar a job, as [Figure 2] shows. It is not meant to punish you. It is meant to help you stay in control so your money does not disappear without you noticing.

Your money might come from allowance, gifts, chores, babysitting, pet care, selling handmade items, or a part-time job. No matter where it comes from, the process is the same: know how much money you have, decide where it should go, and track what actually happens.

A simple budget can be built in three parts: money in, money out, and money saved. Start with the amount you expect to receive. Then decide how much you want to save first. After that, plan how much can be spent.

Suppose you receive $60 this month. You decide to save $20 for a future purchase. That leaves \(60 - 20 = 40\), so you have $40 available for spending. If you already know you will spend $12 on a birthday gift and $8 on school supplies for home learning, then your remaining flexible spending is \(40 - 12 - 8 = 20\), so you have $20 left.

This is why budgeting helps. Without a plan, you might spend the first $25 on snacks and small online purchases, then realize you cannot afford the gift you promised to buy.

| Budget Category | Planned Amount | Why It Matters |

|---|---|---|

| Saving | $20 | Moves you toward a bigger goal |

| Gift | $12 | Known upcoming expense |

| Supplies | $8 | Practical need |

| Flexible spending | $20 | Room for wants and choices |

Table 1. A simple monthly budget showing planned saving and spending.

Budgets work best when they are realistic. If you pretend you will spend $0 on fun when you know that is not true, your budget will fail quickly. It is better to plan a reasonable amount for wants than to ignore them completely.

Basic arithmetic is enough for most budgeting. You mainly add what comes in, subtract what you plan to save, and subtract what you plan to spend. Keeping the numbers simple makes the habit easier to maintain.

Tracking matters too. Planning and reality are not always the same. If you planned to spend $10 but actually spent $16, notice it and adjust. A budget is a living tool, not a perfect prediction.

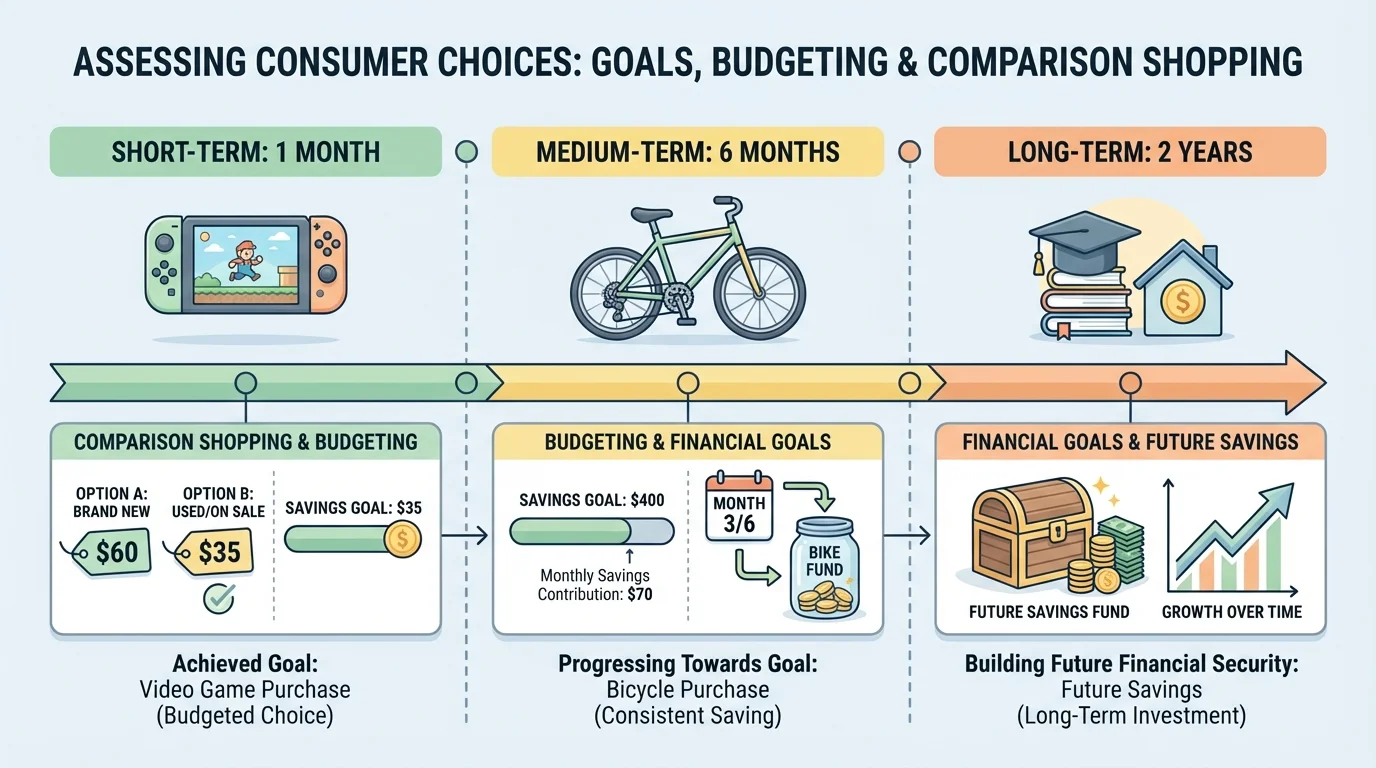

[Figure 3] A financial goal gives your money a direction. Without a goal, spending decisions are often based on mood, pressure, or boredom. With a goal, it becomes easier to say yes to some purchases and no to others.

Goals can be organized by time. A short-term goal might take days or weeks, like saving for a game or event ticket. A medium-term goal might take several months, like buying a bike or upgrading a device. A long-term goal might take a year or more, such as building strong savings for future transportation, training, or emergencies.

Goals also help you understand trade-offs. A trade-off means choosing one thing means giving up another. If you spend $18 on fast food and drinks three times in one week, that is \(18 + 18 + 18 = 54\), which is $54. That same money could have been part of a goal you cared about more.

This is where delayed gratification becomes powerful. Delayed gratification means waiting now so you can get something better later. It is not always easy, especially when apps, ads, and social media are designed to make buying feel urgent. But being able to wait is one of the strongest money skills you can build.

Saving toward a goal

You want a $120 skateboard and already have $30.

Step 1: Find how much more you need.

You still need \(120 - 30 = 90\), so you need $90 more.

Step 2: Decide how much to save each week.

If you can save $15 each week, divide the amount needed by the weekly saving amount: \(90 \div 15 = 6\).

Step 3: Estimate the time.

It will take 6 weeks to reach the goal if you stay consistent.

When you know your goal and timeline, it becomes easier to turn down smaller purchases that would slow you down.

Later, when you are tempted by a random sale, think back to the time-based goal path in [Figure 3]. The question is not only "Can I buy this?" but also "What does buying this do to my plan?"

When you are unsure about a purchase, use this quick process.

Step 1: Name the item or service clearly. What exactly are you buying?

Step 2: Decide whether it is mostly a need, a want, or partly both.

Step 3: Compare at least two or three options. Look at total cost, quality, and policies.

Step 4: Check your budget. Do you truly have room for it right now?

Step 5: Check your goals. Will this purchase slow down something more important?

Step 6: Pause before buying. Waiting even 24 hours can reduce impulse decisions.

Step 7: Make the decision: buy now, wait and save, choose a cheaper option, or skip it.

The best question is not "Do I want it?" A better question is "Is this worth what I must give up?" That could mean giving up time, saved money, flexibility, or progress toward a goal.

This process works for big purchases and small ones. It also works for digital purchases, which can feel less "real" because no cash changes hands physically.

One common trap is impulse buying, which means purchasing something quickly without enough thought. Stores and apps are designed to encourage this. Countdown timers, limited-stock warnings, flashing sale labels, and one-click checkout all push you to act fast.

Another trap is confusing a sale with savings. If something costs $40 and is now $28, you save money only if you were already planning to buy it and it fits your budget. If you buy it just because it is on sale, you still spent $28.

Subscriptions are another danger area. A free trial may become a monthly charge if you forget to cancel. A plan that costs only $6.99 per month may not seem like much, but over 12 months that becomes \(6.99 \times 12 = 83.88\), so the yearly total is $83.88.

Small recurring costs often feel invisible because they are spread out over time. That is exactly why they can be dangerous: your budget can leak money without you noticing.

Social pressure matters too. Seeing influencers, friends online, or creators showing new products can make you feel behind if you do not have the same things. But other people's highlight reels are not a smart budgeting system. Your choices should match your situation, not someone else's feed.

Scams are a real consumer issue. Watch for fake stores, messages asking for payment information, counterfeit products, and deals that seem unreal. Before buying online, check for secure payment methods, real reviews, clear policies, and trusted sites.

Here is how these ideas work in normal life.

Example 1: Earbuds. You have $35. A cheap pair costs $19, but shipping is $8 and reviews say one side stops working quickly. A better pair costs $29 with free shipping and strong reviews. Total cost matters: the first pair costs \(19 + 8 = 27\), so the real difference is only $2. The better-reviewed pair may be the smarter choice.

Example 2: Gaming subscription. You can afford the first month, but your budget is tight and you are saving for sports equipment. The right question is not whether $10 seems small. The right question is whether a repeating charge fits your plan.

Example 3: Trendy jacket. You want a jacket because a style is popular online. Before buying, ask whether you need a jacket, whether a lower-cost option works, and whether you will still like it after the trend fades.

Example 4: Phone plan add-on. A company offers extra data, premium music, and cloud storage in a bundle. Maybe you only need one part of that package. Paying for features you do not use is not good value.

Example 5: Daily snack spending. If you spend $4 after practice or activities five times a week, that is \(4 \times 5 = 20\), so you spend $20 each week. Over four weeks, that becomes \(20 \times 4 = 80\), which is $80 a month. Small habits can have big results.

Quick purchase check: should you buy a $48 hoodie now?

Step 1: Check your available spending money.

You have $70 total, but $30 is already set aside for a concert ticket. That means your available spending money is \(70 - 30 = 40\), so you have $40 available.

Step 2: Compare cost to available money.

The hoodie costs $48, but you only have $40 available. You are short by \(48 - 40 = 8\), so you do not currently have room in your plan.

Step 3: Decide on an action.

You could wait, save $8 more, look for a lower-cost hoodie, or skip the purchase if the concert matters more.

Smart choice: The budget helps you avoid taking money from a goal that already matters to you.

Good consumer skills are built through routines, not one perfect decision. The more often you pause, compare, budget, and connect your choices to goals, the stronger your judgment becomes.

Try these habits in everyday life:

You do not need a lot of money to practice these habits. In fact, learning them early gives you an advantage. Whether you are deciding on snacks, clothes, digital purchases, gifts, or saving for something bigger, the same core skill matters: making choices on purpose.

"Every dollar you spend is a vote for what matters to you."

When your spending, budget, and goals work together, your choices become clearer. You are not just reacting to ads, trends, or pressure. You are deciding what makes sense for your life.