A lot of people lose money without buying anything extra. It happens through tiny charges: a $3 ATM fee here, a $10 monthly fee there, or an overdraft charge that hits when an account drops below zero. One bad choice may not seem huge, but repeated throughout a year, it can quietly drain money you could have saved, spent on something important, or used in an emergency. Knowing how banks work is not just "adult stuff." It directly affects the choices you make now and the options you have later.

When you understand banking services, payment methods, and fees, you become more in control. You stop guessing. You start noticing which tools are helpful, which ones are expensive, and which habits protect your money. That matters whether you are getting paid from a part-time job, receiving money from family, shopping online, paying for subscriptions, or saving for a phone, game system, concert ticket, or future car expenses.

Your money decisions are not only about what you buy. They are also about how you store money, how you pay, and what fees come with those choices. A snack that costs $4 is not really a $4 purchase if you paid with a method that triggered a fee, or if using that method made it easier to overspend.

For example, suppose you take out cash from an ATM that is not part of your bank's network. You might pay a $3 fee from the ATM owner and another $2.50 fee from your own bank. The total extra cost is \(3 + 2.50 = 5.50\). That means getting $20 in cash actually costs you $25.50. Over time, choices like that affect your budget more than many people realize.

Some bank accounts are advertised as "free," but they may still charge fees for certain actions, such as paper statements, out-of-network ATM use, or dropping below a minimum balance.

The smartest approach is to treat your bank account and payment tools like equipment. Good equipment helps you. Bad equipment slows you down, costs extra, or increases risk. You want tools that fit your real habits.

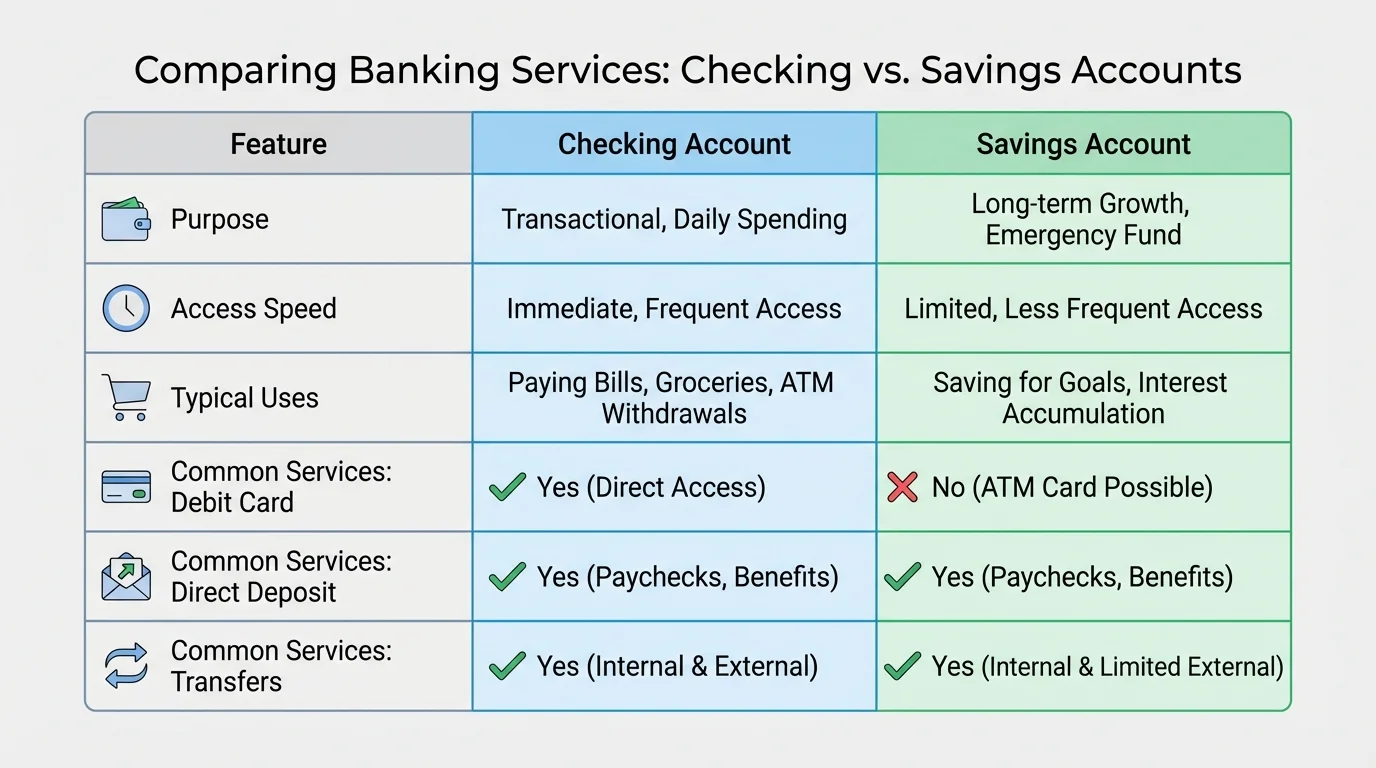

A checking account is usually for everyday spending, while a savings account is usually for money you want to keep for later. These accounts do different jobs, and choosing the right one helps you avoid mixing spending money with savings goals.

[Figure 1] Checking accounts are designed for frequent use. You might use one for a debit card, direct deposit from a job, online bill payments, or sending money through an app. Savings accounts are usually better for goals like emergency money, future purchases, or money you do not want to spend too quickly. Some savings accounts also pay a small amount of interest, meaning the bank adds a little money over time for keeping your money there.

Common banking services include direct deposit, mobile deposit, online banking, ATM access, and transfers. Direct deposit sends money straight into your account, often from a job. Mobile deposit lets you deposit a check using your phone's camera. Transfers move money between accounts. These services make banking faster, but each one may have rules, limits, or fees.

If you get paid from a job, direct deposit can be a strong choice because it is usually fast and secure. If you are saving for something important, moving part of each paycheck into savings can reduce the chance that you spend it automatically. A simple habit like transferring $15 each week adds up to \(15 \times 4 = 60\) in about a month and \(15 \times 52 = 780\) in a year.

Banking services are tools a bank or credit union offers to help you store, move, receive, and monitor money. Examples include debit cards, online bill pay, account transfers, direct deposit, mobile check deposit, and fraud alerts.

Not every account includes the same services. One account may have free ATM use at many locations, while another charges fees more often. One app may send instant alerts for purchases, while another may be less convenient. That is why reading account details matters more than just choosing a well-known bank name.

Later, when you compare account options, think back to the different roles in [Figure 1]. A checking account should make daily use easy, while a savings account should support your goals and help protect money from impulse spending.

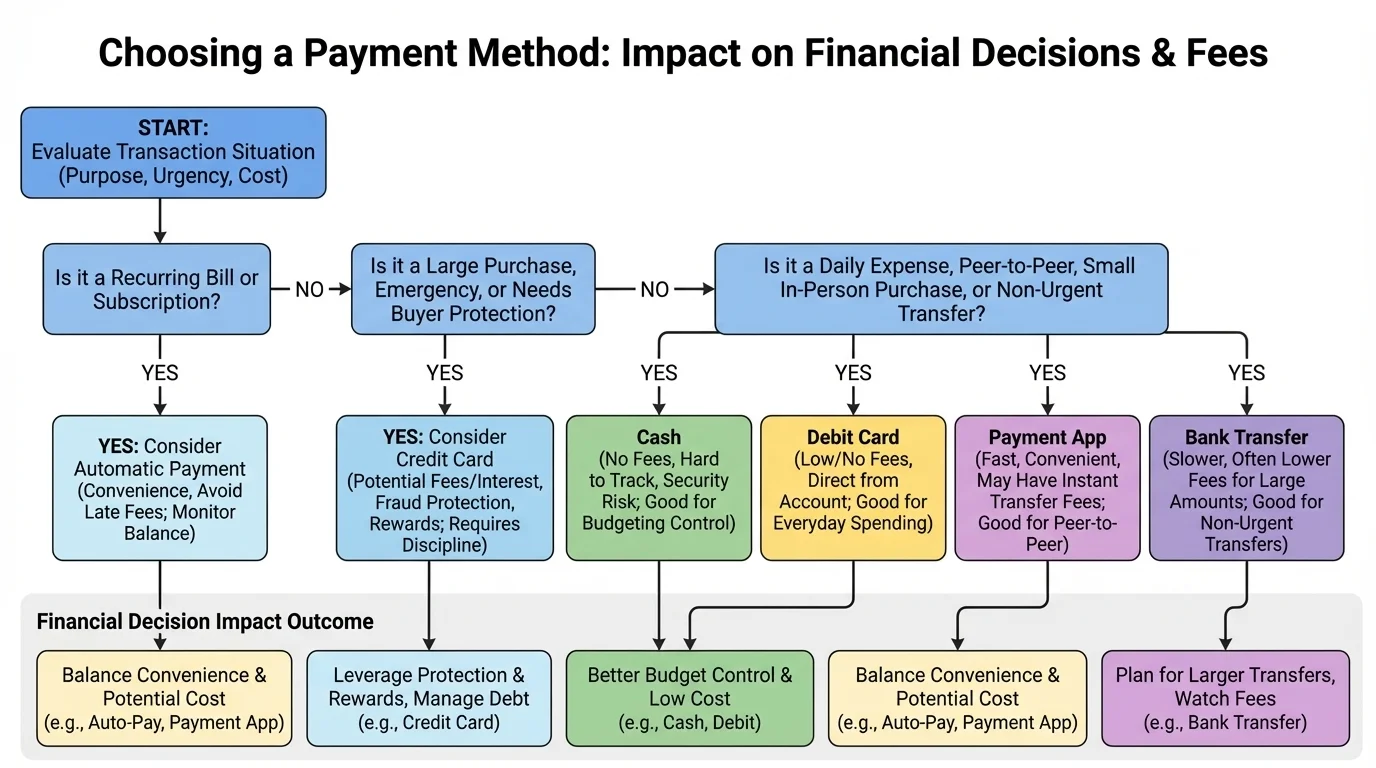

There is no single "best" payment method for every situation. The best choice depends on speed, safety, cost, and whether the money is already in your account. That decision process appears clearly in [Figure 2], because a smart payment choice depends on the situation, not just convenience.

Debit card payments pull money directly from your checking account. This can help you avoid debt, but only if you keep track of your balance. If you spend more than you have, you could trigger an overdraft or a declined payment. A debit card is often useful for everyday purchases when you already have enough money in your account.

Credit card payments borrow money that must be paid back. Credit cards can offer fraud protection and may help build credit history later in life, but they are risky if you spend more than you can repay. For a ninth grader, the key idea is this: credit can make buying feel easy, but the money is not free.

Cash can be useful because it is simple and immediate. You can physically see how much is left. That can help with self-control. But cash can be lost, stolen, or harder to use for online purchases. Bank transfer payments are common for moving money between accounts or paying certain bills. Payment apps can be fast and convenient, but they may have transfer delays, instant-transfer fees, or scam risks if you send money to the wrong person.

Automatic payment means a payment is scheduled to happen on its own, often for subscriptions or monthly bills. This can prevent missed payments, but it can also cause problems if you forget a subscription is active or if your account balance is too low when the payment goes through.

Checks are used less often than in the past, but they still exist. Some landlords, organizations, or businesses may use them. Checks can be useful, but they are slower than digital methods and need careful handling.

Real-life choice: paying for a music subscription

You want a streaming subscription that costs $11.99 per month.

Step 1: Think about convenience

Automatic payment is easy because the bill is handled for you each month.

Step 2: Think about account balance

If your account has only $8 when the charge happens, the payment may fail or trigger a fee.

Step 3: Think about control

Using a debit card and checking your balance before renewal gives more control, especially if your income changes from month to month.

The best method is not always the fastest one. It is the one that fits your money situation without creating extra cost.

As the choices in [Figure 2] make clear, the payment method should match the purpose. Fast is helpful, but not if the fast option adds unnecessary fees or risk.

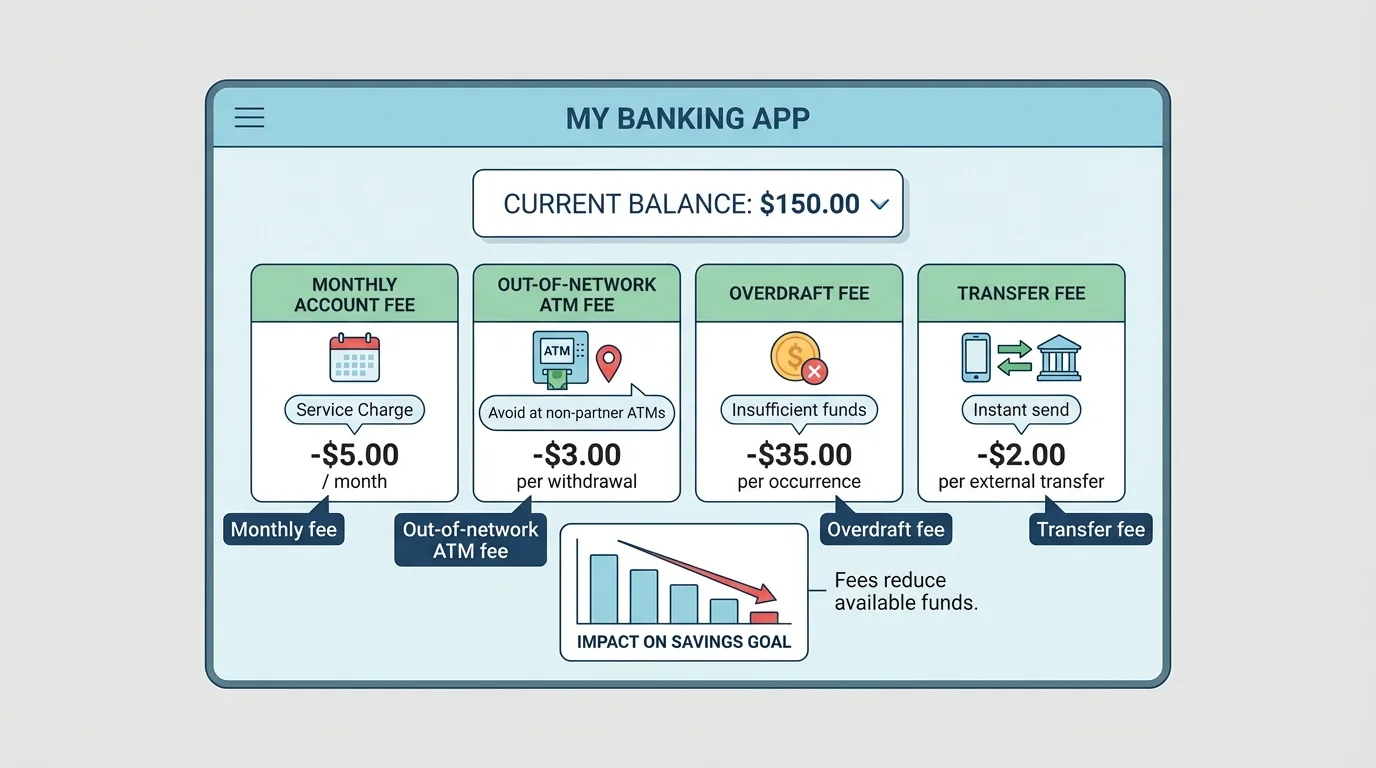

A fee is money charged for a service, action, or rule violation. Small fees matter because they often repeat. [Figure 3] illustrates how different fees can show up during normal account use, even when each one looks minor by itself.

One common fee is a monthly maintenance fee. This is a charge some banks apply each month just for having the account, unless you meet certain conditions such as keeping a minimum balance or receiving direct deposit. A $10 monthly fee may not sound huge, but over a year that becomes \(10 \times 12 = 120\). That is $120 gone without buying anything.

Another important fee is the overdraft fee. An overdraft happens when you spend more money than you have available. Some banks may cover the transaction and then charge a fee. Others may decline the transaction. Either way, overspending creates trouble. There are also nonsufficient funds fees, often called NSF fees, if a payment cannot go through because there is not enough money.

ATM fees happen when you use an ATM outside your bank's network. Transfer fees may apply when sending money quickly or using certain services. Some accounts charge fees for paper statements, replacement cards, or international purchases. Some payment apps charge for instant transfers. A choice that seems convenient in the moment may cost extra later.

The reason banks can feel confusing is that fees are often hidden in long lists of details. You have to look for them on purpose. The good news is that once you know the common fee types, you can spot warning signs quickly.

| Fee type | What triggers it | Why it matters |

|---|---|---|

| Monthly maintenance fee | Having the account without meeting waiver rules | Repeated cost every month |

| Overdraft fee | Spending more than available balance | Can make a small mistake expensive |

| ATM fee | Using an out-of-network ATM | Adds cost just to access your own money |

| Instant transfer fee | Moving money immediately through an app or service | Convenience costs extra |

| Foreign transaction fee | Purchases in another currency or country | Raises total purchase cost |

Table 1. Common banking and payment fees, their triggers, and why they affect financial decisions.

Think about a small emergency. You need $40 right away, use an out-of-network ATM, and pay $5.50 in combined fees. The total cost of accessing your own money becomes \(40 + 5.50 = 45.50\). That is a strong reminder that convenience has a price.

Fees do not just reduce your balance. They also change what choices are smartest. Suppose two payment options let you buy the same item. Option A is a payment app with an instant transfer fee of $1.75. Option B is a standard bank transfer with no fee but takes one business day. If the item is not urgent, waiting may be the better financial choice.

Here is another example. You want to keep $50 in your account, but your bank charges a $12 monthly fee unless your balance stays at $500 or more. If you cannot realistically keep $500 there, that account may be a poor match for your situation. The issue is not whether the bank is "good" or "bad." The issue is whether the account works for you.

Total cost matters more than sticker price

When you compare financial choices, include all extra charges. A payment method or bank service may look convenient, but the real question is: what is the full cost after fees, delays, and risks are included? Smart decisions come from comparing the complete picture, not just the first number you see.

Suppose you buy something online for $24. If your payment app pulls from a low-balance account and causes a $35 overdraft fee, the actual cost connected to that purchase becomes \(24 + 35 = 59\). The purchase did not change, but the financial decision got much more expensive because the payment method did not fit your account balance.

On the other hand, making careful choices can protect your money. Setting low-balance alerts, keeping a small cushion in checking, using in-network ATMs, and reviewing account terms can prevent many common costs.

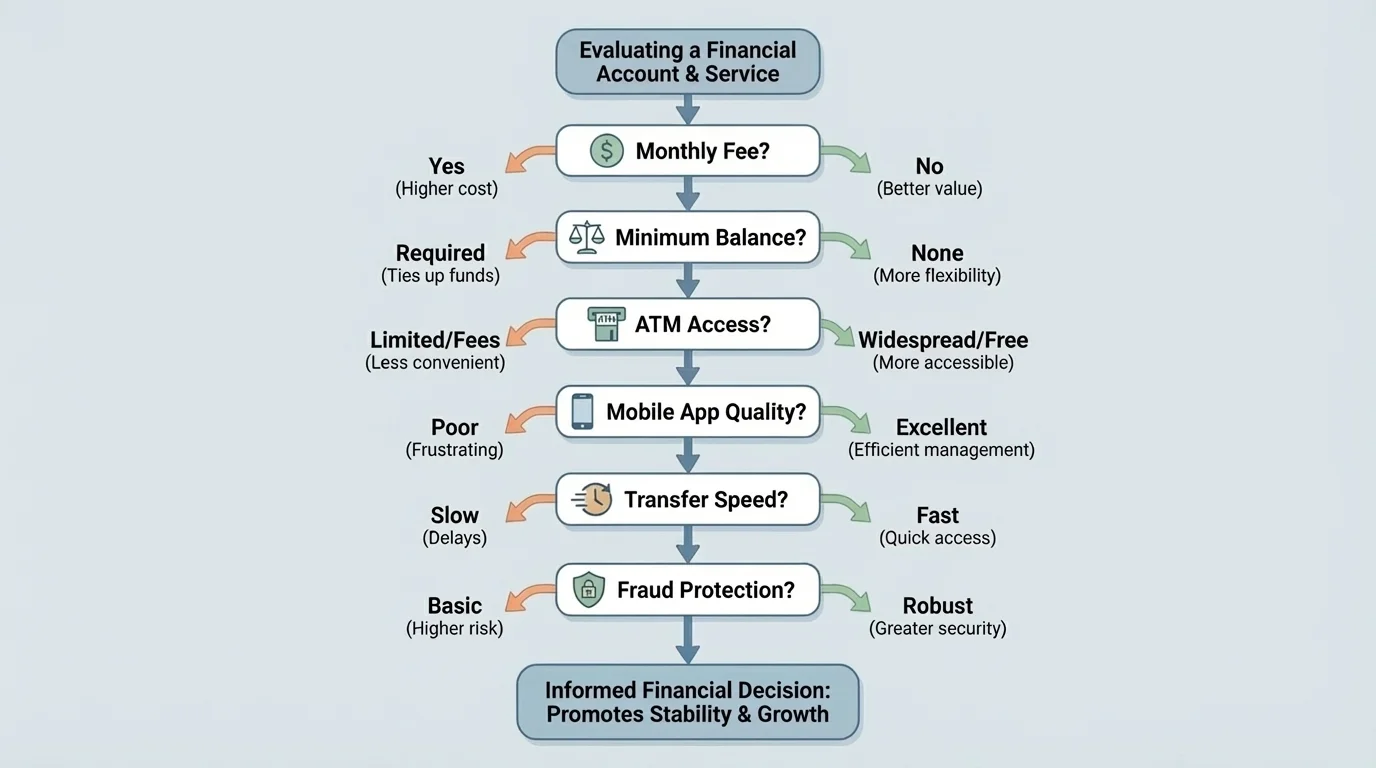

When comparing accounts, do not focus only on ads or app design. Compare features one by one, as [Figure 4] shows. A smart comparison looks at fees, access, limits, and protections together.

Ask yourself practical questions. Does the account charge a monthly fee? Is there a minimum balance requirement? Are there enough nearby or convenient in-network ATMs? Does the app let you check your balance quickly? Are there alerts for suspicious activity? Can you transfer money easily without paying extra?

Also think about your habits. If you often use cash, ATM access matters more. If you buy online, fraud protection and card controls matter more. If your income is irregular, an account with no minimum balance and no monthly fee may be safer. If you are saving for a goal, a separate savings account can help keep that money out of your everyday spending.

A good decision framework is simple:

Step 1: Identify how you actually use money.

Step 2: List the services you need most.

Step 3: Check all likely fees.

Step 4: Compare at least two options.

Step 5: Choose the option that gives the needed services at the lowest realistic cost.

This is where [Figure 4] stays useful. It reminds you that the best financial product is not the most popular one. It is the one that fits your real behavior and reduces unnecessary costs.

Comparing two accounts

Account A has no monthly fee, but charges $3 per out-of-network ATM use. Account B charges $8 per month, but includes many in-network ATMs near your home.

Step 1: Estimate your habits

Suppose you use an out-of-network ATM about \(3\) times per month.

Step 2: Find the monthly cost of Account A

ATM fees would be \(3 \times 3 = 9\), so the monthly extra cost is $9.

Step 3: Compare with Account B

Account B costs $8 per month.

In this situation, Account B may actually be cheaper, even though its monthly fee looks worse at first.

That example shows why details matter. The cheapest-looking option on paper is not always the cheapest option in real life.

Convenience should never replace safety. Digital banking is useful, but it also means you need strong habits. Use unique passwords, turn on account alerts, and avoid sharing login information. If someone asks you to send money immediately through a payment app, stop and verify first. Scams often create fake urgency.

Fraud is any dishonest trick used to steal money or financial information. This can happen through fraudulent emails, text messages, fake job offers, or messages pretending to be from a bank. If a message says your account is "locked" and tells you to click a link fast, go directly to the bank's real app or website instead of trusting the message.

Good money management is not only about earning and saving. It is also about protecting what you already have. A secure account with strong habits can prevent losses that a budget alone cannot fix.

Check your account activity regularly. If a charge looks wrong, report it quickly. The sooner you act, the better the chance of stopping further problems. This habit also helps you notice forgotten subscriptions and repeated charges.

Be careful with automatic payments. They are helpful for bills you truly need and can reliably afford. They are less helpful for free trials, entertainment subscriptions you rarely use, or anything you might forget to cancel.

You do not need to be an expert. You just need a checklist and a habit of slowing down before agreeing to something financial.

First, read the fee list. Look for monthly fees, ATM fees, overdraft rules, transfer charges, and minimum balance requirements.

Second, check access. Make sure the account has ATMs, app features, and customer support that fit your needs.

Third, review safety tools. Look for alerts, card locking, transaction monitoring, and clear fraud reporting steps.

Fourth, think about your patterns. Are you likely to keep enough money in the account? Will you need fast transfers often? Do you shop online a lot? Your real habits should guide your choice.

Fifth, avoid signing up just because of a promotion. A free gift or cash bonus can sound exciting, but if the account has ongoing fees, the deal may not really help you.

"The best financial choice is often the one that costs the least over time, not the one that feels easiest right now."

Try This: Look at one bank account or payment app you already use, or one an adult in your household is willing to show you. Find the fee section and identify at least three possible charges. Then ask which of those charges are easy to avoid and how.

Try This: Before your next online purchase, pause and ask: Which payment method is safest? Which one is fastest? Which one is cheapest? If those answers are different, decide which matters most for that purchase.

Try This: Set a simple rule for yourself, such as "I will check my balance before any online purchase" or "I will not keep subscriptions on automatic renewal unless I use them every month." Small rules can prevent expensive mistakes.