Here's a surprising truth: a lot of the money you use in daily life never feels like "tax money," but taxes are quietly behind many things you probably count on every week. The road your family drives on, the firefighters who respond in emergencies, the public library, city parks, public health programs, and many community services are paid for in part by taxes. If you get your first job, taxes suddenly become personal because they show up on your paycheck, affect how much money you actually take home, and can change the way you budget for everything from streaming subscriptions to saving for a car.

Taxes can feel confusing at first because the words sound official and adult: withholding, deductions, refund, return, taxable income. But the basic idea is simple. Governments collect money from people and businesses to pay for things the public uses together. At the same time, your own tax situation affects your spending, your savings, and how you plan ahead. Understanding that connection makes you more confident with money.

Taxes are required payments collected by governments to fund public services and government operations.

Income is money you earn from work, jobs, tips, or other sources.

Income tax is a tax charged on money a person earns.

Public services are services provided for the community, such as roads, emergency response, and public health programs.

Even if you do not earn a full-time paycheck yet, this topic matters now. You may babysit, mow lawns, sell handmade items online, or work a part-time job. The choices you make with your money work better when you understand the difference between what you earn and what you keep.

Taxes exist because some services are too big, too shared, or too important to depend on one person paying for them alone. If every family had to build its own road, hire its own firefighter team, or run its own water testing system, life would be far more expensive and chaotic. Taxes pool money so communities can pay for shared needs together.

Think of taxes as part of the way a society organizes responsibilities. When people contribute, governments can maintain systems that support daily life, public safety, and long-term growth. That does not mean every person agrees on every tax decision, but it does explain the main purpose: funding things that help the public as a whole.

There are different kinds of taxes, including income taxes, sales taxes, and property taxes. In this lesson, the main focus is on income tax because that is the tax most directly connected to your paycheck and personal financial planning.

Shared costs, shared benefits

One of the most useful ways to understand taxes is to ask, "What services would be hard to organize fairly without them?" Street lighting, public parks, emergency dispatch systems, and road repairs benefit many people at once. Taxes help spread those costs across a large group instead of leaving each person to solve the problem alone.

When taxes are managed well, communities can function more smoothly. When tax systems are misunderstood, people may make poor money choices because they plan based on the wrong number or ignore responsibilities they will still have to pay later.

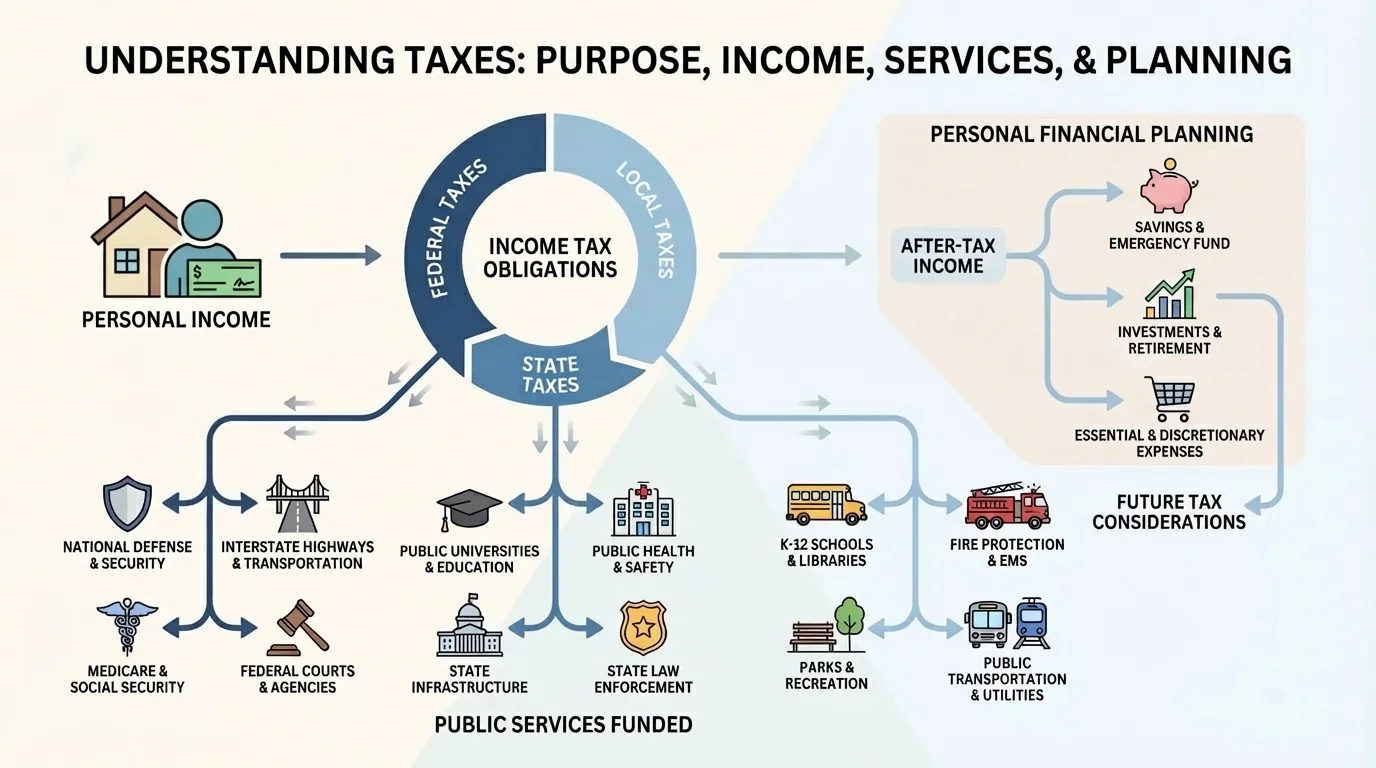

Tax money supports many different services at the same time, as [Figure 1] shows through a simple map of shared spending. One tax system does not pay for only one thing. Instead, collected money is used for many public needs, including transportation, safety, health programs, and community spaces.

Some taxes are collected by the federal government, some by state government, and some by local government. The exact system depends on where you live, but the big idea stays the same: taxes help pay for services people use individually and collectively.

| Level of government | Examples of services |

|---|---|

| Federal | National defense, interstate systems, some public health programs |

| State | State roads, some education funding, state parks |

| Local | Police, firefighters, local libraries, trash collection, community recreation |

Table 1. Examples of public services that may be funded by taxes at different levels of government.

When people complain that taxes "disappear," they usually mean the process feels invisible. But the results are often visible every day: repaired streets, traffic signals, emergency responders, public buildings, and health inspections. Understanding this helps you see taxes as more than just money taken out of a paycheck.

Later, when you start making choices about jobs, savings, and living expenses, this connection matters. You are not only paying for personal obligations; you are also participating in a system that supports community services. That is one reason taxes are often discussed as both a financial issue and a civic responsibility.

If you earn money from a job, that money is called earned income. Before you get your full paycheck amount, part of that income may be taken out for taxes. This process is often called withholding, which means money is held back from your paycheck and sent toward your tax obligation.

Two important paycheck ideas are gross pay and net pay. Gross pay is the total amount you earned before taxes and other deductions. Net pay is what you actually receive after those amounts are taken out. If you work for $15 per hour for 8 hours, your gross pay is \(15 \times 8 = 120\), so you earned $120 before deductions. Your net pay will be less than $120 if taxes are withheld.

That difference matters a lot in real life. If you get excited about your gross earnings and make plans based on that number, you might overspend. Your budget should be based on net pay, not gross pay, because net pay is the amount you can actually use.

Paycheck example

You work 10 hours in one week at $14 per hour.

Step 1: Find the gross pay.

Multiply the hourly wage by the hours worked: \(14 \times 10 = 140\).

Step 2: Estimate taxes withheld.

Suppose $18 is withheld for taxes and payroll-related deductions.

Step 3: Find the net pay.

Subtract deductions from gross pay: \(140 - 18 = 122\).

Your gross pay is $140, but your take-home pay is $122.

Notice what this means for planning. If you want to save half of that week's paycheck, saving half of gross pay would be $70, but saving half of net pay would be \(122 \div 2 = 61\), or $61. The second number is the one that fits real life.

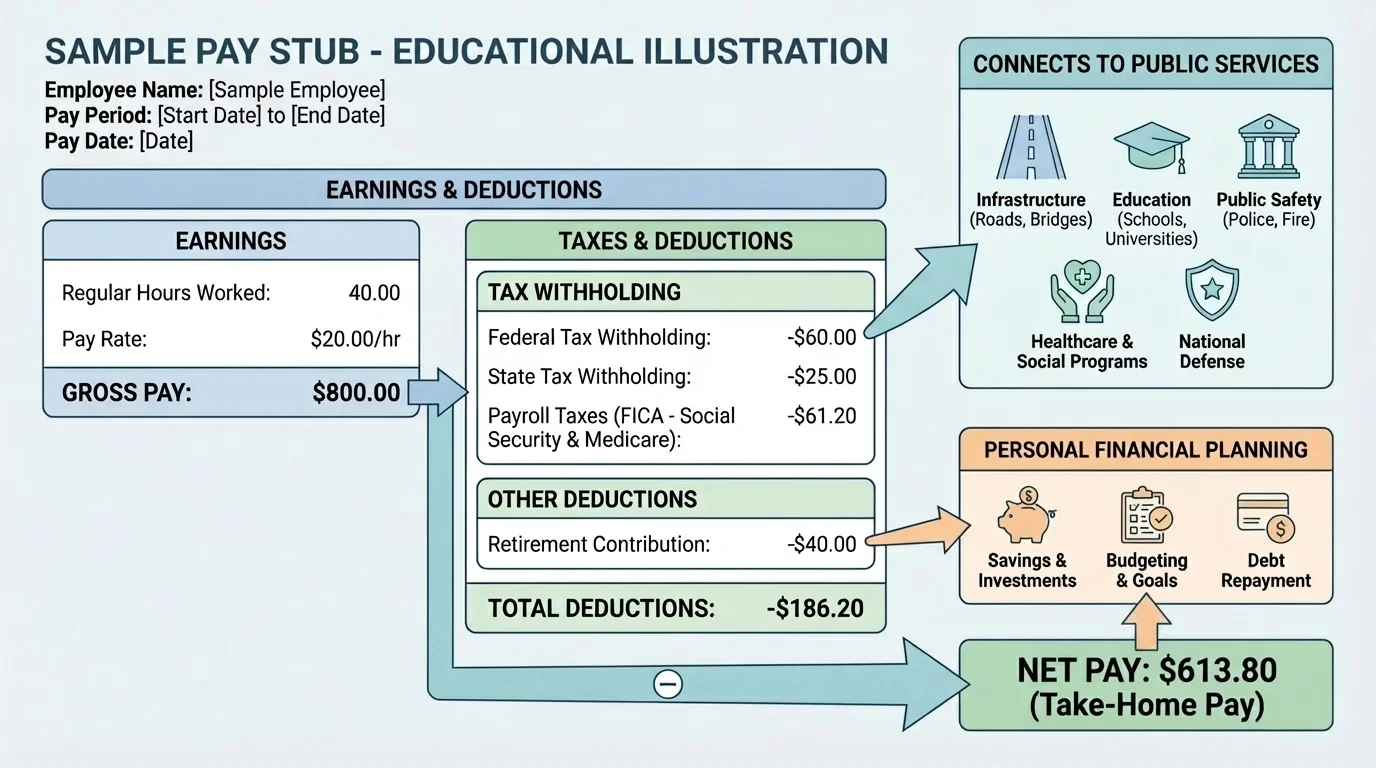

Your pay stub is a record that explains where your paycheck money goes, and [Figure 2] breaks this down visually. It usually lists hours worked, pay rate, gross pay, taxes withheld, and net pay. If you ever look at a deposit and think, "Why is this less than I expected?" the pay stub is where you check.

A pay stub may also show other deductions besides income tax. Depending on the job and the situation, it could include other payroll taxes or optional deductions. At your age, the exact details may vary, but learning to read the categories is a valuable life skill.

Some key terms are worth knowing. A deduction is an amount subtracted from your pay. Tax withholding is one kind of deduction. The important habit is to compare what you expected to earn with what you actually received and understand the reason for the difference.

Checking a pay stub helps you catch mistakes early. Maybe your hours were entered incorrectly. Maybe your pay rate was wrong. Maybe you assumed your first job would pay you the same amount you saw in the job ad, but you forgot to account for taxes. The pay stub turns your paycheck from a mystery into information you can use.

That matters later too. If you apply for an apartment, set a savings goal, or compare jobs, you need a realistic picture of your take-home pay. As we saw with the labeled breakdown in [Figure 2], the top number is not the same as the money available to spend.

Many workers file a tax return. A tax return is paperwork submitted to report income and calculate whether the correct amount of tax was paid during the year. For many people, the government compares what was already withheld from paychecks with what they actually owed.

A tax refund happens when too much tax was paid during the year, so some money is sent back. Owing money means not enough tax was paid during the year, so the person still has to pay the difference. A refund is not "bonus money." It is your own money being returned because too much was taken out earlier.

This idea is important because people sometimes treat a refund like free cash and spend it too quickly. A smarter way to think about it is this: if a refund arrives, decide on purpose what it should do. You might save part, pay off something, or put it toward a goal like a laptop or emergency savings.

A big refund can feel exciting, but it often means you gave the government more of your paycheck during the year than necessary. Some adults prefer a smaller refund and slightly larger paychecks along the way, while others like the forced-savings feeling of a refund.

For a teenager with a first job, the exact filing rules may depend on how much money was earned and the kind of work done. The practical lesson is simple: keep records, save tax documents, and ask a trusted adult or tax professional when you are unsure.

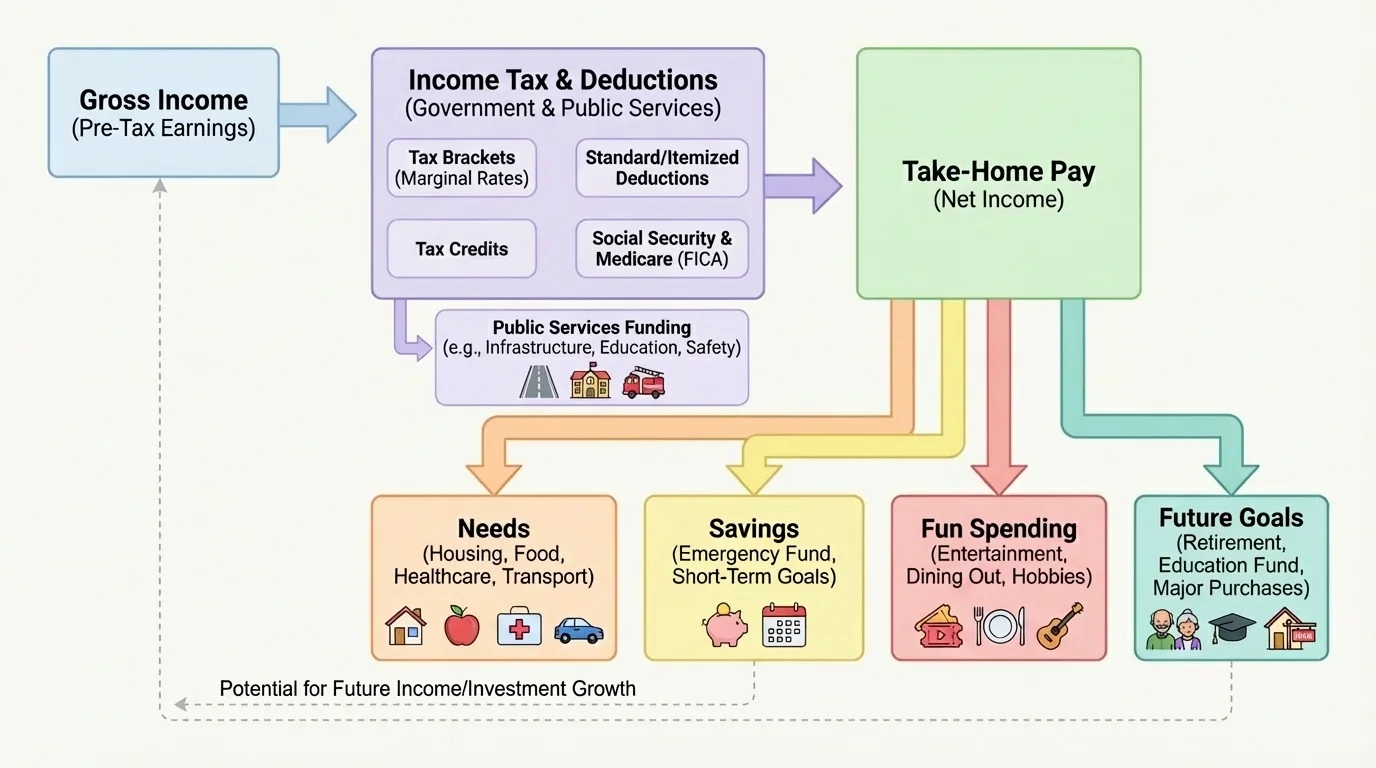

Taxes matter in personal money decisions because budgeting starts with the money that actually reaches you, and [Figure 3] shows how take-home pay can be split into spending, saving, and goals. If you plan with the wrong number, your whole budget can fall apart.

Suppose you expect to earn $300 from part-time work over two weeks. If taxes and deductions reduce that amount to $255, then $255 is the number your budget should use. If you try to spend the full $300, you are planning with money that is not available.

Here is a simple way to think about it. Start with net pay. Then divide it into categories that match your life: needs, savings, fun spending, and future goals. For example, if your net pay is $255, you might choose to save $100, spend $60 on personal needs, use $35 for entertainment, and keep $60 for a larger goal. The math is \(100 + 60 + 35 + 60 = 255\).

This is where taxes connect directly to smart planning. You cannot control every deduction, but you can control how carefully you plan the money left after taxes. That skill helps whether you are saving for headphones, building an emergency cushion, or comparing two part-time job options.

Budgeting with net pay

A student earns $180 in gross pay from a weekend job. After $22 is withheld, the take-home pay is $158.

Step 1: Find the usable amount.

Subtract withheld taxes: \(180 - 22 = 158\).

Step 2: Set a savings goal.

If the student wants to save 25% of take-home pay, calculate \(158 \times 0.25 = 39.5\), so about $39.50.

Step 3: Plan the rest.

The remaining amount is \(158 - 39.5 = 118.5\), so $118.50 can be divided among other needs and wants.

The key is that the plan uses take-home pay, not gross pay.

This also affects long-term choices. If one job pays slightly more per hour but has inconsistent hours, and another job pays a bit less but gives steady hours, you might prefer the predictable income because it makes budgeting easier. Taxes do not make that decision for you, but they are part of the realistic money picture.

Money earned from informal jobs can still create tax responsibilities. If you babysit occasionally for cash, the situation may be simple. If you regularly earn money from online sales, content creation, tutoring, lawn care, or pet sitting, keeping records becomes very important. The more organized you are, the less stressful tax time becomes later.

A good system can be simple. Save pay stubs digitally. Keep a note on your phone or in a spreadsheet with dates, amounts earned, and where the money came from. If you spend money directly related to earning that income, record that too if it matters for your situation. Organization is a financial skill, not just a paperwork skill.

Plan for taxes before you spend

If money comes from side work instead of a regular paycheck, taxes may not automatically be withheld. That means more of the money arrives in your hands right away, but it does not always mean all of it is yours to spend. Setting some aside early can prevent a stressful surprise later.

A practical rule is to avoid treating every dollar earned as spendable. If you are unsure whether taxes will apply, be cautious and save part of what you earn until you understand your obligation better. That habit protects you.

Try This: The next time you earn money, write down three numbers: what you earned, what you actually received, and what you decided to save. That one-minute habit builds financial awareness fast.

One common mistake is confusing gross pay with net pay. Gross pay sounds bigger, so it is easy to build plans around it. But if your phone bill, savings target, and weekend spending all depend on money that gets withheld for taxes, you can end up short.

Another mistake is ignoring paperwork. If you lose tax forms, forget where income came from, or never read your pay stub, small problems can turn into bigger ones. It is much easier to store records as you go than to rebuild everything months later.

A third mistake is spending a future refund before it arrives. Some people mentally use refund money for purchases before they even file. That is risky because the amount may be smaller than expected, delayed, or unavailable.

"Don't plan your life around money you haven't actually received."

— A smart rule for budgeting

There is also a mindset mistake: thinking taxes are only a problem for adults. In reality, the earlier you understand paycheck basics, the stronger your money habits become. People who learn this young are often better at comparing jobs, saving consistently, and avoiding financial surprises.

Scenario one: You get a part-time job at a local store. Your first paycheck is smaller than expected. Instead of panicking, you check your pay stub, identify withholding, and adjust your budget. That is a smart response.

Scenario two: You earn money editing short videos for people online. Since no regular employer is withholding taxes for you, it is safer to save a portion of that money instead of spending all of it. This is one reason understanding taxes matters even in digital jobs.

Scenario three: You want to save $500 for a gaming system or a travel opportunity. If your take-home pay averages $125 per week and you save $50 weekly, the number of weeks needed is \(500 \div 50 = 10\). But that plan only works if the $125 figure is based on net pay, not your larger gross pay amount.

Comparing realistic job income

Job A pays $13 per hour for 12 hours each week. Job B pays $15 per hour for 10 hours each week.

Step 1: Find gross weekly pay for each job.

Job A: \(13 \times 12 = 156\). Job B: \(15 \times 10 = 150\).

Step 2: Estimate take-home pay.

If Job A has about $20 withheld, net pay is \(156 - 20 = 136\). If Job B has about $19 withheld, net pay is \(150 - 19 = 131\).

Step 3: Compare the useful amount.

Even though Job B has the higher hourly wage, Job A gives slightly more take-home pay each week in this example.

This shows why smart financial choices depend on the full picture, not just one number.

As your life gets busier and your money choices get bigger, taxes become part of nearly every important decision. They affect what lands in your account, what you can safely spend, how fast you can save, and how responsibly you handle income from jobs or side work. Understanding taxes does not just help you follow rules. It helps you make better decisions with your own money.

When you look again at the public-services chart in [Figure 1] and the budgeting flow in [Figure 3], you can see both sides of the topic at once: taxes support shared services, and taxes shape your personal financial plan. That is why learning about taxes is both a money skill and a real-world life skill.