Have you ever had just a little money and had to choose: buy something now or save it for later? That is a real money decision. Grown-ups make these choices, and children do too. When we learn how to sort money goals, we become better at choosing what matters most.

Money goals are plans for how to use money. A goal might be buying lunch, saving for a new book, or helping pay for a class trip. Some goals are more important than others. Some are needed right away, and some can wait. Learning to classify goals helps us think carefully before we spend.

People do not have unlimited money. That means we cannot always buy everything we want at the same time. We need to choose. When we choose one thing, we may have to wait for something else. This is why planning is important in personal financial literacy.

A financial goal is something a person wants or needs to do with money. A financial goal can be small, like saving $2 for a pencil topper, or larger, like saving $40 for a scooter helmet. The amount may change, but the idea is the same: we make a plan for money.

Financial goal means a plan for using money. Goals can be for things we need, things we want, things we will buy soon, or things we will save for over a longer time.

One helpful way to sort financial goals is by asking two questions. First, is it a need or a want? Second, is it short-term or long-term? These two questions help us understand what to do first.

Some money goals are for very important things. In daily life, as [Figure 1] shows, people often sort items into things they must have and things that are extra. A need is something important for living, learning, health, or safety.

Food, water, a warm coat in winter, school supplies, and medicine are examples of needs. These are things people should get before spending money on extra items. Needs help keep us safe, healthy, and ready to learn.

A want is something we would like to have, but we can live without it. Wants can still be fun, useful, and enjoyable. A new toy, a fancy sticker set, extra dessert, or a video game may be wants.

Sometimes a thing can seem tricky to classify. For example, shoes are usually a need because feet need protection. But a second pair of sparkling shoes that is not necessary might be a want. This shows that classifying goals means thinking about the situation.

How needs and wants help us decide

When money is limited, needs usually come first. Wants can be chosen after needs are met. This does not mean wants are bad. It means we should think carefully about what is most important right now.

If a child has $10 and needs notebooks for school that cost $6, buying the notebooks first may be the better choice. Then the child can think about using the remaining $4 for something else or saving it. We can describe that amount using subtraction: \(\$10 - \$6 = \$4\).

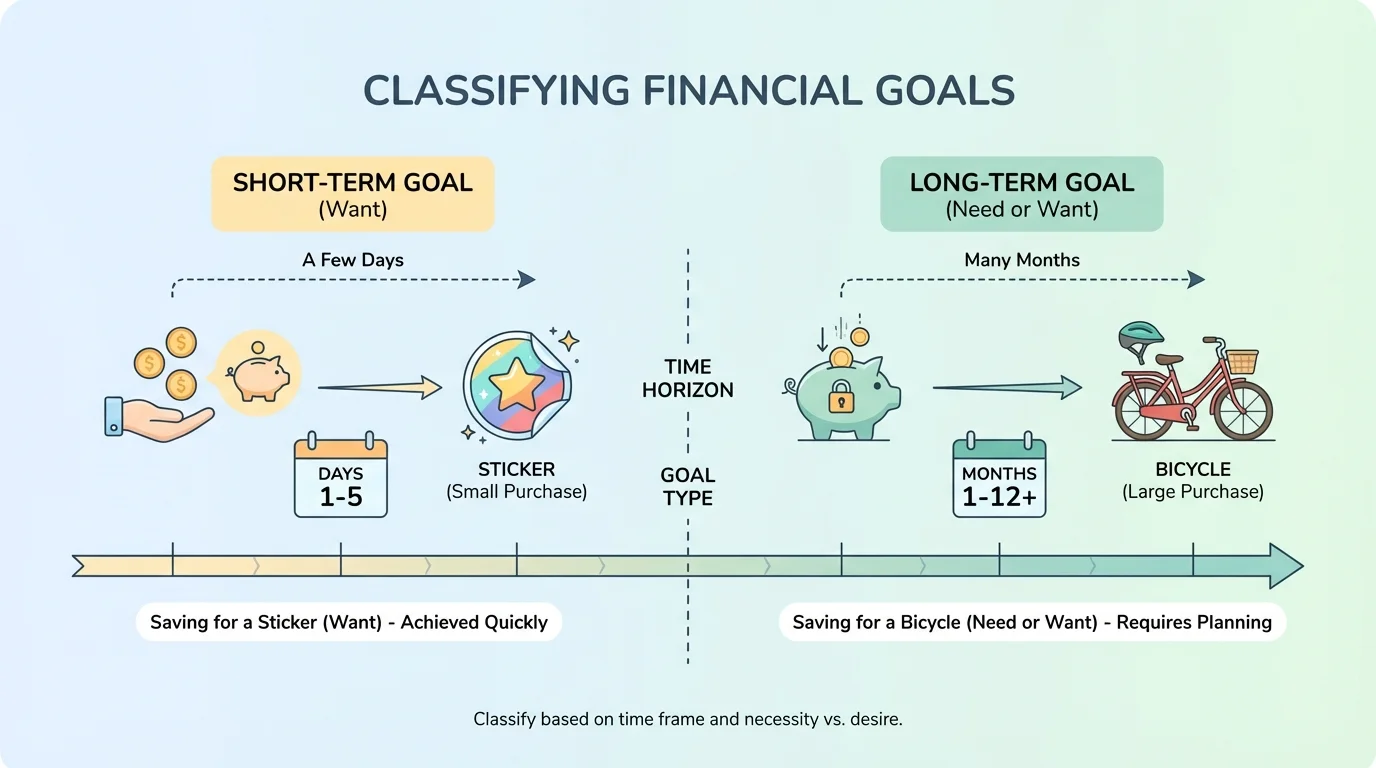

Money goals can also be sorted by time. As [Figure 2] illustrates, some goals happen soon, while others take much longer. A short-term goal is a goal you can reach in a short time, such as in a day, a week, or a few weeks.

Saving for a snack at the school store, a small toy, or a birthday card can be short-term goals. These goals usually cost less money, so it takes less time to save for them. A child might save $1 each week and reach a $3 goal in 3 weeks.

A long-term goal is a goal that takes more time. It may take many weeks, months, or even longer. Long-term goals often cost more money or need more planning.

Examples of long-term goals include saving for a bicycle, a tablet case, sports equipment, or a special trip. If a bike costs $60 and a child saves $5 each week, it will take many weeks to reach the goal. That waiting can be hard, but saving little by little helps.

Short-term goals and long-term goals are both important. A short-term goal can give a quick reward. A long-term goal can help us get something bigger or more meaningful later. Looking back at [Figure 2], the timeline makes it easier to see why larger goals usually need patience.

Many strong savers do not start with big amounts of money. They often reach goals by saving small amounts again and again over time.

Time changes our choices. If you spend all your money today on a want, you may have less money for a long-term goal tomorrow. That is why it is smart to stop and think before spending.

A financial goal does not belong in only one group. It can fit in two groups at the same time. For example, buying toothpaste can be a need and a short-term goal. Saving for a winter coat can be a need and a long-term goal if the money must be saved over many weeks.

Buying a stuffed animal might be a want and a short-term goal if it costs a small amount and can be bought soon. Saving for a game system might be a want and a long-term goal if it costs a lot and takes many months to save for.

These combinations help us classify goals clearly:

| Goal | Need or Want? | Short-Term or Long-Term? |

|---|---|---|

| Lunch at school | Need | Short-term |

| New crayons for class | Need | Short-term |

| Warm winter boots | Need | Long-term |

| Sticker pack | Want | Short-term |

| Bicycle | Want | Long-term |

Table 1. Examples of financial goals classified by importance and time.

Classifying goals this way helps us compare them. If we have to choose between a need and a want, the need often comes first. If we have to choose between a short-term want and a long-term need, we may decide to save for the need.

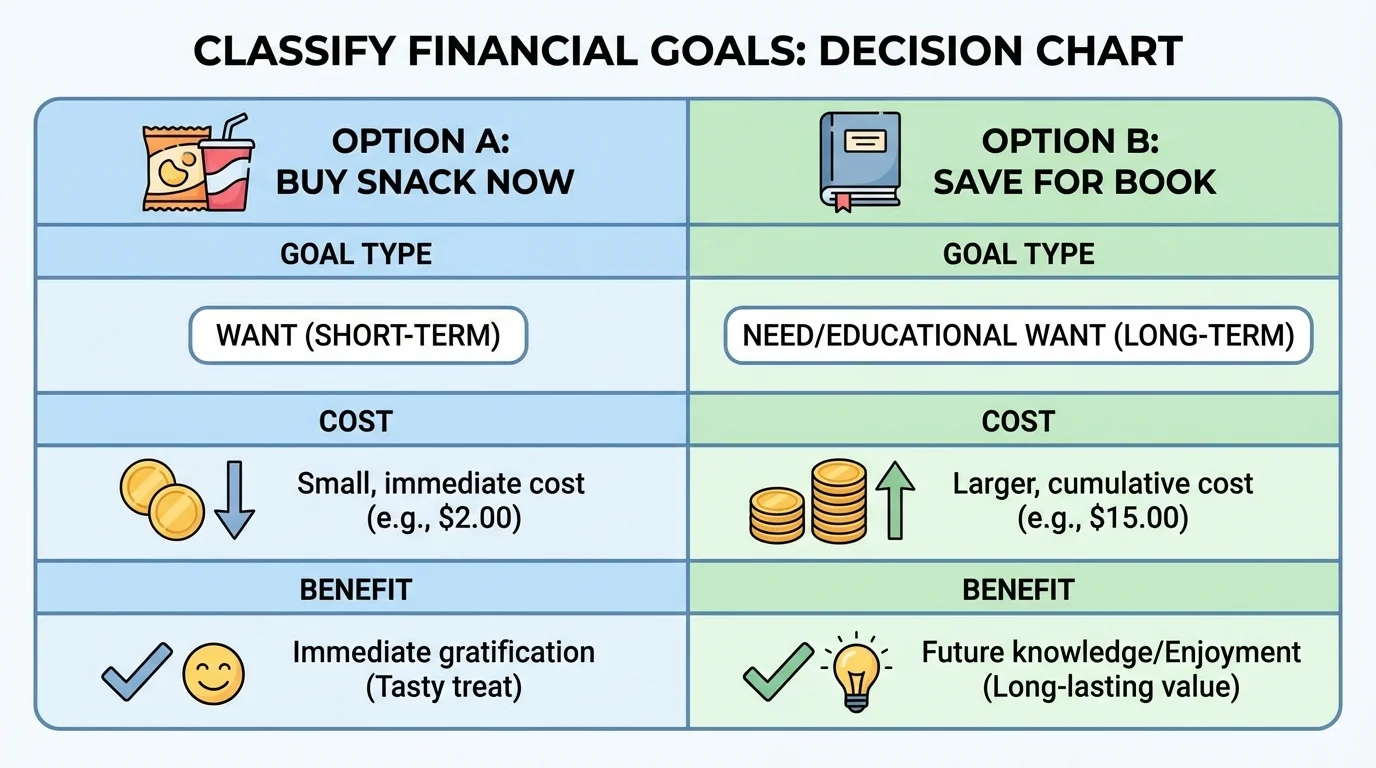

As [Figure 3] shows, when people make money choices, they think about what they give up and what they gain. A cost is what you give up, such as money spent or a choice you cannot make because you picked something else. A benefit is the good thing you get from a choice.

Suppose you have $5. You can buy a snack now for $5, or you can save the $5 toward a $12 book. The benefit of buying the snack is enjoying it right away. The cost is that the $5 is gone, so you are no longer closer to getting the book.

If you save the $5 instead, the benefit is that you are closer to the book. The cost is that you must wait and not have the snack now. Neither choice is magic. Each choice has something good and something you give up.

Example: Comparing two choices

Lena has $8. She wants a toy ring that costs $8, but she also needs glue for a school project that costs $3.

Step 1: Classify each goal

The glue is a need. The toy ring is a want.

Step 2: Think about cost and benefit

If Lena buys the ring, the benefit is having the toy now. The cost is not having money left for the glue.

Step 3: Make an informed choice

If Lena buys the glue first for $3, she still has $5 left because \(\$8 - \$3 = \$5\).

Buying the need first helps Lena finish her school project and still keep some money.

As we saw in [Figure 3], a good money decision is not only about what looks fun first. It is also about thinking ahead and understanding both costs and benefits.

An informed decision is a choice made after thinking carefully. To make an informed decision, ask simple questions: Is this a need or a want? Do I need it soon, or can it wait? What do I gain? What do I give up?

These questions help children become thoughtful money users. They also help families talk about spending and saving in a calm, clear way. Good planning does not mean never buying fun things. It means making sure our choices fit our goals.

Remember: Saving means keeping money to use later instead of spending it now. Saving often helps people reach long-term goals.

Sometimes people divide money into parts. For example, if a child gets $9, the child might spend $4, save $3, and share or donate $2. Thinking about parts can help organize money choices and make goals easier to reach.

It can also help to talk with a trusted adult. Adults may know if something is a need now, a want for later, or a goal worth saving for. Working together can lead to better decisions.

Here are some real-life situations. A child wants colorful markers for art at home, but the family also needs soap. Soap is a need, so it should come first. The markers are a want, so they may need to wait.

Another child wants to save for a class fair ticket that costs $4 next week. That is a short-term goal because it will happen soon. A different child wants to save $30 for soccer shin guards by next season. That is a long-term goal because it takes longer to reach.

Sometimes two wants compete with each other. A child may want candy today and also want to save for a puzzle next month. In that case, thinking about cost and benefit helps. Buying the candy gives quick enjoyment, but saving may lead to a bigger reward later.

"A smart choice is made by thinking before spending."

When students learn to classify financial goals, they become better at planning, waiting, and choosing. They learn that needs and wants are different, and that some goals happen soon while others take time. They also learn that every money choice has costs and benefits.