Every single day, people make choices without even noticing how many there are. Should you buy a snack now or save your money for later? Should you spend your after-school time playing outside or finishing a project first? These may seem like small decisions, but each one has something hidden inside it: when you choose one thing, you give up something else. That "something else" is important, because it helps us understand whether a choice is wise.

A choice happens when a person picks one option from two or more possibilities. Some choices are easy, like picking a pencil color. Other choices are harder, like deciding how to spend allowance money or how to use free time. Choices matter because we cannot always have everything at once.

When you choose one option, you usually cannot choose another option at the same time. If you spend $5 on a comic book, you may not have that same $5 to spend on a game card. If you spend 30 minutes watching a show, you may not have those same 30 minutes for reading or practicing soccer. Learning to think about choices helps people become careful planners and smart decision-makers.

Your brain makes many decisions every day, but not all of them are equally important. Choices about money and time can affect what you are able to do later.

People often focus on what they are getting. That makes sense because the chosen item or activity is right in front of them. But smart thinkers also ask, What am I giving up? That question helps reveal the full cost of a choice.

When people study how choices work, they use the term opportunity cost. Opportunity cost is the best thing you give up when you make a choice. It is not every single thing you did not choose. It is the best other option that you did not take.

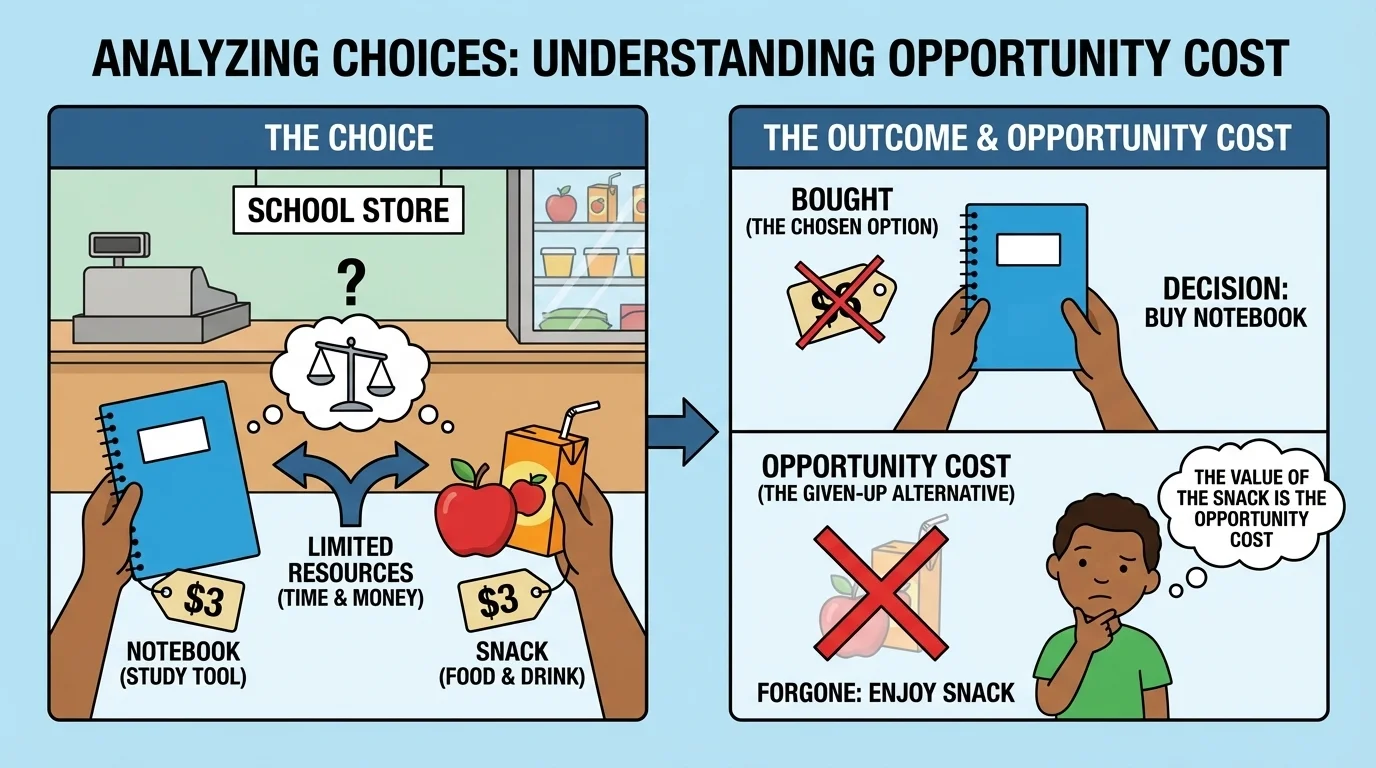

[Figure 1] For example, suppose a student has $3 at the school store. The student can buy a notebook for $3 or a fruit cup for $3. The student chooses the notebook. The opportunity cost is the fruit cup, because that was the best other option the student did not choose.

Opportunity cost is the best alternative that is given up when a choice is made.

Alternative means another option you could choose.

Benefit is something helpful or good that comes from a choice.

Notice something important: opportunity cost is not always about money. It can be about time, energy, or chances. If you choose to spend recess finishing unfinished classwork, the opportunity cost may be playing with friends. You gained one benefit, but you gave up another.

Opportunity cost also depends on what the person values most. One student may think a fruit cup is the best other option. Another may think the better option is saving the $3 for tomorrow. This means opportunity cost can change from person to person and from situation to situation.

Let us look at common situations. These examples help show that opportunity cost is part of normal life, not just something in a textbook.

Scenario 1: Mia has $10. She can buy a small art set for $10 or save the $10 toward a larger board game that costs $20. She chooses the art set today. Her opportunity cost is saving the money toward the board game. She gets the art set now, but gives up making progress toward the game.

Scenario 2: Jalen has one hour after school. He can practice piano or ride his bike. He chooses to practice piano. His opportunity cost is riding his bike. He gains music practice, but gives up bike time.

Scenario 3: Sofia brings $4 to a fundraiser. She can buy one cookie for $2 and save $2, or she can buy two cookies for $4. She chooses one cookie and saves $2. Her opportunity cost is the second cookie. She gains savings, but gives up eating another treat.

These situations show that opportunity cost is connected to the word alternative. In each scenario, there is another possible choice. To understand the opportunity cost, a person must think about the strongest alternative that was not chosen.

Earlier financial lessons may have introduced wants and needs. A need is something important for living and learning, such as food, clothing, or school supplies. A want is something you would like to have but can live without. Opportunity cost can help you compare wants and needs before spending money.

Sometimes the choice that feels most exciting right away is not always the best choice for the future. Looking at opportunity cost helps people slow down and think carefully before deciding.

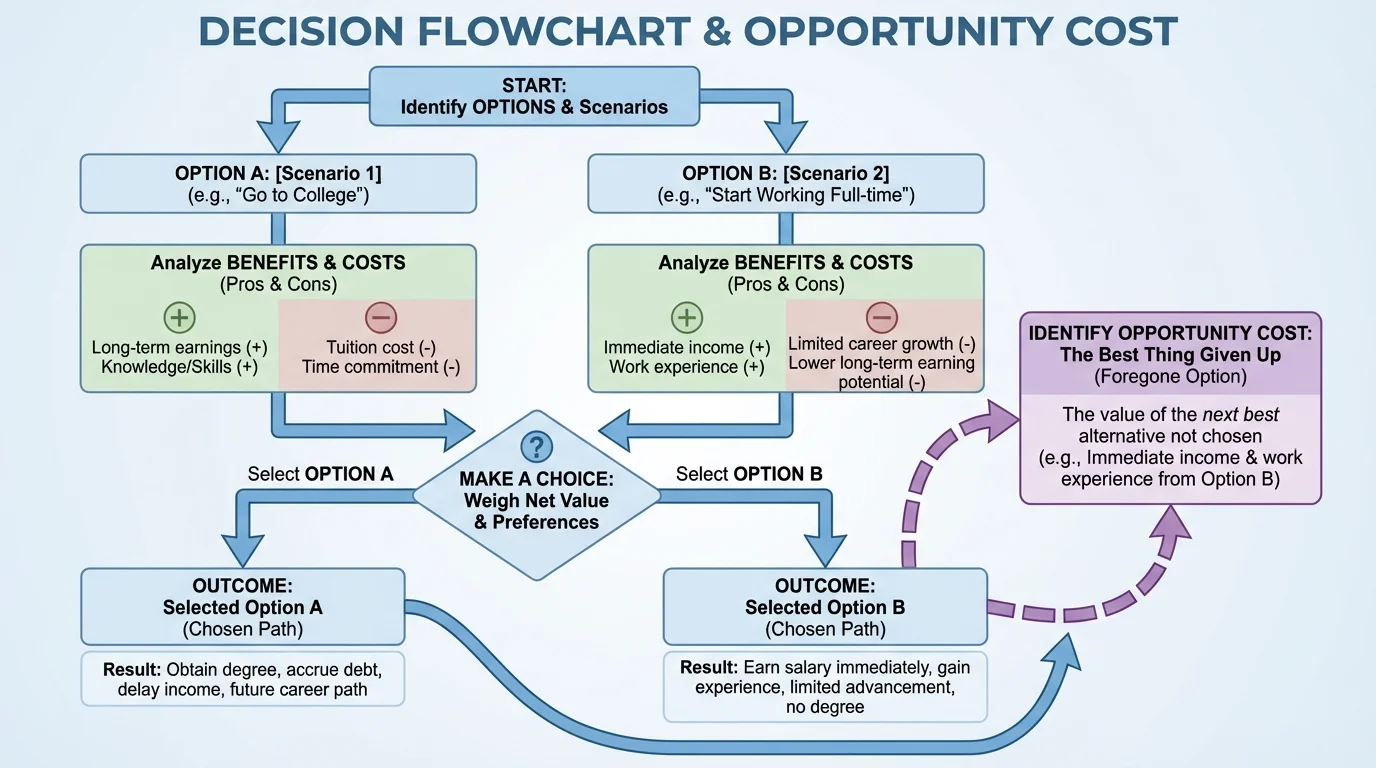

A good decision does not happen by magic. It can be studied step by step, and [Figure 2] illustrates a simple path from choices to opportunity cost. When students analyze a choice, they can ask a few important questions.

First, list the options. Second, think about what you gain from each option. Third, choose the option you think is best. Fourth, identify the best thing you gave up. That last part is the opportunity cost.

A simple way to analyze a choice

Ask: What are my options? What do I gain from each one? Which option do I choose? What is the best other option that I gave up? Answering these questions makes the opportunity cost easier to see.

Suppose you have enough money for only one item: a ruler, a colorful pen set, or a puzzle book. If you choose the ruler because you need it for class, then the opportunity cost is whichever of the other two choices was best for you. If the puzzle book was the option you wanted most after the ruler, then the puzzle book is the opportunity cost.

This method works for time choices too. If you can only do one activity before dinner, your options might be homework, basketball, or a video game. If you choose homework because it is due tomorrow, then the opportunity cost is the best of the other two options you gave up.

Opportunity cost becomes especially useful when money is limited. Most people do not have enough money to buy everything they want. That means they must compare choices carefully.

A careful spender often asks whether a purchase is a want or a need. Buying a folder for school may be a need. Buying a second pack of stickers may be a want. If you only have enough money for one, choosing the stickers means the opportunity cost might be the folder you need for class. That could create a problem later.

On the other hand, not every want is a bad choice. People can choose wants sometimes. The important idea is to understand what they are giving up. If you spend money on a want, you should know which need, saving goal, or other item may have to wait.

| Choice | What You Get | Possible Opportunity Cost |

|---|---|---|

| Buy a snack | A treat right now | Saving money for later |

| Buy school supplies | Items needed for class | A toy or treat |

| Save allowance | More money later | Something you could buy now |

| Spend all money today | Immediate enjoyment | Future choices with that money |

Table 1. Examples of choices, what is gained, and what may be given up.

The table shows that every option has a trade-off. A trade-off is when choosing one thing means losing another benefit. Opportunity cost helps us name the trade-off clearly.

Personal financial literacy means learning how to handle money wisely in everyday life. Students may not pay all household bills, but they still make money choices with allowance, gift money, fundraiser money, or school store money. Comparing these choices side by side makes it easier to spot what is gained and what is given up.

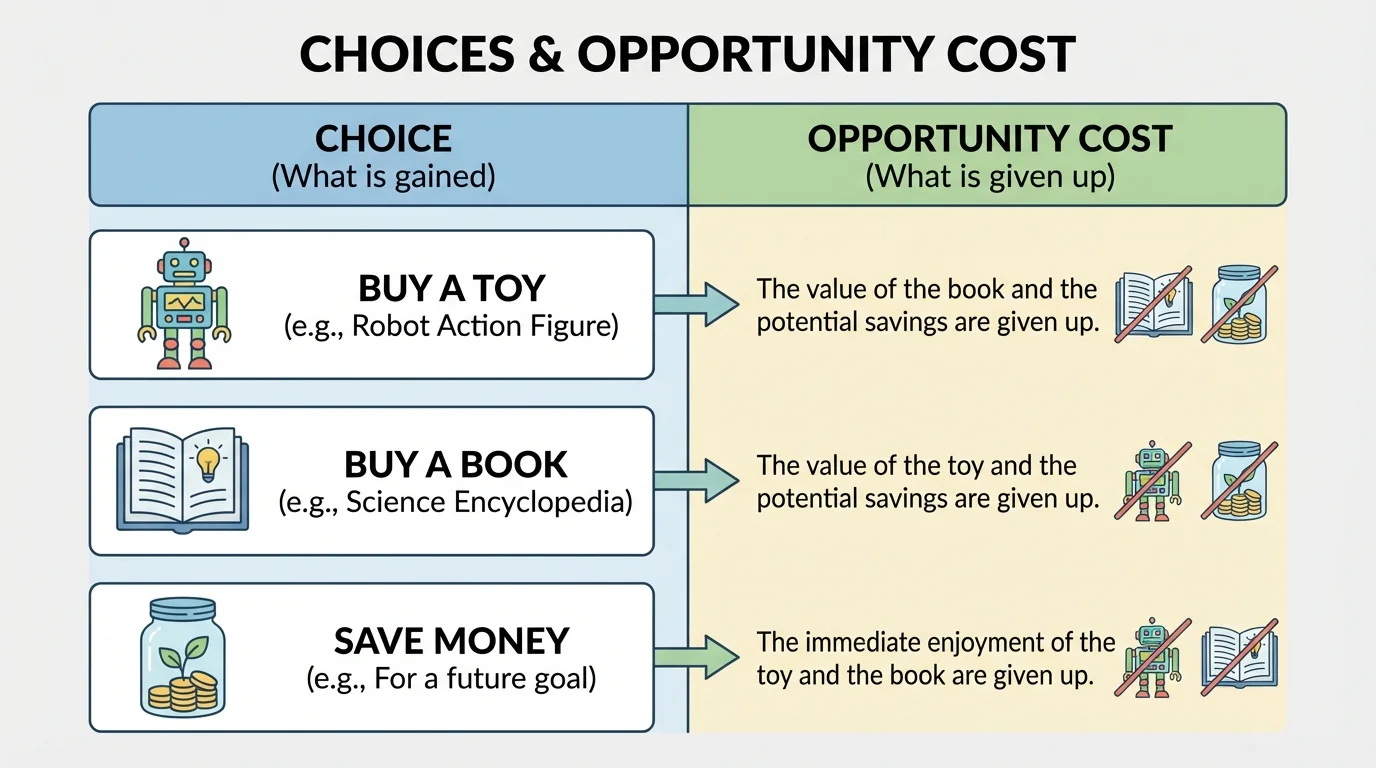

[Figure 3] Suppose a student receives $12. The student has three options: buy a toy for $12, buy a book for $8 and save $4, or save all $12. Each choice has a benefit. The toy gives quick fun. The book gives reading material and still leaves some money. Saving all the money helps with a future goal.

Worked example 1

Lena has $6. She can buy a bracelet for $6 or a puzzle magazine for $6. She chooses the bracelet.

Step 1: Identify the options.

The two options are a bracelet and a puzzle magazine.

Step 2: Identify the choice made.

Lena chooses the bracelet.

Step 3: Find the best other option not chosen.

The puzzle magazine is the best other option.

Step 4: State the opportunity cost.

The opportunity cost is the puzzle magazine.

Lena gains the bracelet, but gives up the puzzle magazine.

Now think about a saving decision. If a student decides not to spend money today, the opportunity cost is the best thing the student could have bought now. Saving is still often a wise choice, because the future benefit may be bigger than the current one.

Budgeting is another helpful idea. A budget is a plan for how money will be used. A budget helps people decide in advance what matters most. When someone follows a budget, they are often choosing to give up some smaller wants in order to reach a larger goal later.

Worked example 2

Marcus has $10 at a book fair. He can buy one poster for $10, or he can buy a bookmark for $2 and save $8. He chooses the bookmark and saves $8.

Step 1: List the main options.

Option A: one poster for $10. Option B: one bookmark for $2 and save $8.

Step 2: Identify what Marcus picked.

He chose the bookmark and saved $8.

Step 3: Determine the best alternative not chosen.

The poster was the best other option he gave up.

Step 4: Name the opportunity cost.

The opportunity cost is the poster.

Marcus chose to keep more money for later, but he gave up getting the poster now.

Opportunity cost is not only about money. Time is limited too. Every person gets the same number of hours in a day, so using time on one activity means not using it on another activity.

If you spend 20 minutes practicing free throws, the opportunity cost might be 20 minutes of drawing. If you read before bed, the opportunity cost might be extra game time. This does not mean the choice is wrong. It simply means every use of time has a cost in terms of another opportunity.

Time choices are sometimes harder because there is no price tag. But they still matter. A student who uses time wisely often finishes work, learns new skills, and avoids stress. The opportunity cost of wasting time may be losing the chance to do something important later.

Worked example 3

Nora has 45 minutes before dinner. She can do one of these: finish homework, practice dance, or watch a show. She chooses to finish homework because it is due tomorrow.

Step 1: List the options.

The options are homework, dance practice, and watching a show.

Step 2: Identify the choice.

Nora chooses homework.

Step 3: Think about the best other option.

If Nora wanted dance practice more than the show, then dance practice is the best alternative.

Step 4: State the opportunity cost.

The opportunity cost is dance practice.

She gains completed homework, but gives up the chance to practice dance.

Notice how [Figure 2] still helps here. The same process works whether the choice involves money or time: list options, compare benefits, choose, and identify the best option given up.

People who understand opportunity cost often make stronger decisions because they look beyond the first thing they want. They ask whether the choice fits their needs, goals, and future plans.

This idea helps students in real life. At a school event, you may choose whether to spend all your money now or save part of it. At home, you may decide whether to use gift money on one large purchase or several smaller ones. In both cases, knowing the opportunity cost helps you think before acting.

The picture in [Figure 3] reminds us that comparing options side by side makes decisions clearer. When choices are written out, it becomes easier to spot which benefit matters most and what is being given up.

"Every choice opens one door and closes another."

That saying captures the heart of opportunity cost. A person cannot walk through every door at once. Choosing wisely means understanding which door is worth opening and which one is being left behind.

Sometimes there is no perfect choice. You may have to choose between two good options. In those moments, opportunity cost is still helpful. It lets you understand the trade-off instead of guessing.

As students grow older, they will face bigger decisions about saving, spending, work, study, and time. The idea stays the same: every choice has a cost, and that cost is the value of the best opportunity not chosen. When you understand that, you are better prepared to make thoughtful decisions.