Two people can each put away $10, but what happens next can be very different. One person may keep that money in a safe place for a short-term goal, like buying a game or a backpack. Another person may use that money to try to grow it over many years. Both are making careful money choices, but they are not doing the same thing. Knowing the difference helps people make better decisions with their money now and later.

When people earn money, they do not always spend it right away. They often decide what part to use now and what part to set aside for the future. That future could be next week, next month, or many years from now. A student might want to save for a class trip, while an adult might invest for retirement. These choices are connected to personal financial literacy, which means understanding how money works in everyday life.

Financial institutions, such as banks and credit unions, help people manage money. Some places are mainly used for keeping money safe and easy to reach. Other kinds of accounts are used for trying to grow money over a longer time. To make wise choices, it is important to understand the difference between saving and investing.

Saving means setting money aside in a safe place so you can use it later, usually for short-term needs or goals.

Investing means using money to buy something that may grow in value over time, usually for longer-term goals.

These two ideas are related because both involve planning for the future. However, they are not the same. The main differences have to do with safety, time, and how much money might grow.

A savings account is a common place to keep money when people are saving. A savings account is a place at a bank or credit union where money can be kept safely. People use saving when they want money to be available soon or when they do not want to take much risk.

Saving is often a good choice for goals such as buying school supplies, paying for a field trip, or building an emergency fund. An emergency fund is money set aside for unexpected needs, such as replacing something broken or helping with a sudden expense. If you need the money soon, saving usually makes more sense than investing.

Money in a savings account may earn interest. Interest is extra money the bank pays for keeping your money there. The amount is often small, but the money is usually safer than money used for investing. For example, if you put $100 into a savings account and the bank pays $2 in interest over time, you would have $102 because \(100 + 2 = 102\).

Saving has several important features. It is usually safer, it is usually easy to access, and it is often best for short-term goals. The trade-off is that saving usually does not grow money very quickly.

Some people think saving is only for large amounts of money, but even small amounts matter. Putting away $5 each week can add up to $20 in about four weeks because \(5 + 5 + 5 + 5 = 20\).

Saving also helps people practice patience and planning. Even when the amount is small, the habit of setting money aside regularly can build strong money skills.

Investing is different from saving because the main goal is growth over a longer time. Instead of only storing money safely, a person uses money to buy something that may increase in value. This could include stocks, bonds, or mutual funds. At this grade level, the important idea is simple: investing gives money a chance to grow more, but it also brings more risk.

Risk means the chance that something may not turn out as planned. With investing, risk means the value can go up, but it can also go down. If someone invests $100, it might grow to $110, but it might also fall to $95. Unlike saving, investing does not promise steady safety.

That is why investing is usually better for long-term goals, such as money for college or for many years in the future. Over a long time, investments may recover from short-term drops and may grow more than a regular savings account. But there is no guarantee.

How investing works over time

When people invest, they are often buying a small part of a company, lending money to an organization, or joining a group of investments. If those investments do well, the money may grow. If they do poorly, the money may shrink. Time matters because investments often rise and fall along the way.

Investing can sound exciting because of the possibility of larger gains, but it should not be confused with "easy money." Smart investors learn, plan, and understand that growth usually takes time.

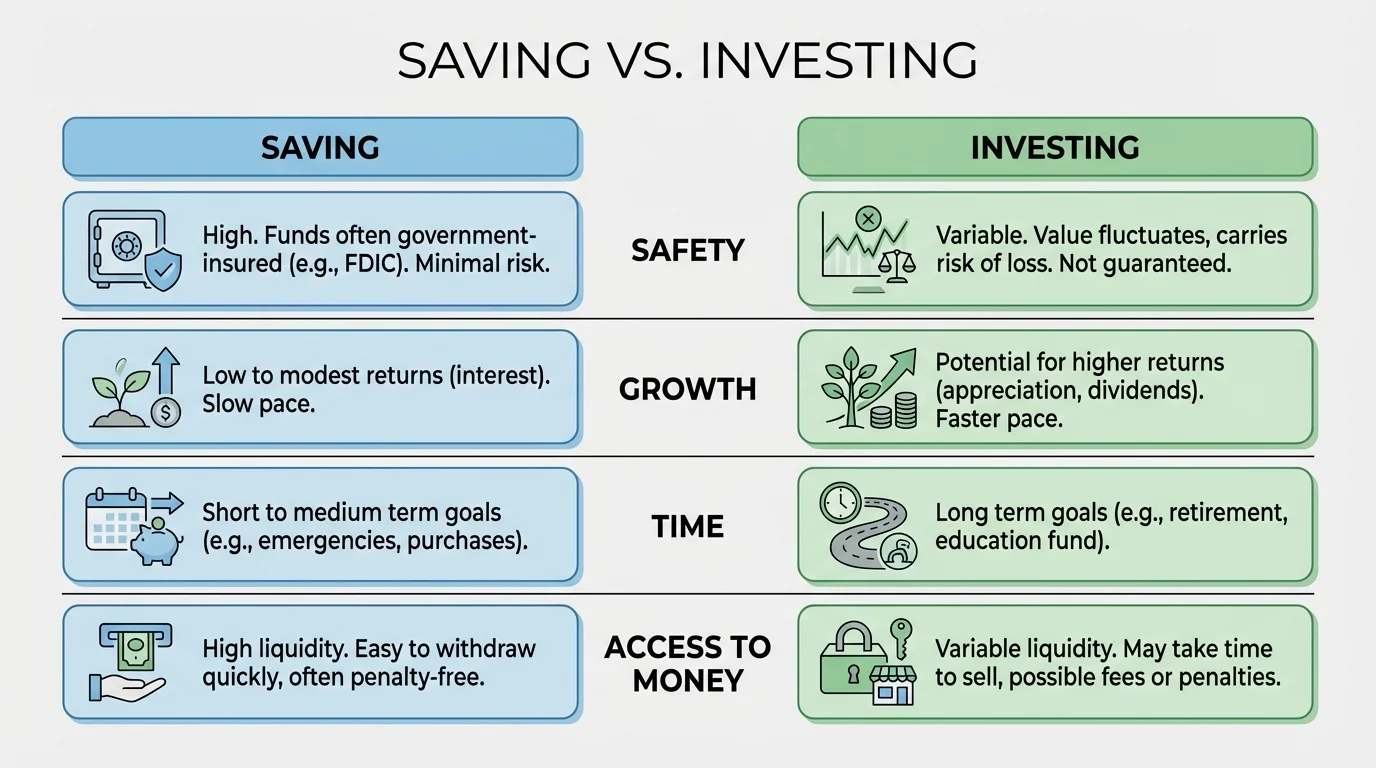

Saving and investing differ in several important ways, as [Figure 1] shows through a simple comparison of safety, growth, time, and access to money. Looking at these categories side by side makes it easier to choose the right tool for the right goal.

Think of saving as parking a bike in a safe rack where you can get it quickly. Think of investing as planting a tree. A parked bike stays ready to use, but it does not grow. A tree can grow taller and stronger, but it needs time, and storms may affect it.

| Feature | Saving | Investing |

|---|---|---|

| Purpose | Keep money safe for later use | Try to grow money over time |

| Time | Usually short-term | Usually long-term |

| Safety | Usually safer | Usually less safe |

| Access | Often easy to reach | May be harder to use right away |

| Growth | Usually slower | May be faster, but not guaranteed |

Table 1. Comparison of saving and investing by purpose, time, safety, access, and growth.

One is not always better than the other. A person may need both. For example, someone may save for a summer camp fee and invest for a goal many years away.

Another big difference is what happens when plans change. If a student is saving for a new soccer ball and needs the money next month, saving fits that goal. If the same student wants money to grow for many years, investing may be worth considering. Time is one of the most important clues when choosing between them.

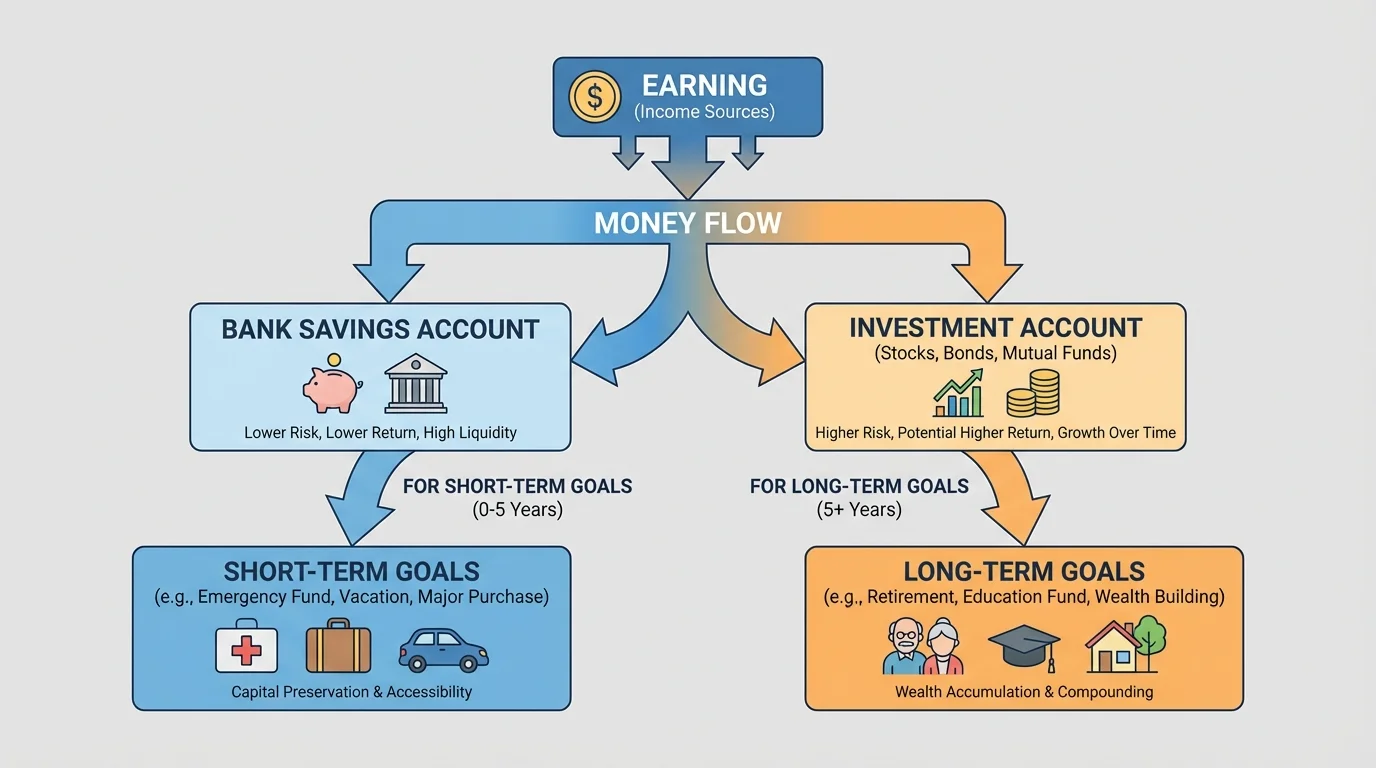

People do not have to manage all money choices by themselves. Different financial institutions help with different jobs, and [Figure 2] illustrates how money can move toward either short-term saving or long-term investing. These institutions provide safe places, accounts, records, and tools that help people organize their money.

Banks and credit unions often offer checking accounts and savings accounts. A checking account is used more for spending and paying bills, while a savings account is used for keeping money set aside. For investing, people may use an investment company or, with help from adults, a brokerage account. These accounts are used to buy investments instead of simply storing cash.

The role of these institutions is important because they help people keep track of money, protect it, and make plans. A bank statement, account balance, and online app can all help someone see how much money has been saved. Investment accounts also help people track changes in value over time.

Using the right kind of account matters. Putting emergency money into a savings account can make it easier to reach when needed. Putting long-term money into an investment account may offer more chance for growth. This reminds us that money goals and account choices should match.

People earn money, spend money, save money, and sometimes borrow money. Good money management means choosing where money should go based on a plan, not just on impulse.

Adults often compare services before choosing a financial institution. They may look at fees, convenience, and how easy it is to access an account. Even though students may not open all of these accounts on their own, understanding their purpose builds strong financial knowledge.

One reason people save or invest is to have more money in the future than they have today. Saving usually grows through interest. Investing may grow because the value of the investment rises or because it earns income over time.

Suppose a student saves $50 and later earns $1 in interest. Then the new total is \(50 + 1 = 51\), so the student has $51. The growth is small, but the money remains in a safer place.

Comparing two money choices

A student has $100 and is deciding whether to save it or invest it.

Step 1: Look at a saving example.

If the student puts $100 in savings and later earns $3 in interest, the total becomes \(100 + 3 = 103\).

Step 2: Look at one investing example with growth.

If the student invests $100 and it grows by $12, the total becomes \(100 + 12 = 112\).

Step 3: Look at one investing example with loss.

If the same $100 investment drops by $8, the total becomes \(100 - 8 = 92\).

This shows why investing can lead to more growth, but it can also lose value.

These examples show a basic rule: saving usually offers smaller but steadier growth, while investing may offer bigger growth with more uncertainty. That uncertainty is part of the risk.

To choose wisely, people ask a few key questions. How soon will the money be needed? How safe does it need to be? Is the goal short-term or long-term? Is the person willing to accept risk?

If the goal is to buy something in a few weeks or months, saving is often the better choice. If the goal is many years away, investing may make more sense. For example, money for a birthday gift next month should probably be saved. Money for a faraway future goal may be invested.

| Goal | Better Choice | Why |

|---|---|---|

| New headphones in 2 months | Saving | Money is needed soon |

| Emergency money | Saving | Needs to be safe and easy to reach |

| College in many years | Investing | More time for possible growth |

| Retirement far in the future | Investing | Long time horizon |

Table 2. Examples of money goals and whether saving or investing usually fits better.

Sometimes the best answer is both. A family might keep some money in savings for emergencies and invest some money for long-term plans. This balanced approach can help with both safety and growth.

Goal-matching example

Maria receives $30 for helping with chores and birthday gifts.

Step 1: She wants a notebook that costs $12 next week.

Because she needs the money soon, saving fits this goal.

Step 2: She decides to set aside $12 for the notebook.

That leaves \(30 - 12 = 18\).

Step 3: She chooses a long-term goal for the remaining money.

If her family is helping her learn about investing for the future, the remaining $18 could be considered for a long-term plan.

This example shows that one person can use saving and investing for different purposes at the same time.

As students grow older, they will face more money choices. Learning to connect each goal with the right tool is an important life skill.

Whether someone is saving or investing, good habits matter. It helps to make a plan, keep track of goals, and review progress. A person can decide how much money to set aside each week or month. Even small regular amounts can build over time.

For instance, if a student saves $4 each week for 10 weeks, the total becomes \(4 \times 10 = 40\), so the student will have $40. A regular habit can matter more than starting with a large amount.

Another smart habit is learning before making choices. People should understand where their money is going, who manages the account, and what risks are involved. Saving usually focuses on safety and easy access. Investing focuses more on long-term growth and requires patience.

"Do not put all your eggs in one basket."

— Old proverb about spreading risk

This saying connects especially well to investing. People often spread money across different investments instead of placing everything in one place. That can help reduce risk, although it does not remove risk completely.

Saving and investing are both tools for reaching goals. The smart choice depends on what the money is for, when it will be needed, and how much risk a person can handle. Understanding the difference helps people use financial institutions wisely and make stronger decisions for the future.