Why does one pair of sneakers cost $25 while another costs $180? Why can a summer job at one place pay more than a similar job somewhere else? These are not random differences. In a market economy, prices and wages are shaped by a powerful set of forces: what people want, what sellers can provide, and how much businesses and workers compete. Once you understand those forces, many everyday mysteries start to make sense.

Every society faces scarcity, which means resources are limited while wants are unlimited. There is only so much land, time, labor, money, and raw materials available. Because of scarcity, people and businesses must make choices. Should a farmer grow corn or strawberries? Should a student spend time mowing lawns or tutoring? Should a company make more video game systems or more tablets?

In a market economy, many of these choices are guided by prices. A price is the amount paid for a good or service. A wage is the payment workers receive for their labor. Prices help buyers decide what they can afford, and they help sellers decide what is worth producing. Wages help workers decide what jobs to take, and they help employers decide how many workers to hire.

Market economy is an economic system in which many decisions about producing, buying, and selling are made by individuals and businesses rather than by the government alone.

Supply is the amount of a good or service that sellers are willing and able to offer.

Demand is the amount of a good or service that buyers are willing and able to purchase.

Competition is the rivalry among sellers or among workers as they try to win customers or jobs.

These ideas do not just belong in textbooks. They affect the cost of lunch at a restaurant, the price of gasoline, the cost of concert tickets, and how much people earn as teachers, electricians, coders, or mechanics.

A market economy depends on millions of choices. Buyers decide what they want. Sellers decide what to offer. Workers decide what jobs to seek. Employers decide whom to hire. When all these decisions come together, they create markets. A market is any place, real or online, where buyers and sellers interact.

One important reason market economies developed in many places is that different societies had different resources, values, and experiences. A region with rich farmland might build strong farm markets. A coastal area might focus on fishing and shipping. A society that values private property and individual choice often gives more freedom to buyers and sellers, which supports market activity. In this way, economic systems grow partly from geography and partly from what people believe is fair or useful.

Resources can include natural resources, human labor, tools, machines, and knowledge. Because no society has unlimited resources, every economy must answer basic questions: what to produce, how to produce it, and for whom to produce it.

In a market economy, prices and wages help answer those questions. If the price of oranges rises, farmers may decide to grow more oranges. If computer programming jobs pay high wages, more people may decide to learn coding. Prices and wages send signals.

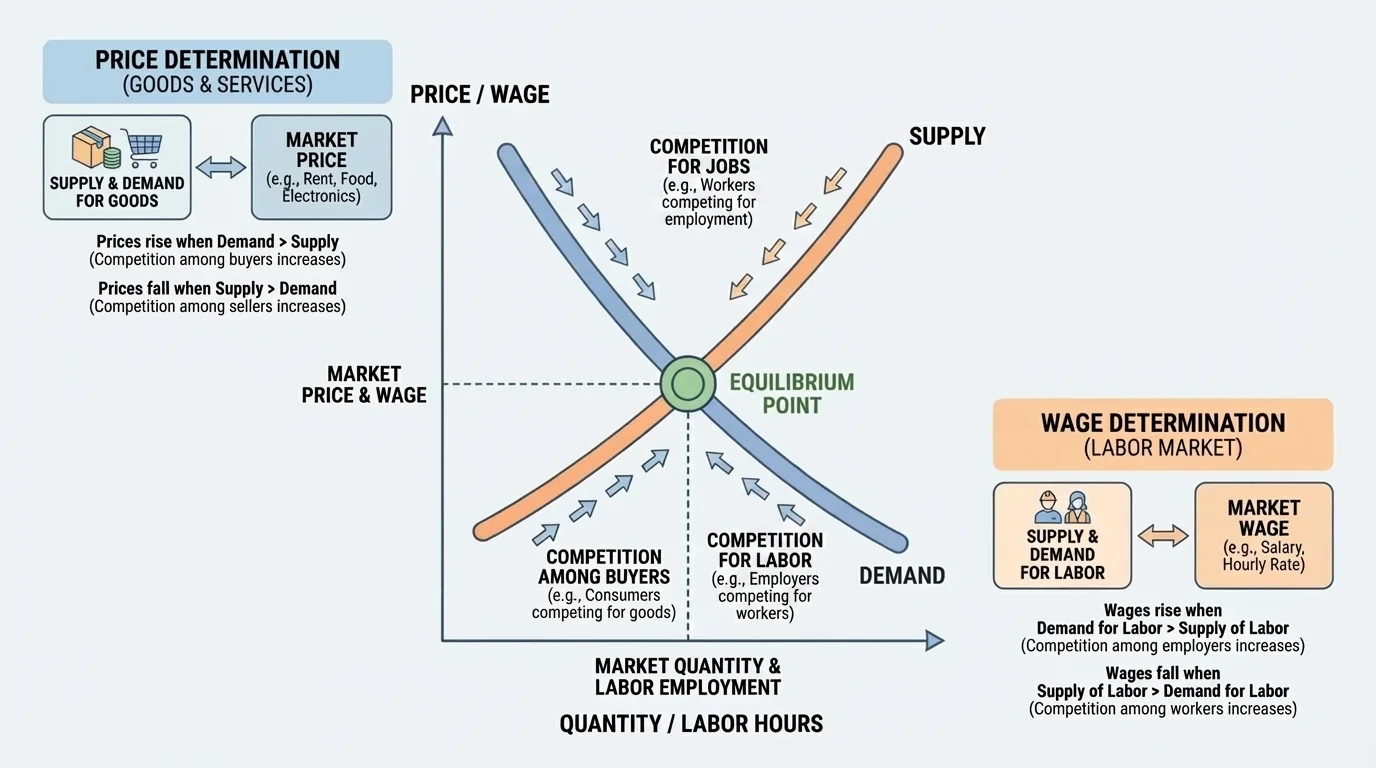

Supply and demand are at the center of market pricing. When buyers and sellers interact, the market tends to move toward a balance point, as [Figure 1] shows. This balance is often called the equilibrium price, which is the price where the amount buyers want matches the amount sellers want to offer.

If demand rises, buyers want more of a product. Suppose a famous athlete wears a certain brand of shoe, and suddenly many students want that shoe. If the supply has not changed yet, stores may raise the price because more people are trying to buy the same number of shoes.

If supply rises, sellers offer more of a product. Suppose a strawberry farm has perfect weather and produces a very large crop. When stores have more strawberries than usual, the price may fall so more customers will buy them.

Economists often describe these patterns in a simple way:

If demand goes up while supply stays the same, price usually rises.

If demand goes down while supply stays the same, price usually falls.

If supply goes up while demand stays the same, price usually falls.

If supply goes down while demand stays the same, price usually rises.

Why the curves matter

Demand usually slopes downward because people often buy more when prices are lower. Supply usually slopes upward because producers are often willing to offer more when prices are higher. The point where they meet is important because it helps explain why markets do not set prices completely at random.

Think about a school bake sale. If 100 students want cupcakes but only 30 cupcakes are available, the cupcakes become more valuable because they are scarce. If 200 cupcakes are available and only 50 students want them, sellers may lower the price to avoid leftovers. The same logic works in much larger markets, from cars to smartphones.

Later, when we compare economic systems, the meeting point in [Figure 1] becomes especially important because in a market economy this balance is usually shaped by buyers and sellers themselves, not mainly by government orders.

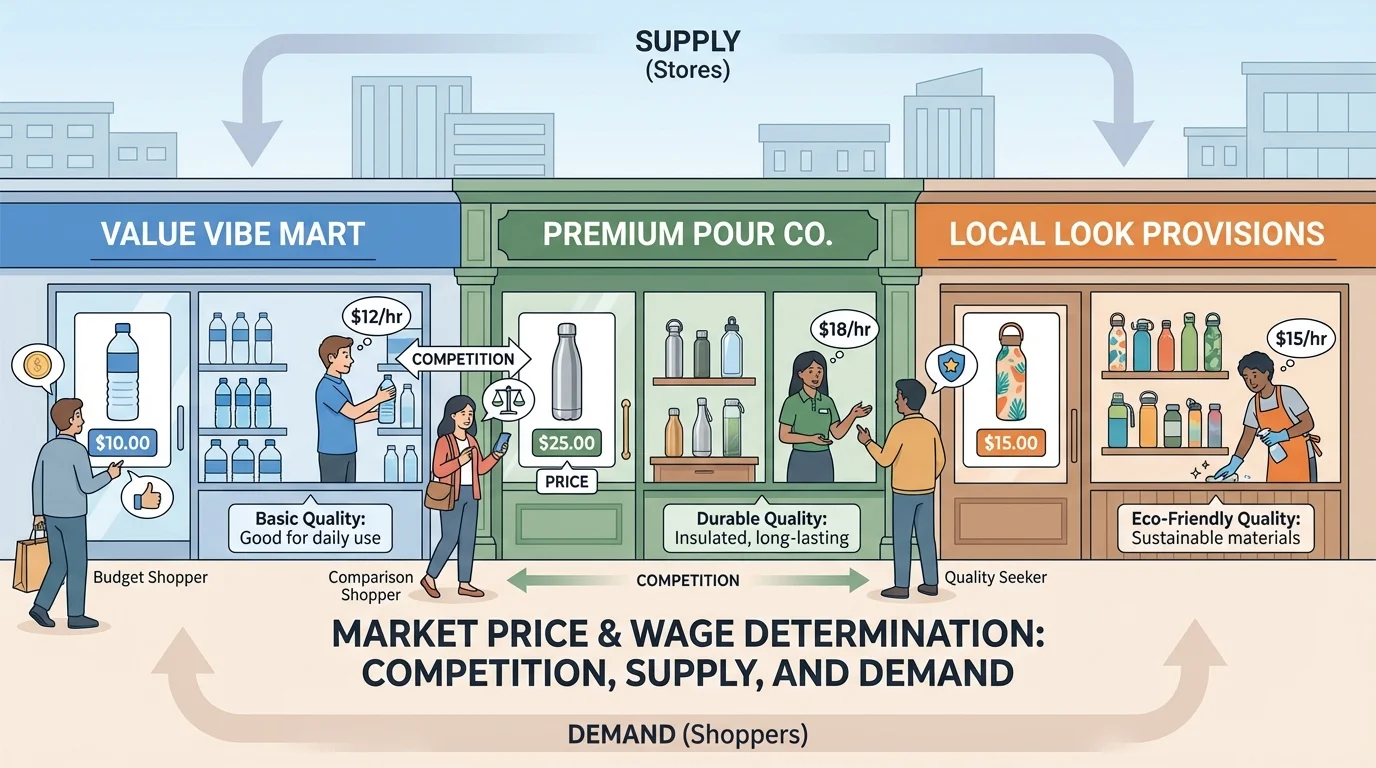

Competition is another major force in a market economy. When many businesses sell similar products, as shown in [Figure 2], each business has to work harder to attract customers. That often pushes prices down, improves quality, or leads to better service.

Suppose three pizza shops open in the same neighborhood. If one shop charges too much for a small pizza, customers may go to the other two shops. To keep customers, the expensive shop might lower its price, make the pizza bigger, or improve its ingredients. Competition gives buyers more choices.

Competition does not always mean the cheapest product wins. Sometimes companies compete by offering better design, longer-lasting products, faster delivery, or friendlier service. But when products are very similar, price becomes a strong tool.

What happens when competition is weak? If only one seller controls a market, buyers have fewer choices. Prices may stay high because customers cannot easily shop elsewhere. This is one reason many countries have rules against unfair business practices that block competition.

Competition can also affect sellers in a positive way. It can encourage creativity and efficiency. A company that finds a faster way to produce bicycles may lower its costs. Then it may lower the bicycle price to attract more customers. Buyers benefit, and other companies may improve too.

Online shopping has increased competition in many markets because customers can compare prices from different sellers in seconds. That quick comparison can pressure businesses to keep prices reasonable.

The store comparison in [Figure 2] helps explain why prices for the same type of item can differ from one place to another. Businesses are not just reacting to supply and demand; they are also reacting to one another.

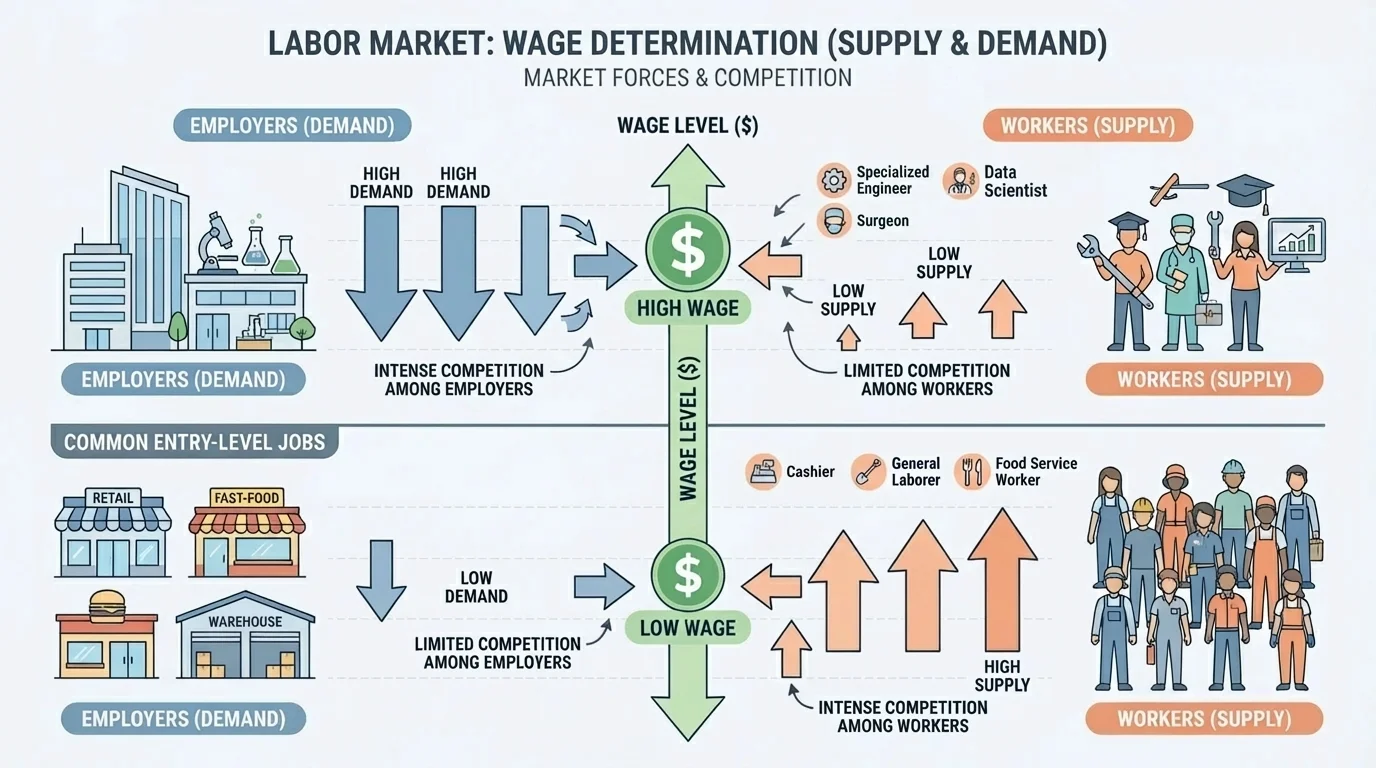

Wages are often called the price of labor. In the labor market, employers demand workers, and workers supply labor. Wages are shaped by the same broad forces that affect product prices: supply, demand, and competition.

[Figure 3] If many businesses need workers with a certain skill, wages for that skill may rise. For example, if hospitals need more nurses but there are not enough trained nurses available, hospitals may offer higher wages to attract them.

If many people are able to do a job and few employers are hiring, wages may stay lower. This does not mean the work is unimportant. It means the supply of workers is larger compared with the demand from employers.

Several factors influence wages:

Consider lifeguards during summer. If a beach town suddenly has many tourists, the demand for lifeguards may rise. If there are too few trained lifeguards, wages may increase. But if many certified students apply for the same small number of lifeguard jobs, wages may not rise much.

Real-world wage example

A town has only a few people who can repair advanced heating and cooling systems. During a heat wave, many homes and businesses need repairs quickly.

Step 1: Demand for this work rises because many customers need help at the same time.

Step 2: Supply stays limited because only a small number of trained workers can do the job.

Step 3: Businesses may raise wages or offer overtime pay to attract and keep these workers.

This example shows why scarce skills often earn higher wages in a market economy.

The labor relationships in [Figure 3] also help explain why learning new skills can matter. When a skill is harder to find, workers who have it may be in a stronger position when wages are negotiated.

Markets do not stand still. Prices and wages change as conditions change. Weather, technology, trends, transportation costs, new laws, and world events can all shift supply or demand.

Suppose drought damages wheat crops. Wheat supply falls, so bread prices may rise. Suppose a new machine helps factories make shirts more quickly. Shirt supply may increase, which can lower prices. Suppose a popular social media trend suddenly makes one kind of toy famous. Demand may rise fast, and stores may sell out.

Wages change too. A new technology may increase the demand for software designers. A recession, which is a period of slower economic activity, may reduce hiring in some jobs. If fewer businesses are hiring, workers may face tougher competition for jobs.

Signals and incentives

Higher prices and higher wages can act as signals. A higher price can signal producers to make more of a product. A higher wage can signal workers to train for a certain job. These signals help move resources and labor toward areas where they are most wanted.

That process is not perfect. It can take time for farmers to plant more crops or for students to complete job training. Because of that delay, markets can have shortages one year and surpluses the next.

Think about gasoline. If many people are traveling during holidays, demand for gas can increase. If a refinery shuts down or shipping is disrupted, supply can decrease. When higher demand and lower supply happen together, prices often rise quickly.

Think about farm products. If apple orchards produce an unusually large harvest, stores may have more apples than usual. Prices may fall, and stores may advertise sales. Lower prices encourage customers to buy more apples, applesauce, or pies.

Think about part-time jobs. If one local business needs only two workers but 40 students apply, the business does not need to offer a very high wage to fill the jobs. But if several businesses are all looking for reliable workers at the same time, they may offer higher wages to compete for applicants.

Case study: concert tickets

A famous singer announces one concert in a city with 20,000 seats, but 200,000 fans want tickets.

Step 1: Demand is very high because many people want to attend.

Step 2: Supply is fixed at 20,000 seats because the stadium size does not change.

Step 3: Ticket prices tend to rise because the event is scarce.

This is a strong example of scarcity affecting market price.

These examples show why prices and wages are not simply chosen from nowhere. They respond to what people want, what is available, and how strongly buyers, sellers, workers, and employers compete.

Even in market economies, governments often set rules. These rules can affect prices and wages in everyday life. For example, a minimum wage is the lowest legal wage employers can pay in certain jobs. It is meant to protect workers from being paid extremely low amounts.

Some governments also use price controls in special situations. A price ceiling is a legal maximum price. A price floor is a legal minimum price. These policies can help some people, but they can also create shortages or surpluses if the set price is far from the market level.

Workers may also join unions to bargain for better wages or working conditions. A union increases workers' ability to negotiate together instead of one by one. This can affect wage levels in some industries.

"Prices are signals wrapped up in numbers."

— A simple way to think about markets

Policy choices matter because societies do not care only about efficiency. They also care about fairness, safety, and stability. That is why most real economies mix market forces with government rules.

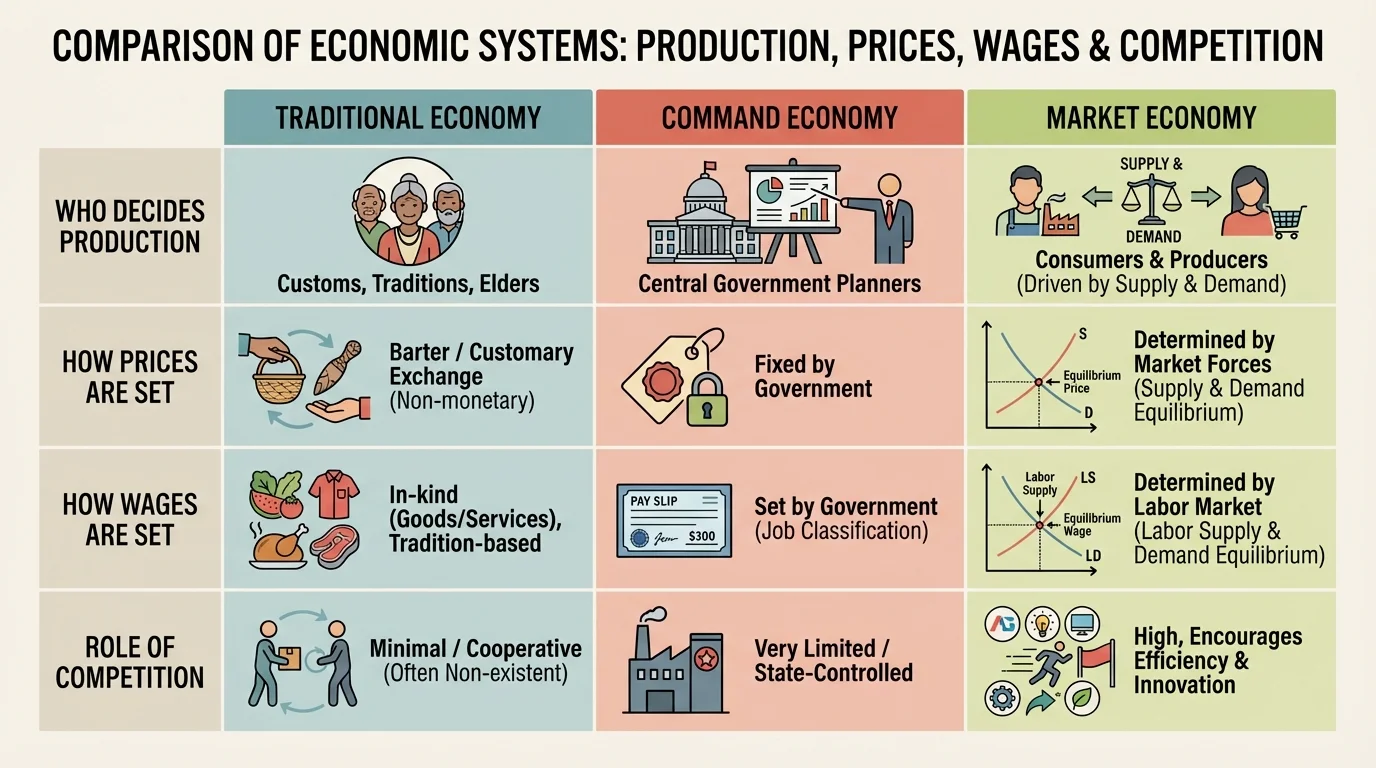

To understand a market economy better, it helps to compare it with other systems, as [Figure 4] shows. In a traditional economy, customs and long-standing habits guide many choices about work and production. In a command economy, the government makes many major decisions about what to produce, how much to produce, and what prices or wages should be.

In a market economy, by contrast, prices and wages are mostly shaped by supply, demand, and competition. This system often develops where societies value individual choice, private business activity, and flexible responses to scarcity.

No real country is purely one system. Most economies are mixed. Still, the comparison matters because it shows that the way prices and wages are determined depends partly on a society's values and experiences, not only on resources.

| Economic system | Who mainly decides? | How prices and wages are mostly set | Role of competition |

|---|---|---|---|

| Traditional | Customs and habits | Often based on tradition | Usually limited |

| Command | Government planners | Often directed by government | Usually limited |

| Market | Buyers, sellers, workers, and businesses | Mostly by supply and demand | Usually important |

Table 1. A comparison of how different economic systems make decisions about production, prices, wages, and competition.

The comparison in [Figure 4] makes clear that market economies rely more heavily on decentralized decisions. Instead of one authority setting every value, many separate choices interact to produce prices and wages.

A quick way to organize market changes is to connect the direction of supply or demand with the likely price effect.

| Change in market | Likely effect on price | Example |

|---|---|---|

| Demand increases | Price tends to rise | A toy becomes trendy |

| Demand decreases | Price tends to fall | Students lose interest in a game |

| Supply increases | Price tends to fall | A large harvest of peaches |

| Supply decreases | Price tends to rise | A storm damages crops |

Table 2. Common changes in supply or demand and their usual effects on prices in a market economy.

Wages follow similar patterns. If the demand for workers rises, wages often rise. If the supply of workers rises much faster than available jobs, wages may stay lower. In both product markets and labor markets, scarcity plays a major role.