Every phone, meal, backpack, bus ride, and streaming subscription depends on resources. A chocolate bar in a store may seem simple, but behind it are soil, water, cocoa farms, factory machines, workers, trucks, store shelves, electricity, and money. Economics helps us study how people and businesses use these limited things. Personal finance helps us understand how an individual manages limited time, money, and skills. In both cases, resources are at the center of every choice.

In everyday life, people often think of a resource as something useful. In economics, that idea becomes more specific. A resource is anything that can be used to produce goods and services or to help meet human wants and needs. Since resources are limited but human wants are many, people must choose carefully. That is why resources matter to families, businesses, and entire countries.

Resources also help explain how consumers and businesses connect with one another. Consumers buy and use goods and services. Businesses produce and sell them. To do that, businesses need land, raw materials, labor, tools, money, and ideas. Consumers, meanwhile, use their own resources such as income, time, and knowledge to decide what to buy and how much to save.

Resources are useful things people, businesses, and governments can use to produce goods and services or satisfy needs and wants.

Scarcity means resources are limited, so not everything people want can be produced or purchased.

Consumers are people who buy and use goods and services, while businesses organize resources to produce and sell them.

Understanding resources helps explain large patterns in the Eastern Hemisphere as well. Countries in Africa, Europe, Asia, and Australia have different climates, minerals, workers, technologies, and transportation systems. These differences affect what each place can produce efficiently and what it may need to import from somewhere else.

From an economic point of view, a resource is not just something valuable. It is something that can be used in production. If a bakery wants to make bread, it needs flour, water, ovens, workers, delivery vehicles, and a plan for selling the bread. Each of these is part of production. Without enough resources, the bakery cannot make as much bread as it wants.

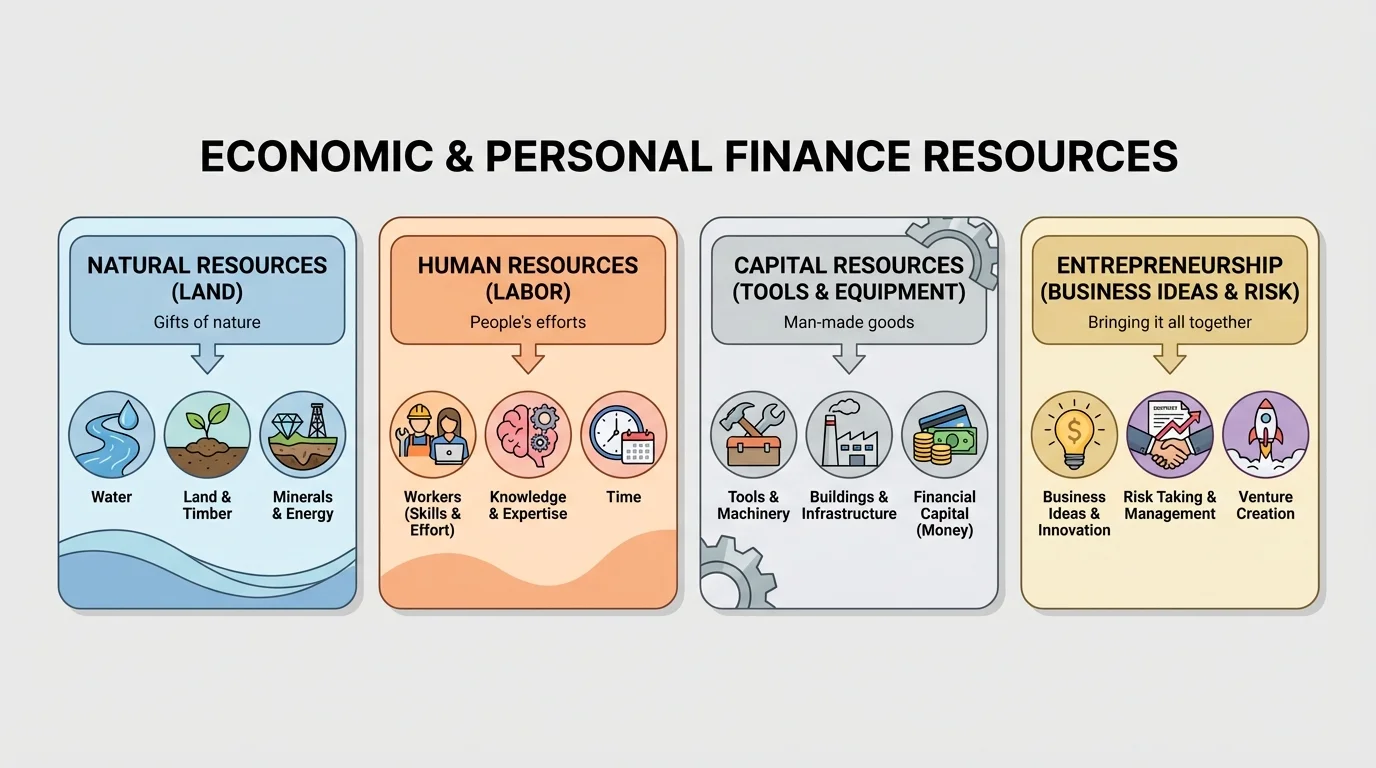

Economists often connect resources to the idea of factors of production. This phrase means the basic categories of inputs used to create goods and services. These inputs are grouped into four major types: natural resources, human resources, capital resources, and entrepreneurship. Looking at resources this way makes it easier to understand why some businesses succeed, why products cost what they do, and why countries trade.

Economics also reminds us that value depends on use. Sand in a desert may seem ordinary, but if it can be used in construction or manufacturing, it becomes an important resource. Information can also be a resource. Knowing weather patterns, shipping routes, or consumer preferences can help a business make better decisions and avoid waste.

Economic resources are commonly grouped into four main categories. These categories help us organize how goods and services are produced and how businesses combine different inputs.

[Figure 1] Natural resources are materials that come from nature. These include water, forests, fertile soil, sunlight, fish, natural gas, oil, and minerals such as copper or iron. A farm depends on soil and water. A fishing business depends on oceans or rivers. A country with large oil reserves may export petroleum, while another country with rich farmland may export wheat or fruit.

Human resources are the people who do the work and the skills they bring. A nurse, engineer, teacher, mechanic, farmer, and software designer are all human resources. Education and training can improve human resources because skilled workers often produce more and higher-quality goods and services.

Capital resources are tools, machines, buildings, and equipment used to make other goods and services. A sewing machine in a clothing factory, a tractor on a farm, and a computer in an office are all capital resources. Capital resources are not the same as money. In economics, capital means productive tools and equipment.

Entrepreneurship is the ability to organize the other resources, take risks, and start or manage a business. An entrepreneur might decide to open a food business, buy equipment, hire workers, and create a marketing plan. Without entrepreneurship, the other resources may not be combined effectively.

The four categories often work together. Think about a bicycle factory. The metal and rubber are natural resources. The workers who design and assemble bicycles are human resources. The factory building and machines are capital resources. The person who launches the business and decides what type of bikes to produce is the entrepreneur.

| Resource Type | What It Includes | Example |

|---|---|---|

| Natural | Materials from nature | Water, timber, oil |

| Human | People and their skills | Farmers, doctors, builders |

| Capital | Tools and equipment used in production | Machines, trucks, computers |

| Entrepreneurship | Risk-taking and organizing production | Starting and managing a company |

Table 1. The four major categories of economic resources and examples of each.

Resources are not only for businesses and economies. They also matter in personal finance, which is the way people manage money and other useful assets in their own lives. From a personal finance perspective, resources include money, time, knowledge, health, talents, and access to information. A student may not own a factory, but that student still has resources that can be used wisely or poorly.

Budget is one of the most important personal finance tools. A budget is a plan for how money will be earned, spent, and saved. If a student receives $40 for the week and spends $15 on snacks, $10 on a game, and $5 on transportation, the total spent is $30, leaving $10. Written mathematically, the money left is \(40 - 15 - 10 - 5 = 10\). That remaining $10 is still a resource, and the student must choose whether to save it or spend it.

Personal resources are broader than money. A person with strong math skills, reliable transportation, healthy habits, and good time management often has more choices than someone without those supports. In personal finance, using resources wisely means balancing income, spending, saving, and long-term goals.

Time is a resource too. If a person spends two hours scrolling on a phone, those same two hours cannot be used for homework, exercise, sleep, or a part-time job. That does not mean relaxation is wrong, but it does show that time is limited. Managing time well can improve school performance, reduce stress, and even help people earn more money later through stronger skills.

Skills and knowledge are personal resources because they can increase earning power. Someone who learns coding, welding, nursing, graphic design, or accounting may qualify for better jobs. In this way, education is an investment in human resources at the individual level.

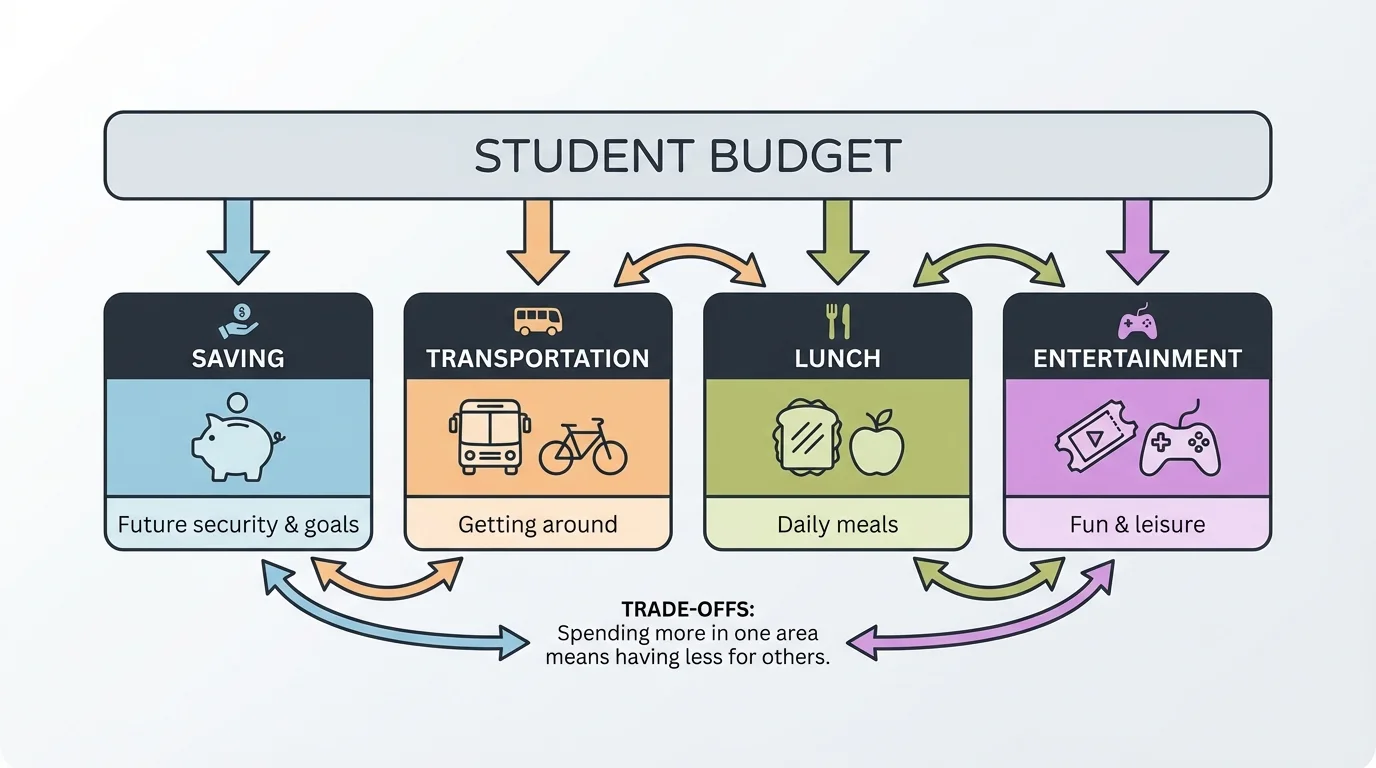

[Figure 2] illustrates a simple truth of economics: because resources are limited, choosing one option usually means giving up another. This idea applies whether the decision is made by a student, a business owner, or a government.

Opportunity cost is the value of the next best choice that is given up when a decision is made. If you have $20 and choose to spend it on a movie and snacks, you cannot also use the same $20 to buy a book or save for headphones. The opportunity cost is the next best thing you gave up.

A trade-off is the balancing of benefits and costs when choices must be made. Suppose a family has a monthly transportation budget. If fuel prices increase, the family may need to reduce spending somewhere else, such as entertainment. If a business pays more for electricity, it may raise prices, reduce output, or find ways to use energy more efficiently.

Scarcity affects countries as well. A nation may have rich farmland but little fresh water. Another may have a highly educated workforce but limited energy supplies. Governments must decide how to use tax money, land, and labor. Should more money go to transportation, schools, health care, or defense? Every choice has an opportunity cost.

Case study: one limited amount, several choices

A student has $25 for the weekend and is considering a sports event ticket for $18, lunch with friends for $9, or saving the money.

Step 1: Compare the costs.

The student cannot buy both the ticket and the lunch because \(18 + 9 = 27\), and \(27 > 25\).

Step 2: Identify the trade-off.

Choosing the ticket means giving up lunch with friends or some savings. Choosing lunch means giving up the ticket or some savings.

Step 3: Identify the opportunity cost.

If the student chooses the ticket, the opportunity cost is the next best option not chosen, such as lunch with friends.

This example shows that limited resources force decisions, even when all choices seem good.

The same ideas shape major world industries. A company deciding whether to build a factory in India, Vietnam, Germany, or Kenya must compare labor costs, transportation, energy supply, laws, training, and access to customers. No location is perfect. Every decision includes trade-offs.

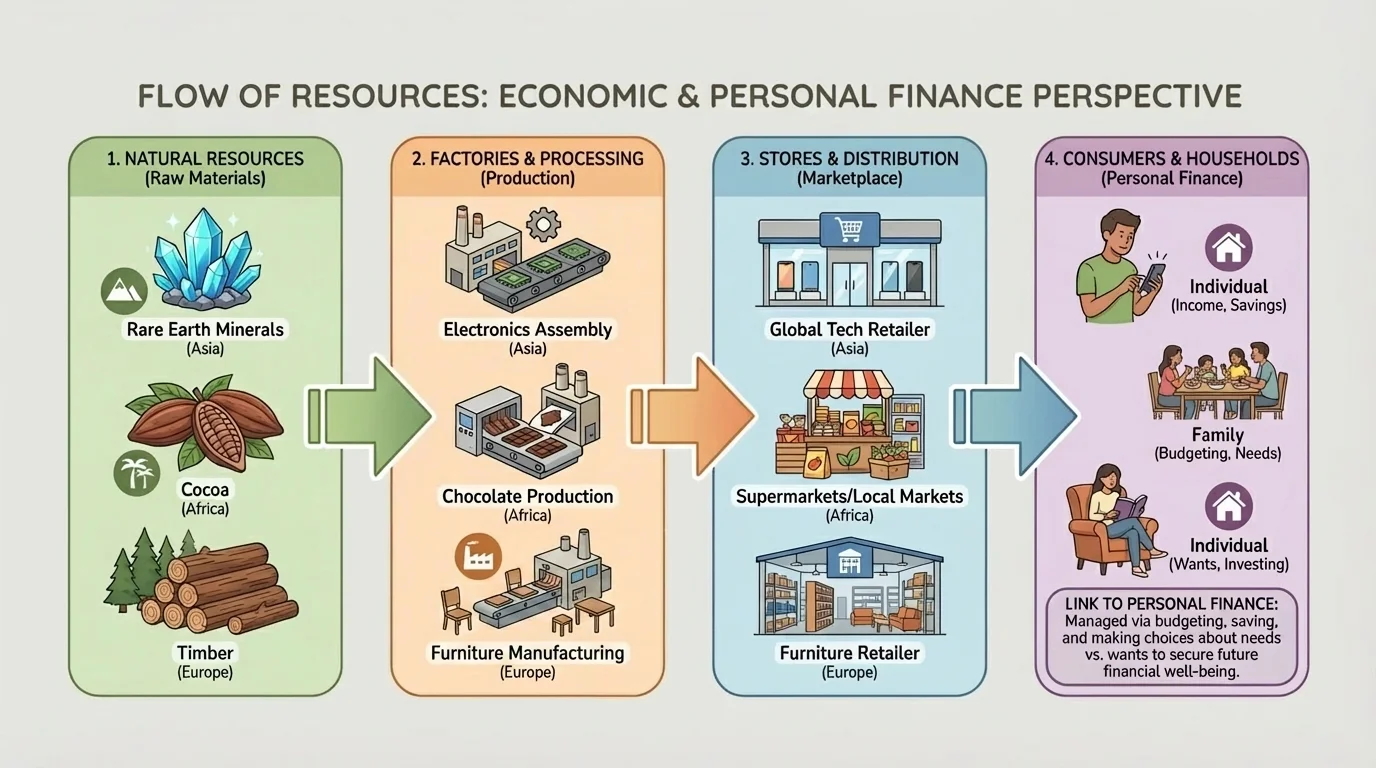

The Eastern Hemisphere includes a huge variety of economies, climates, and resource patterns. Resources often move through a chain: natural resources are extracted or grown, businesses process them, stores sell goods, and consumers buy them. This flow connects farms, mines, factories, shipping companies, retailers, and households.

Consider cotton grown in India, Egypt, or Pakistan. Farmers use land, water, seeds, equipment, and labor. Textile factories turn cotton into fabric. Clothing companies design and sew garments. Stores then sell shirts or jeans to consumers in cities across Europe, Asia, or Africa. One simple product may involve resources from several countries.

[Figure 3] Another example is electronics. Minerals such as cobalt, copper, and rare earth elements may come from parts of Africa or Asia. Factories in East or Southeast Asia may assemble phones or computers. Shipping companies move the products to markets worldwide. Consumers then decide whether the price, quality, and features are worth their money.

Businesses in the Eastern Hemisphere often choose locations based on available resources. A company may build near a port to reduce shipping costs. A factory may open in a region with skilled workers. A tourism business may grow where natural beauty or historic sites attract visitors. These choices show that resources are not just physical materials; location, education, and infrastructure also matter.

Consumers influence businesses through demand. If many people want electric vehicles, healthier foods, or lower-cost clothing, businesses respond by changing production. But businesses are still limited by resources. If battery minerals are scarce or shipping costs rise, prices may increase. The market reflects the push and pull between wants and available resources.

We can also see how resource differences encourage trade. Japan has limited natural resources compared with some larger countries, yet it has developed strong human resources, technology, and manufacturing. Saudi Arabia has major petroleum resources. Kenya has important agriculture and tourism sectors. Germany has advanced industry and engineering. These differences help explain why countries specialize and exchange goods and services.

Some of the busiest trade routes in the world connect Eastern Hemisphere regions through the Mediterranean Sea, the Indian Ocean, and the South China Sea. When a shipping lane is blocked or delayed, stores far away may still feel the effects through higher prices or product shortages.

Consumers are part of this system every time they buy food, clothing, fuel, or technology. Their choices send signals to businesses about what to make, how much to make, and sometimes where to get resources. This shows that consumers are not separate from production; they are connected to it at the end of the chain and influence what happens earlier in the chain as well.

Good resource management means using limited resources in ways that meet needs without wasting them. For individuals, this may mean making a budget, comparing prices, saving part of income, and using time carefully. For businesses, it may mean training workers, maintaining machines, reducing energy waste, and tracking supply costs.

Savings are money not spent right away. Savings are a resource for future goals and emergencies. If a person saves $5 each week for 12 weeks, the amount saved is \(5 \times 12 = 60\). That $60 could later help pay for school supplies, a gift, or part of a larger purchase. Saving gives people more choices later.

Conservation is also important. A business that wastes water, fuel, or raw materials increases costs and may damage the environment. A household that turns off unused lights, fixes leaks, and plans meals carefully may lower expenses. Wise use of resources often helps both finances and the environment at the same time.

Earlier economic ideas still matter here: needs are things people must have to live, while wants are things people would like to have. Resources are often used first to meet needs, and then to satisfy wants when possible.

Technology can improve resource use. Better irrigation can help farmers use less water. More efficient machines can reduce electricity costs in factories. Online banking and budgeting apps can help people track spending. When technology helps produce more with the same amount of input, economists often call that improved productivity.

Resources do not stay constant. Drought can reduce crop yields. War can interrupt trade. New discoveries can make previously unused materials valuable. A new invention can reduce the need for one resource while increasing the need for another. Because of this, consumers and businesses must adapt.

For example, if a flood damages roads and ports, transportation slows down. Stores may receive fewer products, and prices may rise. If a country invests heavily in education, its human resources may improve over time. If a business trains workers well, quality may improve and waste may decrease. Resource changes can happen suddenly or slowly, but they always affect choices.

Information is especially important during change. Businesses study weather reports, market prices, customer trends, and political events because information helps them decide how to use resources. Individuals do something similar when they compare prices, check reviews, or plan for future expenses.

You use resources every day, even if you do not think about them in economic terms. When you decide how to spend an allowance, how to divide homework time, or whether to save for something bigger, you are managing limited resources. When your family compares brands at a store or decides whether to repair or replace an item, it is also making resource decisions.

These choices are not small. They build habits. A person who learns to plan, save, compare costs, and think about opportunity cost becomes better prepared for adult financial decisions. A student who develops skills and values time is also building personal resources that may lead to future opportunities.

Economics and personal finance both teach the same powerful lesson: resources are useful, limited, and deeply connected to choice. Whether the setting is a household budget, a factory in China, a farm in Egypt, a technology company in South Korea, or a clothing market in Turkey, the basic question stays the same: how can limited resources be used in the best possible way?