Have you ever had just enough money for one thing, but not two? That happens to everyone. A child may have money for a snack or a small toy, but not both. An adult may have money for groceries and other bills before buying something extra. Money choices can feel small, but they are important. When we decide how to use money, we are really deciding what matters most.

Money is not endless. Because money is limited, people must choose. A smart choice often begins by thinking about priorities. A priority is something that is more important than something else. If two things both seem good, the priority is the one that should come first.

Priority means what is most important right now.

Cost is what you give up to get something, usually money.

Benefit is the good thing you get from a choice.

When people make financial decisions, they look at what they need, what they want, how much things cost, and how useful those things will be. Sometimes the best choice is to buy now. Sometimes the best choice is to wait. Sometimes the best choice is not to buy at all.

Every time you spend money, you choose one thing instead of another. If you spend $4 on a juice and a cookie, you may not have that same $4 for crayons later. This means choices are connected. One choice can affect another choice.

A financial decision is a choice about money. Even children make financial decisions. Choosing how to use birthday money, allowance, or money from the tooth fairy is a financial decision. Good decisions are made by slowing down and thinking first.

It helps to ask simple questions: What do I need most? What will help me the longest? Is this worth the money? Can I wait? These questions help us be thoughtful instead of rushed.

You already know how to compare numbers. That helps with money too. If one item costs $3 and another costs $5, then $3 is less than $5, so the first item costs less.

Comparing money is part of being responsible. If you have $10 and spend $6, then you have \(10 - 6 = 4\) dollars left. Thinking about what is left can help you decide whether spending right now is a good idea.

A need is something important for living, learning, or staying safe and healthy. Food, water, clothes, and a place to live are needs. School supplies can also be needs when they help a child do schoolwork. A want is something you would like to have but do not need to live. Toys, stickers, and extra treats are often wants. Thinking this way helps set priorities.

[Figure 1] Sometimes something can be a want in one situation and a need in another. A coat in winter may be a need because it keeps you warm. A second fancy coat in the same size might be more of a want. This is why we do not just ask, "Do I like it?" We also ask, "Do I need it now?"

Priorities help us put first things first. If a child has $8 and needs a folder for school that costs $3, but also wants a toy car that costs $8, the folder should come first. The child can still want the toy car, but the need has a higher priority.

Here is another example. Lena has $7. She sees a pack of pencils for $2 and a bag of candy for $3. She needs pencils for class. Candy is a treat. If Lena buys the pencils first, she still has \(7 - 2 = 5\) dollars left. If she buys only candy, she may still need pencils later. That is why the pencils are the better priority.

Needs usually come before wants. When money is limited, people often pay for the most important things first. After needs are covered, they can think about wants.

Later, when you compare choices again, the same idea from [Figure 1] still matters: sorting needs and wants helps make calm, smart decisions.

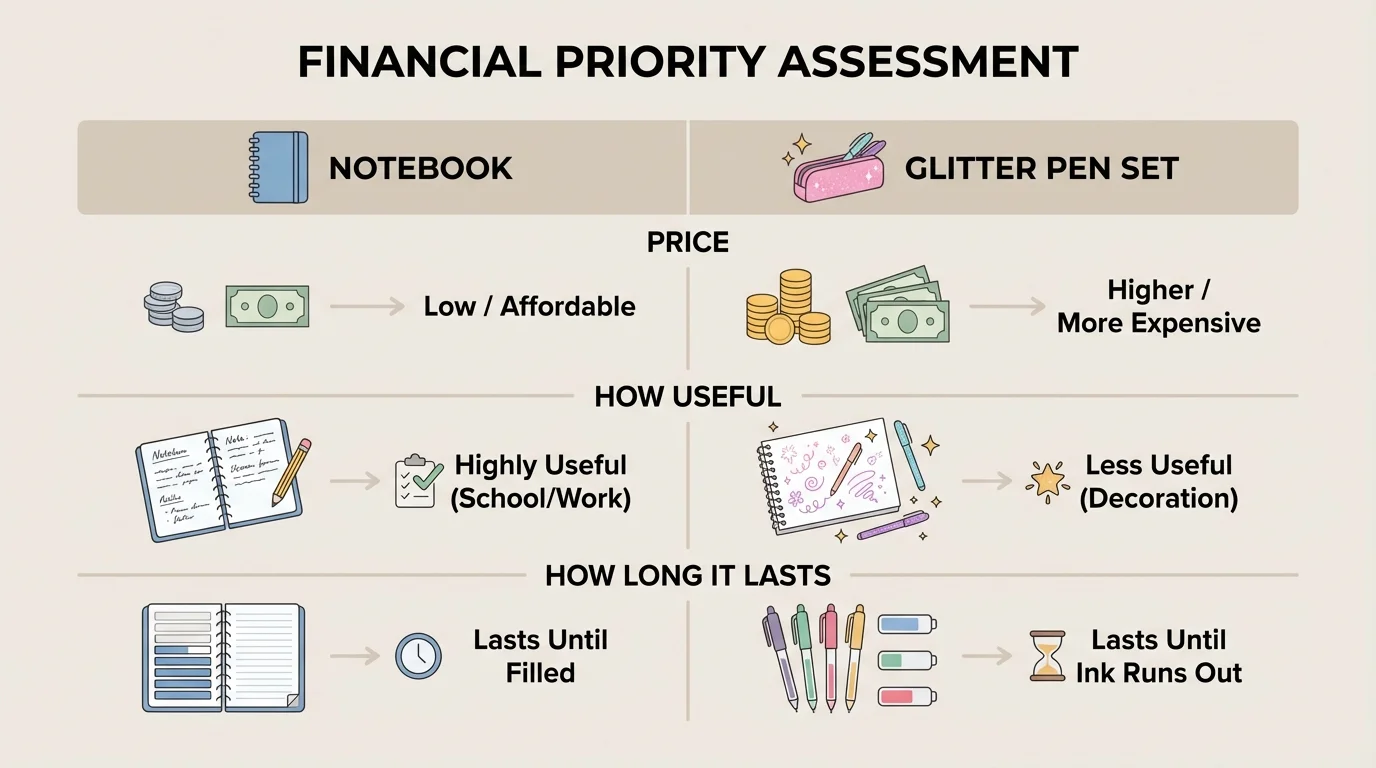

When people make money choices, they can think about cost and benefit. Cost is how much money you spend. Benefit is how helpful or enjoyable the item is. A comparison chart can make these ideas easier to see.

[Figure 2] Suppose Amir has $5. He can buy a glitter pen set for $5 or a notebook for $3. The glitter pens may look exciting, but the notebook may help with homework every day. The cost of the pen set is higher, and the benefit of the notebook may last longer because it is useful for school.

Sometimes the benefit is not about school. It might be about health, safety, or saving time. A healthy snack may have more benefit than candy because it gives your body better fuel. A lunchbox may have more benefit than a toy keychain because it is useful every school day.

Here is a simple way to compare two choices:

| Choice | Cost | Benefit |

|---|---|---|

| Apple slices | $2 | Healthy snack, fills you up |

| Candy | $2 | Sweet taste for a short time |

| Notebook | $3 | Useful for schoolwork |

| Fancy eraser toy | $3 | Fun, but not very useful |

Table 1. A simple comparison of cost and benefit for common choices.

If two things cost the same amount, the one with the greater benefit is often the better choice. If one thing costs less and still helps a lot, that can also be a very smart choice. This is one reason people compare before buying.

Worked example: Choosing a snack

Mila has $4. She can buy yogurt for $2 and fruit for $2, or she can buy a cupcake for $4.

Step 1: Find the total cost of yogurt and fruit.

The total is \(2 + 2 = 4\) dollars.

Step 2: Compare the choices.

Both choices cost $4, but yogurt and fruit give food for a snack with more lasting benefit.

Step 3: Decide which choice matches the higher priority.

If Mila needs a filling snack, yogurt and fruit are the better choice.

The cost is the same, but the benefits are different.

As you keep comparing, remember the chart in [Figure 2]: looking at price, usefulness, and how long something helps can make the best choice clearer.

Sometimes a smart decision is not about the cheapest item. It is about the item that gives the best value. Value means how useful or worthwhile something is for the money you spend.

For example, one pack of markers costs $2 but dries out quickly. Another pack costs $4 and lasts much longer. If the second pack works better for many weeks, it may have better value even though it costs more at first.

It also helps to think about time. Will you use the item once, or many times? A reusable water bottle may be a smarter purchase than a single small treat because it can be used again and again.

Some smart shoppers wait a day before buying a want. After waiting, they sometimes decide they do not want it as much as they first thought.

Good questions for comparing choices are: Is it a need or a want? How much does it cost? How much money will I have left? Will it help me now, later, or both? These questions build good financial habits.

Worked example: How much money is left?

Noah has $9. He buys a ruler for $2 and an eraser for $1.

Step 1: Add the costs.

The total cost is \(2 + 1 = 3\) dollars.

Step 2: Subtract from the money Noah has.

The money left is \(9 - 3 = 6\) dollars.

Noah has $6 left.

Having money left matters. If all your money is gone, you cannot buy something important later. Leaving some money unspent can be a smart choice too.

Sometimes the best financial decision is to wait and save. Saving means keeping money to use later. When a goal is important, saving helps you reach it step by step.

[Figure 3] Suppose Eva wants a soccer ball that costs $12. She has $4 now. If she spends the $4 on candy and stickers, she will still have $0 saved for the ball. But if she keeps the $4 and later adds more money, she can get closer to her goal.

If Eva gets $2 each week, then after one more week she will have \(4 + 2 = 6\) dollars. After two more weeks she will have \(6 + 2 = 8\) dollars. After four weeks of saving $2 each week, she will have \(4 + 2 + 2 + 2 + 2 = 12\) dollars. Then she can buy the soccer ball.

Saving teaches patience. It also helps with priorities because you are choosing a bigger future goal instead of a smaller now choice. That can be hard, but it is often wise.

Worked example: Saving to reach a goal

Jaden wants a book that costs $10. He already has $3 and saves $1 each week.

Step 1: Find how much more money he needs.

He needs \(10 - 3 = 7\) more dollars.

Step 2: Match the saving amount to the missing amount.

If he saves $1 each week, then he needs 7 weeks to save $7.

Jaden can reach his goal in 7 weeks.

The picture in [Figure 3] reminds us that saving is progress over time. Small amounts can grow into enough money for an important goal.

Financial decisions happen in real life every day. At school, you might choose between buying a treat and saving for a book fair. At home, a family might choose groceries before entertainment because food is a priority. In a store, someone may compare two items and pick the one with better value.

Smart decisions are not always the same for every person. One child may need new shoes. Another child may already have shoes and decide to save for art supplies. The important part is to think carefully about what matters most in that situation.

A simple plan can help: first, think about your money. Next, decide whether the choice is a need or a want. Then compare cost and benefit. Finally, choose the option that fits your priority best.

"Spend for what matters most, and save for what matters next."

When you practice these habits, you become stronger at making decisions. You learn that money is a tool. It can help you meet needs, enjoy some wants, and reach goals when you use it wisely.