Many people think taxes are an "adult problem" they can ignore until much later. That is not really true. If you earn money from a job, freelance online, get paid for tutoring, sell products, or receive tips, taxes may already be part of your life. The good news is that personal taxes are much less scary when you understand the basics and build a simple system early.

Taxes are about three practical habits: knowing what money came in, knowing what money went out, and keeping the documents that prove both. Once you can do those three things, filing a return becomes a process instead of a mystery.

Taxes are payments required by governments to help fund services like roads, schools, emergency response, and public programs.

A tax return is the form you submit to report income, claim any allowed deductions or credits, and calculate whether you owe money or should receive a refund.

A refund is money returned to you when you paid more tax during the year than you actually owed.

One important thing to understand right away is that taxes are connected to real consequences. Filing on time and keeping records can help you avoid stress, late fees, and confusion. Ignoring taxes can lead to letters you do not understand, penalties, interest, and a bigger mess later when you need financial aid records, proof of income, or documents for an apartment or job application.

If you work a part-time job, your employer may take money out of each paycheck for taxes. If too much is taken out, you may get that money back as a refund after filing. If too little is taken out, you may owe money. Either way, filing helps settle the difference.

Taxes also matter because they create a paper trail. If you ever apply for student aid, try to rent a place, open certain financial accounts, or show proof of earnings, your tax records can help. A person who keeps organized records looks more reliable and usually has fewer surprises.

Many first-time workers assume that if taxes were already taken from their paycheck, they do not need to do anything else. In reality, filing a return may be the only way to claim a refund you are entitled to receive.

Think of taxes like maintaining your phone battery. If you keep charging it regularly, things run smoothly. If you ignore it until it dies, you lose time and scramble to fix it. Tax habits work the same way.

You do not need to memorize every tax rule right now, because the exact filing requirement depends on your age, income type, and total amount earned. What matters most is recognizing the situations that can trigger a filing responsibility.

A student may need to file if they earn money from a regular job, self-employment, contract work, tips, or online gigs. Income can come from a coffee shop, mowing lawns, editing videos, streaming, reselling clothes, babysitting, coding for a client, or creating content. Money earned in different ways may be taxed differently.

The biggest practical difference is between being an employee and being self-employed. An employee usually has taxes withheld by an employer. A self-employed person often has to set aside money on their own and may owe both income tax and self-employment tax.

For example, if Maya works at a grocery store and earns $3,000 over the summer, taxes may already be withheld from her paycheck. If Jordan earns $3,000 designing logos online for clients, no one may be withholding money for taxes. Jordan has more responsibility to track income and prepare for possible tax payments.

Income type changes your tax routine

When you are paid as an employee, your employer handles more of the paperwork during the year. When you are paid as an independent worker, you are responsible for keeping much more of your own tax information. That is why two people earning the same amount can have very different tax experiences.

Another thing to watch for is mixed income. You might have a regular job and also make money from side work. In that case, you may receive more than one type of tax document and need records from both.

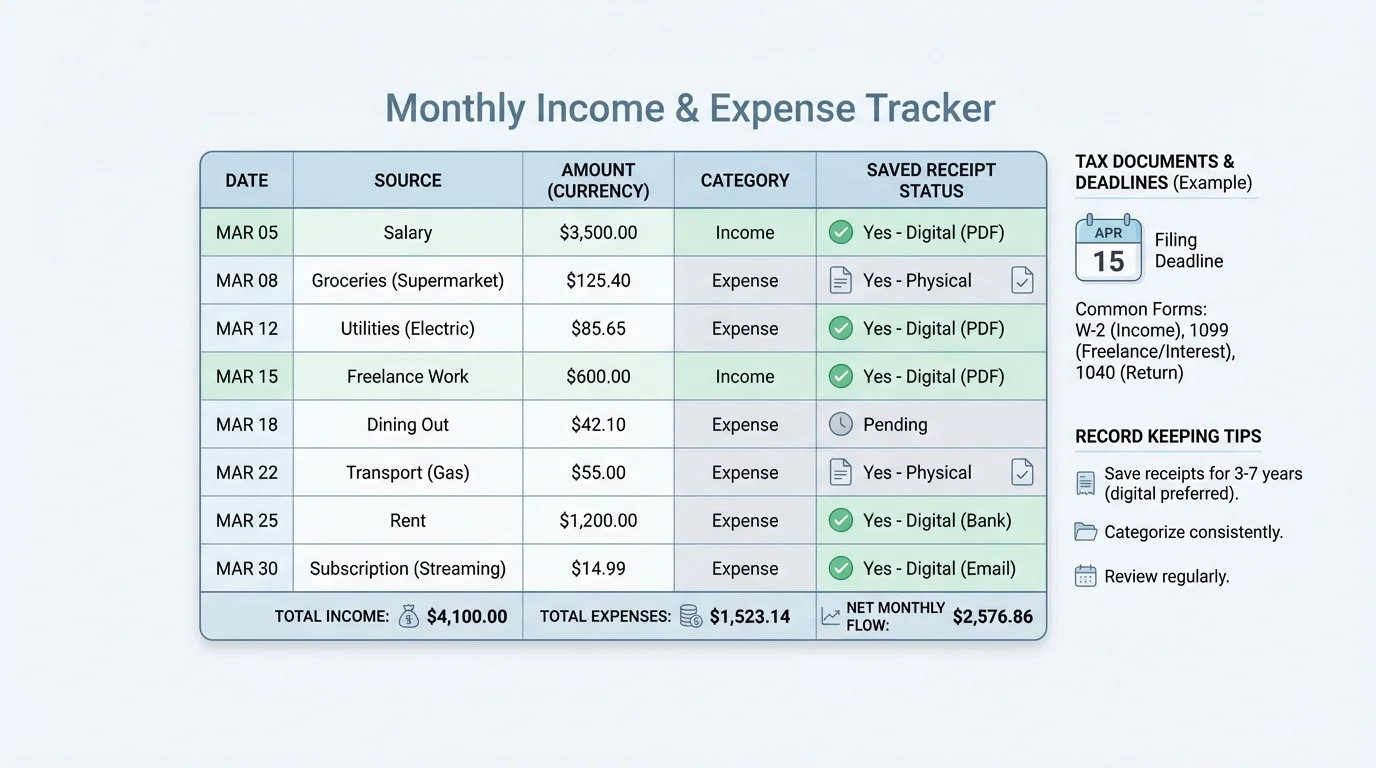

The easiest way to make tax season manageable is to use a simple recordkeeping system all year, as shown in [Figure 1]. You do not need a complicated app. A spreadsheet, notes app, or cloud folder can work if you use it consistently.

For income, track the date, who paid you, what the work was, how much you received, and how you were paid. For expenses, track the date, what you bought, why it was related to earning income, and save the receipt. If you are self-employed, this matters much more because some business-related expenses may reduce your taxable income.

A basic monthly tracker might include columns for date, description, income amount, expense amount, category, and receipt saved. If you earned $45 from tutoring, $120 from pet sitting, and spent $18 on printed flyers for your tutoring service, your records should show all three clearly.

Here is a practical rule: if money moves, record it. Do not trust your memory. A payment app history helps, but it is not enough by itself because you still need notes about what the transaction was for.

Categories can keep things organized. Income categories might include wages, tips, freelance work, sales, or interest. Expense categories might include supplies, advertising, software, mileage, or equipment if those expenses are genuinely connected to earning money.

Suppose you earn $600 from selling handmade bracelets online and spend $95 on beads, shipping supplies, and listing fees. Your net income is calculated as income minus qualifying expenses: \(600 - 95 = 505\). That does not mean every expense is automatically allowed, but it shows why careful tracking matters.

Saving documents matters too. Keep digital copies of receipts, invoices, and payment confirmations in labeled folders by month or category. Later, when you need to confirm an amount, you will not be digging through screenshots for hours. This organized system works just like the tracker in [Figure 1], where each transaction has a category and proof attached.

Simple tracking setup you can start today

Step 1: Create one folder called "Taxes."

Inside it, make subfolders for income forms, receipts, pay stubs, and filed returns.

Step 2: Make a tracker.

Use columns for date, source, description, income, expense, category, and notes.

Step 3: Update it weekly.

Spending five minutes each week is much easier than trying to rebuild a whole year later.

Step 4: Save proof immediately.

Upload receipts or screenshots the same day you receive or spend money.

If you are only earning wages from a job, your expense tracking may be less important for taxes, but it is still a strong money habit. It helps you see what you earn versus what you keep, which is an important part of financial literacy.

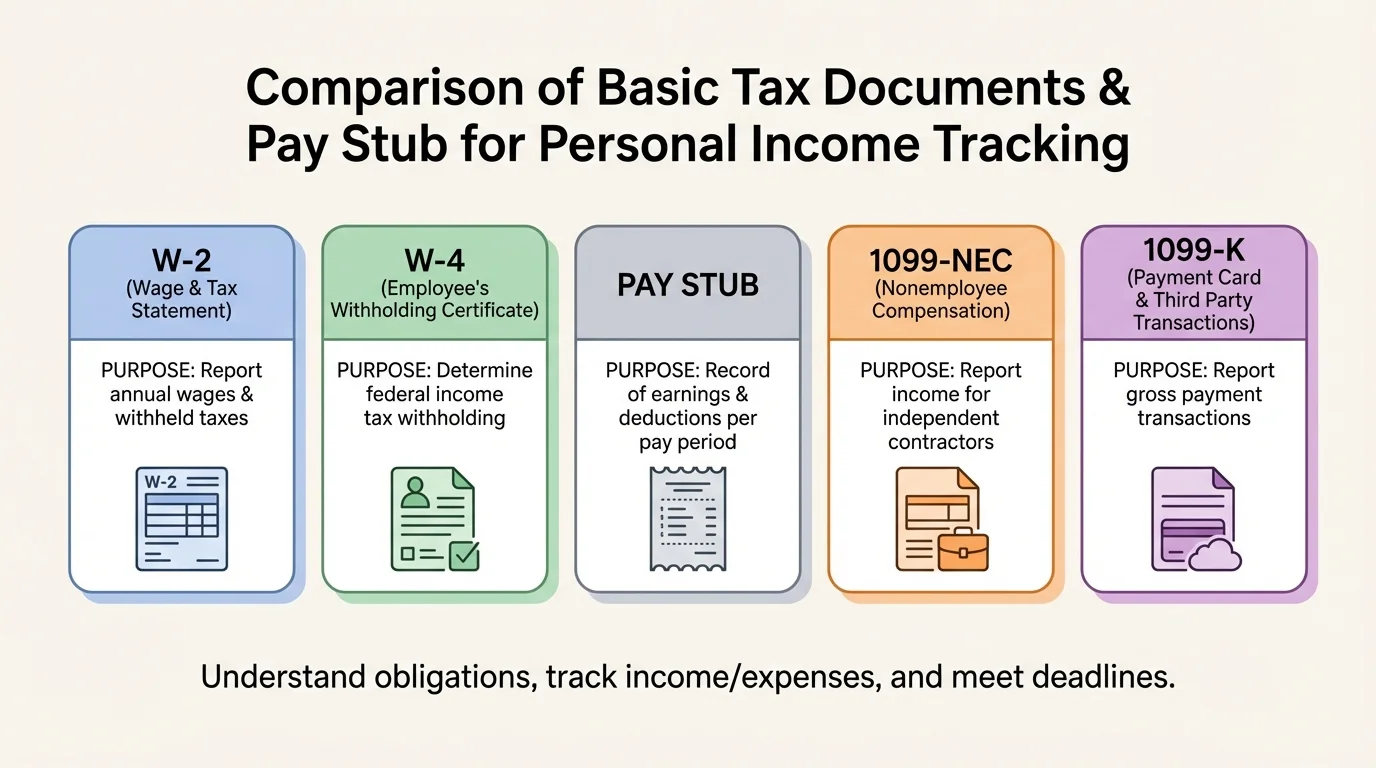

[Figure 2] The main tax papers can feel confusing at first, but they fit into a few simple categories: forms about your job setup, forms reporting what you earned, and forms you use when filing your return.

A W-4 is usually completed when you start a job. It tells your employer how to handle tax withholding from your paycheck. It does not report what you already earned; it helps set up withholding going forward.

A W-2 is sent by an employer after the year ends. It reports wages you earned and taxes withheld. If you worked as an employee, this is one of the most important forms you will use when filing.

A 1099-NEC usually reports nonemployee compensation, often for freelance or contract work. A 1099-K may report payments processed through third-party platforms in certain situations. Even if you do not receive a form, income can still be taxable, which is why your own records matter.

Your pay stub is not the same as a tax form, but it is still useful. It shows gross pay, deductions, and net pay. Gross pay is the amount before deductions. Net pay is what you actually receive after deductions.

| Document | What it does | When you usually see it | Why it matters |

|---|---|---|---|

| W-4 | Sets tax withholding at a job | When starting a job | Affects how much tax is taken from paychecks |

| W-2 | Reports employee wages and tax withheld | After the year ends | Used to prepare a tax return |

| 1099-NEC | Reports contract or freelance pay | After the year ends | Shows nonemployee income |

| 1099-K | Reports certain platform payment transactions | After the year ends | Helps verify income from payment platforms |

| Pay stub | Shows paycheck details | Each pay period | Helps monitor earnings and withholding |

Table 1. Common tax-related documents and what each one is used for.

When you compare forms, look for your name, address, taxpayer identification information, the tax year, and the amounts reported. Mistakes happen. If your name is misspelled or income looks wrong, contact the employer or payer quickly.

Later, when you file, the wage and withholding details from forms like the W-2 become the backbone of your return. That is why the comparison in [Figure 2] matters: each document plays a different role, and mixing them up can lead to errors.

If you have learned about reading a paycheck, bring that skill here. Taxes are easier when you already know the difference between money earned, money withheld, and money received.

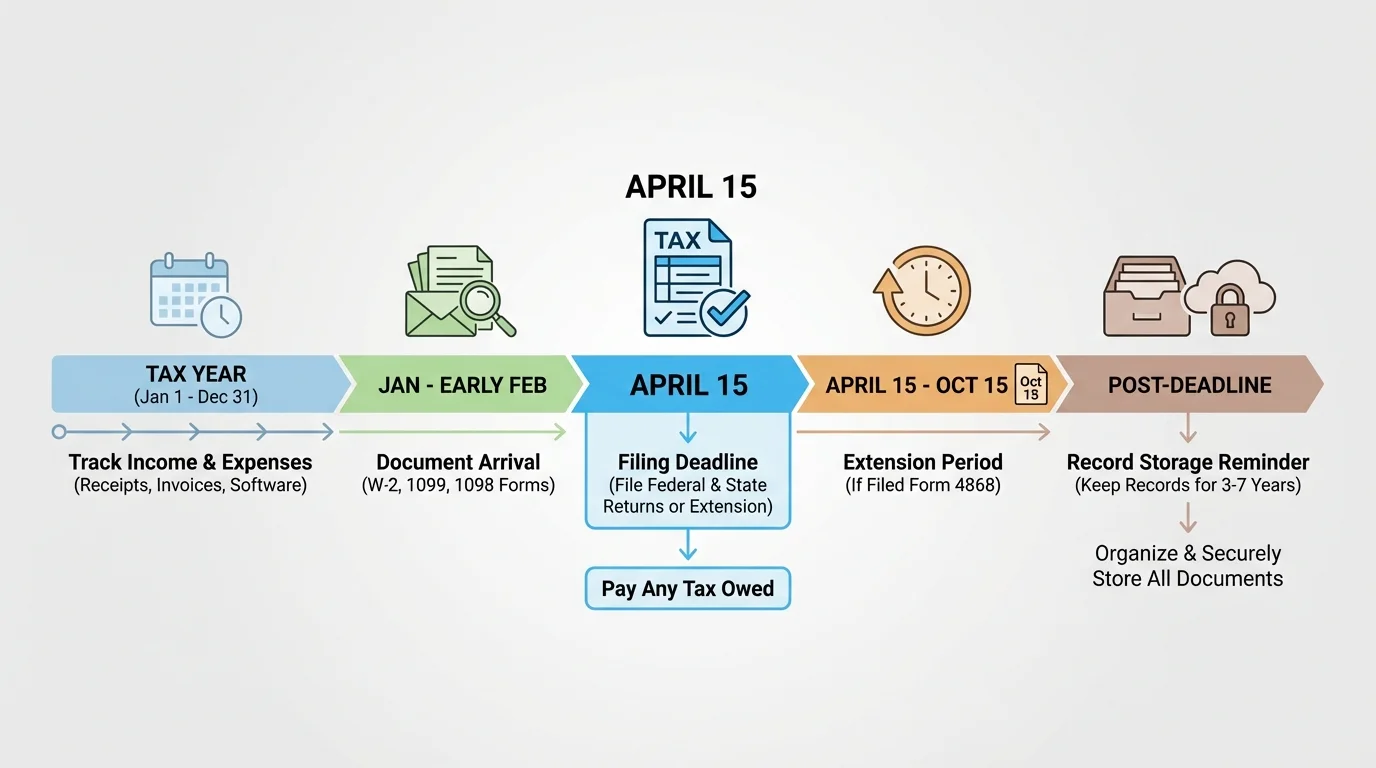

[Figure 3] Taxes follow an annual rhythm, and that yearly flow is easier to understand when you picture it as a timeline. You earn income during the year, receive many forms after the year ends, and usually file your tax return in the spring.

For many people in the United States, the main federal filing deadline is around mid-April for the previous tax year. Exact dates can shift slightly, so checking the current year matters. Waiting until the last minute is risky because you may discover missing documents or mistakes when there is no time left to fix them.

You can sometimes request an extension to file, but an extension to file is not the same as an extension to pay. If you owe tax, interest and penalties can still grow on unpaid amounts. That is a costly misunderstanding.

Some people with self-employment income may also need to make estimated taxes during the year instead of waiting until the end. This usually applies when not enough tax is being withheld from payments and you expect to owe enough tax to require periodic payments.

It also helps to know how long to keep records. A safe habit is to keep tax returns and supporting documents for several years. Digital storage makes this much easier than keeping only paper copies.

Deadlines protect you from extra costs

Filing late, paying late, or ignoring notices can lead to penalties and interest. Those extra charges do not buy you anything useful; they are simply the price of delay. Meeting deadlines keeps more of your money in your control.

If you build your system early, deadlines become checkpoints instead of emergencies. The sequence in [Figure 3] works best when you gather forms as they arrive instead of waiting for all of them to pile up.

Filing a simple return is usually a process of collecting forms, entering information accurately, reviewing it, and submitting it on time. The details depend on your situation, but the overall path stays similar.

Step 1: Gather your documents. This may include a W-2, 1099 forms, your Social Security number or taxpayer ID information, bank account details for direct deposit, and your income and expense records.

Step 2: Check whether your information matches across documents. Your name, address, and identification details should be consistent.

Step 3: Enter income information. If you are using filing software, follow prompts carefully. If a form says you earned $1,850, enter $1,850, not a rounded guess.

Step 4: Add any qualifying deductions, credits, or business expenses if they apply. This is one reason organized records matter. You cannot claim what you cannot support.

Step 5: Review the result. The return will generally show whether you owe tax or should receive a refund.

Step 6: File and save proof. Keep a copy of the filed return, confirmation emails, and payment or refund details.

Worked example: estimating net self-employment income

Leah earns $1,200 designing social media graphics and spends $140 on software and $35 on stock images directly related to client work.

Step 1: Add qualifying expenses.

The total expense amount is \(140 + 35 = 175\).

Step 2: Subtract expenses from income.

Leah's net income is \(1,200 - 175 = 1,025\).

Step 3: Save proof for both numbers.

She should keep client payment records and receipts for the software and images.

The important takeaway is that organized records make the calculation straightforward: \(1,200 - 175 = 1,025\).

If you are getting a refund, direct deposit is often the fastest option. If you owe money, make sure you understand the payment method and keep confirmation records. Never assume a payment went through without checking.

One common mistake is assuming no form means no tax. That is false. If you earned money, you may still need to report it, even if no document arrived in the mail or by email.

Another mistake is mixing personal spending with business expenses. If you buy headphones mostly for entertainment, you usually cannot call them a business expense just because you sometimes use them while working. Be honest and specific.

Students also struggle because of poor organization. Screenshots with unclear filenames, lost login information, and forgotten payment app histories can turn a simple return into a frustrating scavenger hunt.

"What gets tracked gets managed."

— A useful financial rule of thumb

Scams are another real risk. Tax scammers may send texts, emails, or calls claiming urgent problems or demanding gift cards, wire transfers, or immediate payment. Real tax agencies follow formal procedures and do not resolve serious tax issues through random threats on social media or text messages.

Smart habits are simple: update records weekly, read your pay stub, save forms as soon as they arrive, verify names and amounts, and file before the deadline. These habits take very little time compared with the time lost fixing mistakes.

Scenario 1: Employee with a part-time job. Ava works weekends at a restaurant. She gets pay stubs every two weeks and receives a W-2 after the year ends. Her best move is to keep all pay stubs, compare them to the W-2, and file if required so she does not miss a possible refund.

Scenario 2: Freelancer paid online. Eli edits videos for creators and gets paid through an online platform. Some clients send forms, some do not. Eli needs his own tracker because his tax responsibility does not disappear when paperwork is inconsistent.

Scenario 3: Mixed income. Nia works at a retail store and also sells custom digital art. She may have both employee income and self-employment income. That means she needs both wage documents and separate records for art income and related expenses.

Case study: comparing two students

Student A: Keeps every pay stub, updates a spreadsheet weekly, and saves receipts in a cloud folder.

When tax forms arrive, filing takes a short amount of time because the records are ready.

Student B: Relies on memory, deletes emails, and never tracks side-gig income.

At tax time, this student has to guess amounts, search old accounts, and risks missing income or making errors.

The difference is not intelligence. It is system design.

You do not need to become a tax expert this year. You do need to become organized, careful, and aware of deadlines. Those three skills will protect you whether your income comes from one paycheck or five different apps.