A lot of people your age can name phone plans faster than health plans, even though one bad medical decision can cost far more than a year of streaming subscriptions. That is not because healthcare is impossible to understand. It is because the system often uses confusing words, hidden rules, and stressful timing. Learning how it works now gives you an advantage later, especially when you start working, move out, age out of a parent or guardian's support, or need care quickly.

As a young adult, you may feel generally healthy, which can make health insurance and healthcare systems seem like "future you" problems. But this is exactly the stage when practical knowledge matters. Sports injuries, mental health support, birth control, infections, prescriptions, therapy, skin issues, dental pain, and sudden emergencies can all show up with no warning. If you know where to go, what to ask, and what costs to expect, you are more likely to get help early instead of waiting until a problem gets worse.

Good healthcare decisions are not just about health. They affect your money, time, schoolwork, job attendance, privacy, and stress level. Someone who gets a preventive checkup and catches a problem early may pay much less than someone who ignores symptoms and later needs emergency care. Someone who understands their plan's network may avoid a surprise bill. Someone who knows their rights may speak up when a charge or denial seems wrong.

Health system means the way a country or region organizes healthcare services, funding, rules, and access. Access to care means how easily a person can get the right care at the right time. Health insurance is a contract that helps pay for medical costs in exchange for set payments and shared costs.

When you evaluate a health system, do not just ask, "Is it good?" Ask more useful questions: How easy is it to get an appointment? How much does care cost people directly? Are mental health and preventive services included? Can people in rural areas or low-income communities actually use the services? Are wait times reasonable? Are patients protected from huge medical bills?

Different places organize healthcare in different ways. In a public system, the government plays a major role in funding or providing care. In a private system, private companies and employers often play a bigger role. Many places use a mixed model, combining public programs with private insurance and private healthcare providers. In real life, most systems are not purely one type.

For you, the practical difference shows up in questions like these: Do people get basic care even if they have low income? Are there long wait times for specialists? Do patients need to choose from many insurance plans? Can they see a doctor without worrying about a giant bill? A system might offer broad coverage but slower specialty access, or faster access for some people but high costs for others.

One simple way to evaluate a health system is to look at four things: cost, coverage, quality, and convenience. Cost means what patients pay directly and through taxes or premiums. Coverage means which services and people are included. Quality includes safety, outcomes, and patient experience. Convenience includes wait times, location, online scheduling, telehealth, and whether care is easy to understand.

| Feature | What it asks | Why it matters to you |

|---|---|---|

| Cost | How much do patients pay? | Affects whether you delay care or seek help early. |

| Coverage | What services are included? | Determines whether therapy, prescriptions, or preventive care are affordable. |

| Quality | Does care actually help people? | Good access means less if the care is poor. |

| Convenience | How easy is it to use? | Long travel, long waits, or confusing systems reduce real access. |

Table 1. Four practical categories for evaluating a health system from a patient perspective.

Try This: The next time you hear someone say a healthcare system is "better" or "worse," test the claim using those four categories. You do not need to become a policy expert to ask smart questions.

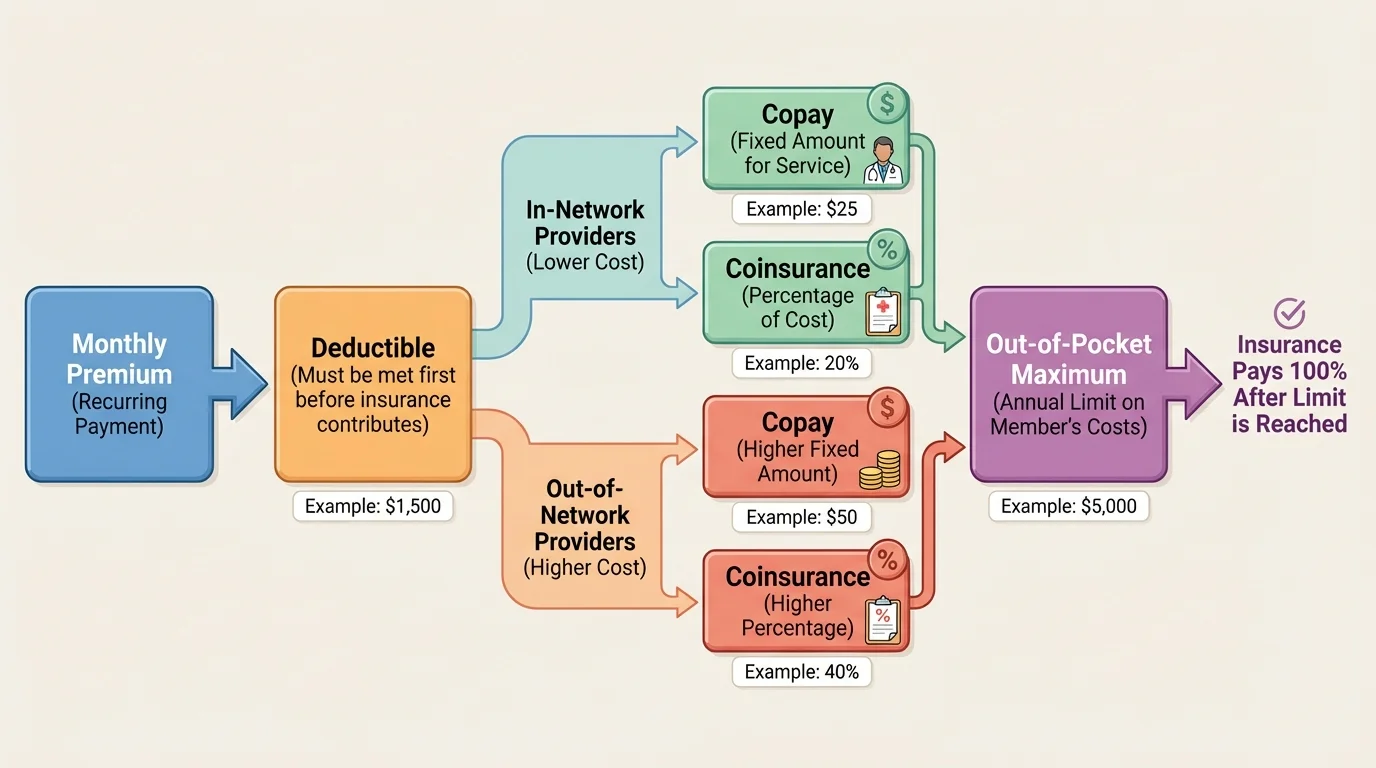

Insurance language sounds technical, but the main idea is simple: you and/or someone on your behalf pay regular amounts so that a large medical cost does not fully land on you alone. The tricky part is that shared costs happen in layers, as [Figure 1] shows, so you need to understand how the pieces connect before you compare plans.

Your premium is the amount paid each month to keep the insurance active. You pay it whether you use care or not. A deductible is the amount you usually pay for covered services before the plan starts sharing more of the cost. A copay is a fixed amount, like $25 for a visit. Coinsurance is your percentage of a bill after the deductible, such as paying 20% or 30% while the plan pays the rest. Your out-of-pocket maximum is the most you pay for covered in-network care in a plan year before the insurer pays 100% of covered costs.

Another major term is network. A network is the group of doctors, clinics, hospitals, and pharmacies that have a contract with your insurance company. In-network care is usually cheaper. Out-of-network care can be much more expensive, and sometimes it is not covered at all except in emergencies. This is why checking a provider's network status before a visit matters so much.

You may also run into prior authorization. That means your insurer wants approval before it will cover certain medicines, tests, or treatments. It does not always mean "no." It often means paperwork, waiting, or proof that a treatment is medically necessary. If you do not know this rule exists, you might assume your doctor's prescription is automatically covered when it is not.

How cost-sharing changes your behavior

Low premiums can look attractive, but they often come with higher deductibles or other costs when you actually need care. Higher premiums can feel annoying each month, but they may reduce what you pay when you visit doctors often, take prescriptions, or receive therapy. The best plan is not always the cheapest monthly plan. It is the one that fits your likely health needs and protects you from large surprise costs.

Think of it this way: a plan with a $0 premium but a very high deductible may be okay for someone who rarely uses care and has savings for emergencies. A plan with a higher monthly premium might be smarter for someone with regular prescriptions, counseling appointments, or a health condition that needs monitoring.

When people compare health plans, they often focus on one number and ignore the others. That is a mistake. You need to compare the full picture: premium, deductible, copays, coinsurance, out-of-pocket maximum, network, prescription coverage, and whether your preferred clinic or therapist is included.

Suppose Plan A has a monthly premium of $80 and Plan B has a monthly premium of $160. Over a year, Plan A costs $960 in premiums because \(80 \times 12 = 960\), while Plan B costs $1,920 because \(160 \times 12 = 1,920\). At first, Plan A looks clearly cheaper. But if Plan A has a $3,000 deductible and Plan B has a $500 deductible, Plan B may save money if you actually need several visits, tests, or prescriptions.

Comparing two plans for a year with moderate healthcare use

You expect \(6\) therapy visits with a $30 copay each, \(4\) primary care visits with a $25 copay each, and one lab bill where you pay $400 under Plan A or $100 under Plan B after the plan rules apply.

Step 1: Add annual premiums.

Plan A: \(80 \times 12 = 960\)

Plan B: \(160 \times 12 = 1,920\)

Step 2: Add visit costs.

Therapy: \(6 \times 30 = 180\)

Primary care: \(4 \times 25 = 100\)

Total visit copays: \(180 + 100 = 280\)

Step 3: Add the lab costs.

Plan A total: \(960 + 280 + 400 = 1,640\)

Plan B total: \(1,920 + 280 + 100 = 2,300\)

In this example, Plan A still costs less overall. But if you expected surgery, frequent prescriptions, or many specialist visits, Plan B could become the better deal. You have to compare based on likely use, not guesses.

Try This: If your household has plan documents, look for the "Summary of Benefits and Coverage." Find the premium, deductible, and out-of-pocket maximum first. Those three numbers tell you a lot very quickly.

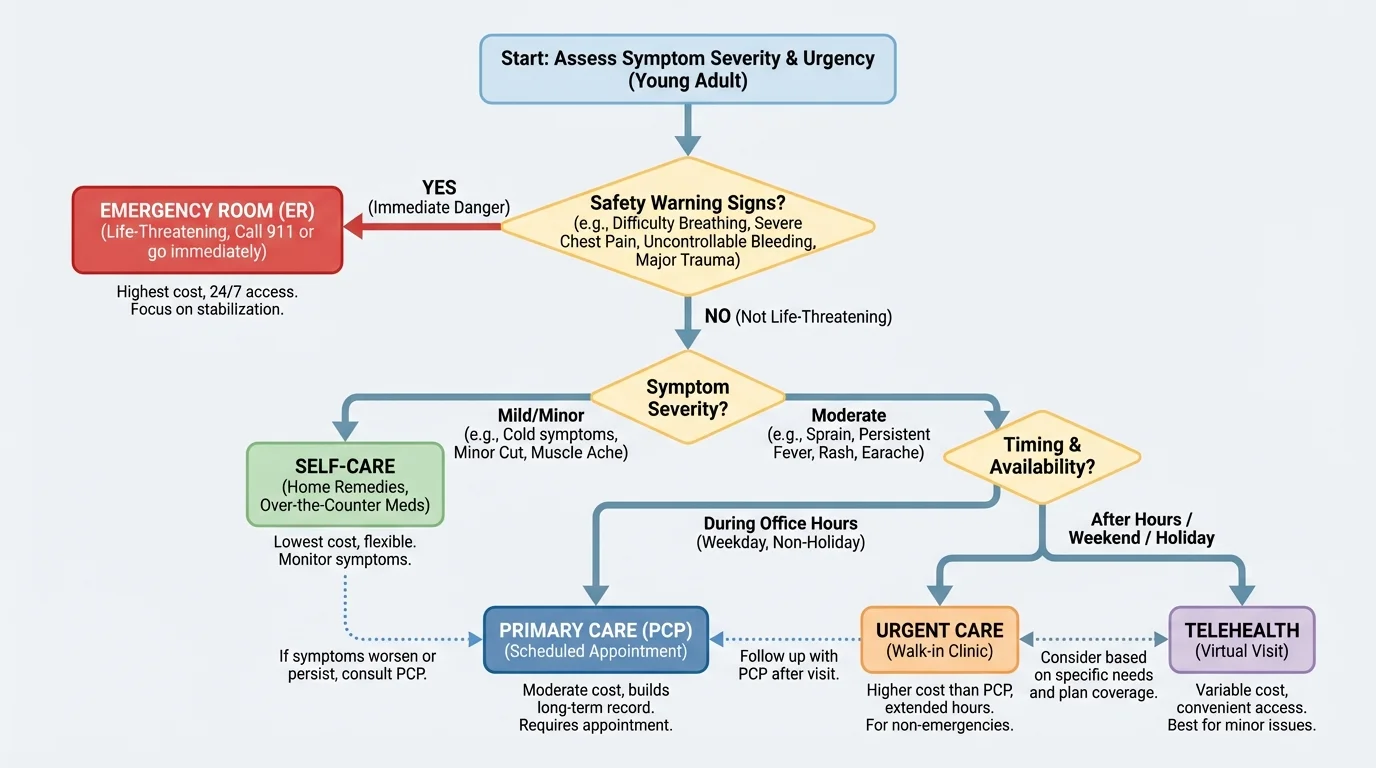

Getting care is not only about having insurance. It is also about choosing the right place. That choice affects cost, speed, and the type of help you receive. The decision path in [Figure 2] makes this easier: not every health problem belongs in an emergency room, and not every issue should wait weeks for a routine appointment.

Primary care is your regular healthcare home for checkups, vaccines, referrals, basic illness, and long-term health questions. Urgent care is useful when you need same-day help for problems that are not life-threatening, such as a painful ear infection, minor cuts, or a sprain. The emergency department is for severe symptoms like trouble breathing, signs of stroke, severe chest pain, major injury, or uncontrolled bleeding. Telehealth works well for many follow-ups, medication questions, mild illness, and some mental health visits.

Mental healthcare matters too. Counseling, therapy, crisis lines, support groups, and psychiatric care are all part of healthcare access. A strong health system does not treat mental health as optional. If someone can get an X-ray quickly but waits months for therapy, access is incomplete.

Reproductive and sexual healthcare are also important for many young adults. This can include birth control, STI testing, pregnancy care, menstrual concerns, and questions about sexual health. The right care setting depends on the concern, but the key point is that preventive and confidential care often leads to better outcomes than waiting until there is a crisis.

Preventive care is often covered at lower cost than treatment after a problem gets worse. Vaccines, screenings, and routine checkups may save both money and stress by catching issues early.

If you are unsure where to go, a nurse advice line, telehealth service, or your primary care office can often guide you. As with the route choices in [Figure 2], the safest option is to go straight to emergency care if symptoms are severe or life-threatening.

Even in places with doctors and hospitals, people may still struggle to get care. That is why access means more than "services exist somewhere." Barriers include cost, transportation, lack of internet, long waits, limited clinic hours, not understanding insurance, language differences, disability access issues, fear of judgment, and lack of nearby providers.

Young adults often face privacy concerns too. You may worry that someone on your insurance plan will see explanations of benefits, or you may feel uncomfortable discussing mental or sexual health. The exact privacy rules depend on age, location, and the type of care, so it is smart to ask the clinic directly: "How are visits and billing communications handled?" and "What stays confidential?"

Here are practical ways to reduce barriers: ask about sliding-scale fees if you do not have strong coverage; check for community clinics; request telehealth if transportation is a problem; use online portals for faster messaging; ask for interpreter services if needed; and schedule preventive care before a problem becomes urgent. If a provider is out of network, ask whether there is a similar in-network option nearby.

| Barrier | What it looks like | Practical response |

|---|---|---|

| Cost | You avoid visits because the bill feels unpredictable. | Ask for estimated charges, financial assistance, or lower-cost in-network options. |

| Transportation | You cannot easily get to a clinic. | Use telehealth, public transit planning, or community transportation support. |

| Scheduling | Appointments are booked for weeks. | Ask for cancellation lists, urgent slots, or another provider in the practice. |

| Language | You cannot fully understand forms or instructions. | Request an interpreter and written instructions in your preferred language. |

| Privacy | You worry who will see your information. | Ask how records, portals, and billing notices are handled. |

Table 2. Common barriers to healthcare access and realistic ways to respond.

When barriers are ignored, small issues can become big ones. A missed prescription refill can trigger an asthma attack. Delaying therapy can make everyday functioning harder. Skipping a preventive visit can mean a condition is found later, when treatment is more intense and expensive.

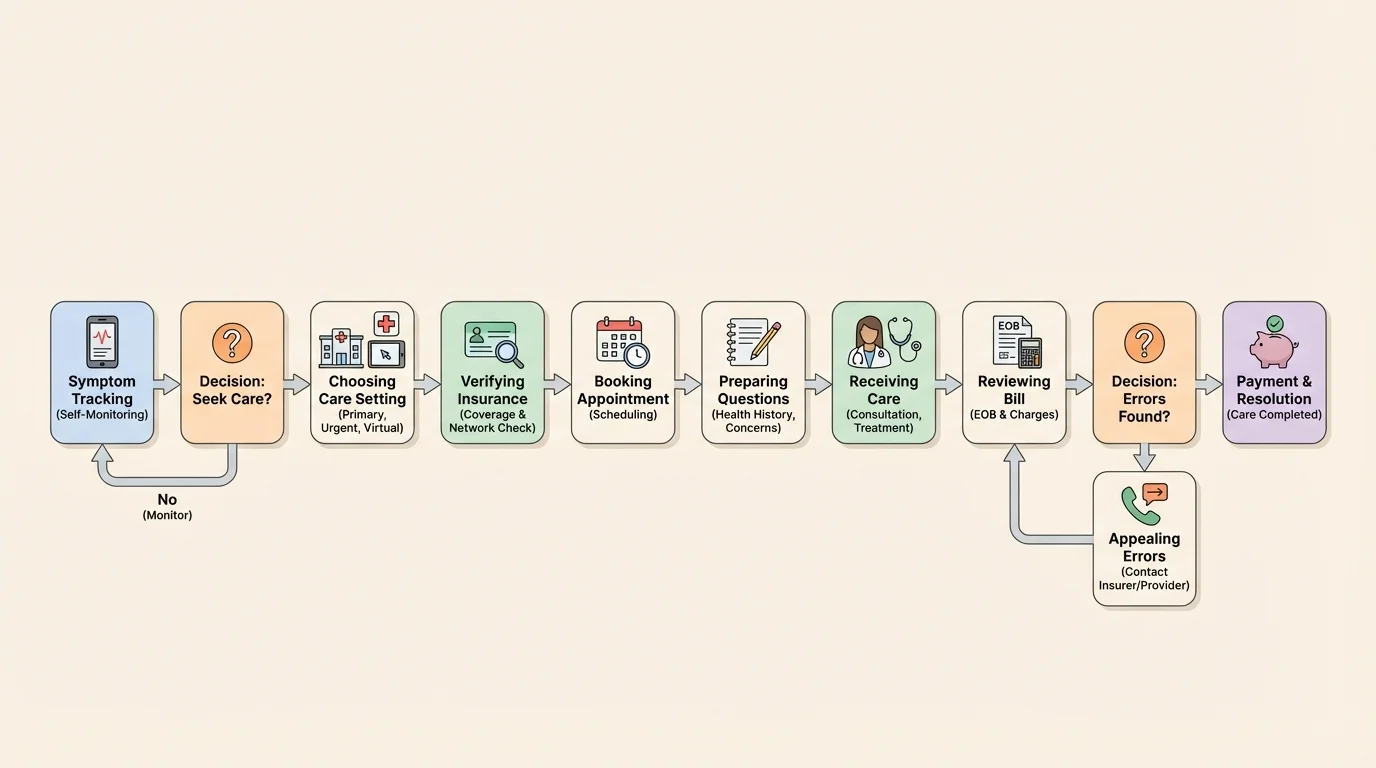

Healthcare works better when you treat it like a process, not a mystery. The sequence in [Figure 3] shows that a good outcome often depends on what you do before and after the visit, not just during the appointment itself.

Step 1: Notice the problem clearly. Write down symptoms, when they started, what makes them better or worse, and any medicine you already took. This helps you explain the issue accurately.

Step 2: Check where to go. Decide whether it fits self-care, telehealth, primary care, urgent care, or emergency care. If unsure, call a nurse line or clinic.

Step 3: Verify coverage. Ask whether the provider is in network, whether the service needs prior authorization, and what your estimated cost may be. This step often prevents surprise bills.

Step 4: Prepare for the visit. Bring your insurance card if you have one, photo ID if required, a medication list, allergies, and your questions. If the issue is emotional or complex, write your questions in advance so stress does not make you forget them.

Step 5: During the visit, ask direct questions: What do you think is happening? What are my treatment options? What are the risks or side effects? When should I follow up? What symptoms mean I need urgent help? If you do not understand something, say so. That is not rude; it is responsible.

Step 6: Review the after-visit instructions and any bill or explanation of benefits. A bill is not always the same as your final patient responsibility. Sometimes it arrives before insurance finishes processing. Compare the provider bill with the insurer's explanation of benefits before paying if something looks off.

Handling a possible billing error

You go to an in-network clinic and later receive a large bill that seems wrong.

Step 1: Compare documents.

Check the bill against the insurer's explanation of benefits. Look for provider name, service date, and whether the claim was marked in network.

Step 2: Call with a script.

Say: "I'm reviewing this charge and I think there may be an error. Can you explain how this amount was calculated and whether insurance has fully processed the claim?"

Step 3: Escalate if needed.

If the answer is unclear, call the insurer, ask for a claim review, and write down the date, time, and the representative's name.

Many billing problems are fixed by careful follow-up, not panic-paying the first amount you see.

Later, if you need to repeat the process for another issue, [Figure 3] still applies: organize the problem, verify coverage, prepare, ask questions, and review the result.

You have the right to ask questions, receive understandable information, request copies of records, seek a second opinion, and speak up about safety concerns. In many places, you also have rights related to privacy and nondiscrimination. But rights are strongest when you use them actively.

You also have responsibilities. Give accurate health information. Follow medication directions carefully. Show up for appointments or cancel early. Read forms before signing. Keep copies of bills, test results, and insurance messages. If you move, update your address and contact information so time-sensitive medical notices do not get lost.

"The most powerful patient is an informed patient."

Be alert for scams. Fake insurance plans, false online pharmacies, and suspicious messages asking for payment or personal information are real risks. Use official insurer websites, verified clinic contact information, and licensed pharmacies. If a deal sounds unrealistically cheap or urgent, slow down and verify it.

Another safety skill is knowing your emergency information. Keep a list in your phone of allergies, medications, emergency contacts, health conditions, and insurance details if you have them. In stressful moments, you may not remember everything clearly.

You do not need to wait for a crisis to get organized. Build a simple personal health plan for the next year. Choose a primary care provider if possible. Save the clinic phone number. Know where the nearest urgent care and emergency room are. Learn whether telehealth is covered. Keep a list of medications and allergies. If you use glasses, counseling, prescriptions, or regular treatment, set reminders before refills run out.

If you are covered under a family plan, ask practical questions now: Which doctors are in network? How do referrals work? Where can I find the member ID? What happens if I need care while traveling? If you are not insured or your coverage is limited, look into community clinics, public programs you may qualify for, and local health resources before you urgently need them.

Try This: Create a note on your phone called "Health Info." Add your birth date, emergency contact, allergies, medications, insurance member number if applicable, preferred pharmacy, and one nearby clinic. That small step can save real time later.

Being good at healthcare navigation does not mean you will never face delays, confusion, or unfair costs. It means you are less likely to get stuck. You can evaluate a system by whether it helps people get affordable, timely, quality care, and you can protect yourself by knowing how to use the parts that affect your life most directly.