Much adult stress starts with one simple mistake: signing something you did not fully read. A lease can lock you into monthly payments. A loan can cost far more than the amount you borrowed. A job document can affect your schedule, pay, privacy, and even whether you can be fired without warning. Learning to read contracts is not just about being careful. It is about protecting your money, your time, and your future.

Contracts show up earlier than many people expect. You might rent your first apartment, finance a car, sign up for a phone plan, accept a part-time job, or agree to a gym membership. Some contracts are short and straightforward. Others are full of legal language that feels designed to make people skim. Your goal is not to become a lawyer. Your goal is to become someone who knows what they are agreeing to before they say yes.

A contract is a legally enforceable agreement between two or more parties. In plain language, it is a promise with consequences. If you agree to do something and the other side also agrees, the document usually creates responsibilities for everyone involved. That means a contract is not just information. It is a commitment.

In civic and community life, contract awareness matters because many adult systems run on written agreements. Landlords, employers, lenders, service providers, and government-related institutions often expect you to sign forms that affect your rights and duties. When you understand those forms, you are more likely to act responsibly, avoid conflicts, and speak up when something is unfair or misleading.

Contract means a legally binding agreement. Clause means a specific section or rule within the contract. Obligation means something you are required to do. Penalty means a consequence, often financial, for breaking the agreement.

Good contract reading can prevent expensive mistakes. If you miss a late fee on a loan, your total cost increases. If you miss an auto-renewal date on a lease, you may owe more rent than expected. If you ignore an employment policy, you might lose a job opportunity or face discipline at work. On the other hand, when you read carefully, ask questions, and save copies, you put yourself in a much stronger position.

Most contracts, even very different ones, have a few basic features in common. First, they identify the parties involved. Second, they describe what each side agrees to do. Third, they explain what happens if someone does not follow the agreement. Fourth, they include timing, such as start dates, due dates, or end dates. Fifth, they usually contain signatures or another formal way to show consent.

As you read, look for these basic questions: Who is involved? What am I agreeing to? What is the total cost? When do payments or actions happen? What happens if I change my mind, pay late, quit, move out, or break a rule? If the contract does not clearly answer those questions, you should slow down.

The most important contract habit is separating what someone says from what the document actually says. Verbal promises can be forgotten, denied, or misunderstood. If a salesperson, landlord, or manager tells you something important, ask for that promise to appear in writing before you sign.

Another key point is that signing quickly does not make you mature; reading carefully does. Pressure tactics such as "This deal expires in ten minutes" or "Everybody signs this without reading it" are warning signs. Responsible adults do not rush major commitments just to avoid feeling awkward.

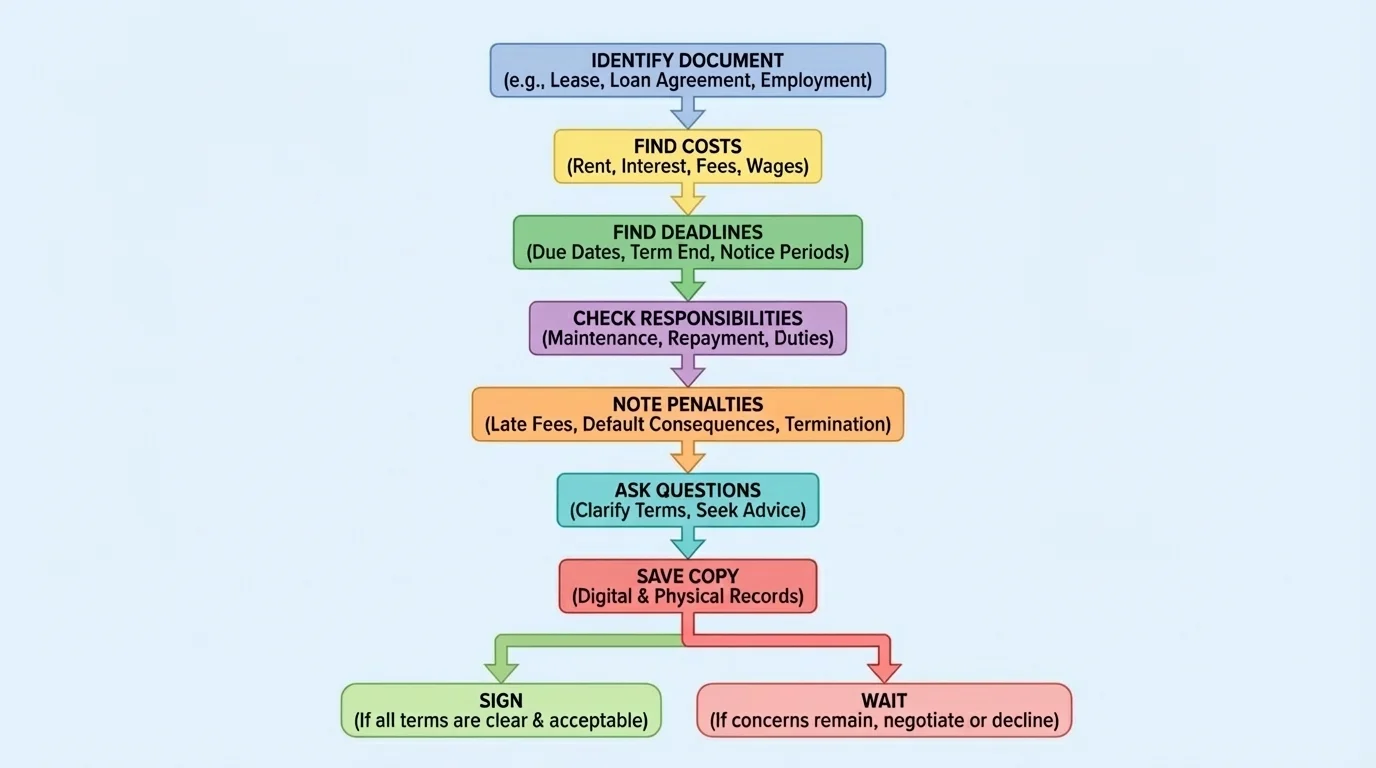

You do not need a perfect memory to review a clause-heavy document well. You need a repeatable process, and [Figure 1] shows a useful order: identify the document, find the money details, find the deadlines, check responsibilities, look for penalties, ask questions, and save a copy before you decide.

Step 1: Identify what type of document it is. Is it a lease, a loan, an offer letter, a policy acknowledgment, or something else? Different documents create different risks.

Step 2: Find every cost. Look for rent, monthly payment, deposit, fees, charges for late payment, repair costs, cancellation costs, and automatic increases. Do not focus only on the advertised number. Focus on the total financial commitment.

Step 3: Mark every date. Contracts often become expensive because people miss dates, not because they misunderstand the main idea. Look for due dates, renewal dates, move-in or move-out dates, grace periods, and deadlines for canceling.

Step 4: List your responsibilities in plain language. For example: "I must pay by the first of the month," "I must give thirty days' notice," or "I must keep company information private." If you cannot rewrite the contract in simple words, you probably do not understand it yet.

Step 5: Find the consequences. What happens if you pay late, lose your job, damage property, miss work, or want to end the agreement early? This is where many contracts become much more serious than they first appear.

Step 6: Ask questions before signing, not after. Use email when possible so there is a record. Save screenshots, PDFs, and messages in one folder.

That review process is useful beyond the documents in this lesson. As we saw in [Figure 1], the same sequence works for subscriptions, phone plans, insurance forms, and online service agreements. The exact terms change, but the habits stay useful.

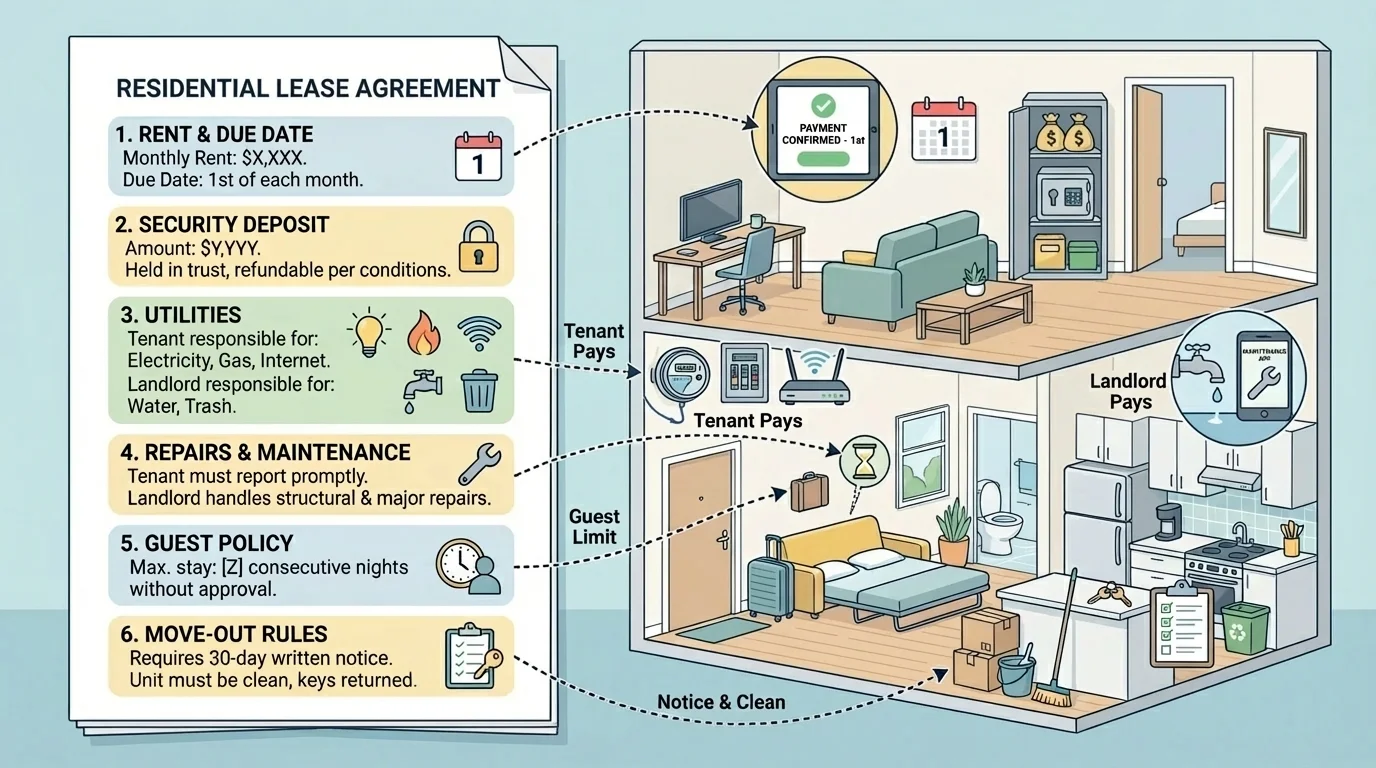

[Figure 2] A lease is a contract for using property, usually housing, for a set period of time. In a lease, the main exchange is simple: you pay rent, and the landlord provides a place to live under certain terms. The common sections shown in the figure deserve your attention first.

Start with the basic money terms: monthly rent, due date, accepted payment methods, late fee, and security deposit. A security deposit is money held in case of unpaid rent or property damage beyond normal wear. Ask exactly when it can be kept, when it should be returned, and what counts as damage.

Next, check who pays for utilities such as electricity, water, internet, and trash. A place that looks affordable at first may cost much more once utility bills are added. If rent is $900 and utilities average $180, your monthly housing cost is not $900. It is approximately \(\$900 + \$180 = \$1,080\).

Then read the rules about repairs and maintenance. Who handles broken appliances? How do you submit repair requests? Are there rules about guests, pets, parking, noise, smoking, or decorating? A lease can also limit subletting, meaning you may not be allowed to let someone else take over your space without permission.

Length matters too. Some leases are month-to-month, while others last for a fixed term such as twelve months. A fixed-term lease may offer stability, but it can also make moving out early expensive. Look for the early termination clause. It explains what happens if you need to leave before the lease ends.

Lease example: moving out early

You sign a twelve-month lease at $950 per month. After four months, you need to move for work.

Step 1: Find the early termination rule.

The lease says you must pay a fee equal to two months of rent if you leave early.

Step 2: Calculate the fee.

Two months of rent equals \(\$950 + \$950 = \$1,900\).

Step 3: Check for added responsibilities.

The lease also says you still owe rent until a new tenant is found unless local law says otherwise.

Leaving early may cost far more than expected, so this clause deserves close attention before you sign.

Move-out conditions are just as important as move-in conditions. Take photos when you move in and when you move out. Keep copies of inspection forms. Later, if there is a dispute over the security deposit, your records matter. This is one place where legal awareness protects your money in a very practical way.

Several lease issues become easier to compare when you think back to [Figure 2]: the money terms, property rules, and exit rules all work together. A low rent number may hide stricter guest rules, repair duties, or move-out penalties.

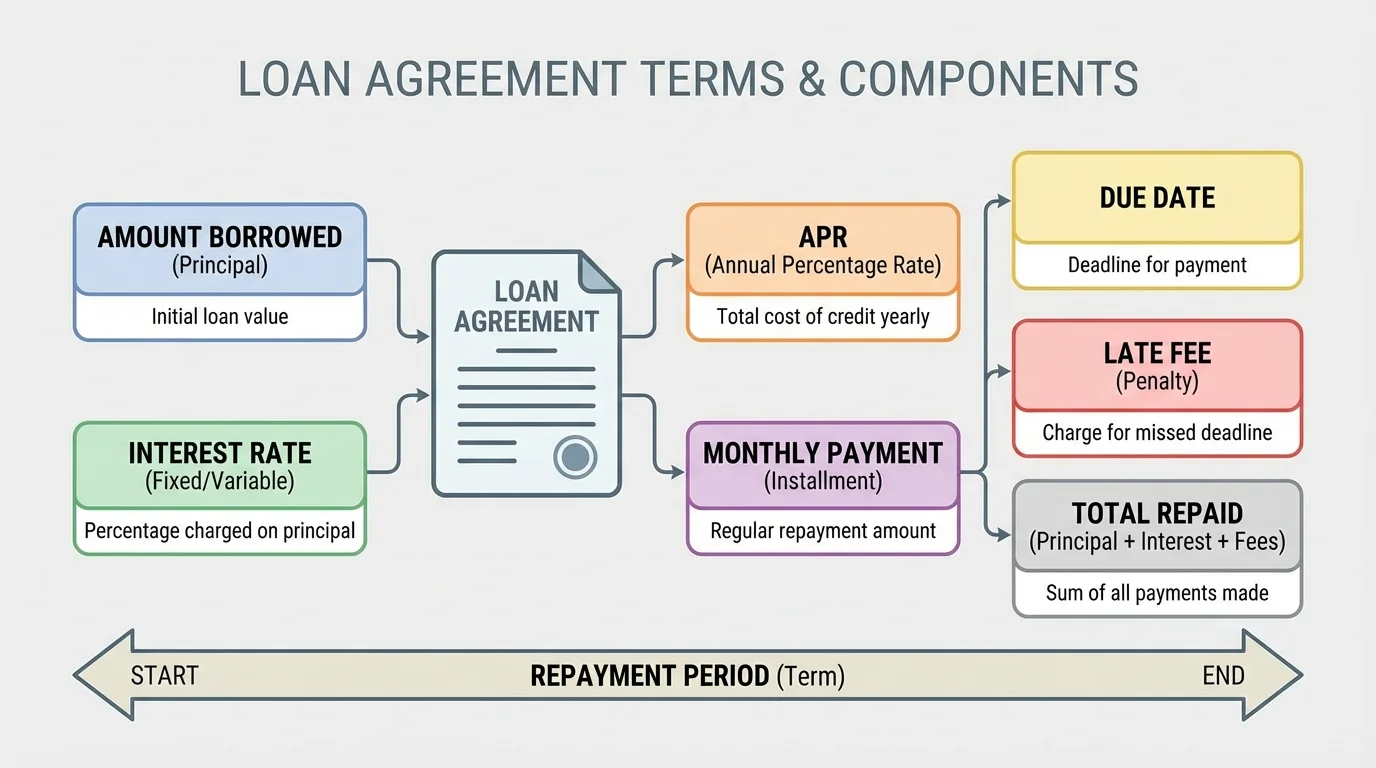

A loan agreement is a contract in which a lender gives you money and you promise to repay it under stated terms. Those terms often look simple at first, but the major cost categories are easier to separate clearly, as [Figure 3] shows: amount borrowed, interest rate, APR, payment schedule, fees, and consequences of default.

Principal is the amount borrowed. Interest is the cost of borrowing. The interest rate is one measure of that cost, while APR, or annual percentage rate, usually reflects a broader yearly borrowing cost that may include certain fees. If two loans advertise the same monthly payment, the one with the lower APR may still be the better deal, but you must compare carefully.

Also check the payment schedule. Is the payment due monthly, every two weeks, or on another schedule? Is the rate fixed or variable? A fixed rate stays the same. A variable rate can change over time, which can make future payments less predictable.

Late fees and default terms matter a lot. Default means failing to meet the loan terms, usually by missing payments. Default can damage your credit, trigger extra fees, lead to collections, or even result in losing collateral if the loan is secured. Collateral is property tied to the loan, such as a car in an auto loan.

Loan example: comparing total cost

Loan A lets you borrow $1,000 and repay $1,120 over time. Loan B lets you borrow $1,000 and repay $1,260 over time.

Step 1: Find the total repaid amount for each loan.

Loan A total repaid is $1,120. Loan B total repaid is $1,260.

Step 2: Compare the extra cost beyond the amount borrowed.

Loan A costs \(\$1,120 - \$1,000 = \$120\) extra. Loan B costs \(\$1,260 - \$1,000 = \$260\) extra.

Step 3: Decide which costs less overall.

Loan A costs $140 less because \(\$260 - \$120 = \$140\).

If you only looked at whether you qualified, you might miss a major difference in total cost.

Be especially careful with co-signers. A co-signer is another person who agrees to be legally responsible if you do not pay. That is not a casual favor. It is a serious legal and financial risk for both people. If someone asks you to co-sign, read the contract with even more caution than usual.

The categories in [Figure 3] also help you compare offers from banks, credit unions, schools, or financing companies. Instead of asking only, "Can I get this loan?" ask, "What will this really cost me, and what happens if life gets complicated?"

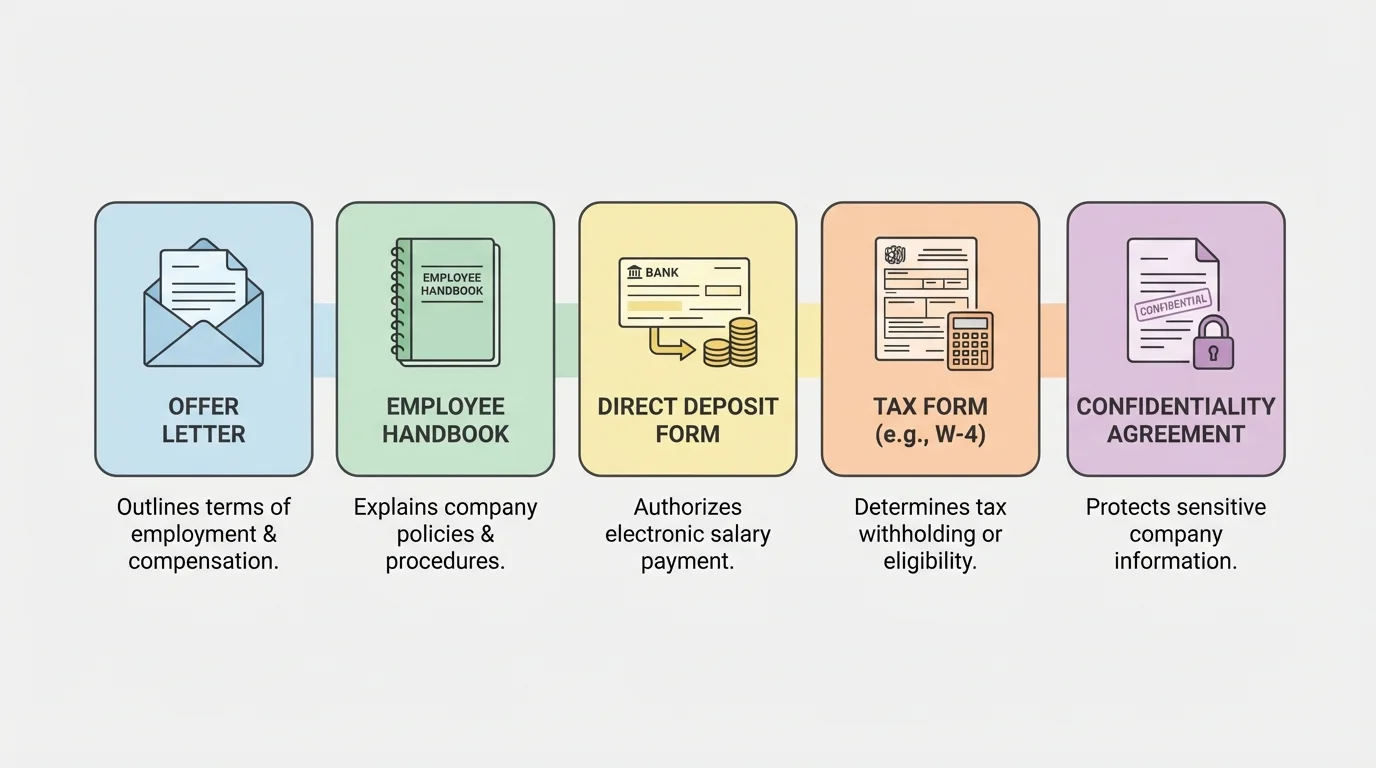

Starting a job often involves more paperwork than people expect, and [Figure 4] displays some of the most common documents: an offer letter, tax forms, direct deposit forms, policy acknowledgments, and sometimes a confidentiality or non-disclosure agreement. Each document serves a different purpose, so do not treat the whole stack as one thing.

An offer letter usually states your job title, pay rate, expected hours, start date, supervisor, and sometimes benefits. Read every line. If you were told you would work remotely, have flexible hours, or earn a certain starting wage, check that the written document matches.

You may also receive an employee handbook. That handbook often includes attendance rules, conduct expectations, dress or communication standards, reporting procedures, and discipline policies. Even if it feels long, skimming can lead to avoidable problems later.

Pay details deserve special attention. Are you paid hourly or by salary? If hourly, what is your exact rate? How often are you paid? If your rate is $16 per hour and you work approximately 20 hours in a week, your gross pay for that week is about \(\$16 \times 20 = \$320\) before taxes and other deductions. Gross pay is not the same as take-home pay.

Schedule expectations matter too. Can the employer change your hours with little notice? Are weekends required? Is overtime possible? Are breaks explained? For students balancing work with online coursework, unclear schedule terms can create stress quickly.

Some jobs include a confidentiality agreement or non-disclosure agreement. This means you may not share certain business information, customer data, or internal materials. That can be reasonable, but you should still understand what information is covered and for how long.

Employment example: checking whether a job offer matches what you were told

You are told in a video interview that the job pays $17 per hour and usually schedules you for evenings only. The written offer says $15.50 per hour and "hours vary by business need."

Step 1: Pause before signing.

The written document does not match the spoken promise.

Step 2: Ask for clarification in writing.

Send a professional message asking whether the pay rate and schedule can be corrected or explained.

Step 3: Decide based on the written terms, not the interview memory.

If the employer will not update the document, assume the written terms are the real agreement.

This protects you from confusion and shows professional judgment.

Later, if a workplace issue comes up, documents matter. An employer may rely on what you signed, acknowledged, or agreed to electronically. That is why [Figure 4] remains useful beyond your first day: each form shapes a different part of your job experience.

Some contracts are fair but complicated. Others are designed to push people into bad decisions. Watch for red flags such as blank spaces, missing dates, unreadable fine print, promises that are "not in the contract," surprise fees, pressure to sign immediately, and refusal to let you take time to review the document.

Be wary of contracts sent through suspicious links, especially if someone asks for personal data quickly. Scams often use urgency and emotional pressure. A real business can still be careless, but a scam usually tries to stop you from slowing down.

Many serious contract problems begin with details that seem small at first, such as automatic renewal, required notice periods, or late fees that repeat every month. Tiny lines can create very large costs over time.

You also have the right to ask for help. Depending on where you live, useful resources may include a parent or guardian, a trusted adult, a legal aid organization, a tenant rights group, a consumer protection office, a workforce office, or a school counselor who can point you toward local support. Asking for another set of eyes is not weakness. It is smart risk management.

Clear communication can prevent conflict before it starts. If something is confusing, ask direct questions such as: "What is the total cost including fees?" "What happens if I need to end this early?" "Can you show me where that promise appears in writing?" and "When will I receive a copy signed by both sides?"

Keep your tone calm and professional. You do not need to sound aggressive to protect yourself. You do need to be specific. If possible, communicate by email or follow a phone call with a written message that confirms what was discussed. For example: "Thanks for speaking with me today. My understanding is that rent includes water and trash, and the lease requires thirty days' notice before move-out. Please let me know if that is incorrect."

"Read before you sign, ask before you agree, and save what you are told."

This habit supports civic responsibility too. Communities work better when people keep records, understand obligations, and resolve disputes using facts instead of guesses. Being contract-aware helps you participate more confidently in housing, work, and financial systems.

Before signing any important agreement, pause and run through this checklist. First, identify the type of contract. Second, highlight all costs and due dates. Third, list your responsibilities and the other party's responsibilities. Fourth, find all penalties, exit rules, and renewal terms. Fifth, compare verbal claims with written language. Sixth, ask questions and get answers in writing. Seventh, save a copy for yourself.

If you still feel confused after doing that, do not sign yet. Waiting is often the smartest option. A strong decision is not the fastest decision. It is the one you can explain clearly afterward: what you agreed to, what it costs, what could go wrong, and what rights you still have.

| Document type | What to find first | Common risk | Smart question to ask |

|---|---|---|---|

| Lease | Rent, deposit, utilities, move-out terms | Unexpected fees or early move-out cost | What exactly can cause me to lose part of the deposit? |

| Loan agreement | Total repayment, APR, due dates, late fees | Paying much more than expected | What is the full amount I will repay if everything goes as planned? |

| Employment document | Pay, hours, duties, policies, start date | Written terms not matching verbal promises | Can you show me where the pay rate and schedule are stated in writing? |

Table 1. A quick comparison of the first details to review in common adult contracts.

Being able to evaluate contracts is part of becoming independent. It helps you avoid preventable debt, housing problems, and workplace confusion. More than that, it helps you act with confidence in systems that affect your everyday life.