Have you ever had money for something fun, but then realized you did not have enough left for something important later? That happens to a lot of people. Money can seem to disappear quickly when there is no plan. A budget is a simple tool that helps you tell your money where to go instead of wondering where it went.

A budget helps you make choices before you spend. If you get an allowance, birthday money, money for helping with chores, or money for a special trip, a budget gives that money a job. You can decide what part is for things you want now, what part is for later, and what part you want to give to help someone else.

When people use a budget, they are more prepared. They are less likely to spend all their money too fast. They can reach goals, like buying a game, a book, art supplies, or a gift for someone. They can also feel calmer because they know their plan.

Budget means a plan for how you will use your money. It helps you decide how much money will be used for different purposes.

Income is money that comes to you. For a child, income might be an allowance, gift money, or money earned by helping at home.

A budget does not need to be complicated. It can be written on paper, typed on a tablet, or written in a small notebook. What matters most is that your plan is clear and simple enough to use.

Think of a budget like a map. A map helps you get where you want to go. A budget helps your money get where you want it to go. Without a map, you might get lost. Without a budget, you might spend money on one thing and then not have enough for another.

Budgets work best when you start with how much money you have. Then you decide how to divide it. If you have $10, you cannot plan to spend $12. Your total plan must fit your total money. For example, if you put $4 for spending, $4 for saving, and $2 for sharing, then your budget uses all your money because \(4 + 4 + 2 = 10\).

Your money needs jobs. A budget is really a way of giving each dollar a job. Some dollars help you buy things now. Some help you get bigger things later. Some help you be generous. When every part has a job, it is easier to make thoughtful choices.

This is important because every financial choice affects another. If you spend more in one place, you may need to save less or share less. A budget helps you notice those trade-offs early.

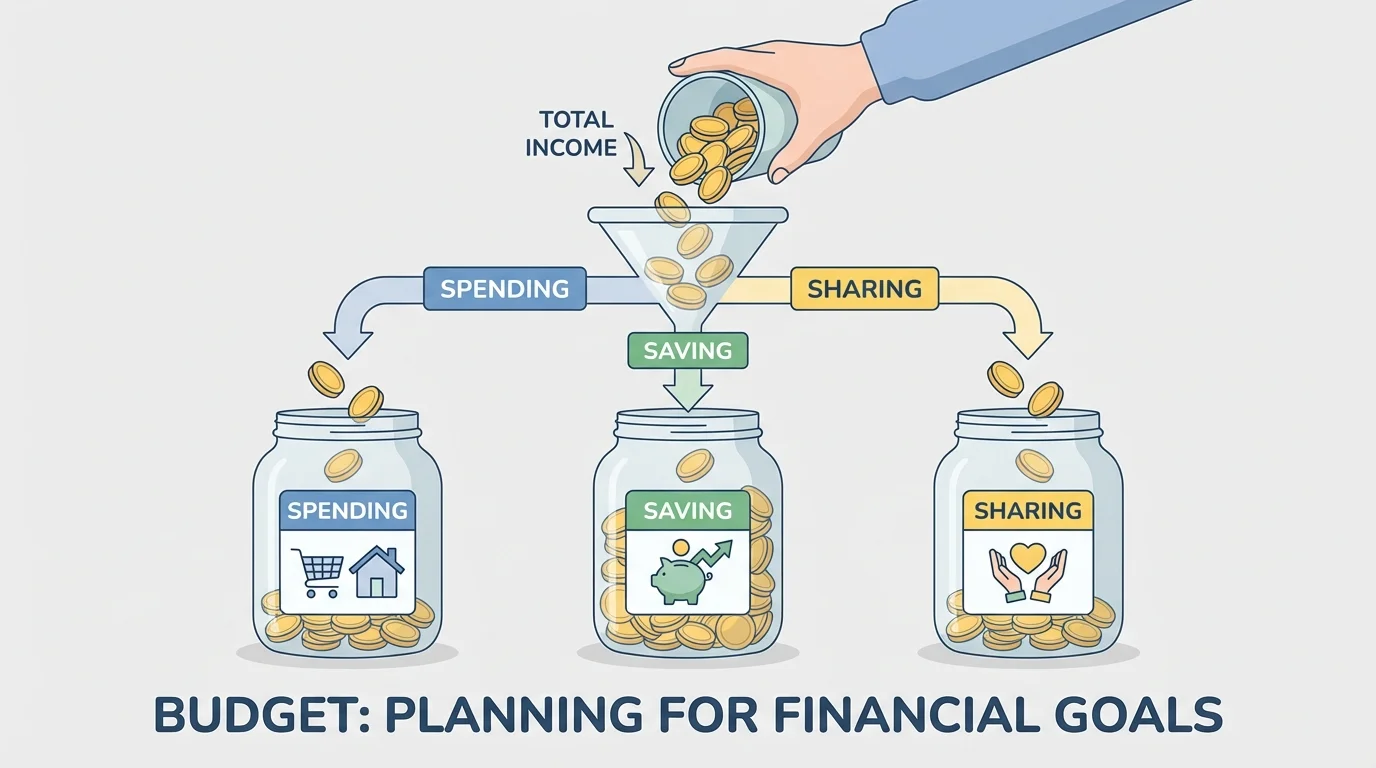

[Figure 1] Many simple budgets for kids use three main parts: spending, saving, and sharing. These three jobs help you think about today, tomorrow, and other people.

Spending is money you use now. You might spend on a snack during an outing with family, stickers, a small toy, or supplies for a hobby. Spending is not bad. It is part of using money wisely. The key is choosing carefully so you do not use all your money at once.

Saving is money you keep for later. Maybe you want a bigger item that costs more than you have right now. Saving means waiting and building up your money over time. If you save $3 each week, after \(4\) weeks you will have \(3 \times 4 = 12\), or $12.

Sharing is money you choose to give to help others. You might donate to an animal shelter, a community event, a fundraiser, or a cause your family supports. Sharing shows kindness and generosity. Even a small amount can matter.

These three parts do not always have to be equal. One week you might save more because you have a big goal. Another time you might share more because there is a special reason to help. The budget is your plan, and you can adjust it to fit the situation.

Some families really do use jars, envelopes, or boxes to separate money into categories. Seeing the money in different places can make budgeting easier, especially when you are learning.

When you look again at [Figure 1], you can see why this method works so well. Instead of one pile of money that can disappear quickly, you have clear groups with clear purposes.

Making a budget is easier when you do it step by step. You do not need fancy tools. You just need to know how much money you have and what you want your money to do.

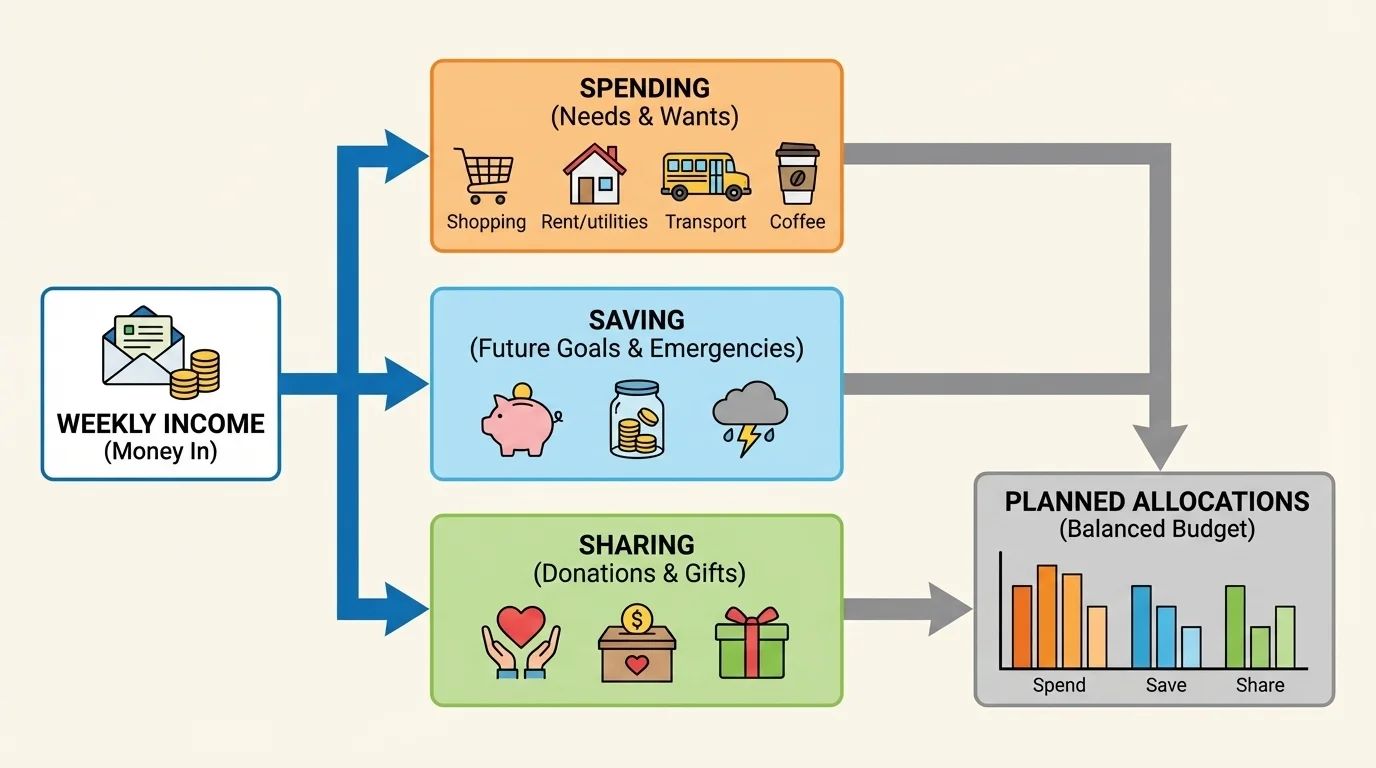

[Figure 2] Step 1: Find your total money. This is the amount you can plan with. Suppose you have $15.

Step 2: Decide your goals. Maybe you want some money for now, some for later, and some to give. For example, you might choose $6 for spending, $7 for saving, and $2 for sharing.

Step 3: Check the total. Your parts should add up to all your money. Here, \(6 + 7 + 2 = 15\), so the plan works.

Step 4: Write it down. A written plan is easier to follow than a plan you only keep in your head.

Worked example: Making a weekly budget

A student gets $12 for the week and wants to divide it into spending, saving, and sharing.

Step 1: Choose amounts for each job.

Spending: $5, Saving: $5, Sharing: $2.

Step 2: Check that the total matches the money available.

\(5 + 5 + 2 = 12\)

Step 3: Decide what each part is for.

The $5 spending money is for a small treat, the $5 saving money is for a new book, and the $2 sharing money is for a donation jar.

This budget works because all the money has a purpose.

Another student may choose a different plan. If they want to save for something special, they could budget $3 for spending, $8 for saving, and $1 for sharing. That also works because \(3 + 8 + 1 = 12\). Budgets are personal plans, not one-size-fits-all rules.

| Money Job | Example Amount | What It Could Be For |

|---|---|---|

| Spending | $5 | Small treat or craft item |

| Saving | $5 | Book, game, or bigger goal |

| Sharing | $2 | Donation or helping a cause |

Table 1. A simple example of how one weekly budget can divide money into spending, saving, and sharing.

Try This: Next time you get money, write the total at the top of a page. Under it, make three lines: spending, saving, and sharing. Pick an amount for each line and check that the total matches your money.

A budget helps you feel in control. If you know you set aside money for a goal, you do not have to guess whether you can afford it later. You already made a plan. That can make waiting easier.

Following a budget also helps stop overspending. Overspending means using more money than you planned for one category. If you only budgeted $4 for spending and used all $4, then buying one more item means taking money away from saving or sharing unless you make a new plan.

Here is a simple example. Suppose you budget $10 like this: $4 for spending, $5 for saving, and $1 for sharing. If you spend $6 instead, then you are $2 over your spending amount. Now your plan is off by \(6 - 4 = 2\). You may need to take $2 from saving, from sharing, or from both.

Good budgeting gives you choices before problems happen. Instead of being surprised later, you can notice early when a choice will affect another part of your plan. That is why budgeting is useful in real life.

When you look back at [Figure 2], notice that each category has a clear amount. That makes it easier to tell whether you are staying on track or need to adjust something.

Budgets are not frozen forever. Sometimes prices change. Sometimes your goal changes. Sometimes you get more money, and sometimes you have less than expected. A smart budget can bend when life changes.

Suppose you planned to spend $5 on a small item, but the item now costs $6. You have choices. You could wait and save $1 more. You could choose a cheaper item. Or you could move $1 from another category if that fits your priorities. The new plan still has to match your total money.

Worked example: Adjusting a budget

You have $10. Your first plan is $4 spending, $4 saving, and $2 sharing. Then you decide you want to save more for a bigger goal.

Step 1: Keep the total money the same.

Total money is still $10.

Step 2: Change the category amounts.

New plan: $3 spending, $5 saving, and $2 sharing.

Step 3: Check the total again.

\(3 + 5 + 2 = 10\)

This adjusted budget works because it matches the same total money while fitting the new goal better.

Changing a budget is not failure. It is part of smart planning. The important thing is to notice the change and make a new choice instead of ignoring it.

Small habits make budgeting easier. First, write your plan down. Second, keep your money in a way that helps you remember its jobs. Some people use jars. Some use envelopes. Some keep a list on a device. Third, check your budget after you spend money so you know what is left.

It also helps to set a goal for saving. Saving feels easier when you know what you are saving for. "I am saving for something someday" is harder than "I am saving $20 for a science kit" or "I am saving for a gift for my cousin."

You already know how to add and subtract money amounts. Budgeting uses those same skills in real life. You add to make sure your plan fits your total money, and you subtract to see how much is left after spending.

Sharing can be part of your habit too. If you always put a small amount aside for helping others, generosity becomes part of your plan instead of something you try to do only if money is left over.

Try This: Make a tiny budget for the next money you receive. Even if it is just $5, try dividing it on purpose. For example, $2 for spending, $2 for saving, and $1 for sharing. Then check that \(2 + 2 + 1 = 5\).

Over time, budgeting helps build trust in yourself. You learn that you can make a plan, follow it, and reach your goals. That is a powerful life skill, whether you are planning with $5 now or much more money when you are older.

"A budget is telling your money where to go instead of wondering where it went."

— A popular money-planning saying

People who budget are not saying "no" to everything fun. They are saying "yes" in a smart order. They make room for enjoyment, future goals, and kindness all at the same time.