Have you ever spent a little money on something small, then later wished you had saved it for something better? That happens to a lot of people, including adults. A few dollars may seem tiny in the moment, but those small choices can decide whether you get the game, book, art set, or gift you really wanted by the end of the week or month. Learning to make smart money choices now helps you in real life every single day.

Money is a tool. You can spend it now, save it for later, or sometimes do a little of both. Good money decisions do not mean never buying fun things. They mean using your money in a way that matches what matters most to you.

When you make thoughtful choices, you are more likely to reach your goals and feel proud of how you used your money. When you spend without thinking, you might run out of money fast and have nothing left for something important later. That is why even everyday purchases, like a snack, a sticker pack, or an app add-on, are worth thinking about for a moment.

Short-term goal means something you want to save for or do soon, usually in a few days, weeks, or months. Budget means a simple plan for how to use your money. Value means how useful or worth it something is for the money you spend.

A short-term goal can be small and realistic. You might want to save for a new soccer ball, a craft kit, a birthday gift for someone, or a trip to the community pool. These goals matter because they give your money a job.

A goal works best when it is clear. Instead of saying, "I want something fun," say, "I want to save $12 for a sketchbook set." A clear goal helps you know how much money you need and how close you are.

Short-term goals are different from very big goals that take years. For you, a short-term goal should feel possible. If your goal costs $10 and you already have $4, then you know you still need $6 more. That sounds manageable because you can picture getting there.

If you get $2 each week for chores or from a money gift, saving can be simple. For example, if you need $6 more, and you save $2 each week, then in about three weeks you can reach your goal because \(2 + 2 + 2 = 6\).

Many smart money habits start with tiny amounts. Saving even $1 at a time teaches your brain to pause, plan, and choose.

Goals also help with self-control. It is easier to say no to a small purchase when you remember what you are saying yes to later.

One helpful way to decide is to sort choices into need, want, and saving for a goal. This kind of sorting helps you stop and think before spending.

A need is something important for health, safety, learning, or daily living. A want is something you would enjoy but can live without right now. For kids, adults usually pay for many needs, but you still make choices about wants and savings.

Let's say you have $5. You see a $3 toy capsule and also remember you are saving for an $8 puzzle book. The toy capsule is a want. Saving is a smart choice if the puzzle book matters more to you. That does not make the toy "bad." It just means it may not fit your goal today.

Sometimes a choice can change depending on the situation. A water bottle for a sports practice may feel more important than a candy bar. A notebook for your drawing hobby may support a real goal. Smart money decisions are not only about labels. They are about asking, "What matters most right now?"

If you spend all your money on wants right away, you may feel happy for a short time but disappointed later. If you always save and never enjoy any money, that can feel frustrating too. Balance matters.

Before you buy something, use a quick budget plan. Good spending decisions can happen step by step, not in a rush.

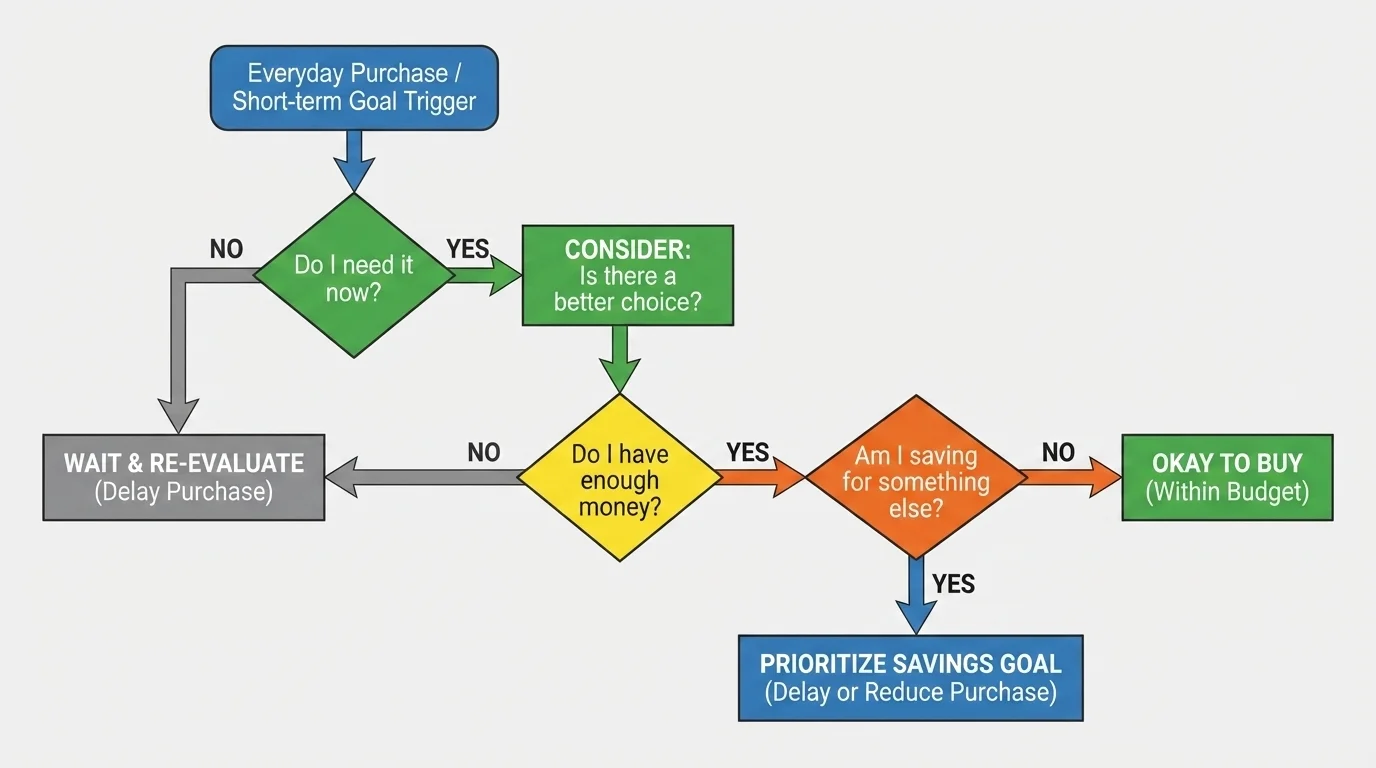

[Figure 2] Step 1: Ask, "Do I need this now?" If the answer is no, move to the next question.

Step 2: Ask, "Do I have enough money?" If an item costs $6 and you only have $4, then you do not have enough because \(4 < 6\).

Step 3: Ask, "Am I saving for something else?" If buying this item will slow down your goal, decide if it is still worth it.

Step 4: Ask, "Is there a better choice?" Another item may cost less, last longer, or be more useful.

This plan only takes a minute, but it can save you from regret. It is especially useful for online purchases because clicking fast can make spending feel less real.

Example: Using the buying plan

You have $9. You are saving for a $12 card game. You see a keychain for $4.

Step 1: Ask if you need it now.

No. A keychain is fun, but it is not urgent.

Step 2: Check your money.

You do have enough for the keychain because \(9 > 4\).

Step 3: Think about your goal.

If you spend $4, you will have $5 left because \(9 - 4 = 5\). You would still need $7 more to get the card game.

Step 4: Decide.

If the card game matters more, save your money. If the keychain matters more, buy it knowing your goal will take longer.

The important part is not that one answer is always right. The important part is that you choose on purpose.

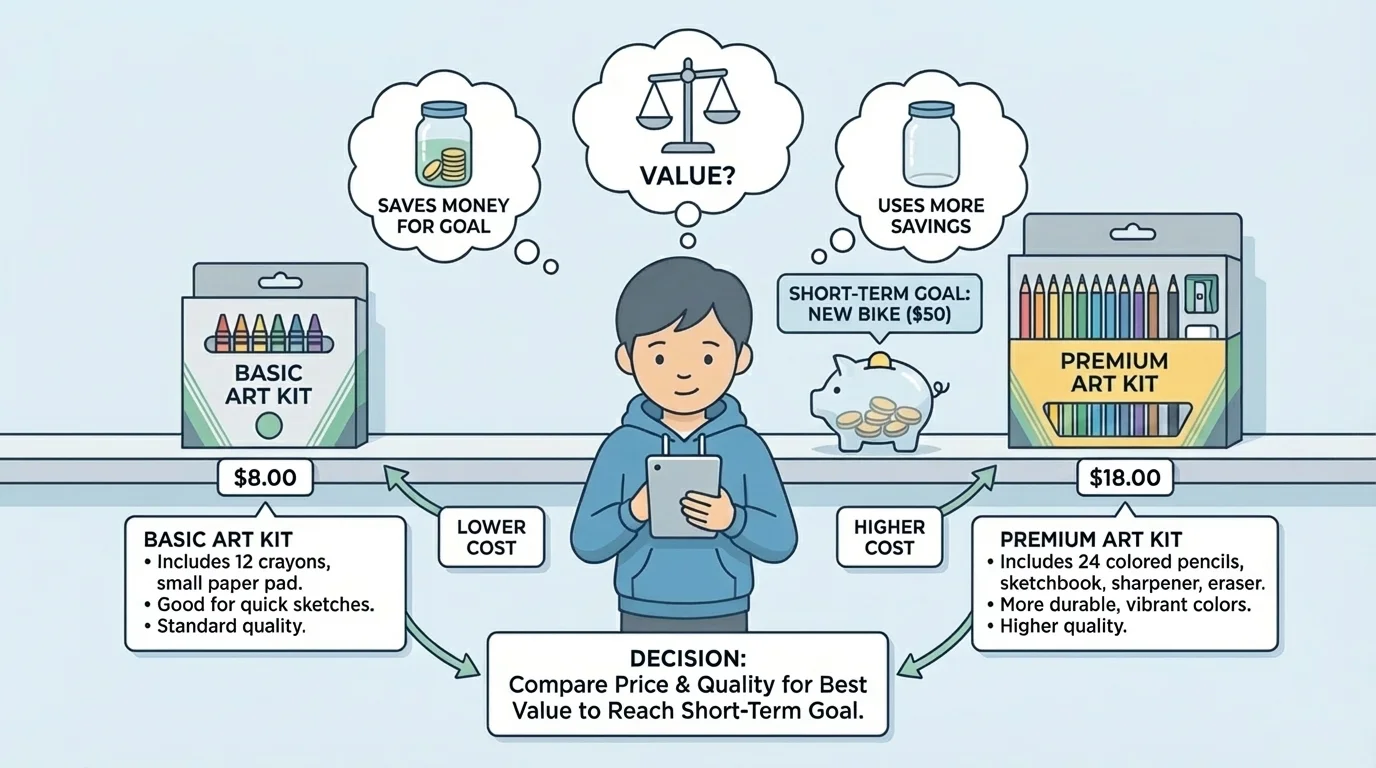

Sometimes the cheapest item is the best choice, but not always. Value means looking at what you get for the money. In real shopping situations, one item may cost less but also break quickly or not work as well.

[Figure 3] If you are comparing two items, look at three things: price, quality, and usefulness. Ask yourself how often you will use it and how long it might last.

Suppose one pack of markers costs $4 and another costs $6. If the $6 pack has more colors and lasts much longer, it may be the better value for someone who draws every week. But if you only need a few markers for one project, the $4 pack may make more sense.

| Choice | Cost | What you get | Best for |

|---|---|---|---|

| Snack A | $2 | Small size | Quick treat |

| Snack B | $3 | Bigger size, can share | Longer use |

| Notebook A | $1 | 20 pages | Short project |

| Notebook B | $3 | 80 pages, stronger cover | Longer goal |

Table 1. Examples of comparing price and value for everyday purchases.

You can also compare how much money stays in your pocket after buying something. If you have $10 and buy the $3 snack, then you have $7 left because \(10 - 3 = 7\). If you buy the $2 snack, then you have $8 left because \(10 - 2 = 8\). That extra $1 may help your goal.

Advertisements sometimes try to make you feel that you need something right away. Slowing down helps you notice whether an item is truly useful or just exciting for the moment. The same need-want thinking from [Figure 1] also helps when you compare value.

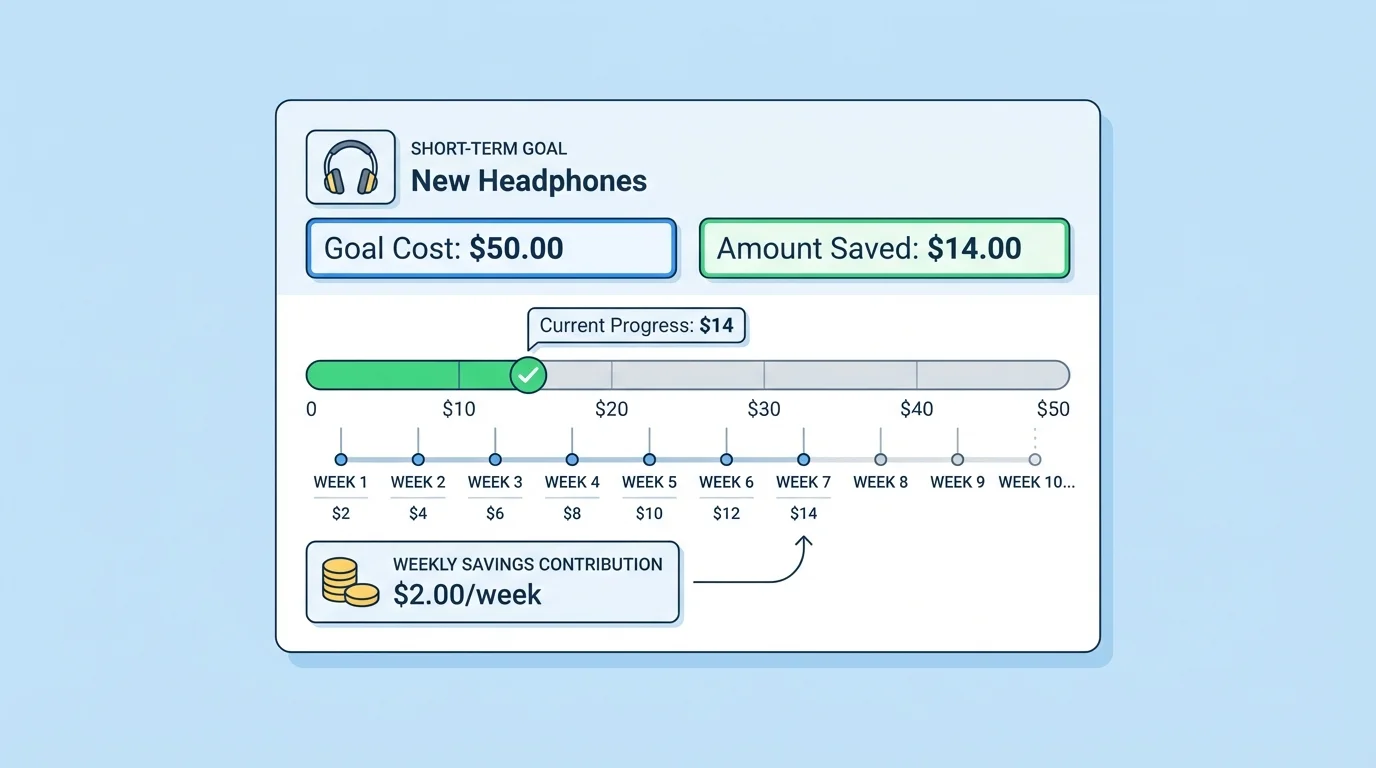

Saving works best when you break a goal into small pieces. Small amounts can grow into enough money for something you really want.

[Figure 4] Let's say your goal costs $15. You already have $3. First, find how much more you need: \(15 - 3 = 12\). If you save $2 each week, then it will take about six weeks because \(12 \div 2 = 6\).

This is helpful because a big number can feel hard, but smaller steps feel possible. You are not trying to get $15 all at once. You are trying to save $2, then another $2, and so on.

You can keep track with a jar, envelope, notebook, or a simple note on a device with an adult's help. Every time you add money, write the new total. For example, if you have $5 and save $2 more, your new total is \(5 + 2 = 7\).

Example: Reaching a short-term goal

You want a book that costs $11. You already saved $5, and you will save $2 each week.

Step 1: Find how much more you need.

Subtract the amount you have from the total cost: \(11 - 5 = 6\).

Step 2: Find how many weeks it may take.

Save $2 each week, so \(6 \div 2 = 3\).

Step 3: Make your plan.

Keep your $5 safe, add $2 each week, and check your total.

After about three weeks, you can have enough money for the book.

When you watch your savings grow, it becomes easier to stay patient. That is one reason tracking your progress helps so much.

Real money choices happen in small moments. One day you may want a snack while you are out with family. Another day you may want to buy a game item online. Comparing choices in real life, like the example in [Figure 3], helps you decide what is worth your money.

Situation 1: You have $6. You want a smoothie for $5, but you are saving for a $10 mini basketball. If you buy the smoothie, you will have $1 left because \(6 - 5 = 1\). If your goal matters more, skipping the smoothie may be the smarter choice today.

Situation 2: You want to buy a digital sticker pack for $3 during a game. Ask yourself if it changes anything important or if it is just a quick want. Online items can be fun, but they are easy to buy without much thinking.

Situation 3: You need a small gift for a friend. You have $8. One gift costs $8, and another costs $5. The $5 gift might still be kind and thoughtful, and it leaves you $3 because \(8 - 5 = 3\). A smart choice is not always the biggest or most expensive one.

Situation 4: You are choosing between two craft kits. One costs $7 and includes enough supplies for one project. The other costs $9 and includes supplies for three projects. If you will really use all three, the second kit may be better value.

Smart spending is about matching money to purpose. A good decision depends on your goal, how much money you have, and whether the item is useful, lasting, and important to you. That is why the same item may be a smart buy one day and not a smart buy another day.

Notice that these choices are not only about saying no. They are about choosing what matters most with the money you have right now.

Smart money choices become easier when you build habits. A habit is something you practice often until it feels natural.

Habit 1: Count your money before you shop. Knowing your total helps you avoid guessing.

Habit 2: Pause before buying. Even waiting one minute can help you think clearly.

Habit 3: Keep goal money separate. If possible, put saving money in a jar or envelope labeled with your goal.

Habit 4: Track what you spend. If you bought two snacks for $2 each, your total spending was \(2 + 2 = 4\). Writing it down helps you notice patterns.

Habit 5: Ask a trusted adult when you are unsure, especially for online purchases, subscriptions, or sales that feel rushed.

"When you tell your money where to go, it is easier to reach where you want to go."

These habits protect you from impulse buying. An impulse purchase is something you buy quickly without thinking enough about it first.

Sometimes the smartest choice is to wait. Here are some signs a purchase may not be a good idea right now.

You do not have enough money. You would spend money meant for an important goal. You only want the item because someone else has it. You are buying too fast because of excitement. You are not sure what the item really does, how long it lasts, or whether an adult has approved it.

This does not mean you can never buy fun things. It means you are learning to notice red flags before spending. The buying plan from [Figure 2] is useful here because it slows you down and helps you ask the right questions.

You already know how to add and subtract money amounts. Those same skills help you decide whether you can afford something now, how much you will have left, and how long saving may take.

If you make a money mistake, that is okay. Everyone does sometimes. The goal is to learn from it. You might think, "Next time I will wait before clicking buy," or "Next time I will compare two choices first."

When you face an everyday money decision, try this simple order: know your goal, count your money, think about needs and wants, compare choices, and decide on purpose. That is a practical skill you can use at home, online, in stores, and during activities in your community.

For example, if you have $10 and your goal is a $14 board game, you still need $4 because \(14 - 10 = 4\). If you are thinking about spending $3 on candy, pause and ask whether that candy matters more than reaching your goal sooner. If not, waiting may be the better decision.

As your goals change, your choices may change too. Sometimes spending now is fine. Sometimes saving is smarter. The real power is that you are learning how to choose, not just how to buy.