Have you ever had money in your pocket one day and then wondered where it all went a few days later? That happens to lots of people, including adults. Money can disappear quickly when you spend a little here and a little there. A budget helps you give your money a job before you spend it.

A budget is a simple plan for your money. It helps you decide how much to save, how much to spend now, and how much to set aside for something you want later. When you use a budget, you are the boss of your money instead of letting your money choices happen by accident.

Budgeting matters because small choices add up. If you get $5 and spend all of it on snacks, that money is gone right away. If you save part of it each time, you can build up enough for something bigger. A budget gives you a clear picture so you can enjoy money now and still work toward future goals.

Income is money you receive, such as allowance, birthday money, or money from doing a small job. Expenses are the things you use money to buy. Savings are money you keep for later instead of spending right away. A planned purchase is something you want to buy in the future after you save for it.

People who budget well often feel calmer because they know what their money is for. People who do not budget may run out of money fast, forget their goals, or feel upset when they cannot afford something they really wanted.

When you make a budget, start by knowing where your money comes from and where it goes. Your money coming in is your income. Your money going out is your expenses. Some expenses are small and quick, like a treat or a sticker pack. Some are bigger and take planning, like a new game, art supplies, or sports equipment.

You also need to think about goals. A money goal is something you want your money to help you do. Your goal might be to save $15 for a book series, $25 for a gift, or $40 for a special item. A good budget connects your money to your goals.

Even adults use very simple budgets. Many people just write down money in, money out, and money saved. A budget does not have to be fancy to be useful.

Another helpful idea is knowing the difference between a need and a want. A need is something important for daily life. A want is something you would enjoy but can live without for now. Since many fifth graders do not pay for major needs on their own, your budget will mostly focus on wants, choices, and goals. [Figure 1]

A simple budget works well when you sort your money into three clear parts: saving, spending, and planned purchases. These parts help you avoid using all your money in one place.

Saving means money you keep and do not touch right now. This can be for emergencies, future goals, or just building a good habit. Spending means money you can use soon on smaller items. Planned purchases mean money set aside little by little for a specific item you want later.

You do not need the same amount in each part every time. If you are saving for something important, you might put more into planned purchases. If you already reached a goal, you might allow a little more for spending. The key idea is that every dollar or coin has a purpose.

One easy way to remember this is: save some, spend some, plan some. That keeps your money balanced. You can enjoy today while still thinking ahead.

A budget is a choice tool. It is not about never buying fun things. It is about choosing on purpose. When you plan first, you can say yes to some things now and yes to bigger goals later.

If you have ever spent all your money quickly and then wished you had waited, this three-part system can help. The visual split in [Figure 1] makes it easier to see that spending everything in one category can leave the others empty.

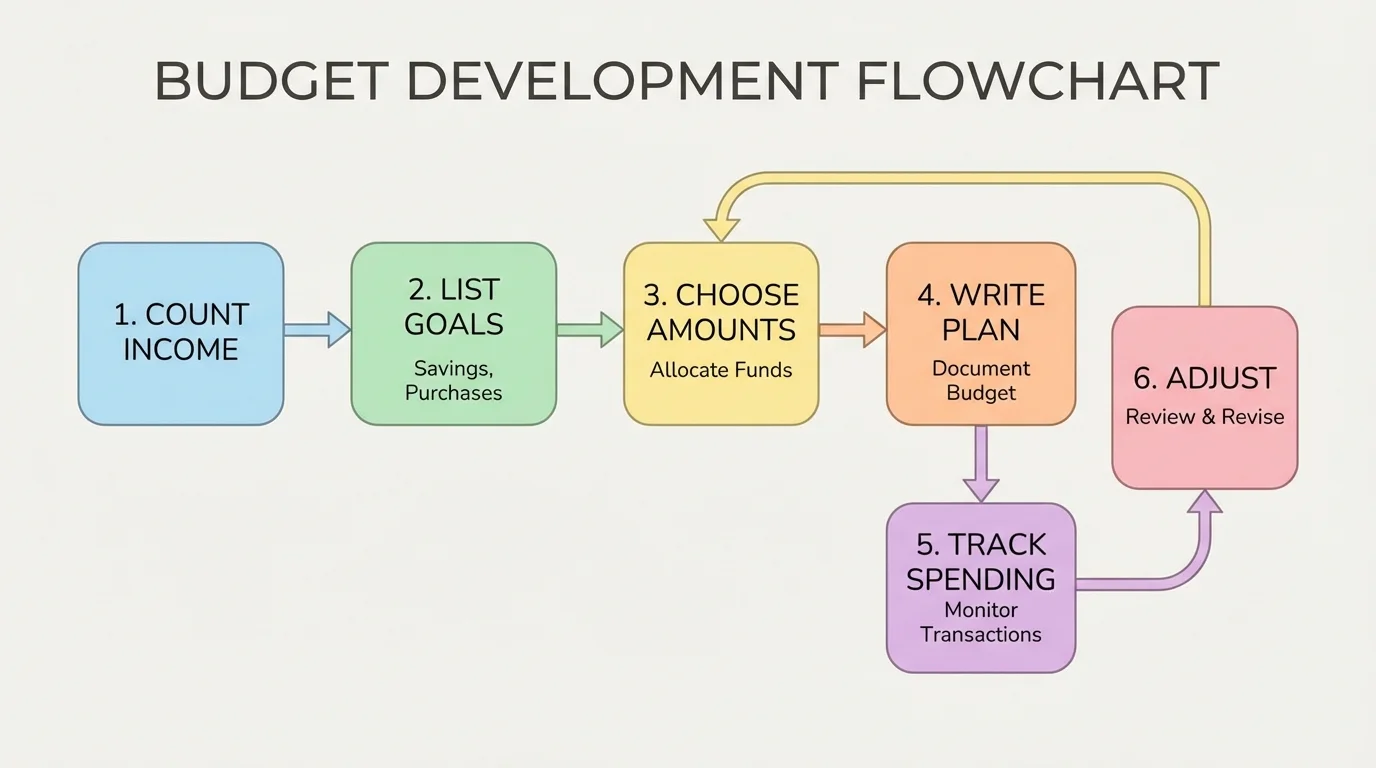

Making a budget is a repeatable process, and [Figure 2] lays out the steps in a simple order. Once you learn the routine, you can use it again every week or every month.

Step 1: Count your income. Write down all the money you expect to receive. This might be weekly allowance, money for chores, or gift money. If you get different amounts at different times, write only what you actually have right now or what you know is coming soon.

Step 2: Pick your money goals. Ask yourself: What do I want to save for? What small things might I buy soon? Is there a bigger item I want later? Clear goals make budgeting easier.

Step 3: Decide how much goes into each category. Your total money must equal the amount you divide up. If you have $12, your plan might be $4 to savings, $3 to spending, and $5 to a planned purchase. In math, that looks like \(4 + 3 + 5 = 12\).

Step 4: Write it down. Use paper, a note on a device, or a simple chart. A written plan is much easier to follow than trying to remember everything in your head.

Step 5: Track what you actually do. If you planned to spend $3 but spent $5, your budget needs an update. Budgets are not traps. They are tools you can adjust.

You do not need perfect numbers. You just need honest numbers. A simple, realistic budget works better than a perfect-looking budget you never use.

Building a weekly budget

You receive $10 this week and want to save for headphones while still having some money for a treat.

Step 1: Start with total income.

Your total is $10.

Step 2: Choose category amounts.

You decide on $3 for savings, $2 for spending, and $5 for planned purchases.

Step 3: Check the total.

\(3 + 2 + 5 = 10\)

Step 4: Write the finished budget.

Saving: $3, Spending: $2, Planned purchase: $5.

This budget works because the parts add up to the whole amount.

If you like, you can use containers or envelopes labeled with your categories. That makes your plan feel real. Digital notes also work well if that is easier for you at home.

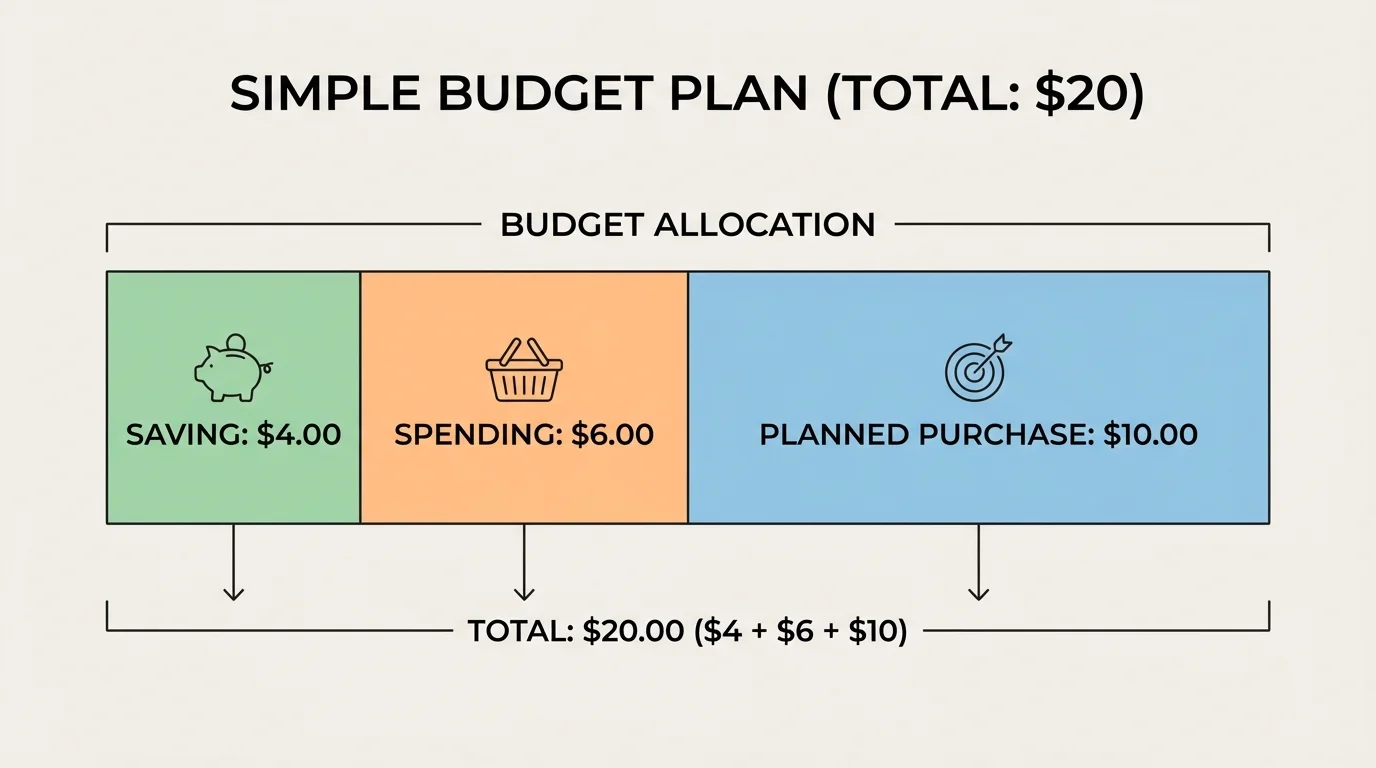

Sometimes it helps to see the whole plan at once, and [Figure 3] presents a simple example. Suppose you have $20 from allowance and a birthday card, and you want to use it wisely.

You decide that saving matters, but you also want money for small choices now and for a larger item later. One possible plan is to save $6, keep $4 for spending, and put $10 toward a planned purchase. The total is \(6 + 4 + 10 = 20\).

| Category | Amount | Purpose |

|---|---|---|

| Saving | $6 | Build a money cushion |

| Spending | $4 | Small choice this week |

| Planned purchase | $10 | Save for a larger item |

Table 1. A sample budget showing how $20 can be divided into saving, spending, and planned purchases.

This budget works because every part has a reason. The saving amount helps build the habit of not spending everything. The spending amount gives flexibility. The planned purchase amount moves you closer to a goal.

Now suppose your planned item costs $30 and you already set aside $10 this week. You still need \(30 - 10 = 20\) more. If you add $5 each week, it will take \(20 \div 5 = 4\) more weeks. This is how budgeting turns a wish into a plan.

Checking whether a budget works

A student receives $15 and writes this plan: $5 to savings, $5 to spending, and $7 to planned purchases.

Step 1: Add the budgeted amounts.

\(5 + 5 + 7 = 17\)

Step 2: Compare with total income.

The student only has $15, but the plan uses $17.

Step 3: Fix the plan.

One corrected budget could be $5 to savings, $4 to spending, and $6 to planned purchases.

Step 4: Check again.

\(5 + 4 + 6 = 15\)

A budget must match the money you actually have.

When you look at a full plan like the one in [Figure 3], it becomes easier to spot mistakes before you spend anything.

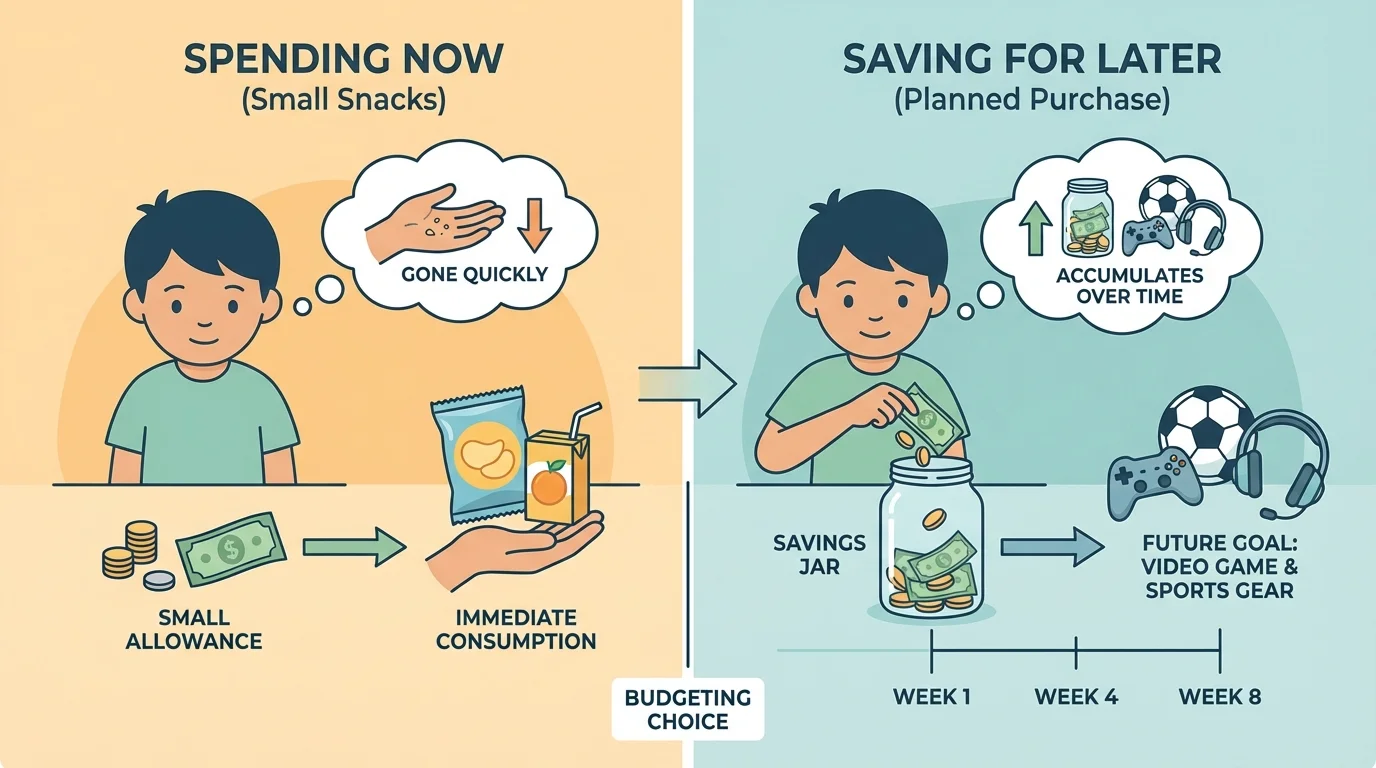

Real life changes. Maybe you expected $8 this week but only got $5. Maybe you spent more than planned on a small item. Maybe your goal changed. A good budget is flexible. [Figure 4]

If your income goes down, you have to lower at least one category. For example, if your plan was based on $12 but you only got $9, then your budget must shrink by \(12 - 9 = 3\). You might take $1 away from spending and $2 away from your planned purchase amount.

If you overspend in one category, do not ignore it. Move money from another category and rewrite the plan. That teaches you to notice the effect of your choices. If you spend an extra $2 today, that may mean waiting longer for a bigger goal.

When you add and subtract money amounts, always check that the total money going out does not become more than the money coming in. Your budget should balance.

Some weeks are different from others. A birthday may bring more money than usual. Another week may bring none at all. That is why it helps to budget again each time you get new money instead of assuming every week will look the same.

Every spending choice you make today affects what you can buy later. This is why smart budgeting is not just about math. It is also about self-control and priorities.

One helpful question is, "Do I want this now, or do I want my goal more?" Sometimes buying something small right away is fine because you planned for it. Other times, waiting helps you get something you care about more.

An impulse buy is something you buy quickly without planning. Impulse buys are not always terrible, but they can ruin a budget if they happen often. A snack here and a toy there can quietly use up all your money.

To avoid impulse buying, try the wait rule. If you want something that was not in your budget, wait one day before deciding. During that time, ask yourself whether you still want it and whether it fits your plan.

Needs, wants, and timing. Sometimes the best money choice is not "yes" or "no." It is "not yet." Waiting gives you time to compare options, check your budget, and decide if the purchase is worth it.

The choice shown in [Figure 4] is common in real life: a few small purchases now can delay a more meaningful purchase later. Budgeting helps you see that trade-off before it happens.

You do not need special software to budget. A notebook page works. A simple chart works. A note on a tablet or phone works. What matters is that your system is easy for you to update.

Here is a simple format you can copy:

| Money In | Saving | Spending | Planned Purchase | Remaining Balance |

|---|---|---|---|---|

| $10 | $3 | $2 | $5 | $0 |

Table 2. A basic budget tracker showing how one amount of income is fully assigned.

You can also keep a running total for a goal. If you are saving for something that costs $24 and you already have $9 saved, then you still need \(24 - 9 = 15\). Seeing your progress can keep you motivated.

Tracking a planned purchase goal

You want an item that costs $18. You already saved $7. This week you add $4 more.

Step 1: Find the new saved total.

\(7 + 4 = 11\)

Step 2: Find how much is still needed.

\(18 - 11 = 7\)

Step 3: Use the result to plan ahead.

You now know you need $7 more to reach your goal.

Tracking helps you know exactly where you stand.

If your family helps you manage money, you can share your written budget on a message, video call, or family planning note and ask for feedback. Another person may notice if your plan does not add up or if your goal amount needs adjusting.

Budgeting is useful in everyday situations. If you get birthday money, a budget can stop you from spending it all in one weekend. If you earn money from helping with tasks at home or in your neighborhood, a budget helps you keep part of it for future goals. If you want to buy a gift for someone, budgeting helps you set the money aside ahead of time.

Subscriptions and online purchases can also affect your budget. Even small recurring costs matter because they repeat. If something costs $2 each week, then after four weeks you have spent \(2 \times 4 = 8\). That could have been part of a bigger goal. Looking at repeated spending helps you make wiser choices.

Small amounts saved often surprise people. Saving just $2 each week for 10 weeks gives you \(2 \times 10 = 20\), enough for many planned purchases.

Budgeting is also helpful when plans change. Maybe a sale lets you buy something for less than expected. If your goal item drops from $25 to $20, then you save \(25 - 20 = 5\). That extra $5 can stay in savings or go toward another goal.

Good budgeting is easier when you build small habits. First, write your plan as soon as you get money. Second, check your budget before you buy something. Third, keep your saved money separate from your spending money if possible. Fourth, review your budget regularly.

You can do a fast budget check with three questions: How much do I have? What is it for? What will happen if I spend this now? Those questions take less than a minute, but they can prevent regret.

"A budget is telling your money where to go instead of wondering where it went."

These habits do not make money decisions perfect every time. They make your decisions stronger over time. The more often you budget, the easier it becomes to spot smart choices quickly.

Try This: The next time you receive money, pause before spending any of it. Write the total, choose one amount to save, one amount for spending, and one amount for a planned purchase. Then check that your numbers add up correctly.

Try This: If you already have a money goal, write the total cost and how much you have so far. Use subtraction to find what is left: total cost minus saved amount.

Try This: If you often make quick purchases, test the one-day wait rule on your next unplanned item and see whether you still want it later.