A surprising truth about money is that small choices can matter just as much as big ones. Spending $5 here and $8 there may not feel important in the moment, but over time, those choices can decide whether you have enough for something you really want. Money is limited, so every time you use some of it, you also give up other possibilities.

If you have ever had to choose between buying a snack, saving for a game, or putting money toward a gift, you already know what this topic is about. Real financial skill is not just knowing how to count money. It is knowing how to pause, compare options, and choose based on what matters most to you.

Every purchase is a decision. A spending choice is simply the way you decide to use your money. Some choices are quick, like buying a drink at a store. Others take more thought, like deciding whether to spend birthday money now or save it for later.

Good spending choices help you feel in control. Poor spending choices can leave you frustrated. For example, if you spend all your money on random online purchases, you may not have enough when something important comes up, like replacing broken headphones or contributing to a friend's birthday gift. The goal is not to never spend. The goal is to spend on purpose.

Spending choice means deciding how to use your money.

Opportunity cost is the value of the next best thing you give up when you choose something else.

Financial trade-off means accepting one benefit while also giving up another, such as paying less but getting lower quality.

These ideas show up in almost every money decision you make. They matter whether you are using allowance, gift money, earnings from chores, or money from a small job like pet sitting.

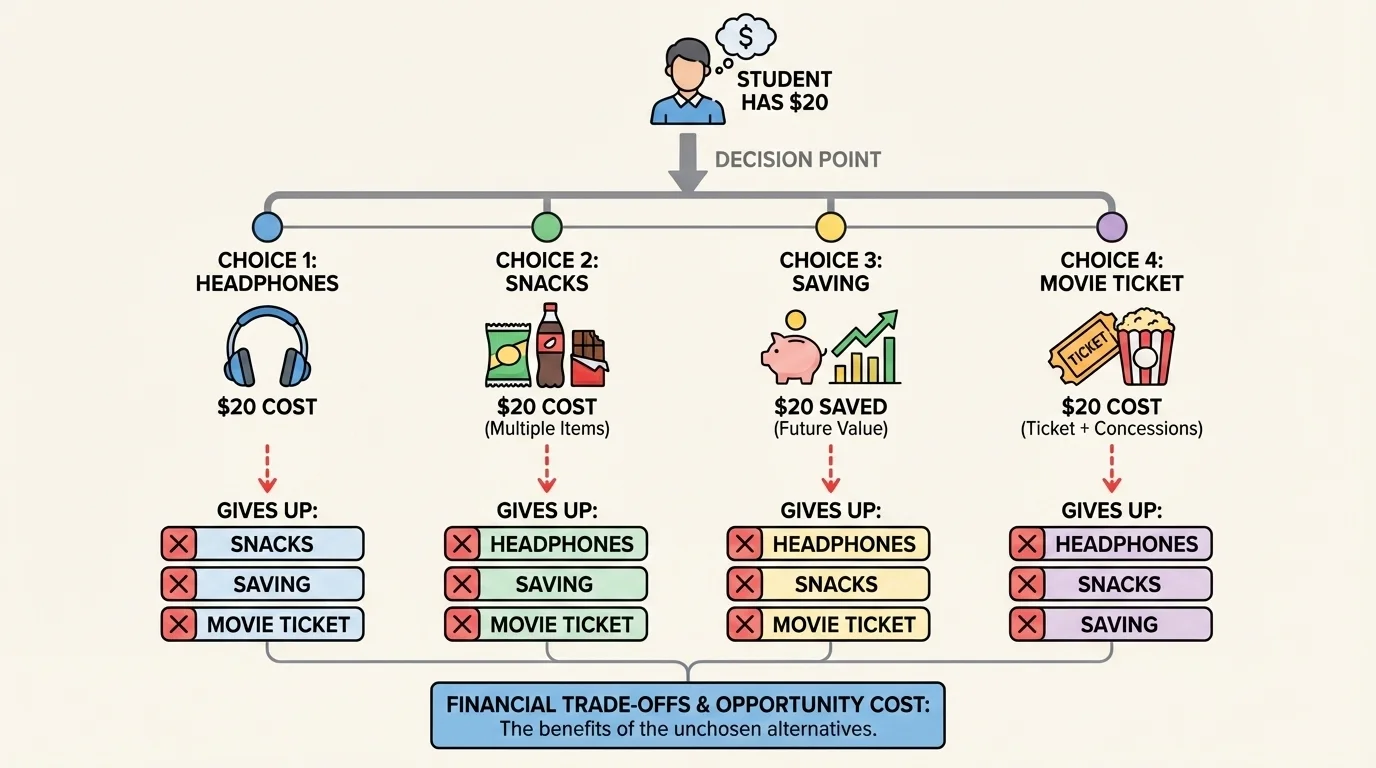

When you make a money decision, you are dealing with more than price. As [Figure 1] shows, choosing one option usually means saying no to something else. That "something else" is often your opportunity cost. If you spend $20 on fast food and treats, you cannot use that same $20 for a movie, a phone accessory, or savings.

A financial trade-off happens when each option has positives and negatives. Maybe one pair of earbuds costs less, but breaks quickly. Another costs more, but lasts longer. One choice saves money now. The other may save money later because you do not need to replace it as soon.

Here is the key idea: money choices are rarely just about what you buy. They are also about your goals, your timing, and what you lose by choosing one thing over another. This is why two people can make different choices with the same amount of money and both still be making smart decisions, depending on their priorities.

Stores and apps often try to make spending feel fast and easy because people are more likely to buy when they do not stop to think. Even waiting one day before buying something can change your decision.

That pause matters because your first reaction is not always your best reaction. Sometimes you want something because it looks exciting in a video, because friends are talking about it online, or because a sale seems urgent. But a smart choice comes from asking whether the purchase actually fits your needs and plans.

One helpful way to think about money is to sort purchases into needs, wants, and priorities. A need is something important for daily life or basic function. For a student, this might include school supplies for online learning, replacing shoes that no longer fit, or paying for something necessary for an activity. A want is something nice to have but not necessary, like extra snacks, game add-ons, or trendy accessories.

Priorities are personal. Something can be a want and still be a high priority for you. For example, if you have been saving for a drawing tablet because art matters to you, that tablet may be a high priority even though it is not a basic need. This is why smart money choices are not about other people telling you what to value. They are about making sure your spending matches what you value.

Try asking yourself three quick questions before spending: Do I need this? Do I really want this? Is this more important than the other things I could do with the money? That last question brings you back to opportunity cost.

Example: needs, wants, and priorities

Step 1: Jordan has $30.

Jordan is considering a $6 smoothie, a $12 phone case, and adding $20 to a savings goal for a new skateboard.

Step 2: Sort the options.

The smoothie is a want. The phone case might be a need if the old one is broken, or a want if it is just for style. The skateboard savings is a priority because Jordan has a larger goal.

Step 3: Compare outcomes.

If Jordan buys the smoothie and phone case, the total is \(12 + 6 = 18\). That leaves \(30 - 18 = 12\), which is less progress toward the skateboard.

Step 4: Make a choice based on priorities.

If the current phone case still works, Jordan might skip both purchases and save $30, or skip the smoothie and save $24.

The best choice depends on what matters most to Jordan right now.

You do not have to label every purchase as "good" or "bad." A treat is not automatically a bad decision. Problems usually happen when wants quietly take over your whole budget and push out your bigger priorities.

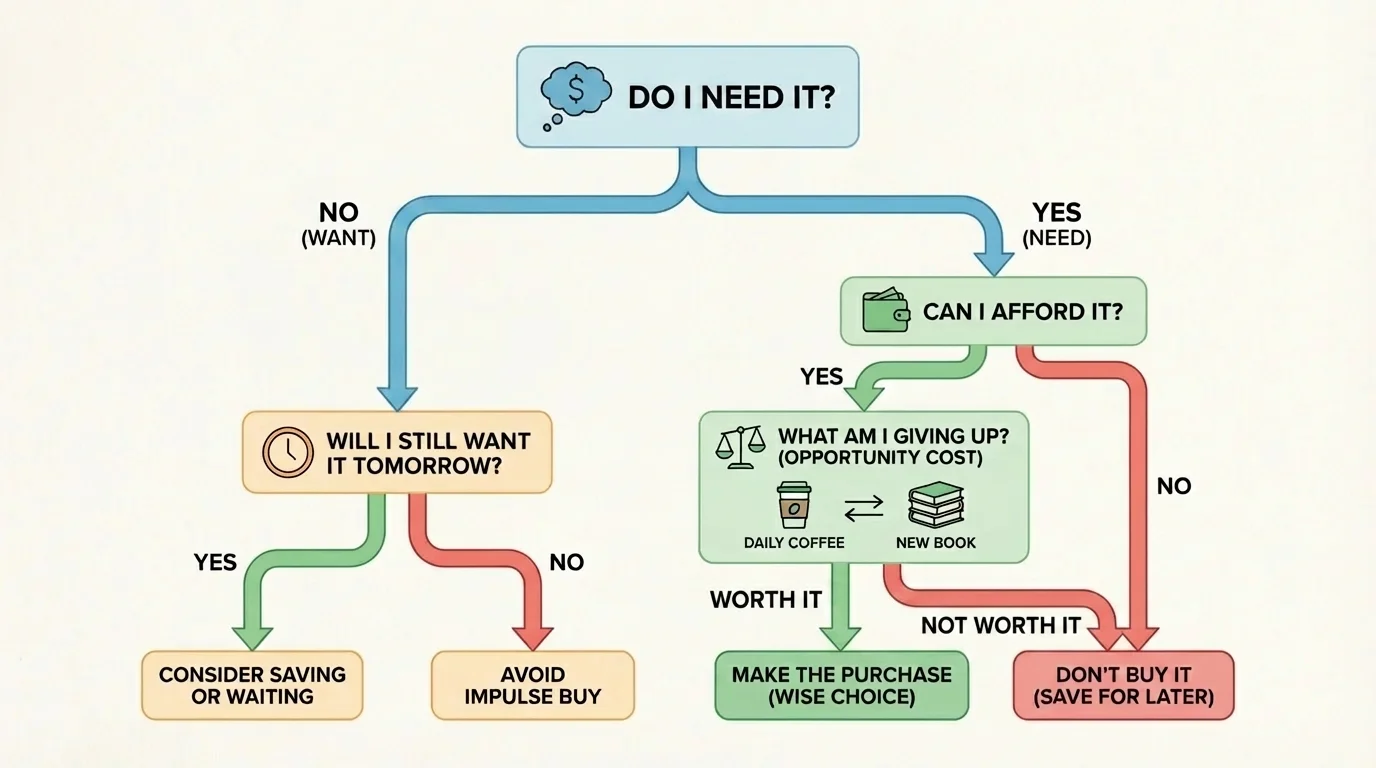

You do not need a complicated system to make better money decisions. A quick process, like the one in [Figure 2], can help you slow down and think clearly before you buy.

Step 1: Ask what you are buying and why. Are you solving a real problem, or are you bored, pressured, or caught up in the moment?

Step 2: Check whether you can afford it without ruining another plan. If you have $25 and want to spend $18, ask yourself whether the remaining $7 is enough for anything else you need or care about.

Step 3: Identify the opportunity cost. What is the next best thing you would do with that money instead?

Step 4: Think about the future. Will you still feel good about this purchase tomorrow, next week, or next month?

This process works especially well for online shopping, in-app purchases, and limited-time deals. Those situations are designed to make you act fast. Taking even a short pause can stop regret before it starts.

A useful rule is the impulse purchase check. An impulse purchase is something you buy quickly without planning. If you were not thinking about it before today, give yourself a waiting period. For a small purchase, wait a few hours. For a bigger one, wait a day or more.

Why waiting helps

Strong feelings can make a purchase seem more important than it really is. Waiting gives your brain time to compare the item with your goals, your savings, and other choices. Often, the item feels less urgent after a little time passes.

Later, when you face another decision, the same framework still helps. Just as [Figure 2] shows, the best questions are usually simple ones asked at the right time.

Opportunity cost becomes easier to understand when you see it in ordinary situations. Suppose you have $15.

If you spend $15 on snacks during the week, your opportunity cost might be not having money for a streaming rental with your family over the weekend. If you spend the $15 on a game item, your opportunity cost might be having to wait longer to save for a real-world item you use often, like sports gear or another physical item.

Sometimes the opportunity cost is not another item. It can be time or flexibility. If you commit your money to one thing, you lose the ability to use it later for a better opportunity. Keeping some money unspent can be a smart choice because it gives you options.

Example: finding the opportunity cost

Step 1: Maya has $40.

She can buy a $40 concert livestream ticket or keep saving for a $60 pair of running shoes.

Step 2: Identify the choice.

If Maya buys the livestream ticket now, she uses all $40.

Step 3: Identify the next best alternative.

The next best alternative is putting the $40 toward the running shoes.

Step 4: State the opportunity cost.

The opportunity cost of the livestream ticket is the lost progress toward the shoes. Maya would still need \(60 - 40 = 20\) more if she saved instead.

This does not mean the ticket is a wrong choice. It just means Maya should be honest about what she is giving up.

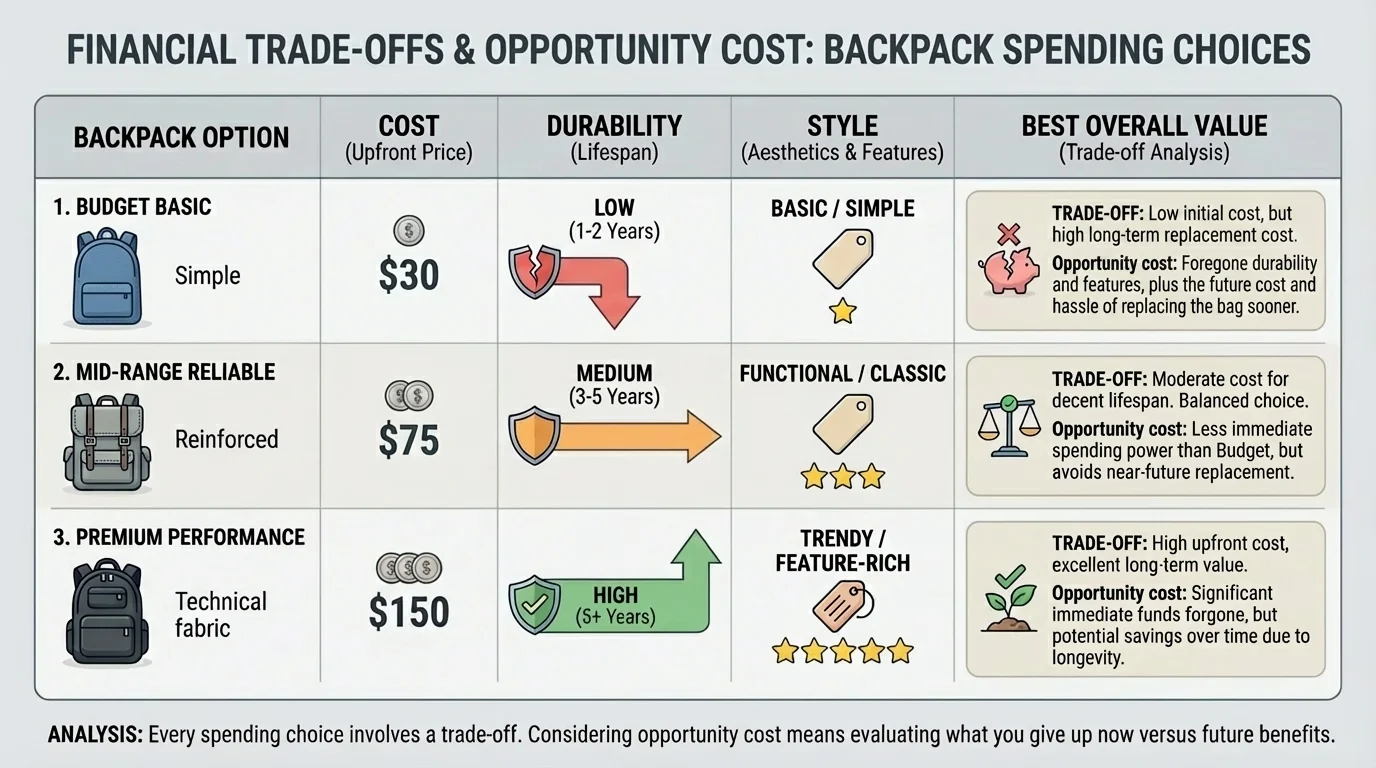

Financial decisions are often comparisons between several good-enough options, not between one perfect option and one terrible option. [Figure 3] shows how comparing several factors at once can lead to a smarter choice than looking at price alone.

For example, suppose you need a backpack. One costs $18 but tears easily. Another costs $28 and lasts two school years of daily use. A third costs $35 and has extra features you do not really need. The cheapest option is not always the best value, and the most expensive option is not automatically the smartest either.

When comparing trade-offs, look at these questions:

Sometimes paying more upfront saves money later. Suppose one water bottle costs $10 and lasts a month before leaking, while another costs $18 and lasts a year. The second bottle may actually be the better deal if it prevents repeated replacement.

| Option | Cost | Likely Use | How Long It Lasts | Possible Trade-Off |

|---|---|---|---|---|

| Cheap earbuds | $9 | Often | Short time | Lower cost now, may replace sooner |

| Mid-range earbuds | $20 | Often | Longer | Higher cost now, better durability |

| Premium earbuds | $45 | Often | Longer | Best features, but may delay other goals |

Table 1. A comparison of purchase options showing how cost, use, and durability affect trade-offs.

The same kind of thinking from [Figure 3] works for clothes, electronics, hobbies, and food choices. Looking at value instead of only price helps you spend more wisely.

A budget is a plan for how you will use your money. Even a simple budget makes spending choices easier because it gives each dollar a job before you spend it.

Let's say you receive $50 for the month. You might plan:

That total is \(20 + 15 + 10 + 5 = 50\). Now if you want to buy a $14 item, you know which part of your money it should come from. If you already used your personal spending money, then buying the item means taking from savings, gifts, or flexibility. That is a trade-off.

Example: adjusting a budget after a purchase

Step 1: Start with the plan.

Savings: $20, spending: $15, activities: $10, flexible: $5.

Step 2: Buy a $12 game card.

If the game card comes from spending money, then the new spending amount is \(15 - 12 = 3\).

Step 3: Notice the effect.

Only $3 remains for other fun purchases this month, so another nonessential purchase may need to wait.

Budgets do not stop you from spending. They help you see the real effect of spending.

Tracking your money also helps. You can use notes on your phone, a spreadsheet, or a simple paper list at home. If you write down what you spend for even one week, patterns become obvious. You may notice that several small purchases add up fast.

Adding small amounts still matters. For example, four purchases of $4 add up to \(4 + 4 + 4 + 4 = 16\). Small spending can quietly become big spending.

That is why many people are surprised by where their money goes. They remember the big purchases but forget the repeated small ones.

Some spending mistakes happen because of poor planning. Others happen because companies are very good at influencing people. Limited-time offers, countdown clocks, free shipping minimums, "buy now" buttons, and social media trends can all make you feel that you should spend right away.

One common trap is the subscription. A subscription is a payment that repeats automatically, such as monthly access to an app or service. A small recurring cost can feel harmless, but over several months it adds up. For example, a $6 monthly app charge becomes \(\$6 \times 4 = \$24\) in four months.

Another trap is comparing yourself to other people online. Someone else's purchase does not tell you whether it is a smart choice for your life. People often post the exciting result, not the money stress behind it.

"When you say yes to one thing, you are also saying no to something else."

That quote is a simple way to remember opportunity cost. It applies to money, time, and energy.

Good financial habits do not need to be complicated. They need to be consistent. Start by setting one short-term goal and one longer-term goal. A short-term goal might be saving $15 for a book or accessory. A longer-term goal might be saving $80 for sports equipment, event tickets, or a creative tool.

Next, split incoming money on purpose. When you receive money, decide how much goes to saving, spending, and giving or sharing. Even saving a small amount regularly builds progress. For example, saving $5 from each of six payments gives \(5 \times 6 = 30\).

Talk about purchases with a trusted adult if the choice feels big. You are not asking them to control your money. You are using another perspective to spot trade-offs you may have missed. This is a strong skill, not a weak one.

Review your past choices without shame. Ask: Was it worth it? Would I buy it again? What did I give up? Honest reflection helps you improve.

Progress matters more than perfection

Everyone makes money mistakes. What matters is noticing patterns, learning from them, and making one better choice next time. Financial confidence grows through practice.

As you keep making decisions, the ideas from [Figure 1] stay important: one choice opens one path and closes another. The more clearly you see those paths, the stronger your decisions become.

Sometimes all your options have downsides. Maybe you want to save for something important, but you also need to replace an item you use every day. Maybe the lower-cost option is less durable, but the higher-cost option is out of reach right now. In real life, money decisions are often about choosing the best available option, not the perfect one.

When this happens, focus on what you can control. Can you wait? Can you find a lower-cost version? Can you borrow, repair, or use something you already have a little longer? Can you earn more money through age-appropriate tasks like yard help, pet care, tutoring a younger child online with parent approval, or selling a craft?

Financial skill grows when you stay calm, compare your choices, and pick the option that best fits your situation right now. Then you adjust as needed. That is real-world money management.