A lot of money problems do not start with huge mistakes. They start with tiny habits: buying without thinking, forgetting where money went, or telling yourself, "It's only a few dollars." The good news is that strong money habits work the same way. Small smart choices, repeated over time, can help you save for things you care about, avoid stress, and feel more confident every time you spend.

Money is a tool. At your age, that tool might come from allowance, gifts, doing chores, selling handmade items online with adult help, or earning a little money through local jobs like pet sitting or yard work. No matter where it comes from, learning how to manage it now makes life easier later. You do not need a lot of money to build good habits. You just need a plan and the willingness to practice it.

Good financial habits help you do three big things: save for goals, plan ahead, and spend responsibly. Saving means putting aside money now so you can use it later. Planning means deciding ahead of time where your money should go. Responsible spending means using your money in ways that match your needs, values, and goals instead of making random choices.

Think about two students who each get $15 a week. One spends almost all of it on snacks, game add-ons, and quick purchases online. By the end of the month, that student has very little to show for it. The other sets aside part of the money each week, tracks spending, and waits a day before making extra purchases. After four weeks, that student has money saved and probably feels more in control. The amount was the same. The habits were different.

Saving means keeping some money for future use instead of spending it right away. Budgeting means making a plan for how to use your money. Responsible spending means making thoughtful choices so your money supports what matters most to you.

When you use money well, you get more than just stuff. You get choices. You might be able to buy a gift, handle an unexpected cost, or save for something meaningful without feeling panicked. That feeling of control is one of the best reasons to build money habits early.

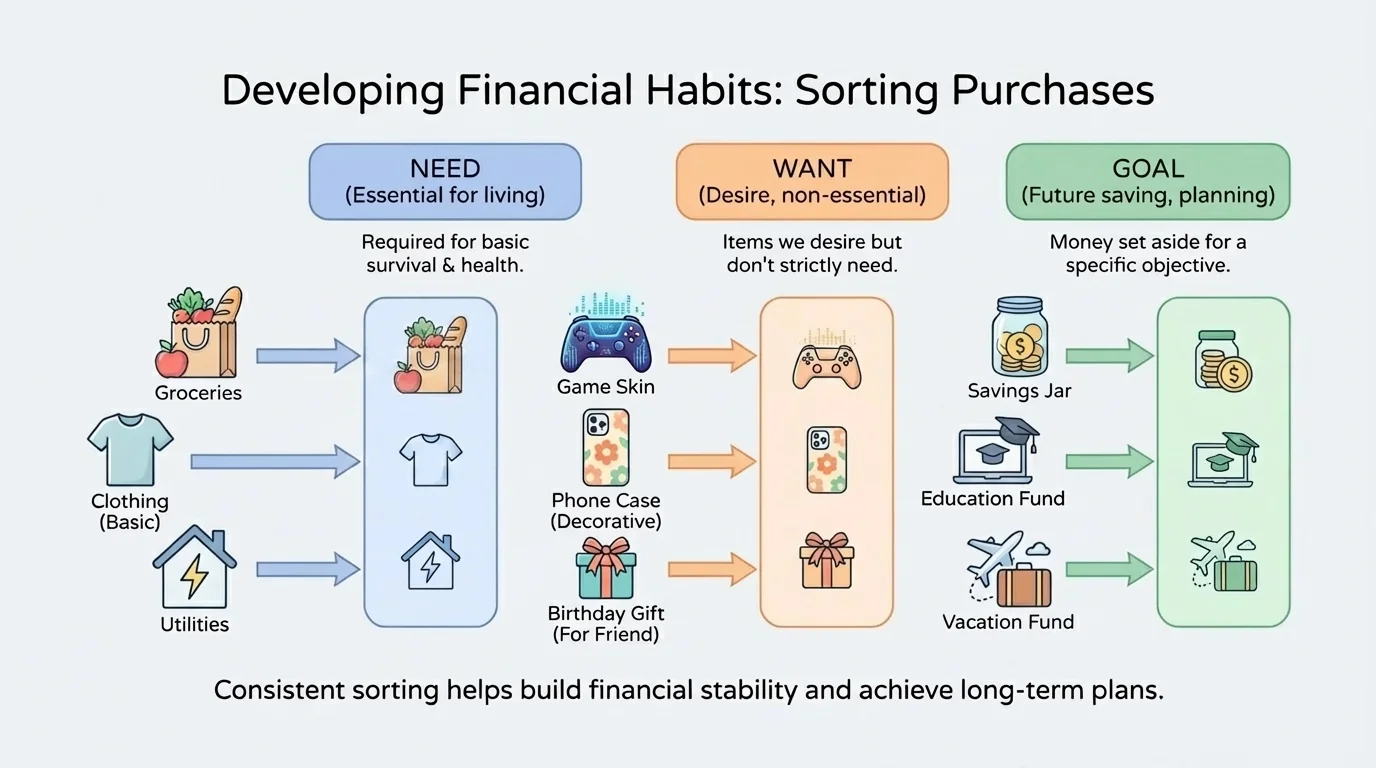

One of the most useful money skills is learning how to sort purchases by priority. A simple way to do that is to think about needs, wants, and values. This kind of sorting, as shown in [Figure 1], helps you pause before spending and ask, "What kind of purchase is this?"

A need is something important for basic living, health, safety, or daily function. At your age, many needs are handled by adults in your household, but you still make choices connected to them, such as replacing school supplies for online learning, buying hygiene items, or contributing to an activity fee. A want is something you would enjoy but do not truly need, like a new game, extra accessories, or trendy decor for your room. Values are what matter most to you. Maybe you value creativity, sports, helping others, or saving for a future goal.

Here is where it gets interesting: the same item can be a want for one person and part of a value-based goal for another. A plain notebook may just be paper to one student, but for another student who loves writing stories, it supports a real priority. That does not mean every wanted item becomes a need. It means you should think about whether a purchase matches your actual goals.

Try asking yourself three quick questions before buying anything: Do I need it? Do I just want it right now? Does it fit something important to me? If the answer is "I just want it right now," that does not automatically make it bad. It just means you should be honest about what it is.

This habit protects you from a common problem: spending based on mood instead of purpose. You might feel bored, left out, or excited after seeing something on social media. When that happens, your brain may push for a fast decision. Sorting the purchase into need, want, or value helps slow that down. The categories in [Figure 1] remind you that every dollar can only be used once, so choosing one thing means saying no to something else.

Many stores and apps are designed to make spending feel fast and easy. Bright colors, countdown timers, "limited-time" labels, and one-click buying all try to reduce the amount of thinking you do before purchasing.

A smart habit is to write down one or two current goals. For example: "Save for wireless earbuds," or "Keep some money ready for a birthday gift." When your goals are clear, spending decisions become easier because you are not choosing in the dark.

A budget does not have to be complicated. It is simply a plan for money coming in and money going out. A simple plan helps you decide what to do with your money before you spend it.

[Figure 2] Start with your total amount. Suppose you receive $20 this week. One easy method is to split it into three parts: save, spend, and optional giving or sharing. For example, you might save $8, plan to spend $10, and set aside $2 for a gift, donation, or family contribution. In math, that plan is \(8 + 10 + 2 = 20\). Because the total matches what came in, your plan works.

You can also think in percentages if that helps. Saving about \(\dfrac{1}{4}\) to \(\dfrac{1}{2}\) of your money is a strong habit when possible. For a $20 amount, \(\dfrac{1}{4}\) is found by calculating \(20 \div 4 = 5\), so saving one-fourth would be $5. Saving half would be \(20 \div 2 = 10\), so that would be $10. You do not have to use the exact same amount every week, but choosing a regular saving percentage can make the habit automatic.

The best budgets usually follow one important rule: pay yourself first. That means you move money into savings before you start spending. If you wait to save whatever is left over, there often is not much left. Saving first is one of the strongest habits you can build.

Example: making a weekly plan

You earn $24 for helping with yard work and want to save for a $60 item.

Step 1: Choose a saving amount.

If you save half, then \(24 \div 2 = 12\), so you save $12.

Step 2: Find the amount left for other uses.

Money left after saving is \(24 - 12 = 12\), so you still have $12 for planned spending or sharing.

Step 3: Estimate progress toward the goal.

If you save $12 each time, then \(60 \div 12 = 5\). You would reach $60 after about 5 similar earning periods.

This plan turns a big goal into smaller, doable steps.

Plans should be realistic. If you make a plan so strict that you never allow yourself any enjoyable spending, you may give up on it. A better budget includes both responsibility and choice.

A spending plan works much better when you also track your money. Tracking means recording what comes in, what goes out, and what remains. You can do this with a note on your device, a spreadsheet, or a small notebook.

Tracking matters because memory is not always accurate. You may think, "I barely spent anything," but then realize you bought a drink, two app purchases, and a snack over a few days. Those smaller amounts can add up fast. For example, spending $3 four times in one week gives \(3 + 3 + 3 + 3 = 12\), which is $12 gone on things you might not even remember clearly.

A good tracker includes the date, the item, the cost, and the reason. That last part is powerful. If you notice that many purchases happen when you are bored or scrolling online late at night, you have learned something useful. You are not just tracking money. You are tracking behavior.

| Date | Item | Cost | Reason |

|---|---|---|---|

| Mon | Snack | $3 | Hungry after practice |

| Wed | Game add-on | $4 | Friends were buying it |

| Fri | Gift bag | $2 | Birthday gift prep |

| Sat | Savings deposit | $6 | Goal: headphones |

Table 1. A simple spending tracker showing date, item, cost, and reason for each money choice.

Tracking also helps you find "money leaks." A money leak is a small repeated expense that quietly drains your money. One leak might not seem important, but repeated leaks can block your goals. If you notice a pattern, you do not need to feel guilty. You just need to adjust.

Why small amounts matter

People often ignore small purchases because each one seems harmless. But repeated spending creates a pattern. If you spend $5 every weekend, then after four weekends you have spent \(5 \times 4 = 20\). After ten weekends, you have spent \(5 \times 10 = 50\). Small habits can either build savings or erase them.

One useful routine is to check your tracker once a week. Look for three things: what you did well, what surprised you, and one thing to change next week.

Saving is easier when you know why you are doing it. A goal gives your savings a job. Instead of just "saving money," you might be saving for a sports item, art supplies, a special event, a future trip, or a backup fund for unexpected needs.

There are different types of savings goals. Short-term goals are things you can reach fairly soon, such as in a few weeks or months. Long-term goals take more time and patience. It also helps to build a small emergency fund, which is money saved for unexpected expenses. At your age, that might help with replacing something important, covering a last-minute need, or avoiding the stress of having no money available at all.

A goal works best when it is specific. "I want to save more" is hard to follow. "I want to save $40 for a new sketchbook set in the next two months" is much clearer. Then you can break it down. If you need $40 in 8 weeks, saving \(40 \div 8 = 5\) means putting aside $5 each week.

Example: breaking a goal into weekly saving

You want to save $48 in 6 weeks.

Step 1: Identify the total goal and time.

Total needed is $48, and the time is 6 weeks.

Step 2: Divide to find the weekly amount.

Calculate \(48 \div 6 = 8\).

Step 3: Use the result as your weekly target.

You need to save $8 each week to reach the goal on time.

Breaking a big amount into smaller pieces makes saving feel possible.

Another helpful idea is to keep savings separate from spending money when possible. If all your money is mixed together, it is easier to spend your goal money by accident. Even using two labeled envelopes or two notes in a digital tracker can help.

Saving can feel slow at first, but progress builds. If you save $6 one week, then another $6 the next week, your total becomes \(6 + 6 = 12\). Add $8 the next week and you have \(12 + 8 = 20\). Watching the total grow can be motivating because it proves your habit is working.

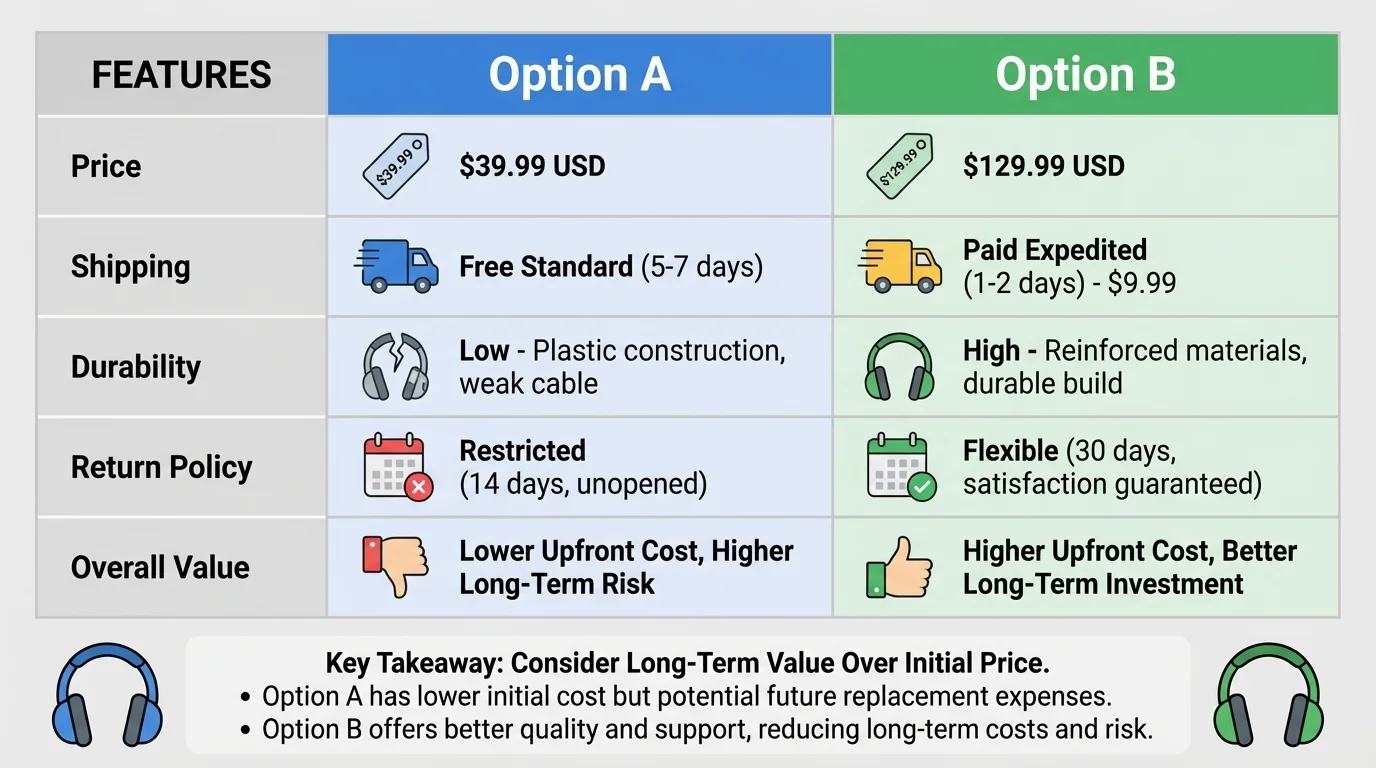

Responsible spending is not just about spending less. It is about spending better. One strong habit is comparison shopping, which means looking at options side by side before buying. As [Figure 3] shows, the cheapest price is not always the best value.

Suppose one pair of headphones costs $18 and another costs $25. The $18 pair seems better at first. But what if the cheaper one breaks quickly, has an extra $6 shipping fee, or cannot be returned? Then the more expensive pair may actually be the smarter buy. Good spending decisions look at total cost, quality, how long the item lasts, and whether you will truly use it.

Another useful idea is cost per use. If you buy a $20 water bottle and use it 100 times, the cost per use is \(20 \div 100 = 0.2\), which is 20 cents per use. If you buy a $10 novelty item and use it once, the cost per use is much higher. Thinking this way can help you decide whether something is really worth it.

Impulse buying is another challenge. An impulse purchase is something you buy quickly without planning, often because of emotion, pressure, or excitement. One of the best ways to stop impulse buying is the wait rule. For small wants, wait at least 24 hours. For bigger purchases, wait a few days. If you still want the item and it fits your plan, then think again about buying it.

This wait rule is especially useful online. Advertisements, influencers, and shopping apps often make products feel urgent. You may see "Only 2 left" or "Sale ends tonight." Sometimes those messages are real, but sometimes they are just designed to push quick action. The comparison habits in [Figure 3] help you slow down and choose based on value, not pressure.

When you compare choices, go back to your needs, wants, and values. A purchase can be exciting and still not be the right choice for you right now.

Also watch for subscriptions and repeat charges. A free trial can turn into a regular payment if no one cancels it. Before signing up for anything online, read the terms carefully and check with a trusted adult.

Today, money moves quickly through apps, websites, and digital games. That makes spending more convenient, but it also increases risk. If you use a family account, payment app, or online store with permission, be careful with your information. Never share passwords, security codes, or payment details with friends or strangers.

A scam is a trick used to steal money or personal information. Scams can look like fake giveaways, messages claiming you won a prize, links to fake stores, or requests to "verify" account information. If something feels rushed, secret, or too good to be true, pause. That is a warning sign.

Use a simple safety checklist: check the website name, avoid random links, ask a trusted adult before entering payment information, and never feel pressured to act immediately. Responsible spending includes protecting your money, not just deciding how to use it.

"Do not save what is left after spending; spend what is left after saving."

— Warren Buffett

One more digital habit: keep records. Save receipts, screenshots of order details, and confirmation emails when appropriate. If something goes wrong, those records help you solve the problem.

Financial habits get stronger when you repeat them. You do not need a complicated system. A short weekly routine can keep you organized and prevent money stress from building up.

Step 1: Count or check how much money you have. Step 2: Move part of it to savings first. Step 3: Decide what spending is already planned. Step 4: Write down purchases during the week. Step 5: Review what happened and make one improvement for next week.

Here is a realistic example. You start the week with $14. You save $5 right away. That leaves \(14 - 5 = 9\) for spending. During the week, you spend $3 on a snack and $4 on supplies, so total spending is \(3 + 4 = 7\). Now you have \(9 - 7 = 2\) left in spending money, while your $5 savings is still protected.

Example: checking your week

You planned to spend no more than $12 this week but actually spent $15.

Step 1: Compare the plan and the real amount.

Difference is \(15 - 12 = 3\).

Step 2: Identify the reason.

Maybe there was one unplanned purchase, or several small ones that added up.

Step 3: Make one adjustment.

You might lower next week's extra spending by $3, use the 24-hour wait rule, or bring a snack from home when possible.

The goal is not perfection. The goal is noticing, learning, and adjusting.

Good money habits are not about being afraid to spend. They are about making your money match your goals. When you save regularly, plan ahead, track spending, compare options, and stay alert online, you become the person in charge of your money instead of the person wondering where it went.

Try This: Choose one habit to start today: track every purchase for one week, save a fixed amount first, or wait 24 hours before buying wants. Small actions done consistently create real financial strength.