If every person had to hide money at home, pay for everything in cash, and keep track of every dollar with no records, everyday life would be much harder. Buying groceries, saving for a bike, paying a bill, or sending money across town would take more time and cause more mistakes. Banking helps solve these problems. It gives people safe places to keep money, ways to move money, and tools to plan for the future.

Banking is a big part of daily life. Adults may get paid by direct deposit into a bank account. Families may use a bank card at a store. A student who receives birthday money may place some of it into savings for a future goal. Even when people do not see the inside of a bank building very often, banking services are working behind the scenes.

The main function of banking is to help people manage money. That includes keeping money safe, recording how much money a person has, allowing people to take money out when needed, and helping people send money to others. Banks also lend money so families and businesses can make major purchases and pay the money back over time.

Banking is the system of storing, borrowing, lending, and moving money through banks and other financial institutions.

Financial institution is an organization that helps people manage money. Banks and credit unions are common examples.

People use banks because banks make money easier to organize. Instead of carrying all of your cash everywhere, you can keep money in an account. The bank keeps a record of what goes in and what comes out. That record helps people know their balance and make good choices.

A bank is a business that offers financial services. It accepts money from customers, protects it, keeps records, and provides ways to use it. Some banks have buildings people can visit, while others also offer online tools and phone apps.

Another kind of financial institution is a credit union. A credit union is similar to a bank because it holds money and offers accounts and loans. One difference is that credit unions are owned by their members. For this lesson, it is helpful to remember that both banks and credit unions help people manage personal finances.

Banks do not simply put each person's money into a labeled box and leave it there. They keep careful records showing how much belongs to each customer. This is one reason banking is so important: good records help people know what they have, what they spent, and what they still need to save.

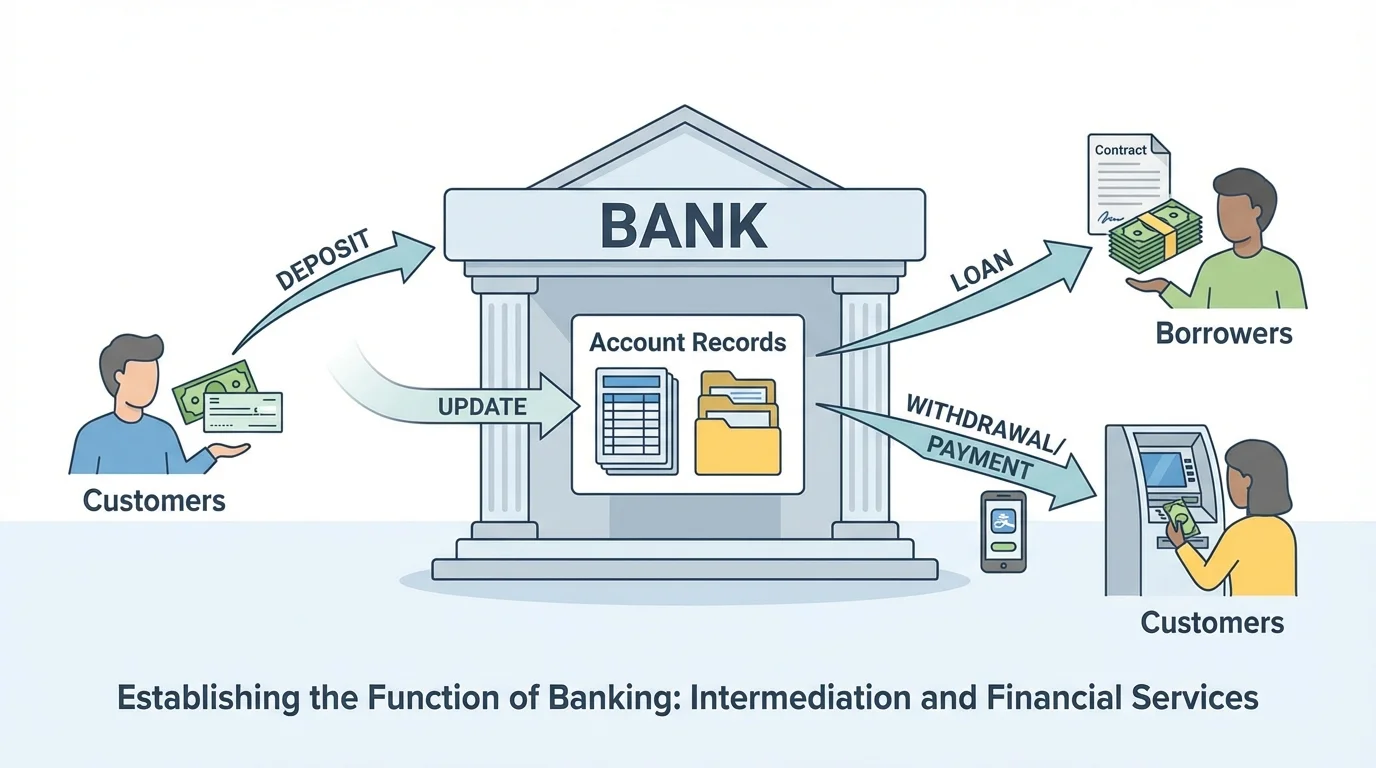

One way to understand banking is to think about a system that stores, tracks, and moves money, as [Figure 1] illustrates. The first important function is keeping money safe. Money kept in a secure account is usually safer than money left loose in a backpack, desk drawer, or bedroom.

The second major function is recordkeeping. Banks track each deposit, each withdrawal, and each payment. This creates an account history. If a family wants to check whether they already paid a bill or whether they can afford a purchase, bank records help them decide.

The third function is moving money from one place to another. A bank can help a person pay a bill, use a card at a store, take out cash from an ATM, or send money electronically. The fourth function is lending money. Banks lend money to people and businesses, then receive the money back over time.

A fifth function is helping people save. Some accounts pay interest, which is extra money paid by the bank for keeping money in an account. If someone leaves money in savings, the balance can slowly grow.

Banks also help communities. When banks lend money, families may buy homes or cars, and businesses may buy supplies or hire workers. So banking affects not only one person's wallet but also the larger economy around them.

Many people receive money without touching paper cash at all. A paycheck can be deposited directly into a bank account, and bills can be paid electronically from that account.

The movement shown earlier in [Figure 1] helps explain why banks are more than storage places. They are centers for money activity. They connect saving, spending, and borrowing in one system.

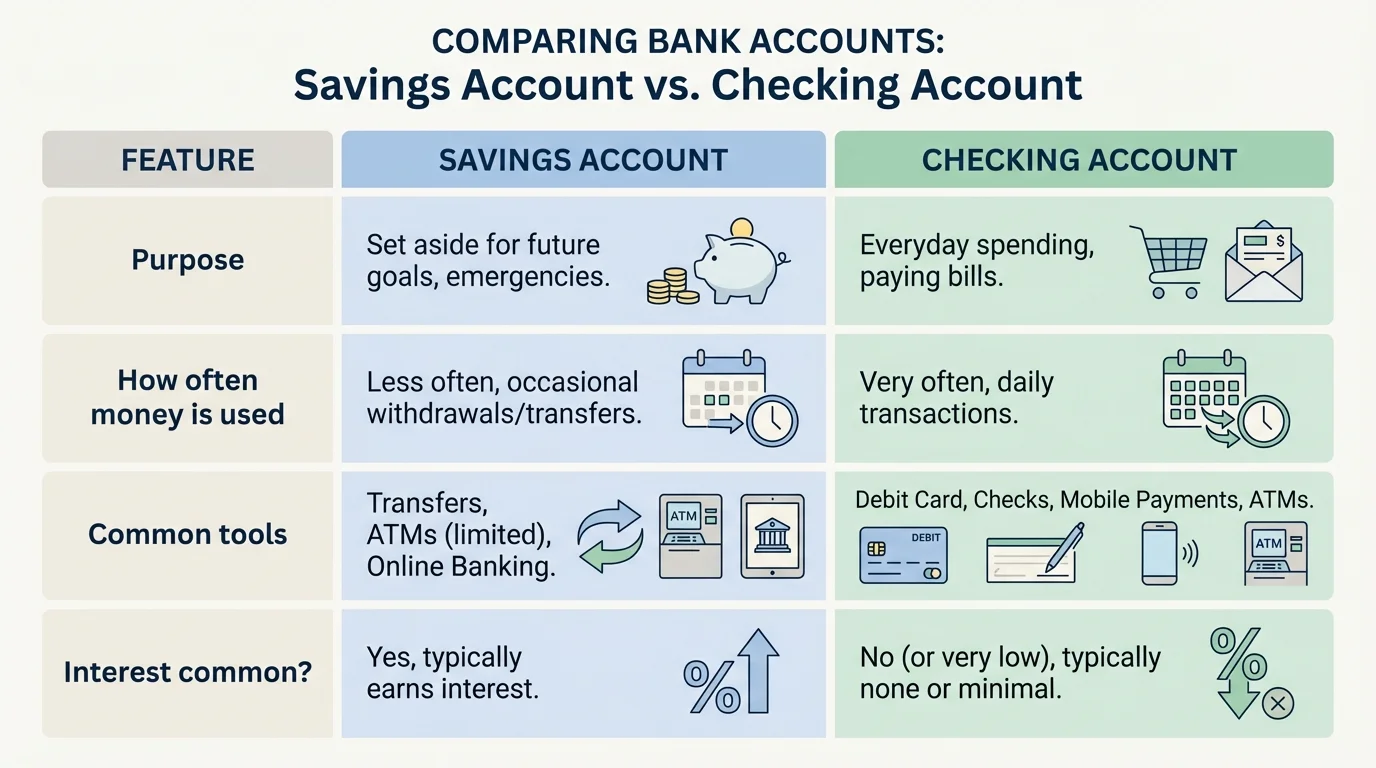

[Figure 2] The two most common accounts for individuals are a savings account and a checking account. These accounts have different jobs. People often use savings accounts for money they want to keep for later and checking accounts for money they plan to use more often.

A savings account is meant for setting money aside. It can help with goals such as buying sports equipment, saving for holiday gifts, or building an emergency fund. A checking account is designed for regular spending, such as groceries, bills, and other everyday purchases.

Although both accounts hold money, they are not exactly the same. A savings account may earn more interest, but a checking account may be easier to use for frequent payments. Families often use both so they can separate money for spending from money for saving.

| Account Type | Main Purpose | How Often It Is Used | Common Tools |

|---|---|---|---|

| Savings account | Save money for future goals | Less often | Online transfers, bank visits |

| Checking account | Spend and pay for regular needs | More often | Debit card, checks, ATM, online payments |

Table 1. A comparison of common personal bank account types and how they are used.

Suppose Elena puts $20 into savings each month for a new scooter. After three months, she has saved \(20 + 20 + 20 = 60\). Her savings account helps her protect that money so she is less likely to spend it too soon. Now suppose Elena's parent keeps money for weekly shopping in a checking account. That money is meant to be used regularly, so checking is the better fit.

Account choice example

A family keeps $300 for monthly bills and $150 for a future vacation. Which account type best fits each amount?

Step 1: Think about the purpose of each amount.

The $300 is for bills that will be paid soon. The $150 is for a later goal.

Step 2: Match the purpose to the account.

Money for bills fits a checking account. Money for a future goal fits a savings account.

The best choice is checking for the $300 and savings for the $150.

When students understand the difference between these two accounts, they begin to see how banking helps people organize money by purpose. That makes planning easier and reduces confusion.

A deposit means putting money into an account. A withdrawal means taking money out. The amount of money in the account at a certain time is called the balance. These are basic ideas in banking, and people use them all the time.

If Jamal has $85 in his account and deposits $25, his new balance is \(85 + 25 = 110\). If he later withdraws $40, the balance becomes \(110 - 40 = 70\). Keeping track of these changes helps prevent overspending.

Tracking a bank balance

Sofia starts with $50 in her account. She deposits $30 and then withdraws $18. What is her final balance?

Step 1: Add the deposit.

Starting balance: $50. After depositing $30, the balance is \(50 + 30 = 80\).

Step 2: Subtract the withdrawal.

After withdrawing $18, the balance is \(80 - 18 = 62\).

Sofia's final balance is $62.

Bank statements and banking apps make these changes easier to follow. People can review when money came in, when money went out, and whether the current balance matches their plans.

Checking a balance often is a smart habit. It helps people avoid spending more money than they have and helps them notice mistakes quickly.

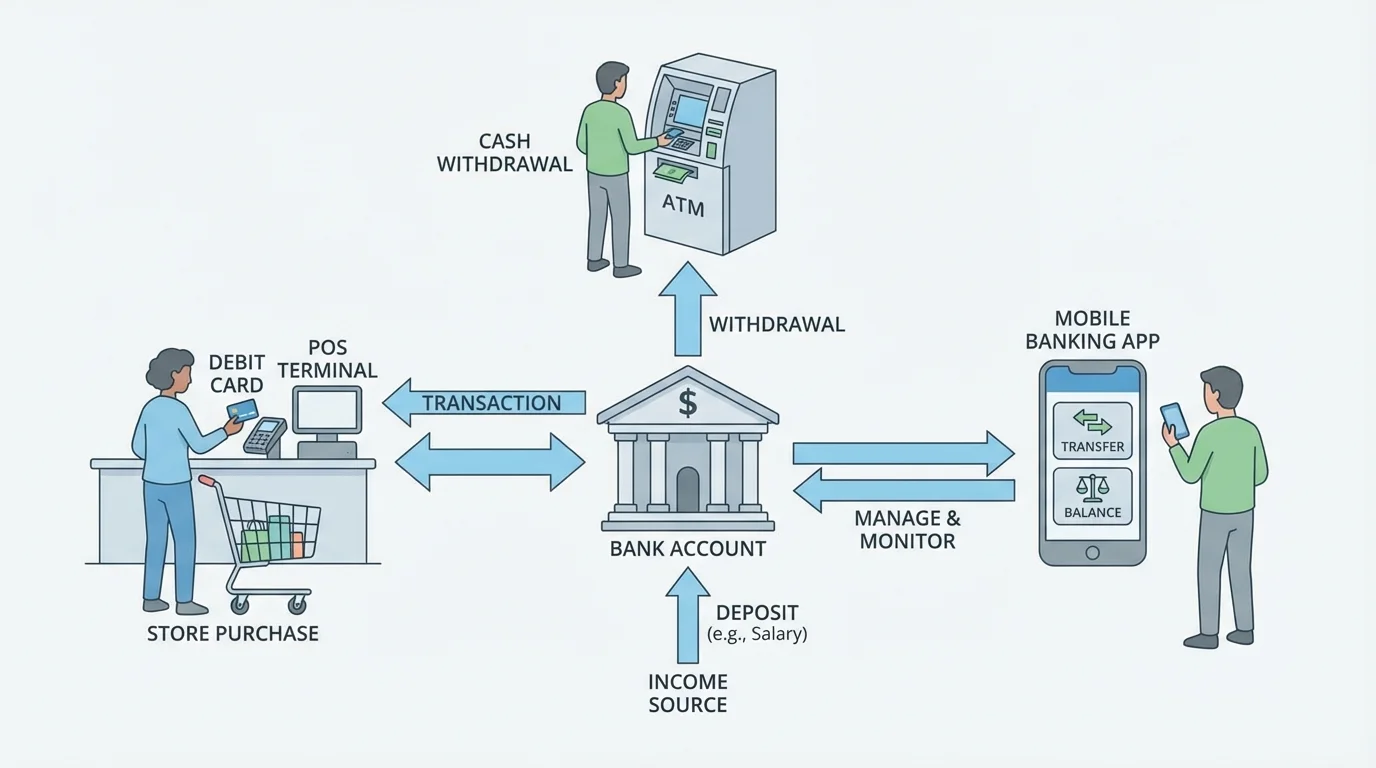

[Figure 3] People use several tools to reach the money in their accounts. A debit card lets a person pay directly from a checking account. An ATM, or automated teller machine, allows people to take out cash, check balances, and sometimes deposit money without going inside a bank.

Online banking lets customers use a computer or phone to see balances, move money, and pay bills. A person may have one account but many ways to use it: at a store with a card, at an ATM for cash, or online from home.

This makes banking faster and more convenient. For example, if a parent notices a utility bill is due today, online banking may let that person pay it in minutes. If a student needs lunch money in cash, an adult may use an ATM to withdraw the amount.

Convenience is helpful, but it also means people must act carefully. Cards and apps are useful only when protected with secure passwords and secret PINs. A PIN is a personal identification number used to help prove the user is allowed to access the account.

Money choices are strongest when people know the difference between wants and needs. Banking tools help people use money, but wise decisions still matter.

Later, when comparing safe habits, it helps to remember the connected tools in [Figure 3]. One account can be reached in several ways, so each method needs protection.

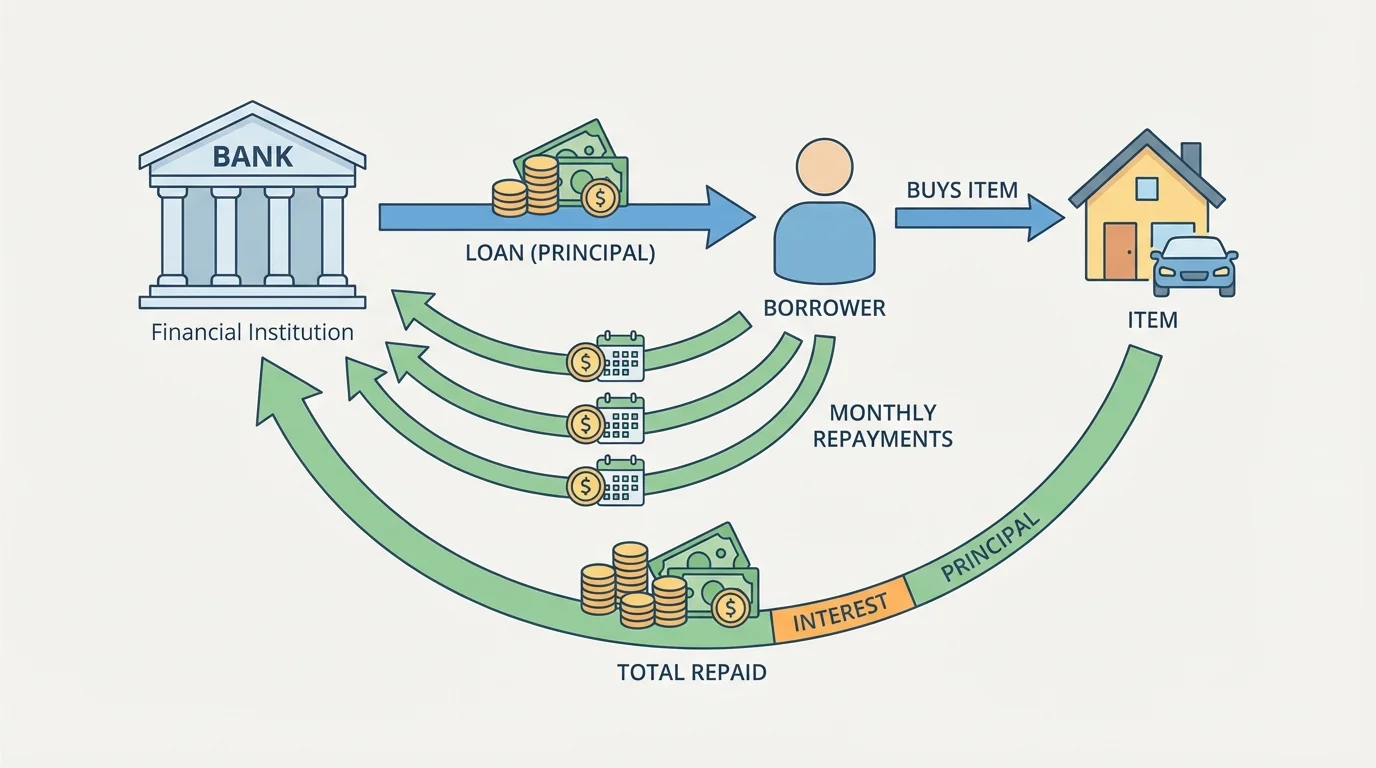

[Figure 4] Another major job of banks is making loans. A loan is money that a bank lets someone borrow and pay back later. Families may borrow to buy a car or a house. Businesses may borrow to buy equipment or open a new store.

When a bank lends money, it expects repayment. The borrower pays back the original amount plus interest. In this case, interest is the cost of borrowing money. So interest can work in two ways: a saver may earn interest, and a borrower may pay interest.

Suppose a family borrows $500 and later repays $530. The extra $30 is interest. The total relationship is \(500 + 30 = 530\). Banks lend money because charging interest on loans is one way they earn income.

Simple loan example

A person borrows $200 from a bank and repays $215 in total. How much interest was paid?

Step 1: Identify the total repaid and the amount borrowed.

Borrowed amount: $200. Total repaid: $215.

Step 2: Subtract to find the interest.

The interest is \(215 - 200 = 15\).

The borrower paid $15 in interest.

Loans can be useful because they allow people to buy important things before they have all the money saved. But loans also create responsibility. Borrowers must make payments on time and understand the total cost.

The system shown in [Figure 4] also connects back to banking's bigger purpose. Banks collect money from depositors, keep records, and use part of that system to lend to borrowers. This is one reason banking affects the whole community.

A bank account is helpful only if people use it safely. That means keeping passwords private, protecting cards, and never sharing a PIN with strangers. People should also be careful with messages that ask for account information. Some messages are scams meant to trick people into giving away personal details.

Adults often teach children an important rule: if something seems suspicious, stop and check with a trusted adult or the bank. Clicking random links or giving account numbers to unknown callers can lead to trouble.

Why safety matters in banking

Banking uses trust. Customers trust banks to protect money, and banks trust customers to use accounts honestly. Safety habits, such as strong passwords and careful checking of account activity, help protect that trust.

Many banks also offer protections such as account monitoring and secure systems. In many places, deposits in banks are insured up to certain limits by government-backed programs. For fifth graders, the key idea is simple: banks work hard to protect money, but customers must also use smart safety habits.

Not all banks are exactly alike. People may compare location, ATM access, fees, customer service, mobile app quality, and account features. Some accounts have minimum balance rules. Some charge fees for certain actions. Others may offer stronger savings options.

A careful customer asks useful questions. Is there a monthly fee? Can I use many ATMs? Does the savings account pay interest? Is the app easy to use? These questions help people choose the financial institution that fits their needs.

| Feature to Compare | Why It Matters |

|---|---|

| Fees | Fees can reduce the money left in an account. |

| ATM access | More ATMs can make it easier to get cash. |

| Interest on savings | Interest can help savings grow. |

| Online tools | Good tools make it easier to track and manage money. |

| Customer service | Helpful service matters when questions or problems come up. |

Table 2. Important features people compare when choosing a bank or credit union.

Using a bank wisely also means good habits: checking balances, saving regularly, reading account information, and avoiding unnecessary fees. Banking does not make decisions for people. It gives them tools. Responsible use is what turns those tools into smart money management.

Banking may sound like something only adults deal with, but students can already understand its role. If a child saves part of a birthday gift for later, that matches the idea of a savings account. If a family uses a card to buy groceries, that connects to a checking account and debit card. If a parent uses an app to pay a bill, that is online banking in action.

Here is one everyday example. A family earns money from jobs and deposits it into a bank. Some of that money stays in checking for rent, food, and electricity. Some goes into savings for emergencies or future goals. If the car breaks down and the family cannot pay the full repair cost immediately, they might use savings or borrow with a loan and repay it over time. Banking helps organize each of these choices.

Here is another example for a student. Marcus receives $40 for his birthday. He wants to spend $15 now on a game and save the rest for a class trip. He can separate the money by purpose. The amount saved is \(40 - 15 = 25\). A savings account would help protect the $25 for later.

"A budget tells your money where to go instead of wondering where it went."

— John C. Maxwell

Banking works best when combined with planning. Saving, spending, and borrowing are easier to manage when people know their goals. That is why banking is such an important part of personal financial literacy. It supports everyday decisions, future plans, and financial safety.