What if you lent someone money today, but when they paid you back a year later, that money bought only half as much food or clothing as before? This problem has challenged people for centuries. Borrowing and investing may sound like modern topics tied to apps, banks, and stock markets, but they have deep roots in history. Over time, people have had to decide whether money was trustworthy, whether banks were safe, and whether investing in a business or company was worth the risk. Those choices shaped families, communities, and even entire nations.

In early American history, these questions were especially important. Colonists and later Americans lived in a growing market economy, where people bought and sold goods, paid taxes, borrowed to expand farms or shops, and sometimes invested in trade or land. But borrowing and investing did not always work the same way. They changed because of laws, war, new financial institutions, and people's confidence in the value of money itself.

Borrowing means receiving money now and agreeing to repay it later, usually with extra money called interest. Investing means using money in hopes of earning more money in the future. Both depend on trust. A lender must trust that the borrower will repay. An investor must trust that the business, land, or stock will gain value. If trust is weak, borrowing and investing become harder.

Financial systems change over time because people respond to risk. If currency keeps its value, people are more willing to lend. If banks are honest and well managed, people are more likely to deposit savings. If businesses can grow and laws protect property, more people are willing to invest. When these conditions break down, fear spreads quickly.

Currency stability means that money keeps a fairly steady value over time, so people can trust what it will buy later. Interest is the extra amount paid for borrowing money. Stocks are shares of ownership in a company. Banks are financial institutions that store deposits, make loans, and help move money through the economy.

These ideas matter because market economies depend on millions of decisions. A farmer deciding whether to borrow for tools, a merchant deciding whether to invest in a ship, and a family deciding whether to save or spend are all making choices shaped by the financial system around them.

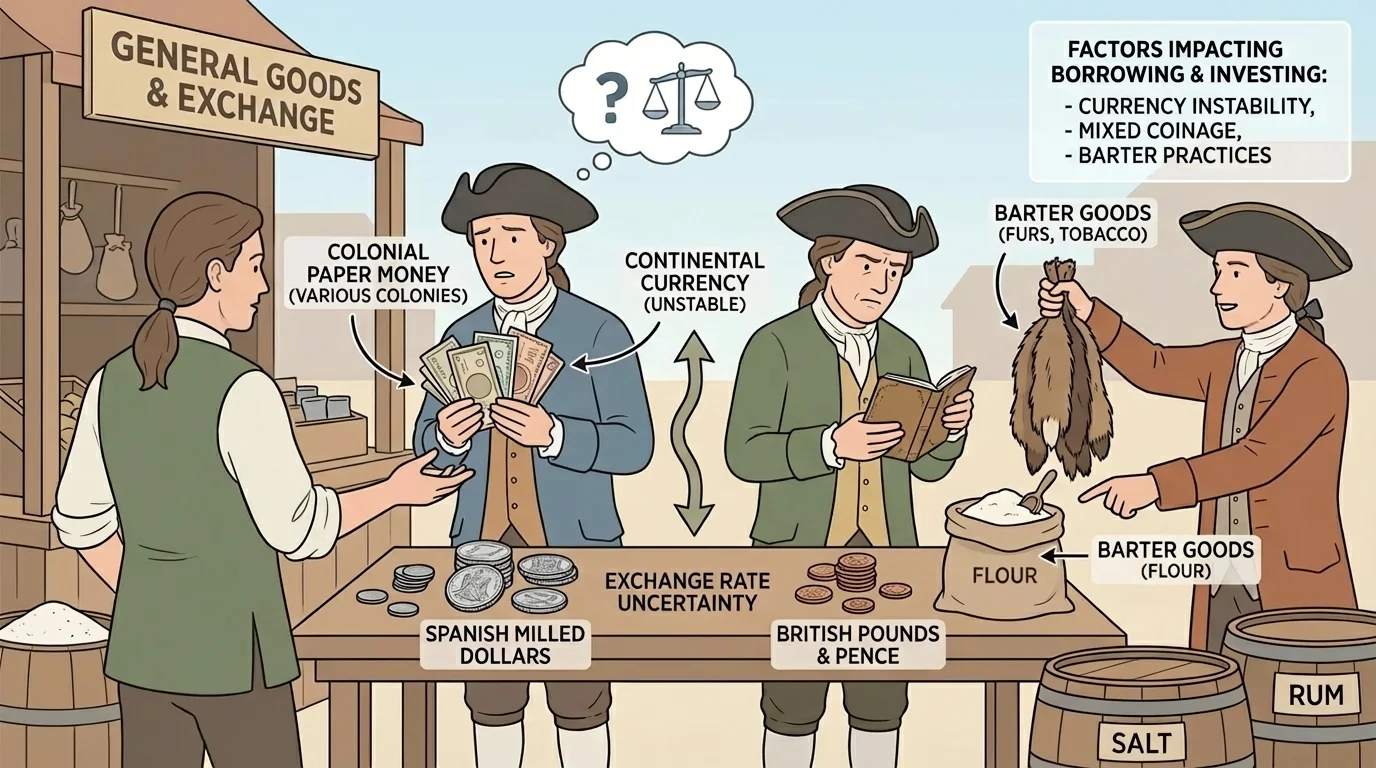

In colonial America, money was often confusing. Different colonies used different kinds of coins and paper notes, and actual gold and silver coins were often scarce. People sometimes relied on barter, exchanging goods directly instead of using money. This mixed system made trade and borrowing difficult, as [Figure 1] illustrates through the use of coins, paper notes, and goods in one marketplace. If no one agreed on what money was worth, it became hard to write fair loan agreements.

Colonial governments sometimes printed paper money to solve shortages, but printing too much could reduce its value. If a lender gave a loan in money that later lost value, the repayment might not be worth as much as expected. That made lenders cautious. Borrowers might like easier access to money at first, but unstable currency could damage the whole system by reducing confidence.

Taxes also affected borrowing and spending. Colonists had to pay certain taxes and debts, and sometimes those payments had to be made in specific forms of money. This pressured households and businesses to get reliable currency. In a market economy, taxes can shape behavior: they can increase demand for certain kinds of money, affect what people buy, and influence how much they borrow.

After independence, the new United States still faced money problems. The country had war debts, weak national finances, and disagreements over banking. Under the Articles of Confederation, the national government had limited power to manage money. The Constitution later gave Congress stronger authority over coinage, helping create a more unified system. That change improved confidence and made long-term borrowing more practical.

The phrase "not worth a Continental" came from the American Revolution, when paper currency called Continentals lost so much value that people used the phrase to mean something almost worthless.

When money loses value quickly, people may rush to spend it before it becomes even less useful. That reaction can make instability worse. A strong economy needs money that people will hold, save, lend, and accept in trade without constant fear.

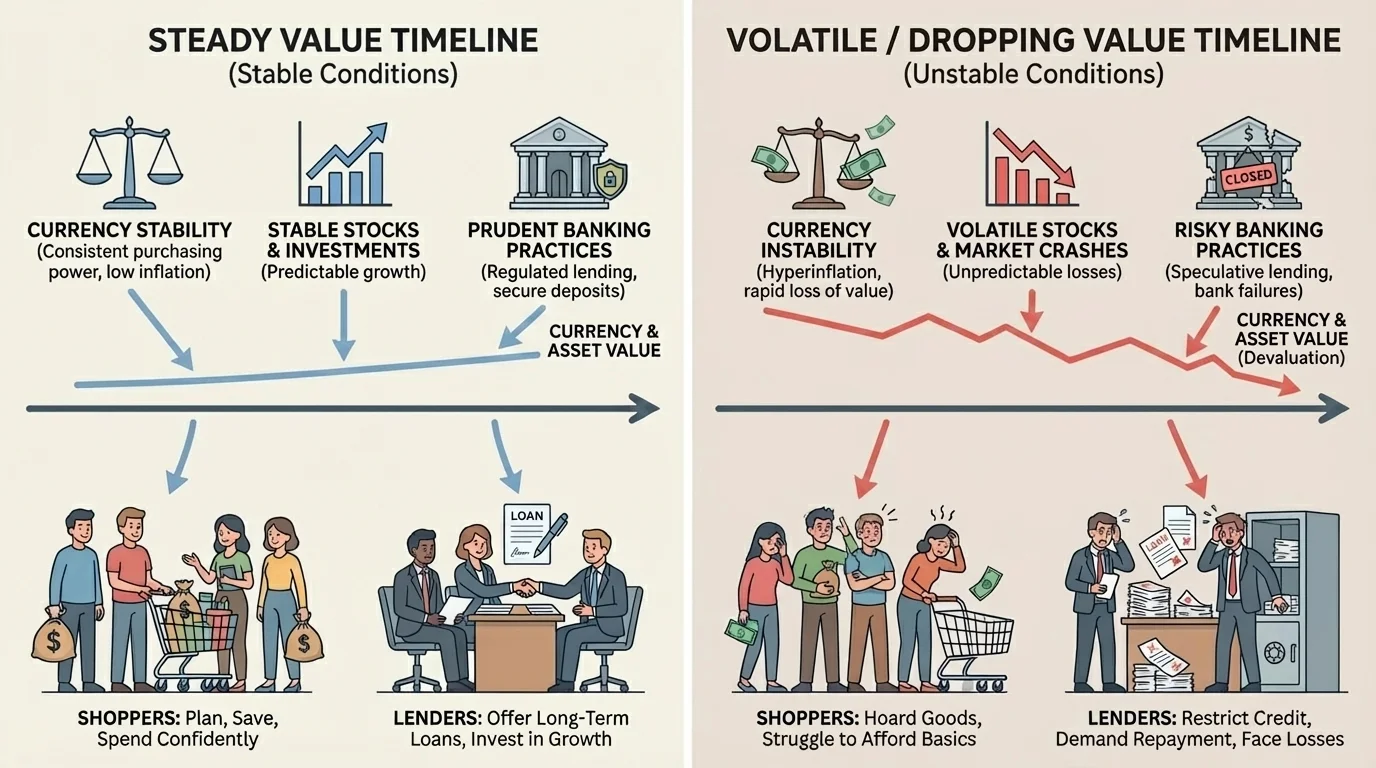

Inflation is a rise in overall prices over time, which means money buys less than before. Moderate inflation can happen in healthy economies, but rapid inflation creates problems. Stable money helps people make long-term plans, as [Figure 2] shows by comparing a steady value path with a sharply falling one. If a person borrows $100 and repays $100 later, the real value of that repayment depends on what $100 can buy at both times.

Suppose $100 can buy 10 bags of flour today, but after heavy inflation it buys only 5 bags a year later. The number is the same, but the value is very different. Lenders notice this risk. They may charge higher interest, shorten loan times, or refuse to lend at all. Borrowers may also struggle because prices for everyday goods rise faster than wages.

Stable currency encourages saving and investing because people feel more certain about the future. If families believe their savings will hold value, they are more likely to keep money in banks. If businesses believe profits will not be wiped out by unstable prices, they are more likely to expand. In this way, currency stability supports growth.

Currency stability also matters for taxes and government finance. If the government collects taxes in stable money, it can plan better. If the currency is unstable, tax revenue may lose value quickly, making it harder to pay debts or fund public needs. In early American history, governments struggled with this problem, especially during wartime.

Why stable money supports borrowing

Borrowing works best when both sides can predict the future reasonably well. A lender wants repayment to keep real value. A borrower wants payments that remain manageable. Stable currency reduces surprises, lowers fear, and makes financial agreements more trustworthy.

This is one reason strong governments often work to protect the value of money. They may regulate banking, control the amount of money in circulation, and build confidence that debts will be repaid in reliable currency.

Early banks played a major role in making borrowing possible. Instead of keeping all money at home, people could place deposits in banks. Banks then used part of those deposits to make loans. This connected savers and borrowers in a powerful way.

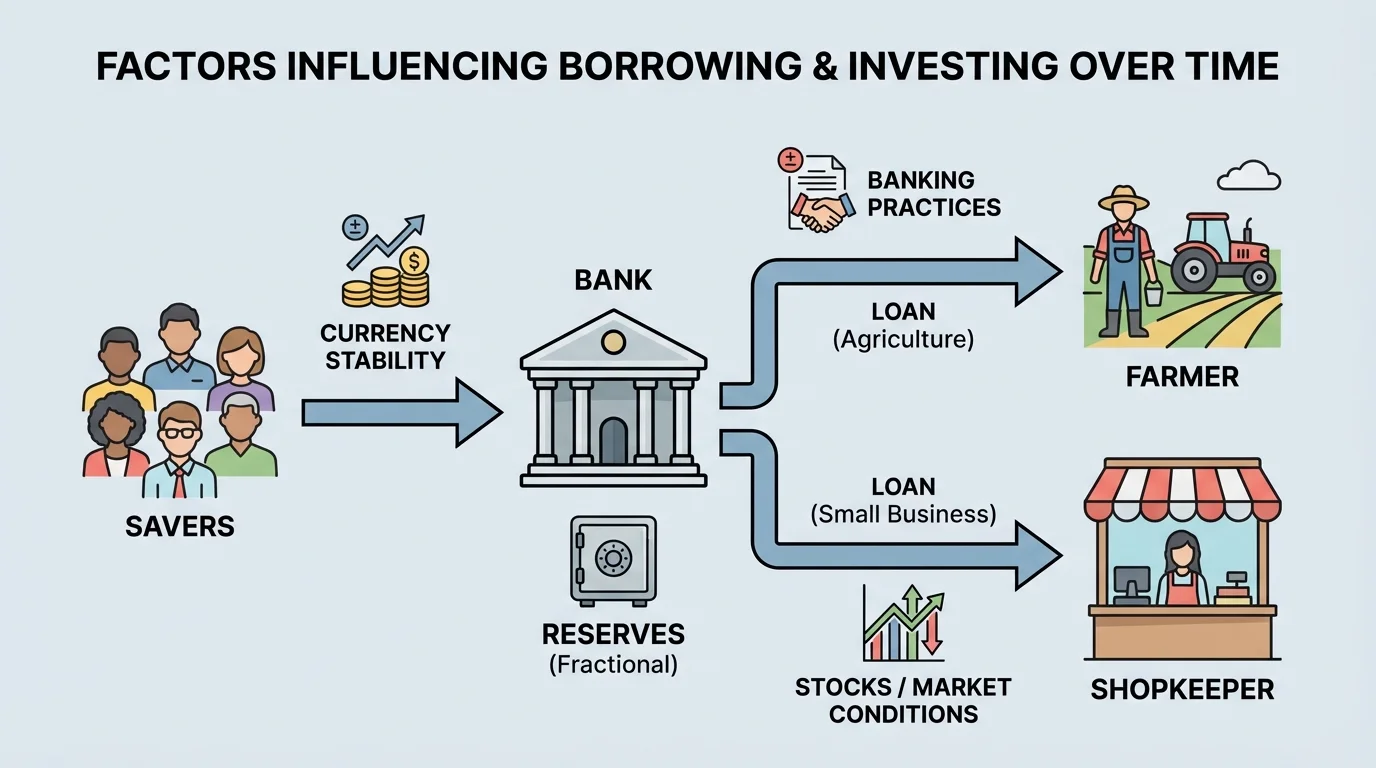

A banknote was a paper promise issued by a bank stating that the holder could exchange it for a certain amount of money, often in gold or silver. Banks helped move money through the economy, and [Figure 3] shows this flow from depositors to loans for farmers and shopkeepers. But early banking was uneven. Some banks were well run, while others made risky loans or lacked enough reserves.

If too many customers demanded their money at once, a bank could fail. This is called a bank run. When one bank failed, fear could spread to others. That happened many times in the 1800s. Such failures made people less willing to trust banks, which reduced borrowing and slowed business growth.

Different banking practices created different levels of safety. Some banks kept stronger reserves and made careful loans. Others issued too many bank notes or lent too freely. Without strong regulation, people had to judge each bank's reliability on their own, which was difficult for ordinary consumers.

Over time, the United States created stronger rules. After the banking crises of the Great Depression, the federal government established the FDIC, which insures many bank deposits. This reduced panic because depositors knew their money was better protected. More trust in banks meant more saving, more lending, and a stronger financial system.

Interest rates also matter in banking. If banks charge high interest, borrowing becomes more expensive. If interest rates are lower, more people may borrow to buy land, start businesses, or expand production. However, rates that are too low for too long can encourage risky behavior. Banking requires balance.

Historical case study: a farmer seeking a loan

A farmer in the early 1800s wants to borrow money to buy better tools and more seed.

Step 1: The farmer goes to a local bank.

If the bank has a strong reputation, people have deposited money there, giving it funds to lend.

Step 2: The bank judges risk.

If crop prices are unstable or many borrowers are already in debt, the bank may worry about repayment.

Step 3: The loan decision affects the economy.

If the bank lends, the farmer may produce more crops and earn more income. If the bank refuses, growth may slow.

This shows how banking practices affect not just one borrower but entire communities.

As seen earlier in [Figure 1], confusing money systems made trade harder. Banks helped solve part of that problem by creating more organized ways to store money, issue notes, and evaluate loans.

A stock represents ownership in a company. If a company grows and earns profits, the value of its stock may rise. Some companies also pay part of their profits to stockholders in payments called dividends. Stocks changed investing because they allowed people to support businesses without running the businesses themselves.

In earlier periods, investing might mean buying land, backing a trading voyage, or joining a local business partnership. As the economy developed, stocks offered a new way to gather large amounts of money for railroads, factories, and other major projects. This helped expand the American economy.

Stocks can bring high returns, but they also carry risk. A company might fail, lose money, or face new competition. Because of this, investing in stocks depends heavily on information and confidence. If investors believe the future looks strong, stock prices often rise. If fear spreads, prices can fall quickly.

Over time, more Americans gained access to stock investing. At first, investing in stocks was mostly for wealthier people and business insiders. Later, stock exchanges grew, financial news spread more widely, and retirement accounts made investing possible for more households. This changed who could build wealth through the market.

Why stocks matter in a market economy

Stocks allow businesses to raise money from many investors at once. This can speed up innovation, transportation, manufacturing, and trade. In return, investors accept the possibility of profit or loss. The stock market therefore links business growth to individual financial decisions.

Even so, the stock market is not the same as guaranteed savings. A bank account is intended to provide safety and easy access to money. A stock investment is designed for possible growth, but with uncertainty. Smart financial systems give people options for both safety and opportunity.

In a market economy, individuals and families make choices about earning, spending, saving, borrowing, and investing. Those choices affect businesses, banks, and governments. In early American history, consumers had to think carefully about what kind of money to trust, when to take on debt, and how to meet tax obligations.

Taxes influence these choices in several ways. If taxes rise, households may have less money to save or invest. If the government taxes imports, prices of imported goods may increase, changing what consumers buy. If taxes help pay national debts and strengthen government credit, investors may feel more confident lending money to the government or to businesses operating under that government.

This connection between taxes and trust was important in early America. Governments needed revenue, but unpopular taxes could create anger and resistance. At the same time, governments that could not raise revenue often struggled to repay debts. A government's financial reputation could affect the entire economy.

Remember that a market economy is a system in which prices, production, and exchange are shaped mainly by choices of buyers and sellers. Governments still matter, especially through laws, taxes, and regulation, but private decisions play a major role.

Consumer decisions also affect interest and credit. If many people borrow heavily and cannot repay, banks may tighten lending rules. If consumers save more, banks may have more funds available for loans. The economy is shaped by these constant choices.

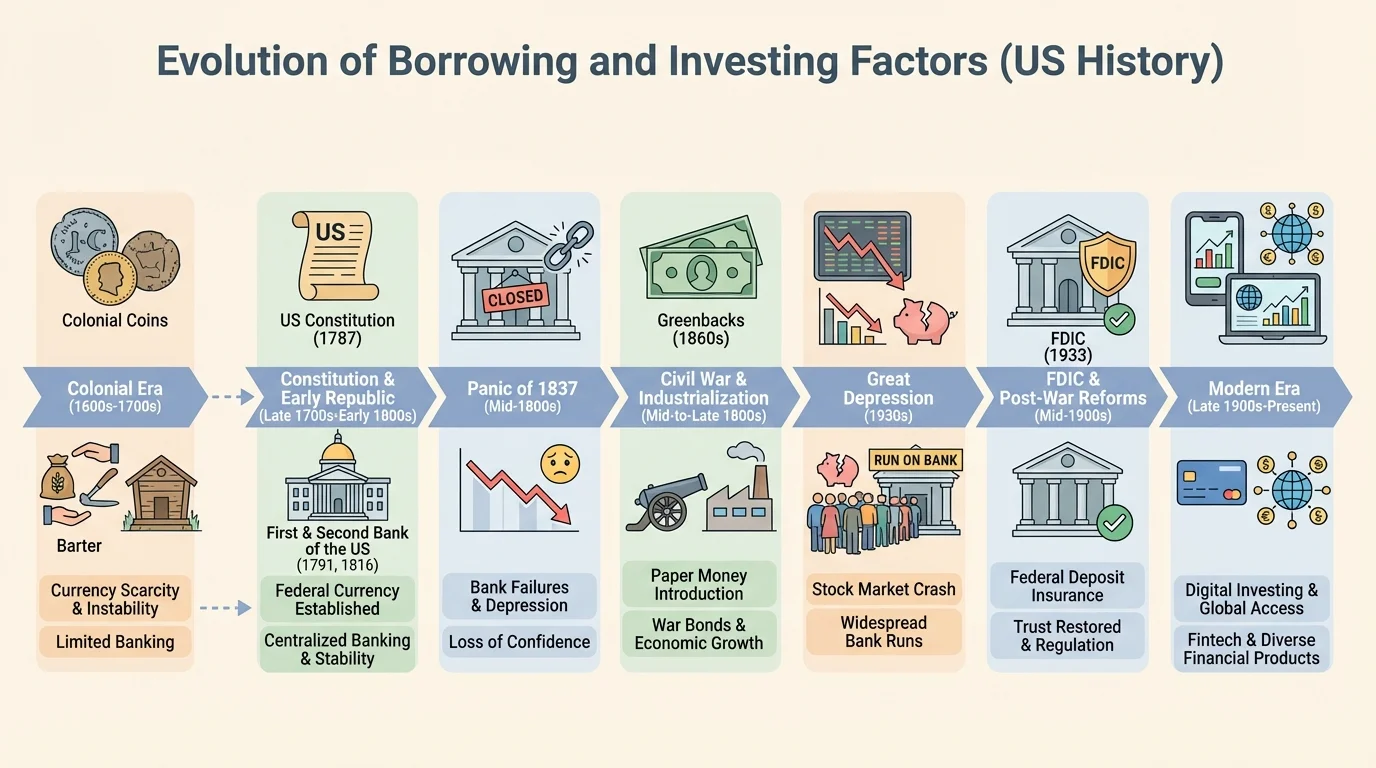

[Figure 4] Several turning points changed how Americans viewed money, banks, and investment over time. This sequence highlights how major events repeatedly changed public trust. Each event affected borrowing and investing not only through laws, but also through confidence.

During the colonial era, money shortages and mixed currencies created uncertainty. After independence, debates over national banking shaped the young republic. The First Bank of the United States, created in 1791, and the Second Bank, created in 1816, were meant in part to improve financial order. Supporters believed national banks would stabilize credit and currency. Opponents feared too much centralized financial power.

The Panic of 1837 brought a severe economic downturn. Bank failures, falling land prices, and weak credit caused hardship across the country. Borrowing became harder, and many people lost faith in financial institutions. Later, during the Civil War, the federal government issued paper money known as greenbacks. This expanded the money supply but also raised questions about value and inflation.

The Great Depression of the 1930s was another huge turning point. Bank failures and stock market collapse destroyed savings and jobs. In response, the government created stronger regulations, including deposit insurance and new rules for financial markets. As a result, many Americans gradually regained trust in banks and investing.

In more recent decades, technology has changed access to finance. People can now move money online, compare interest rates quickly, and buy stocks through digital platforms. Yet the same old issues remain: trust, risk, regulation, and the value of money still shape every decision.

| Period | Financial Challenge | Effect on Borrowing and Investing |

|---|---|---|

| Colonial era | Mixed currencies and coin shortages | Made loans and trade less predictable |

| Early republic | Weak national finance, debate over banks | Limited confidence until stronger institutions formed |

| 1830s–late 1800s panics | Bank failures and unstable credit | Reduced lending and increased fear |

| Civil War era | Paper money expansion and inflation concerns | Changed the value of repayment and savings |

| Great Depression | Mass bank failures and stock collapse | Led to new regulations and deposit insurance |

| Modern era | Fast access to credit and markets | Expanded opportunity but also new risks |

Table 1. Major periods showing how financial conditions affected borrowing and investing in the United States.

As seen in [Figure 3], banks connect savers to borrowers. When that connection is disrupted by panic or poor regulation, the effects spread far beyond one building or one town.

Consider a merchant in a port city in the late 1700s. He wants to borrow money to buy imported goods. If currency values are uncertain and banks are weak, the lender may demand very high interest or refuse the loan. That means fewer goods in the store and less trade in the town. A financial problem becomes a community problem.

Now consider an investor in the 1800s deciding whether to buy shares in a railroad company. Railroads could create great wealth by connecting regions and speeding trade. But they were expensive to build and could fail. The investor had to judge whether the opportunity was worth the risk. This is similar to how modern investors evaluate new companies today.

Comparing two choices

A family has extra money and must decide what to do with it in two different historical settings.

Step 1: In an unstable money system

The family may avoid long-term saving because the money might lose value. They may buy goods quickly or hold something more trusted, such as land or precious metal.

Step 2: In a stable banking system

The family may deposit money in a bank, expecting it to remain safer and keep its value better.

Step 3: In a growing stock market

If the family can accept more risk, they might invest in stocks to seek greater long-term growth.

Different financial systems lead people to make very different decisions.

Even today, people face versions of these same choices. Should you save in a bank, pay off debt, or invest for the future? History shows that these decisions are never made in a vacuum. They depend on larger conditions such as stable money, trusted banks, and fair rules.

One of the biggest lessons from history is that financial systems are built on confidence. People borrow when they believe repayment is possible and fair. People invest when they believe future rewards are worth the risk. People save when they believe money will remain useful and protected.

Currency stability, banking practices, and stocks each changed borrowing and investing over time, but they are connected. Stable currency makes planning easier. Reliable banks help move money safely from savers to borrowers. Stocks allow businesses to grow by attracting investors. Taxes and government policies influence all of these by shaping trust, rules, and incentives.

That is why financial history matters. It is not only about the past. It helps explain why people still care about inflation, bank safety, interest rates, and investment risk today. The tools may look more modern, but the core questions remain the same: Can this money be trusted? Is this loan fair? Is this investment worth the risk?