Why does a city spend money on buses instead of more parks? Why might a family choose to repair an old car rather than buy a new one? Why would a business stop producing a product that still sells? These are not random choices. They are examples of economic thinking: a way of analyzing decisions when wants are unlimited but resources are limited. Economics is not only about money. It is about choices, tradeoffs, and the logic behind how people use scarce resources.

Scarcity means that people do not have enough resources to satisfy every want at the same time. Because land, labor, and capital are limited, every person and every institution must decide what to use them for first. A student has limited hours in a day. A household has limited income. A business has limited workers, machines, and factory space. A government has limited tax revenue and a limited number of public employees. Scarcity is the starting point of economic thinking because if everything were unlimited, choices would not be necessary.

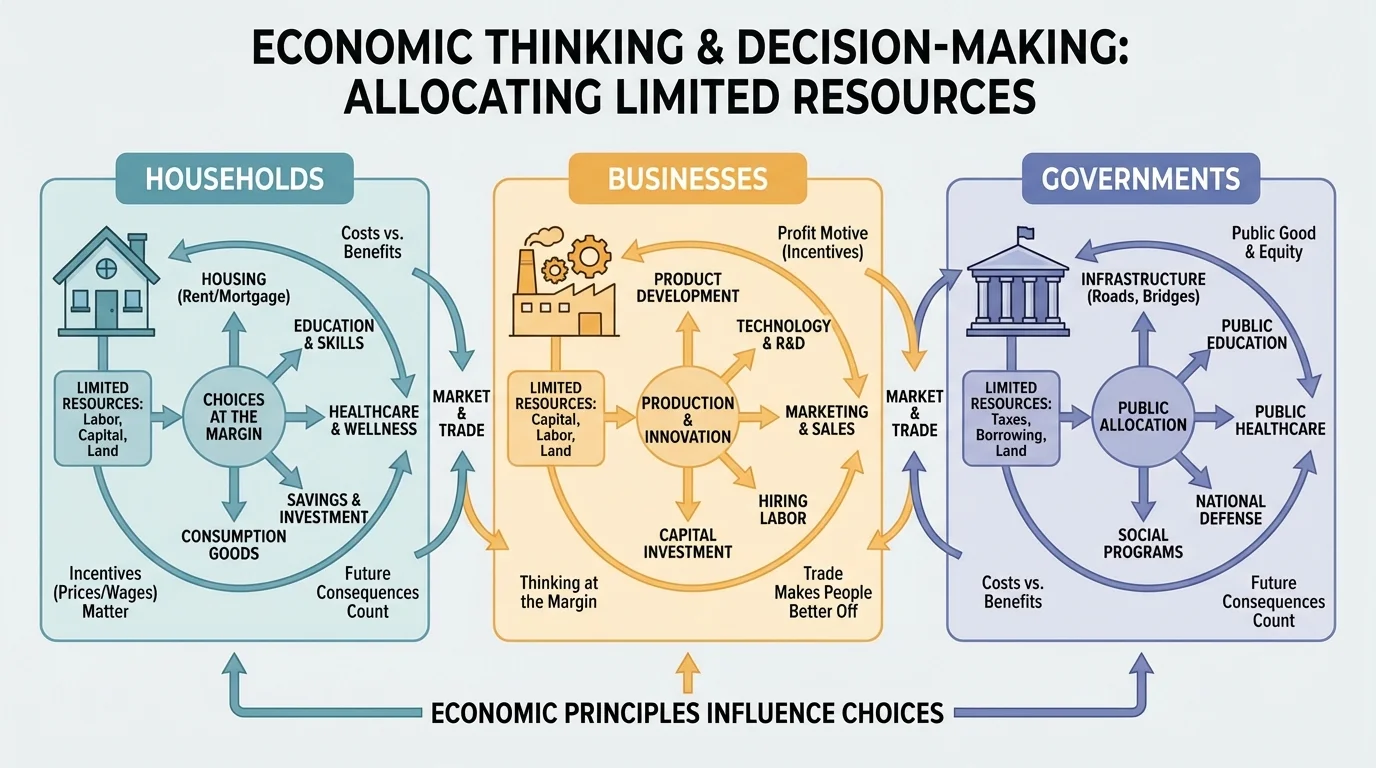

[Figure 1] Economists often group productive resources into three major categories: land, labor, and capital. Land includes natural resources such as farmland, forests, minerals, and water. Labor means human effort, skills, and time. Capital means tools, machines, buildings, and technology used to produce goods and services. When these resources are scarce, using them for one purpose means they cannot be used for another purpose at the same time.

This is why economics focuses so much on allocation. Allocation means deciding where resources go. If a town uses land to build a sports stadium, that land cannot also be used for apartments or a public library. If a business assigns workers to produce sneakers, those same workers cannot produce backpacks during the same hours. If a family spends part of its income on streaming subscriptions, that money cannot also be used for groceries or savings.

Productive resources are the inputs used to create goods and services. Land refers to natural resources, labor refers to human work and skill, and capital refers to tools and equipment used in production.

Scarcity does not mean there is too little of everything everywhere. It means there is not enough to satisfy all wants fully. Even wealthy households face scarcity because time, attention, and physical resources remain limited. Governments in rich countries still make budget decisions. Large businesses still decide which projects deserve investment. Scarcity is universal.

One of the most basic principles of economic thinking is to use cost-benefit analysis. A rational decision-maker asks: What do I gain from this choice, and what do I give up? A benefit is anything that increases well-being, satisfaction, or profit. A cost is anything sacrificed, including time, money, effort, or lost alternatives.

Suppose a student is deciding whether to take a part-time job during the school year. The benefits may include income, work experience, and new skills. The costs may include less study time, less sleep, and less time for sports or clubs. The best choice depends on how those costs and benefits compare for that student. Economics does not say everyone should make the same choice. It gives a method for evaluating the choice.

An especially important idea is opportunity cost, which is the value of the next best alternative that is given up. If a household spends $1,200 on a vacation, the opportunity cost might be paying off part of a credit card balance, replacing an old appliance, or adding to savings. Opportunity cost matters because the real cost of a choice is not only what is spent directly. It also includes what could have been done instead.

For businesses, cost-benefit analysis shapes investment decisions. A company considering a new delivery truck compares the expected extra revenue and efficiency from faster deliveries with the truck's price, maintenance costs, fuel costs, and insurance. If the benefits exceed the costs, the purchase may make sense. If not, the company may wait or choose another investment.

Case study: A city chooses between two projects

A city has enough money to fund only one major project this year: a new sports complex or repairing aging water pipes.

Step 1: Identify likely benefits.

The sports complex may create recreation opportunities and attract local spending. Repairing water pipes may reduce leaks, improve safety, and lower future repair costs.

Step 2: Identify likely costs.

The sports complex uses money, land, and future maintenance funds. Pipe repairs may cause temporary road closures and use funds that cannot be spent elsewhere.

Step 3: Compare the next best alternative.

If the city chooses the sports complex, the opportunity cost is the safer and more reliable water system it gave up. If it chooses the pipe repairs, the opportunity cost is the recreation project it delayed.

Economic thinking pushes decision-makers to consider both visible and less visible costs before choosing.

Sometimes costs and benefits are hard to measure exactly. How much is cleaner air worth? How should a household value time together? How much should a government value national security? Economics still helps by asking decision-makers to identify tradeoffs clearly, even when not every effect can be turned into a number.

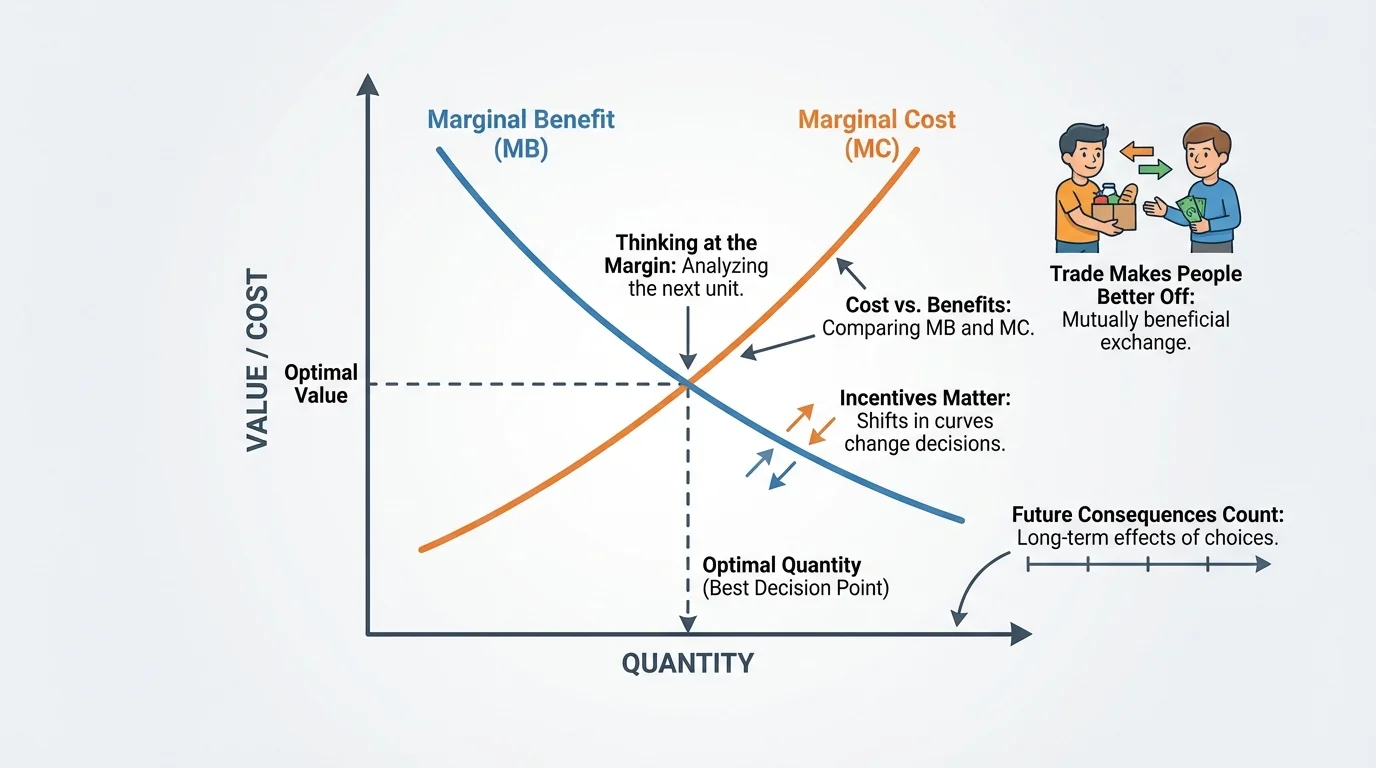

Many decisions are not all-or-nothing. They are decisions about whether to do a little more or a little less. This is called thinking at the margin. A student may not ask, "Should I study or not study?" but instead, "Should I study one more hour tonight?" A business may not ask, "Should we produce shoes or stop?" but instead, "Should we produce 100 more pairs this week?" The smart choice is often found by comparing the added benefit of one more unit with the added cost of one more unit.

[Figure 2] The marginal benefit of a choice is the extra gain from one additional unit, while the marginal cost is the extra cost of that additional unit. In general, a decision-maker should continue an activity as long as marginal benefit is at least as large as marginal cost. When marginal cost becomes greater than marginal benefit, continuing no longer makes sense.

Consider a bakery deciding how many loaves of bread to bake each morning. The first loaves sell quickly and generate strong revenue, so their marginal benefit is high. But as more loaves are baked, demand may weaken and some bread may go unsold. At the same time, overtime wages, energy use, and ingredient costs may rise, increasing marginal cost. The bakery should expand production until the additional revenue from one more loaf no longer exceeds the additional cost.

Households use marginal thinking too. A family deciding whether to buy one more streaming service compares the extra enjoyment from that service with the extra monthly cost. Governments also think at the margin. A state may ask whether hiring 100 more highway workers will reduce road damage enough to justify the additional payroll expense.

Marginal thinking helps prevent poor decisions based on sunk costs. A sunk cost is a cost that has already been paid and cannot be recovered. For example, if a business spent money developing a product that customers no longer want, that past spending should not by itself justify producing more of the product. The decision should depend on future marginal costs and future marginal benefits, not on money already gone.

Professional sports teams use marginal thinking constantly. Coaches and managers ask whether one more minute for a star player raises the chance of winning enough to outweigh fatigue, injury risk, or weaker performance later in the season.

Later, when we consider government borrowing and environmental policy, the same logic from [Figure 2] still applies: the next unit of action should be judged by its extra benefit and extra cost, not by emotion alone or by what has already been spent.

Incentives are factors that encourage or discourage certain actions. They can be positive, like rewards, or negative, like penalties. Economic thinking assumes that people respond to incentives, although not always perfectly. This matters because changing incentives often changes behavior.

At the individual level, wages provide an incentive to work. Grades can provide an incentive to study. Discounts can encourage shoppers to buy more. At the household level, high electricity prices may encourage families to use less energy or buy efficient appliances. At the business level, expected profit encourages firms to innovate, expand production, or enter new markets.

Governments use incentives through taxes, subsidies, and laws. A tax on cigarettes raises the cost of smoking and may reduce consumption. A subsidy for solar panels lowers the cost of clean energy and may encourage adoption. A speed-limit fine creates a penalty that discourages dangerous driving. Good policy often depends on understanding how people will respond to these incentives in real life, not just how leaders hope they will respond.

However, incentives can produce unintended consequences. If a school rewards attendance but ignores learning, students may show up without engaging seriously. If a company pays workers only by the number of items produced, quality may fall. If a government caps rent too strictly without encouraging new housing construction, landlords may reduce maintenance or builders may construct fewer apartments. Economic thinking looks beyond the rule itself and asks how people are likely to react.

Why incentives work

Incentives matter because they change the relative costs and benefits of actions. When a reward rises, the benefit of an action becomes larger. When a penalty rises, the cost becomes larger. People still make their own choices, but the structure of the decision changes.

This is why economists often warn that policy should be tested not only by its goals but also by its incentives. A policy that sounds fair or generous can fail if it encourages less work, less saving, waste, or other behaviors that reduce the intended benefits.

One of the most powerful and sometimes misunderstood principles in economics is that trade can make people better off. When exchange is voluntary, both sides agree because each expects to gain. People often benefit when they specialize in what they do relatively well and then trade for other goods and services.

[Figure 3] This principle applies in many contexts. A student may mow lawns for neighbors and use the money to buy meals, music, or clothes rather than trying to produce all these things personally. A household may trade labor income for food, internet access, transportation, and healthcare. Businesses trade with suppliers and customers every day. Governments engage in trade agreements with other nations because no country can efficiently produce everything at the lowest possible cost.

Specialization means focusing on a narrower set of tasks. Specialization can increase productivity because workers and firms become more skilled, save time, and use equipment more efficiently. A hospital functions better when surgeons, nurses, pharmacists, and lab technicians each specialize in different tasks rather than every worker trying to do every job.

A related idea is comparative advantage. A person, business, or country has a comparative advantage when it can produce a good or service at a lower opportunity cost than another producer. Even if one producer is better at making everything, trade can still help if each side specializes according to comparative advantage. The key is not absolute ability alone, but what must be given up to produce one more unit.

Case study: Two students and comparative advantage

Jordan can write an essay in 2 hours or solve a set of calculus problems in 1 hour. Mia can write an essay in 3 hours or solve the same problem set in 2 hours.

Step 1: Compare opportunity costs for writing.

For Jordan, 1 essay costs 2 problem sets because 2 hours could have been used to complete 2 one-hour sets. For Mia, 1 essay costs \(\dfrac{3}{2}\) problem sets because 3 hours could have been used to complete 1.5 two-hour sets.

Step 2: Compare opportunity costs for calculus.

For Jordan, 1 problem set costs \(\dfrac{1}{2}\) of an essay. For Mia, 1 problem set costs \(\dfrac{2}{3}\) of an essay.

Step 3: Identify comparative advantage.

Mia has the lower opportunity cost in writing because \(\dfrac{3}{2} < 2\). Jordan has the lower opportunity cost in calculus because \(\dfrac{1}{2} < \dfrac{2}{3}\).

If they divide work based on comparative advantage and then share results fairly, both can save time.

Trade does not guarantee that every person benefits equally or immediately. Workers in some industries may face job losses when markets change. Regions may be affected differently. That is one reason trade policy is debated. Still, the core economic principle remains: voluntary exchange and specialization usually expand total output and create gains that did not exist before. As with other principles, economic thinking then asks how those gains are distributed and what policies can reduce harm to affected groups.

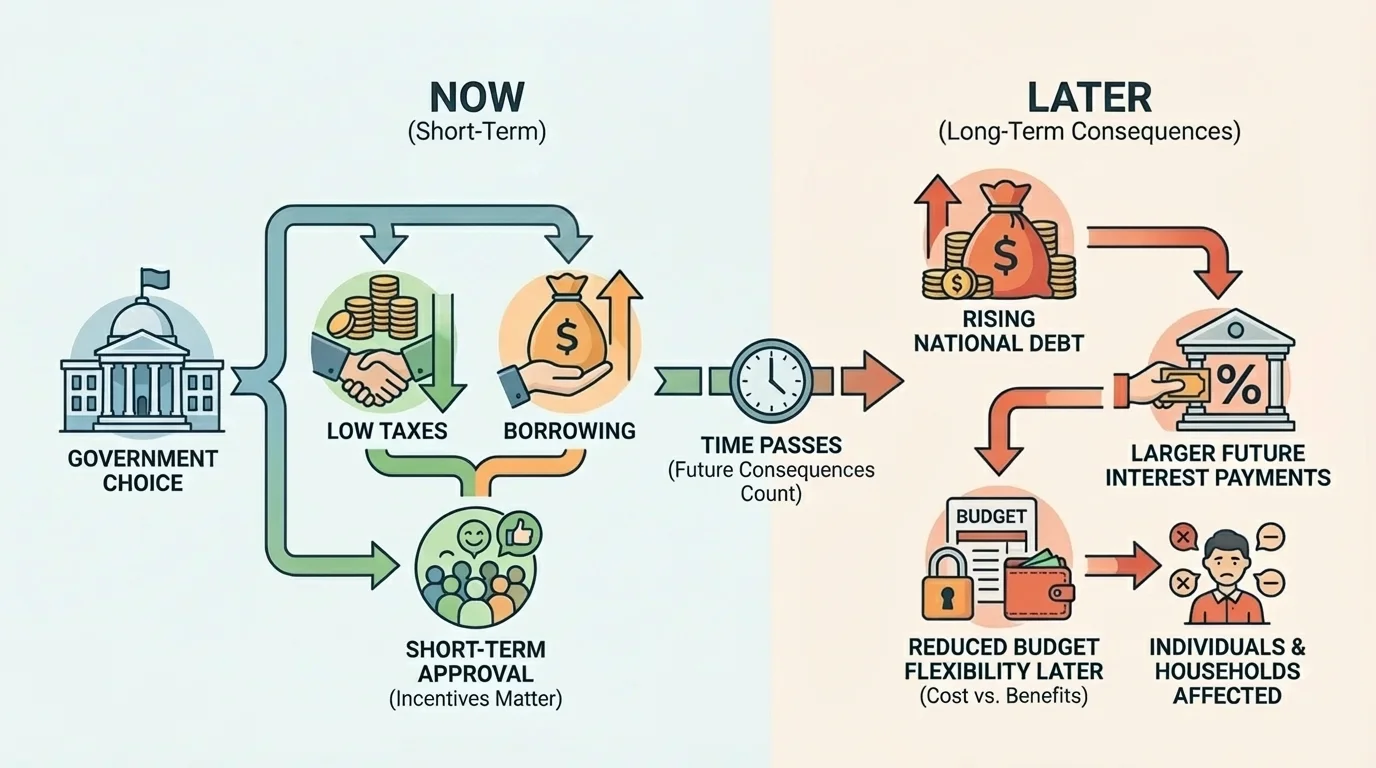

Good economic thinking looks beyond the immediate moment. Choices create ripple effects over time. A decision that feels beneficial now may produce larger costs later. That is why economists pay close attention to long-term consequences, not just short-term results.

[Figure 4] For individuals, this principle appears in saving, borrowing, and education. Spending all income today may feel satisfying, but it reduces future savings and emergency security. Taking on debt may help someone buy a car or attend college, but future loan payments reduce later income available for other uses. Investing time in education may feel costly now, yet it can raise future earnings and opportunities.

Households face the same issue when they choose between present consumption and future stability. A family that delays car maintenance to save money this month may face a much larger repair bill later. A household that regularly saves even small amounts gains flexibility for emergencies, large purchases, or retirement. Economic thinking asks not only, "What happens now?" but also, "What happens next year, or five years from now?"

Businesses must think ahead too. Cutting worker training may raise short-term profit, but it can reduce productivity and quality over time. Ignoring equipment maintenance may save money now while increasing breakdowns later. Releasing a low-quality product quickly may boost short-term sales but damage the company's reputation and future market share.

For governments, future consequences are especially important because public decisions affect millions of people. A government that borrows heavily to fund current spending may face larger interest payments later, leaving less money for schools, roads, or healthcare. Environmental policy is another example. Allowing pollution can lower costs for firms in the short run, but over time it may damage health, reduce agricultural productivity, and require expensive cleanup. The future costs are real even when they are delayed.

This principle also warns against focusing only on visible effects. Suppose a city freezes water prices artificially low. Residents may enjoy lower bills immediately, but the long-term result may be underinvestment in pipes, water shortages, or costly emergency repairs. Economic thinking tries to uncover both the seen and the unseen effects of choices.

"There are no solutions. There are only trade-offs."

— Thomas Sowell

The government borrowing pattern shown in [Figure 4] also applies to personal finance and business management: actions that postpone costs do not erase them. They often move those costs into the future, where they may become larger.

The same economic principles apply across different decision-makers, but the goals and constraints are not always identical. Individuals often focus on personal satisfaction, education, career, and time. Households usually consider shared budgets, housing, childcare, transportation, and savings. Businesses often aim for profit, growth, and survival in competition. Governments consider public services, fairness, stability, and long-term national goals.

Even so, all of them face scarcity, compare costs and benefits, respond to incentives, think at the margin, engage in trade, and face future consequences. The details differ, but the logic is connected.

| Decision-maker | Common scarce resources | Typical choices | Economic principles involved |

|---|---|---|---|

| Individual | Time, income, skills | Study or work, spend or save, buy now or later | Opportunity cost, marginal thinking, incentives |

| Household | Budget, time, housing space | Rent or buy, repair or replace, save or consume | Cost-benefit analysis, future consequences |

| Business | Workers, machines, funds, materials | Hire or automate, expand or pause, price changes | Marginal cost, incentives, trade, specialization |

| Government | Tax revenue, land, labor, public capital | Fund schools or roads, tax or subsidize, regulate or not | Scarcity, incentives, opportunity cost, long-run effects |

Table 1. How core economic principles appear in choices made by different decision-makers.

Consider one issue: transportation. An individual may decide whether owning a car is worth the cost. A household may choose between one vehicle or two. A business may decide whether delivery vans improve efficiency enough to justify expense. A government may decide whether to invest in roads, buses, or rail systems. Different decision-makers, same logic: limited resources, tradeoffs, and choices shaped by expected costs and benefits.

Applied comparison: one principle, four decision-makers

Suppose gasoline prices rise sharply.

Step 1: Individual response.

A student may reduce driving, carpool, or look for a closer job because the cost of each trip rises.

Step 2: Household response.

A family may combine errands, shift part of the budget away from entertainment, or switch to a more fuel-efficient vehicle.

Step 3: Business response.

A delivery company may raise prices, redesign routes, or invest in efficient vehicles.

Step 4: Government response.

Leaders may release fuel reserves, subsidize transit, or reconsider transportation policy.

Each group responds because incentives changed: driving became more expensive.

The specialization and exchange pattern from [Figure 3] also connects here. Transportation itself is part of how trade happens. When transport becomes cheaper and more reliable, businesses can specialize more and households gain access to more goods and services.

Economic reasoning is powerful, but real life is messy. People do not always have perfect information. Emotions, habits, culture, fairness concerns, and political pressures matter. A household may make a choice that is not financially optimal because family traditions matter deeply. A government may support a struggling region even if the policy is not the most efficient in a narrow economic sense. A business may keep extra workers during a downturn to preserve morale and loyalty.

Also, some costs and benefits fall on people who were not part of the original decision. For example, pollution from a factory may harm nearby residents. Economists call these spillover effects externalities. In such cases, private decision-makers may ignore costs imposed on others, and government policy may be used to correct the incentive problem.

Fairness and efficiency can also point in different directions. A policy may increase total economic output but distribute gains unevenly. Another policy may reduce inequality but also reduce incentives to invest or work. Economic thinking does not eliminate these debates. Instead, it helps clarify what is being gained, what is being sacrificed, and who is affected.

Whenever you study economics, return to a few basic questions: What is scarce? What are the alternatives? What is the opportunity cost? How will incentives change behavior? What happens at the margin? Who gains from trade? What are the future consequences?

That is why economic thinking matters so much in everyday life. It gives students, families, business leaders, and public officials a disciplined way to analyze choices. It does not promise easy answers. It does something more useful: it helps people ask better questions before they decide.