Why can two countries have smart workers, natural resources, and advanced technology, yet still produce very different standards of living? One major reason is the way each society organizes its economy. Every nation has to answer the same basic questions: What should be produced? How should it be produced? Who should receive it? The answers depend on its economic system, and those answers shape everything from food prices and job opportunities to health care and business innovation.

At the center of economics is the problem of scarcity. Resources such as land, labor, capital, and entrepreneurship are limited, but human wants are not. Because of scarcity, every society must make choices. An economic system is the method a society uses to decide how to use scarce resources, organize production, and distribute goods and services.

No economic system is perfect. Each one tries to solve economic problems, but each also creates new challenges. Some systems provide more freedom but less equality. Others create more security but less innovation. The central question is not simply which system is "best," but which system does the best job of meeting a society's most important goals while limiting harm.

Economic systems also affect everyday life in ways students can recognize. The price of a smartphone, the availability of jobs, whether medicine is affordable, whether public schools are funded, and whether a company can dominate a market all reflect decisions made within an economic system. That is why comparing systems is really about comparing different ideas of fairness, efficiency, and power.

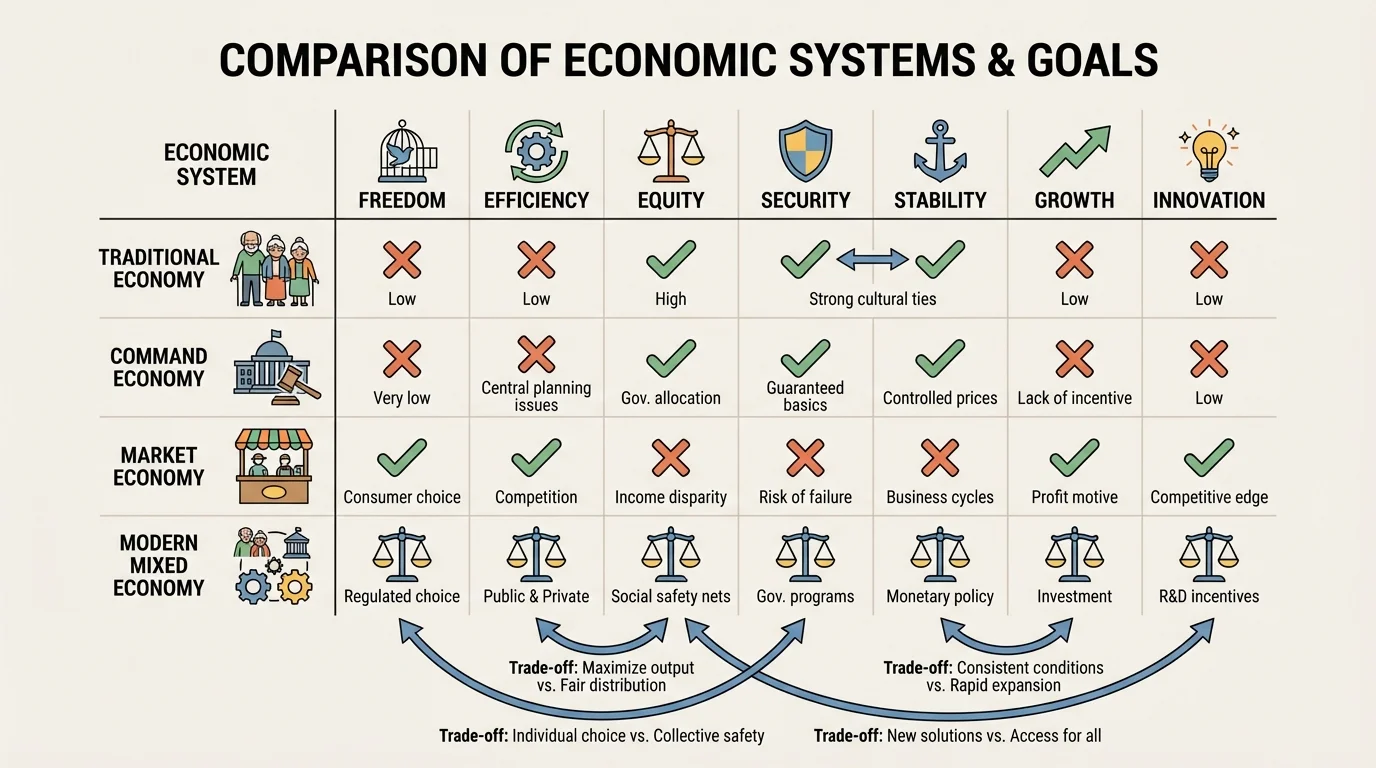

To evaluate any system, it helps to know the main goals societies often pursue. These goals do not always fit together neatly, as [Figure 1] illustrates. A country may increase economic freedom, for example, but then face greater inequality. Another may improve security through government guarantees but reduce business flexibility.

Economic efficiency means using resources in a way that avoids waste and gets the greatest possible output from what is available. Economic freedom means people and businesses can make many of their own choices. Economic equity refers to fairness in the distribution of income, wealth, and opportunity. Economic security means people are protected against severe hardship caused by unemployment, illness, disability, or old age.

Economic growth is the increase in a nation's output of goods and services over time. Economic stability means avoiding extreme inflation, unemployment, or sudden recessions. Innovation involves developing new products, ideas, and methods. Many societies today also consider sustainability, or using resources in ways that do not damage the future.

These goals often conflict. A government that raises taxes to fund more social services may improve security and equity, but some critics argue that higher taxes can reduce investment incentives. A society that removes many business regulations may increase freedom and competition in some areas, but it may also allow unsafe products, pollution, or worker exploitation. Evaluating an economic system means weighing these trade-offs carefully.

Scarcity means limited resources compared with unlimited wants. Opportunity cost is the value of the next best alternative given up when a choice is made. Incentives are rewards or penalties that encourage people to act in certain ways. These ideas help explain why different systems produce different outcomes.

Because people respond to incentives, the rules of an economy matter. If producers earn profits by serving customers well, they may innovate quickly. If officials are rewarded for meeting production quotas, they may focus on quantity instead of quality. The structure of the system shapes behavior.

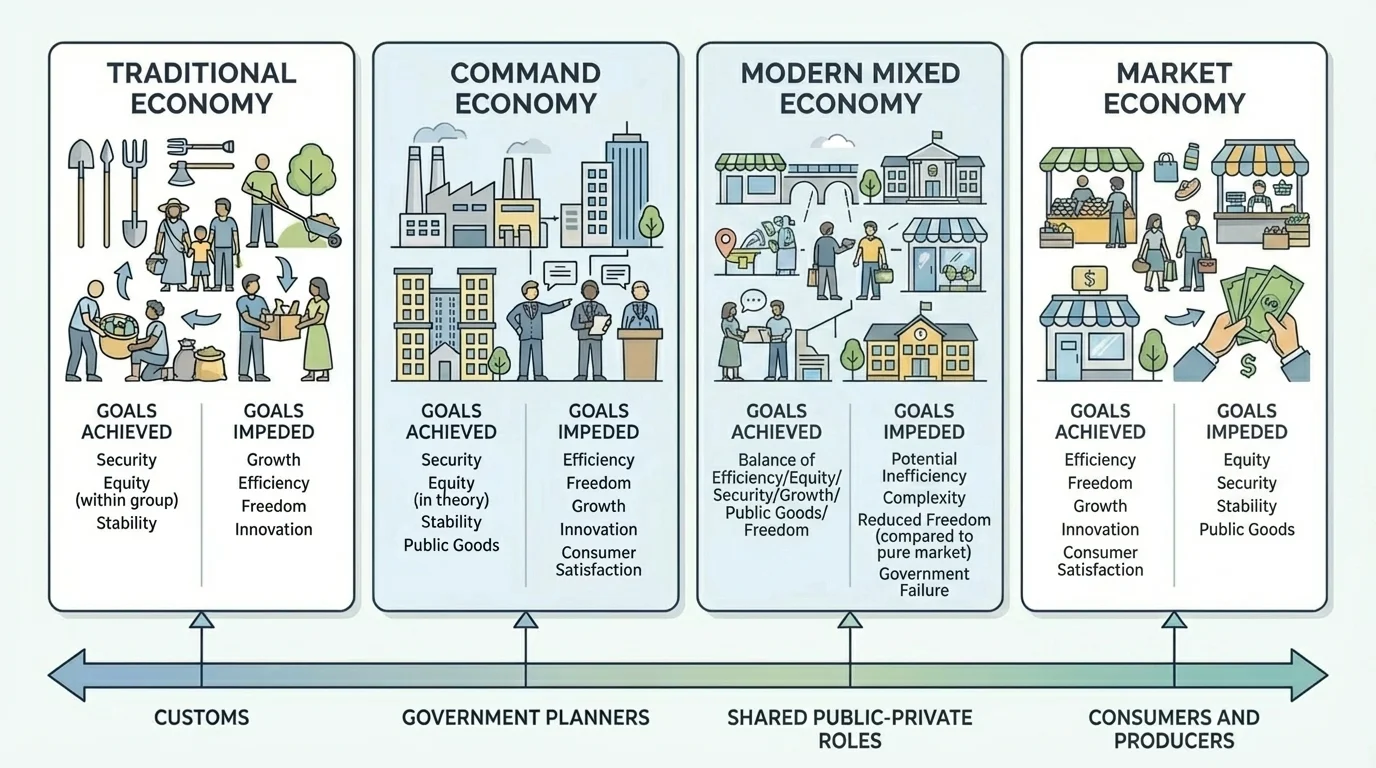

A traditional economy relies on customs, habits, family roles, and long-established patterns of behavior. Economic decisions are often based on what has been done for generations. People may farm, fish, herd animals, or make goods using techniques passed down over time. In these systems, the answers to economic questions come mainly from tradition rather than markets or government planners.

Traditional economies can be found in small rural villages, Indigenous communities, and places where modern industrial development is limited. In such economies, work is often closely tied to family or community roles. A child may learn a trade from parents or elders, and production may focus on meeting local needs rather than earning profit in a large national market.

One strength of a traditional economy is stability. People often know their roles, community bonds may be strong, and resources may be used in ways adapted to the local environment. In some places, traditional practices also support sustainability because communities avoid overusing land, water, or forests.

However, traditional economies may impede growth and innovation. New technology can spread slowly, output may remain low, and living standards may be limited. People may also have fewer choices about occupation or lifestyle. If a drought, disease, or natural disaster harms the local economy, the community may have few backup systems. Traditional economies can provide social belonging, but they may struggle to achieve high efficiency, rapid growth, or broad economic freedom.

A command economy is one in which a central authority, usually the government, makes major economic decisions. The government may decide what goods to produce, how much to produce, what prices to charge, and how workers and resources are assigned. Major industries are often state-owned.

Command systems are designed to coordinate economic activity according to a national plan. Supporters argue that this can be useful when a country needs to mobilize resources quickly, rebuild after war, or guarantee basic services to all citizens. If the state controls transportation, energy, housing, and factories, it can direct output toward national goals.

In theory, command economies can promote equity and security. The government can set low prices for essentials, provide jobs directly, and reduce extreme income gaps. It can also invest heavily in strategic areas such as defense, heavy industry, or infrastructure.

But command economies often struggle with efficiency. When planners, rather than millions of consumers and producers, make decisions, they may not have enough information to match supply with demand. Shortages and surpluses are common. A factory told to meet a numerical target may produce a large quantity of goods that people do not actually want. Without strong competition or profit incentives, quality and innovation may suffer.

Political power is another issue. If the same government controls both the economy and political life, individual freedom can be limited. Historical examples from the Soviet Union and Mao-era China show that command systems can industrialize rapidly in some periods, yet they can also produce chronic shortages, low consumer choice, and repression. North Korea remains a modern example of an economy with strong command elements, and its people face severe limits on both economic freedom and access to consumer goods.

A market economy is an economic system in which decisions are made mainly by individuals and private businesses acting through voluntary exchange. Consumers signal what they want by spending money. Producers respond by deciding what to make, how much to make, and what prices to charge. Private property and profit play major roles.

In a market system, prices act like signals. If demand for electric cars rises, prices and profits may increase, encouraging firms to produce more. If demand for a product falls, firms may cut output or leave the market. This process helps coordinate millions of choices without a central planner. As [Figure 2] shows, market economies place more decision-making power in the hands of consumers and producers than traditional or command systems do.

Market economies often do a strong job promoting innovation, efficiency, and freedom. Businesses have an incentive to lower costs, improve quality, and invent new products because success can lead to higher profits. Consumers have more choice, and workers can often choose among more jobs or even start their own businesses.

Still, market economies do not automatically create fairness or security. Income can become very unequal. Some people may not be able to afford housing, health care, or education even if these goods exist. A pure market may also underprovide public goods such as national defense, street lighting, and some environmental protections because firms cannot easily charge every user.

Market failure can also occur when private decisions produce harmful side effects. Pollution is a classic example. A factory may lower its costs by dumping waste into a river, but nearby communities pay the price through health damage and environmental cleanup. In that case, the market price does not reflect the full social cost.

For these reasons, very few nations operate as pure market economies. Even countries known for strong capitalism, such as the United States, still have taxes, regulations, public schools, environmental laws, and government programs like Social Security and Medicare. These features move them away from a pure market model.

The price system in a market economy helps coordinate decisions without one master planner. When prices rise, producers often see a profit opportunity and increase supply. When prices fall, they may cut production. Consumers also respond to prices by buying more or less. This system can be highly flexible, but it works best when information is accurate, competition is real, and harmful side effects are controlled.

The strengths of markets become weaker when competition is limited. If one company dominates an industry, consumers may face high prices and fewer choices. That is why the structure of the market matters as much as the economic system itself.

A mixed economy combines features of market and command systems. In a modern mixed economy, most production may be handled by private businesses and markets, but the government still plays an important role in regulation, taxation, public services, and social welfare. This is the most common model in the world today.

Mixed economies exist because pure systems rarely work well in real life. Markets are powerful at allocating many goods, encouraging innovation, and rewarding efficiency. Governments are useful for supplying public goods, protecting property rights, reducing fraud, correcting some market failures, and supporting people during hardship.

Countries differ in the extent to which their economies are mixed. The United States is often described as market-oriented, but it still uses regulations, antitrust laws, public education, public roads, and income support programs. Sweden and other Nordic countries rely heavily on markets too, but they combine them with higher taxes and more extensive public benefits, such as broader health care and welfare programs. China has also become a mixed system in important ways: it allows significant market activity, yet the government retains strong influence over finance, land, and major industries.

The key advantage of a mixed economy is flexibility. It can pursue growth and innovation while also trying to improve equity, security, and stability. The challenge is balance. Too little government oversight can allow monopolies, unsafe products, and environmental damage. Too much control can reduce competition, slow investment, and weaken incentives.

This balance is not fixed. During a recession, a mixed economy may temporarily increase government spending to support jobs. During high inflation, the government or central bank may act to cool the economy. In other words, mixed systems constantly adjust.

One of the clearest ways to compare systems is to ask how well they meet major economic goals. No system scores highest in every category. As we saw earlier in [Figure 1], gains in one area may require sacrifices in another.

| Economic System | Main Decision-Maker | Strengths | Common Weaknesses | Goals Most Often Advanced |

|---|---|---|---|---|

| Traditional | Custom and community | Stability, cultural continuity, local sustainability | Low growth, limited choice, slow innovation | Security within community, social cohesion |

| Command | Central government | Can direct resources quickly, may reduce inequality, can provide basic services | Inefficiency, shortages, weak innovation, limited freedom | Security, equity, national coordination |

| Market | Consumers and private firms | Innovation, efficiency, consumer choice, freedom | Inequality, market failure, less security, possible monopolies | Freedom, growth, innovation |

| Mixed | Both markets and government | Balances efficiency with protection, addresses some failures, supports stability | Can become overregulated or underregulated, political conflict over policy | Growth, stability, equity, security, innovation |

Table 1. Comparison of four economic systems by decision-making, strengths, weaknesses, and economic goals.

This comparison shows why real-world debates are often about degree rather than category. People may agree that some government role is necessary but disagree strongly about how large that role should be. They may support markets in most industries while wanting public control over schools, roads, or emergency services.

Many countries that are often seen as opposites actually use similar economic tools. Both highly market-oriented and more welfare-oriented nations use taxes, regulations, central banking, and public spending; the main difference is how much they use and where they apply them.

The most useful evaluation asks not only what a system promises, but what outcomes it produces in practice. Does it create jobs? Does it keep prices stable? Does it reward effort? Does it protect people from extreme poverty? Does it leave room for creativity and entrepreneurship?

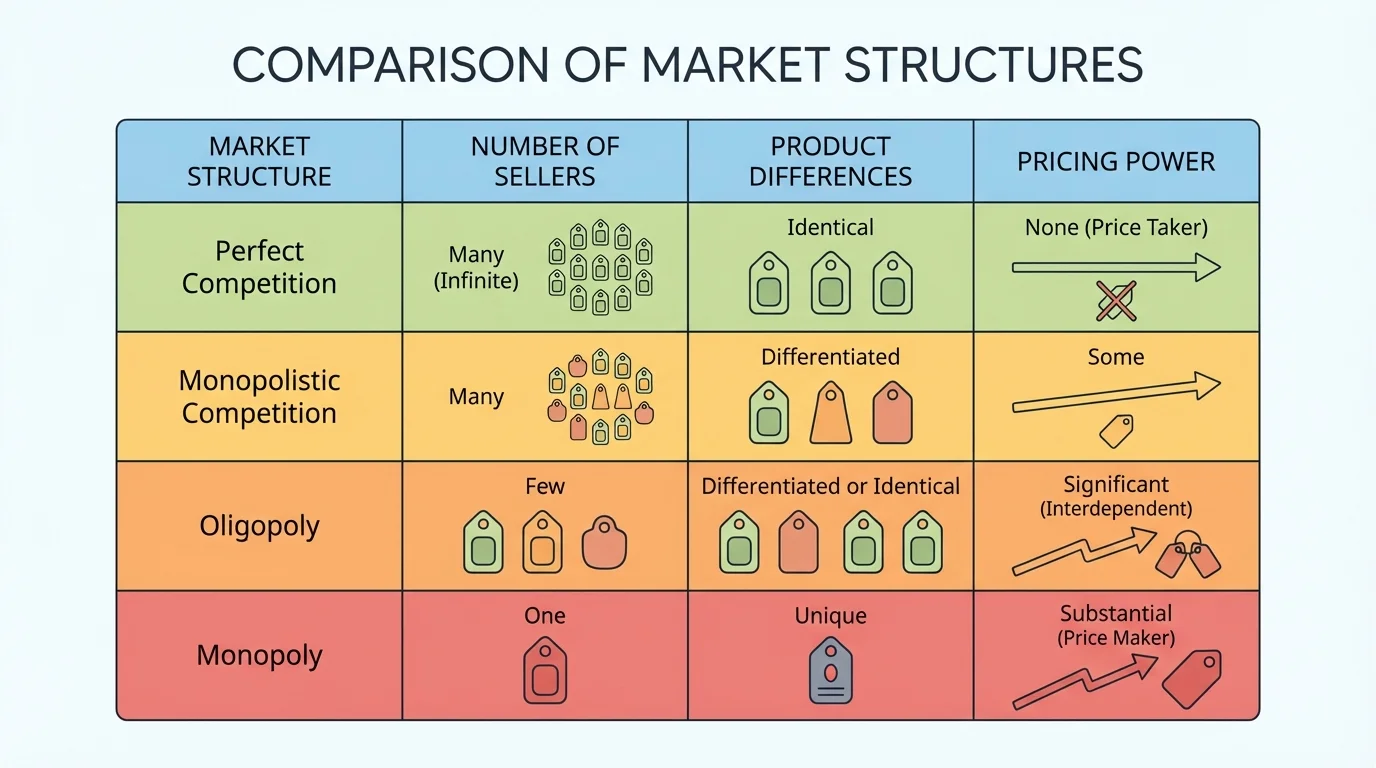

Even within a market or mixed economy, results depend heavily on competition. The number of sellers, the type of product, and the ease of entering an industry all influence prices, quality, and consumer choice. [Figure 3] compares common market structures and helps explain why some industries behave very differently from others.

In perfect competition, many sellers offer nearly identical products, and no single seller controls price. This is rare in a pure form, but some agricultural markets come close. In monopolistic competition, many sellers offer similar but slightly different products, such as clothing brands or restaurants. In an oligopoly, a few large firms dominate, as in commercial aircraft or smartphone operating systems. In a monopoly, one seller controls the market, such as a utility company in some regions.

More competition usually pushes firms to lower prices, improve products, and respond to consumers. Less competition gives firms more pricing power. That means a country can call itself a market economy, but if monopolies and oligopolies dominate, actual market outcomes may not feel competitive to consumers.

Producers and consumers both shape outcomes. Producers decide what to supply, how to market products, and whether to invest in technology. Consumers influence demand through purchases, preferences, and even social trends. If consumers shift toward sustainably produced clothing, firms may adapt quickly. If producers collude to limit output, prices may rise unfairly.

This is why antitrust policy matters. Governments in mixed economies often try to preserve competition by breaking up monopolies, blocking anti-competitive mergers, or preventing price-fixing. These actions are meant to keep markets open and dynamic rather than controlled by a few firms.

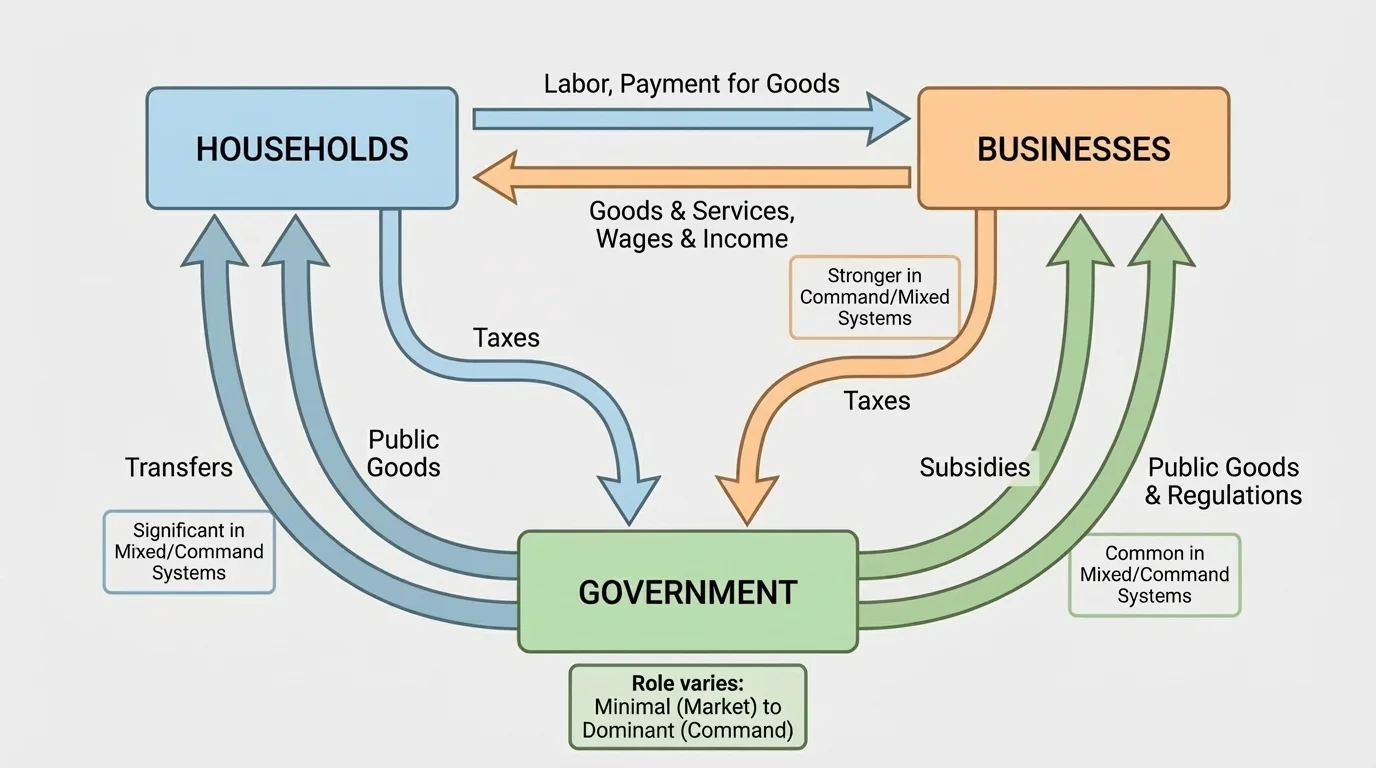

Government policy shapes market outcomes through laws, taxes, spending, and regulation. In a mixed economy, these tools influence what firms produce, what consumers can afford, and how income is distributed. [Figure 4] shows that government is not outside the economy; it constantly interacts with households and businesses.

Taxes raise revenue for public goods and services. Subsidies lower costs for certain activities, such as renewable energy or agriculture. Regulations set rules for workplace safety, consumer protection, food quality, financial reporting, and pollution. Transfer payments, such as unemployment benefits, help provide economic security.

Governments also respond to market failure, which happens when free markets do not allocate resources efficiently on their own. Public goods, externalities, information problems, and monopoly power are major examples. If no one would voluntarily pay enough for a lighthouse, the government may provide it. If a firm pollutes without paying the full cost, the government may regulate emissions or tax pollution.

Policy choices affect everyday life directly. A minimum wage law may raise incomes for some workers but increase labor costs for some employers. A subsidy for electric vehicles may encourage cleaner transportation. A sales tax may reduce consumer spending on certain goods. A central bank raising interest rates can slow borrowing for houses and cars, helping fight inflation but also cooling economic growth.

Case study: A government corrects a market failure

Suppose a city has several factories that release pollution into the air. The factories make products cheaply, but nearby residents suffer health problems.

Step 1: Identify the problem.

The market price of the factories' products does not include the full social cost of pollution. This is an external cost, so the market outcome is inefficient.

Step 2: Consider a policy response.

The city government can require pollution controls, fine firms for excessive emissions, or tax pollution-producing activity.

Step 3: Evaluate the trade-off.

Production costs may rise, and prices may increase, but health outcomes improve and the market reflects more of the true cost of production.

This is one reason mixed economies use regulation: not to replace all markets, but to improve outcomes when markets alone miss important costs or benefits.

Government action can help, but it can also fail. Poorly designed regulations may create unnecessary bureaucracy. Subsidies may go to politically favored industries instead of efficient ones. Price controls can create shortages if set too low. So the question is not whether government should ever act, but whether the action is effective, fair, and well-designed.

Looking at actual countries shows that systems are rarely pure. North Korea remains one of the clearest examples of a command-heavy economy. The state controls much economic activity, private freedom is highly restricted, and consumers have limited choice. The system emphasizes political control and state direction, but it performs poorly in innovation, freedom, and often living standards.

The United States is a market-oriented mixed economy. Private ownership, entrepreneurship, and competition are central. At the same time, the government provides infrastructure, enforces contracts, regulates industries, funds education, and runs social programs. This system has generated major innovation in technology, medicine, and finance, but it also faces criticism over inequality, health care costs, and market concentration in some industries.

Sweden illustrates a different kind of mixed economy. It uses markets and private firms, yet it combines them with broad public services and a stronger social safety net. Taxes are generally higher, but citizens receive more government-supported benefits. This model often scores well in security and social welfare while still supporting high productivity, though debates continue over tax burdens and long-term costs.

Some traditional communities, especially Indigenous or remote rural groups, preserve forms of traditional economic organization. These communities may prioritize mutual aid, land stewardship, and cultural continuity over maximum output. They can succeed in preserving identity and sustainability, though they may still rely on outside markets or government support for modern goods and services.

"There is no such thing as a purely free market or a completely controlled economy in the modern world."

— A principle often emphasized in comparative economics

China is especially important because it combines strong state influence with extensive market activity. Since economic reforms in the late twentieth century, private business and trade have grown dramatically. Yet the government still plays a major role in banking, strategic industries, and long-term planning. This makes China a powerful example of how mixed systems can take very different forms.

Good evaluation requires asking several questions at once. Does the system allocate resources efficiently? Does it encourage innovation? Does it protect consumers and workers? Does it reduce poverty? Does it create opportunity for people born into different social classes? Does it stay stable during crises?

It is also important to remember that outcomes depend not only on the type of system, but on institutions. Property rights, honest courts, low corruption, access to education, reliable infrastructure, and stable laws can make a huge difference. A market economy without the rule of law may work poorly. A mixed economy with strong institutions may balance goals more successfully.

As we saw in [Figure 3], competition matters because markets are not automatically competitive. As we also saw in [Figure 4], government policy can correct problems, but it can also create new ones if poorly designed. That is why economists and policymakers often argue over how much regulation, redistribution, and intervention are appropriate.

In the end, comparing economic systems is really about trade-offs. Traditional economies often preserve community but limit growth. Command economies may promise security and equality but often reduce freedom and efficiency. Market economies energize innovation and choice but can widen inequality and leave some needs unmet. Mixed economies try to combine strengths and reduce weaknesses, which is why they dominate the modern world.