A single bad financial decision can cost far more than people expect. A misleading loan ad, a fake investing tip, or a social media post that leaves out fees can turn what looks like a smart move into months or years of financial stress. In personal finance, information is not just helpful—it is powerful. The quality of the information you use often shapes the quality of the decision you make.

Financial decisions happen all the time, even for teenagers. Choosing a checking account, comparing cell phone payment plans, deciding whether to buy a used car, thinking about college costs, or responding to a "limited-time" online offer all involve money. To make sound financial decisions, you need more than opinions and ads. You need reliable sources of information and a clear way to judge them.

Using reliable information does not mean trusting the first website that appears in a search result. It means asking careful questions: Who created this information? Why did they create it? Is it current? Can it be checked against another trustworthy source? Does it match your goals and values? Good financial decision-making is both logical and personal. Facts matter, but so do the things you care about.

Money decisions often involve trade-offs. If you borrow now, you may have less freedom later. If you save now, you may give up something you want today. If you choose one bank account over another, the differences may seem small at first, but over time they can add up through fees, interest rates, access rules, and account features.

For example, suppose one account charges a $10 monthly fee and another charges no monthly fee. Over one year, that difference is $120. Over two years, it becomes $240. That is enough to change a student budget in a meaningful way. Reliable information helps you see the real cost, not just the attractive headline.

Reliable information also protects people from manipulation. Some financial messages are designed to trigger emotion rather than thought. They may use urgency, fear, status, or promises of easy money. A message like "earn cash fast with zero risk" should immediately raise questions, because in real finance, higher potential returns usually involve higher risk. When a claim sounds too easy, careful research becomes even more important.

Reliable financial information is information from a source that is accurate, current, relevant, and supported by evidence. A reliable source is usually transparent about who created the information, where the facts came from, and what limits or risks apply.

Bias is a tendency to present information in a one-sided way. In finance, bias often appears when a person or company benefits if you make a certain choice.

Fine print refers to detailed terms and conditions that may contain important costs, limits, or rules not emphasized in the main message.

Because financial decisions affect future opportunities, reliable information is a form of protection. It helps you avoid scams, compare choices fairly, and align your decisions with both short-term needs and long-term goals.

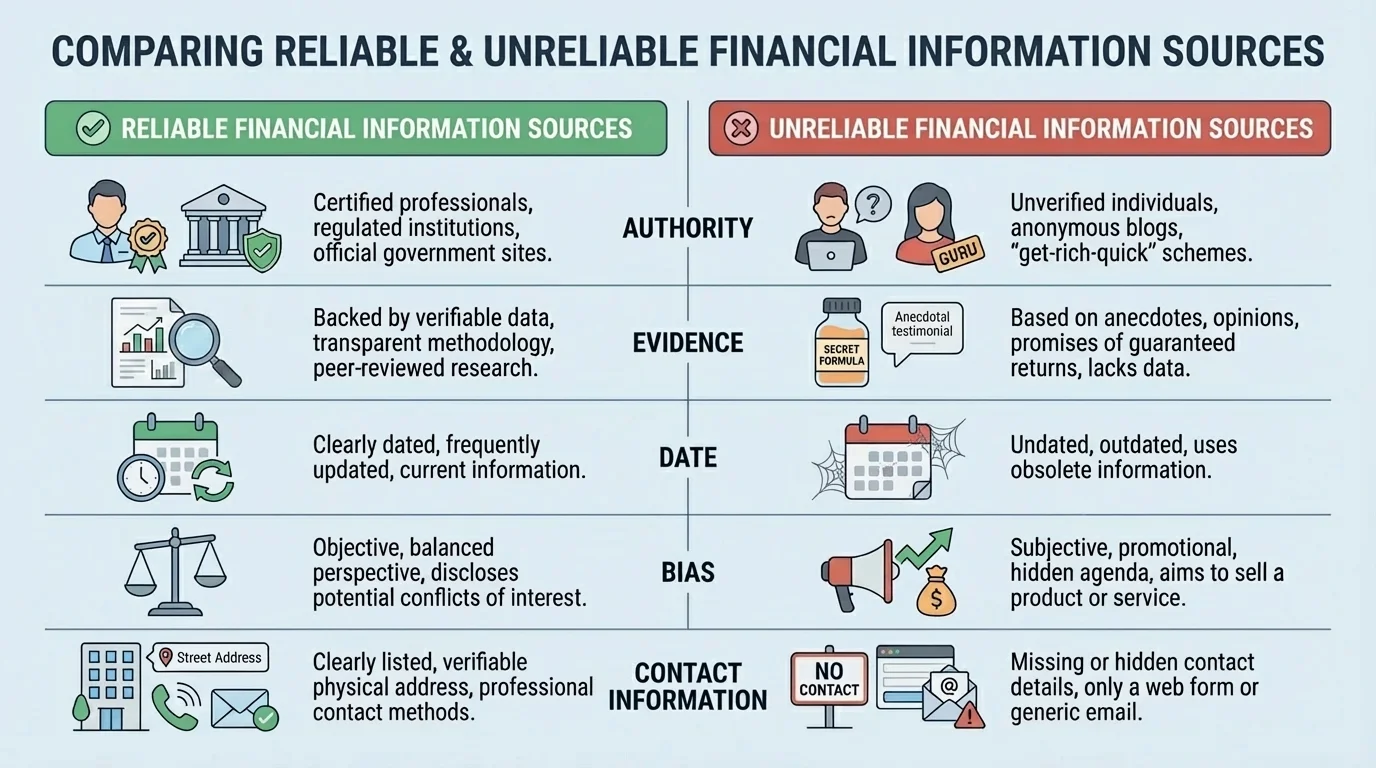

Students can judge source quality using clear criteria, as [Figure 1] shows through a comparison of trustworthy and questionable financial sources. A reliable source usually has authority, meaning it comes from a qualified institution or expert; evidence, meaning claims are supported by data or documents; timeliness, meaning the information is current; and transparency, meaning the source clearly states who produced it and why.

For example, a government consumer protection agency, a bank's official fee schedule, or a college's published financial aid office materials are usually more reliable than a random comment thread, a viral video with no sources, or an anonymous post claiming a "secret trick" to build wealth instantly. Reliability does not mean a source is perfect, but it does mean the information can be checked and is less likely to mislead.

Another important factor is objectivity. A source is more objective when it tries to inform rather than pressure. Many businesses provide useful information, but businesses also have products to sell. That means their information may be accurate in some ways while still emphasizing benefits more than costs. A smart reader does not reject business information automatically. Instead, the reader checks it against neutral or independent sources.

Reliability also depends on relevance. A source might be accurate but not useful for your decision. A national average interest rate, for example, gives context, but your actual decision depends on the rates, fees, and terms available to you in your area, with your age, account type, or credit history.

Finally, good sources provide enough detail to verify a claim. If a source says you can "save more," it should explain how. If it advertises a low loan rate, it should identify whether that rate is available to everyone, whether it is fixed or variable, and what conditions apply. As the comparison in [Figure 1] makes clear, trust increases when evidence and transparency increase together.

Reliable financial information comes from several types of places, and each serves a different purpose. Official financial institutions, such as banks and credit unions, provide direct information about account rules, fees, debit cards, overdraft policies, and online services. Their official disclosures are more dependable than advertisements alone because disclosures must include specific terms.

Annual percentage yield, often shortened to APY, is especially important when looking at savings accounts. APY tells how much money an account can earn in a year, including the effect of compounding. If one account offers a higher APY but also charges a monthly fee, you need both pieces of information before deciding which is better.

Government agencies are among the strongest sources for general financial guidance. They often explain consumer rights, common scams, taxes, student aid, credit, and borrowing rules in plain language. These sources are useful because their purpose is usually public education or consumer protection rather than selling a product.

Schools and community organizations can also be valuable. A counselor, business teacher, school financial aid advisor, library database, or nonprofit credit counselor may help students find trustworthy information and avoid confusion. These resources are especially helpful when a decision affects an entire family, such as paying for college or evaluating transportation costs.

| Resource type | Best use | Strength | Limitation |

|---|---|---|---|

| Official bank or credit union website | Checking fees, savings rates, account features | Direct source of terms | May emphasize selling points |

| Government agency website | Consumer rights, scams, loans, taxes, aid | Usually neutral and evidence-based | May be less specific to your personal case |

| School counselor or aid office | College costs, scholarships, forms | Guidance matched to student needs | Not always experts in every topic |

| Reputable news organization | Economic changes, rate trends, policy updates | Current reporting and context | Needs verification with primary sources |

| Social media post or influencer | Initial awareness of a topic | Can be easy to access | High risk of bias, missing details, or sponsorship |

Table 1. Common financial information resources, including their strengths and limitations.

Reputable news sources can also be useful, especially for understanding broader economic changes such as inflation, changes in interest rates, or updates to student loan policy. Still, news reports are often secondary sources. They may summarize information from a government report or company filing, so important decisions should be checked against the primary source whenever possible.

Many financial scams succeed not because the numbers look realistic, but because the message creates urgency. When people feel rushed, they are less likely to verify details, compare sources, or read the fine print carefully.

Even family and friends can be both helpful and limited. Personal experience matters, but one person's experience with a bank, scholarship, or car loan does not guarantee the same outcome for someone else. Advice from people you trust is best used as a starting point, not as the final answer.

Some financial information is not merely incomplete—it is designed to mislead. One warning sign is a lack of clear authorship. If you cannot tell who created the information, what organization they represent, or how to contact them, trust should drop immediately.

Another warning sign is emotional pressure. Phrases such as "act now," "guaranteed approval," "risk-free profit," or "everyone is getting rich from this" are often meant to push quick decisions. Reliable information invites understanding. Unreliable information often tries to bypass it.

A third warning sign is missing details. If a loan advertisement highlights low monthly payments but hides the total repayment amount, or if an investment promotion focuses on gains but ignores risk, the information is incomplete in a way that matters. Strong financial decisions require the full picture.

Sponsored content also deserves attention. Online creators may receive payment or free products for promoting financial apps, credit services, or investing platforms. That does not automatically make the information false, but it does create a conflict of interest. A recommendation may reflect a business relationship rather than what is best for the audience.

Scams frequently use fake authority, such as logos that resemble official agencies, invented testimonials, or websites with professional-looking designs but no real evidence. Good appearance is not proof. A polished page can still contain false information.

"If you do not understand how someone makes money from a financial offer, pause before you accept it."

Another red flag is information that cannot be confirmed anywhere else. If one source claims something dramatic and no trustworthy source supports it, skepticism is reasonable. In finance, major opportunities and major risks usually leave traces in multiple reliable places.

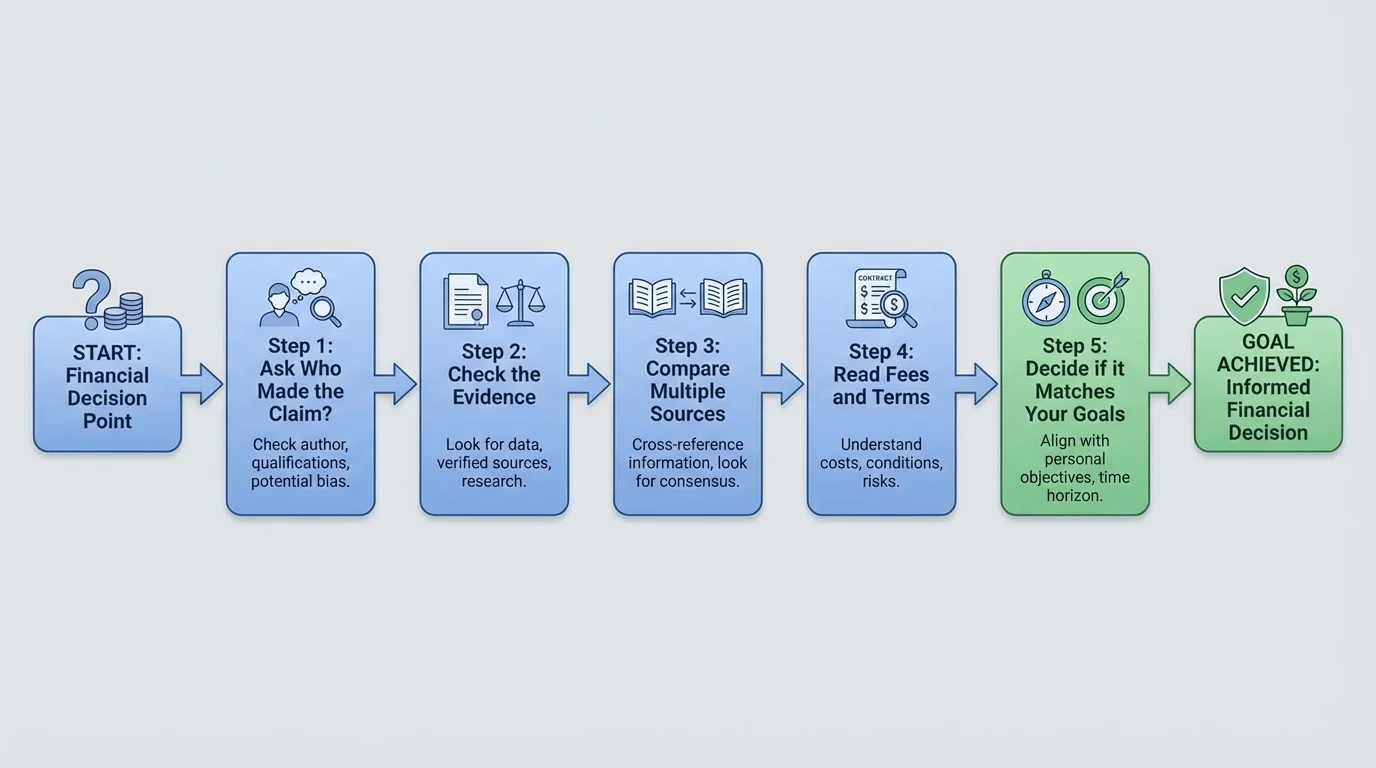

A strong financial decision is rarely based on one claim. It is based on a process, and [Figure 2] illustrates a practical sequence students can use again and again: identify the claim, check the source, verify the evidence, compare alternatives, read the terms, and decide whether the choice matches your goals.

Start by identifying exactly what the claim says. Is a credit card promising rewards? Is a bank account claiming "no fees"? Is a lender offering "low monthly payments"? Being specific matters because vague claims are harder to test.

Next, check the source. Look for official pages, disclosures, or documents. Then ask whether the information is current. Financial products change. A webpage from two years ago may no longer match current rates or rules.

After that, compare at least two or three reliable sources. For a savings account, compare APY, monthly fee, minimum balance, ATM access, and withdrawal rules. For a loan, compare the amount borrowed, total repayment, payment schedule, and penalties. If two sources disagree, keep investigating rather than guessing.

Then read the fine print. This is where hidden costs often appear. A "free" account may charge for paper statements, overdrafts, or out-of-network ATM use. A low introductory credit card rate may rise sharply later. Reading terms carefully is not being suspicious—it is being financially responsible.

Finally, connect the information to your own goals and values. The best option on paper may not be the best option for you. A student who needs easy access to cash might value ATM availability more than a slightly higher APY. A family that wants to avoid debt may reject a tempting financing offer even if the monthly payment seems manageable.

A systematic decision process means using the same careful method each time instead of relying on impulse. In finance, this reduces mistakes because it slows down emotional reactions and increases comparison, verification, and reflection.

Using a system also makes decisions more fair and consistent. If you compare every account or loan using the same checklist, you are less likely to be fooled by flashy language or one standout feature. The process in [Figure 2] works because it focuses attention on evidence before choice.

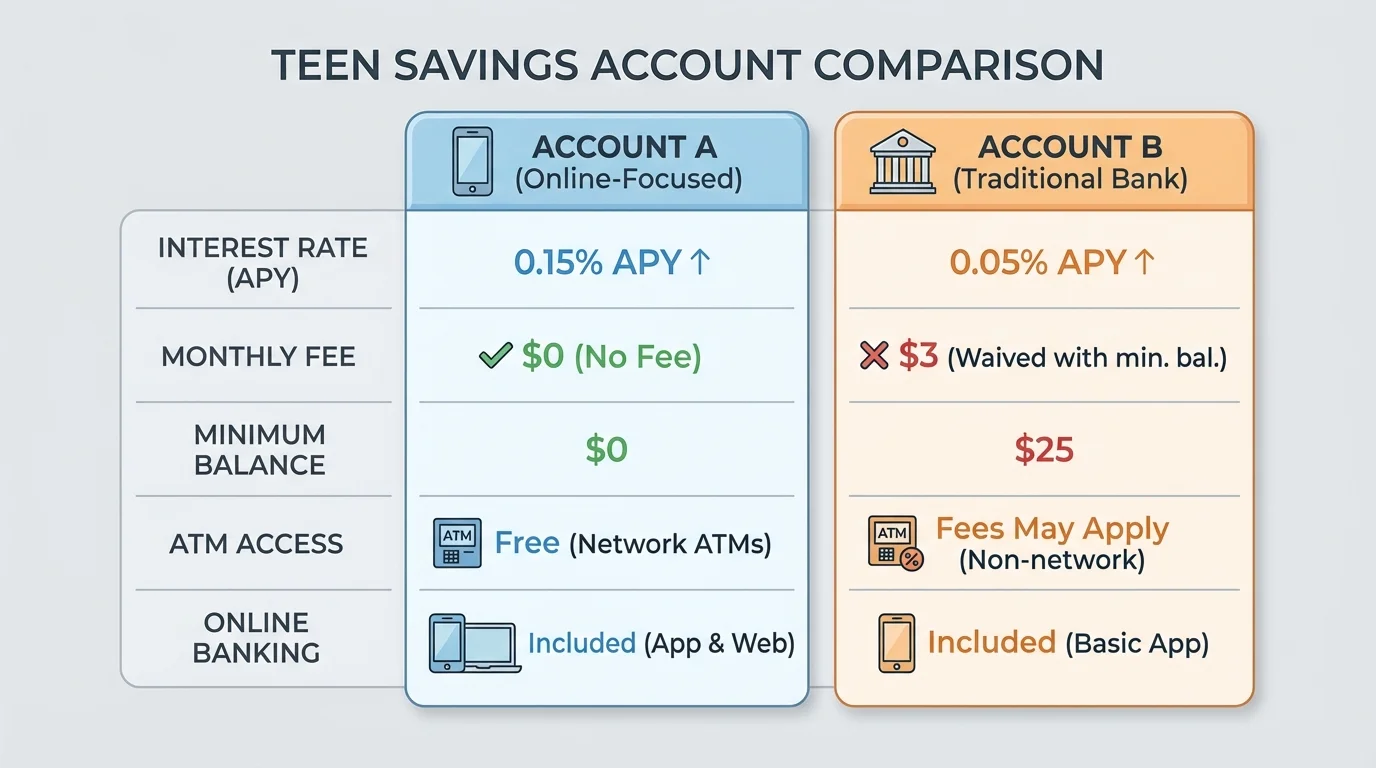

Small differences between financial products can change the better choice. Consider a student choosing between two savings accounts. Account A offers a higher APY, but Account B has no monthly fee and no minimum balance requirement. Without comparing all the details, it is easy to choose the wrong one for your situation.

[Figure 3] If you plan to keep only $100 in the account, a monthly fee can erase the benefit of a higher APY. But if you maintain a larger balance and meet the fee waiver rules, the higher APY may matter more. Reliable decisions come from matching product details to real behavior.

Suppose Account A pays $2 more in interest over a period, but charges $5 in fees. The net effect is a loss of $3, because \(2 - 5 = -3\). A headline that highlights earnings without showing fees is not enough. You need complete information.

Credit cards are another area where reliable information matters. A card advertisement may emphasize points, cashback, or student perks. But the most important details may include the annual fee, the interest rate after a missed payment, and how long an introductory offer lasts. A reward is only valuable if the total cost stays low.

Loans for cars, education, or emergencies also require careful checking. A lower monthly payment may simply mean the loan lasts longer, which can increase the total amount repaid. If one plan costs $220 per month for 24 months, the total repayment is $5,280 because \(220 \times 24 = 5,280\). If another plan costs $150 per month for 40 months, the total repayment is $6,000 because \(150 \times 40 = 6,000\). The lower monthly payment actually costs more overall.

Case study: comparing two phone financing offers

A student is deciding between two ways to get a $600 phone.

Step 1: Identify the offers clearly.

Offer A is $25 per month for 24 months. Offer B is $18 per month for 36 months.

Step 2: Find the total paid for each offer.

Offer A totals \(25 \times 24 = 600\). Offer B totals \(18 \times 36 = 648\).

Step 3: Interpret the result.

Offer B looks cheaper each month, but it costs $48 more overall and keeps the student locked into payments for an extra year.

The more reliable decision comes from looking beyond the monthly payment to the total cost, contract length, and any extra fees.

College financing is another major example. Students should compare tuition, fees, housing, transportation, grants, scholarships, work-study, and loans. A college with a higher listed price may become cheaper after grants, while a lower-price school may require more borrowing if aid is limited. Official financial aid documents, school cost calculators, and government aid sources are much more reliable than rumors or social media posts.

Insurance decisions also depend on reliable information. A plan with a lower monthly premium may have a higher deductible, fewer covered services, or narrower provider choices. The most useful source is usually the actual policy summary, not the short advertisement.

Later, when students begin exploring investing, reliable information becomes even more important. Investment decisions involve risk, return, time horizon, and fees. Online hype can make fast profits look normal, but long-term investing depends on verified information, diversification, and understanding uncertainty. The comparison in [Figure 3] reinforces a larger point: details that seem small at first often determine whether a choice truly helps you.

Financial decisions are not just about getting the highest number or the lowest price. They also reflect values. A person might choose a local credit union instead of a large bank because they value community connection. Another person might avoid certain companies because of environmental or labor concerns. A family might prefer stable, predictable costs over a riskier option with possible savings.

This means a good financial decision has two parts: accurate information and personal judgment. Facts tell you what is possible. Values help you decide what is desirable. Neither part should be ignored.

Community values matter too. Where people bank, borrow, shop, and invest can affect local businesses, jobs, and access to services. For example, choosing trustworthy local services may keep money circulating in the community. Supporting predatory businesses can harm both individuals and neighborhoods. Reliable information helps people see these larger effects.

Good decision-making often combines three earlier ideas: set a goal, gather evidence, and compare options. Personal finance uses the same pattern, but the evidence must include fees, risks, and long-term effects.

Different households also have different financial priorities. A family caring for relatives may value emergency access to money more than maximum earnings. A student trying to avoid debt may turn down a convenience purchase plan that another student accepts. Reliable information does not force everyone toward the same choice. It helps each person make a thoughtful choice that fits their situation.

The strongest financial skill is not memorizing every rule. It is building the habit of checking before choosing. That habit includes reading official documents, comparing multiple reliable sources, asking questions, and slowing down when something feels rushed or confusing.

A practical checklist can help. Before you accept a financial offer, ask: Who created this? What do they gain if I say yes? What are the costs, risks, and conditions? Can I confirm this with an official or neutral source? Does this fit my goals, budget, and values?

Keeping records is also useful. Save screenshots, fee schedules, emails, and policy summaries. If terms change or a problem appears later, documentation helps you understand what you agreed to and what rights you may have.

Another strong habit is updating information. Financial facts change over time. Interest rates move, scholarship deadlines shift, account terms are revised, and policies are updated. Reliable decision-making means using current information, not outdated assumptions.

Finally, ask for help when needed. Careful decision-makers are not people who always know the answer immediately. They are people who know when to verify, when to pause, and when to seek expert guidance. In personal finance, confidence should come from evidence, not from guesswork.