A surprising truth about money is that two accounts that look almost identical on an ad can lead to very different outcomes over time. One might quietly charge monthly fees. Another might pay more interest. A third might make your money easier to reach in an emergency. Choosing where to keep, borrow, or invest money is not just about convenience. It is about matching a financial institution and its products to your goals, your habits, and sometimes even your values.

Financial decisions become more powerful when they are made systematically. Instead of picking the first app, bank, or card you see, informed consumers compare options using reliable information: fees, protections, interest rates, ease of access, and the reputation of the institution. That habit matters whether you are opening a first account, saving for a car, paying for college, or helping your family make household decisions.

A financial institution is a business or organization that manages money and offers financial services. These services may include holding deposits, making loans, issuing credit, processing payments, selling insurance, or offering investment accounts. For most people, financial institutions are part of daily life long before they realize it. A paycheck may be direct-deposited into an account, a debit card may be used for groceries, and an app may transfer money between friends in seconds.

But not all institutions are built the same way. Some are owned by shareholders and aim to earn profits for investors. Some are owned by their members. Some exist mostly online. Some specialize in investing or insurance rather than basic banking. Because of those differences, they may offer different fees, rates, services, and levels of personal support.

APY means annual percentage yield, the amount a deposit account earns in one year including the effect of compounding.

APR means annual percentage rate, the yearly cost of borrowing, including interest and sometimes certain fees.

Liquidity is how quickly and easily money can be accessed without losing value or paying a penalty.

Good choices depend on context. A student who needs frequent access to money for meals and transportation may prefer one product. A family saving for a home down payment may choose another. A person who values local decision-making may prefer a member-owned institution. Financial literacy means knowing how to compare these options rather than assuming one choice fits everyone.

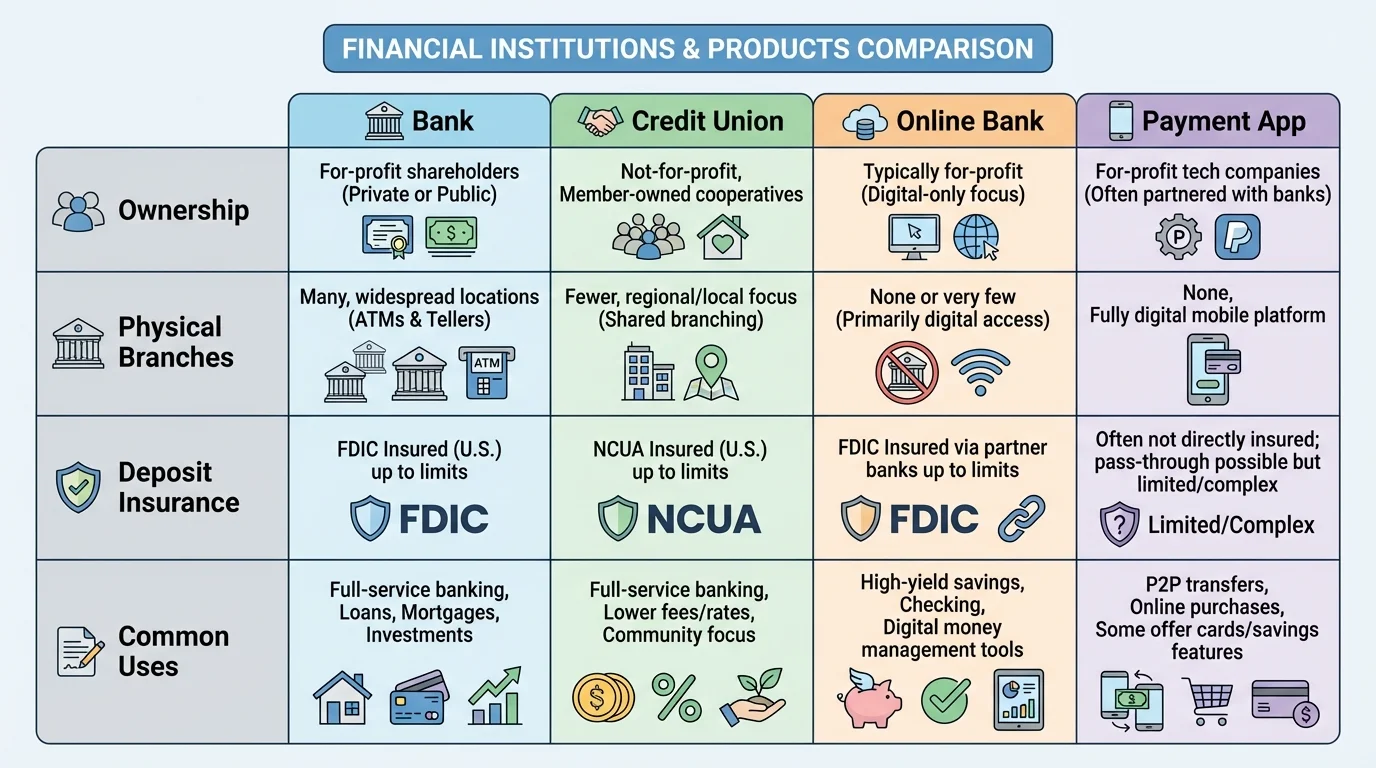

The most common financial institutions people encounter are commercial banks, credit unions, online banks, brokerage firms, insurance companies, and payment technology companies. These do not all serve the same purpose, and understanding their differences helps you avoid comparing unlike things. A comparison chart such as [Figure 1] makes it easier to notice that ownership, services, and protections can vary even when all of them appear in the same app store or shopping center.

Commercial banks are for-profit institutions that offer checking accounts, savings accounts, loans, and other services. They may have branch locations, online tools, or both. Large banks often provide many services and many ATMs, but some accounts may include fees unless certain requirements are met.

Credit unions are member-owned financial cooperatives. If you join, you become both a customer and a part-owner. Credit unions often emphasize community service and may offer lower loan rates or lower fees, though they may have fewer branch locations than large banks.

Online banks usually operate without many physical branches. Because they save money on buildings and staffing, they sometimes offer higher APYs on savings accounts and lower fees. However, depositing cash or getting in-person help may be less convenient.

Brokerage firms focus on investing. They allow customers to buy stocks, bonds, mutual funds, and exchange-traded funds. Some brokerages also offer cash management tools, but their main purpose is helping people build wealth through investments rather than handling everyday spending.

Insurance companies help people manage risk. Instead of holding spending money, they provide financial protection against losses from events such as car accidents, illness, property damage, or death. Insurance is a financial product because it transfers risk in exchange for regular payments called premiums.

Fintech companies use technology to offer financial services, often through apps. Some make payments easier, some help users budget, and some offer investing or lending. A payment app may feel like a bank, but it may not offer all the same protections or services. That is why consumers should verify whether money is insured, how transfers work, and what happens if the account is frozen or hacked.

Some people keep money in a payment app balance for convenience, but that balance may not work exactly like a traditional bank account. Protections depend on how the service is structured, so reading the details matters.

Another key difference is deposit insurance. In the United States, bank deposits are typically protected by the FDIC and credit union deposits by the NCUA up to legal limits when accounts are structured properly. That does not mean investments are guaranteed. If you buy stocks or mutual funds, their value can rise or fall.

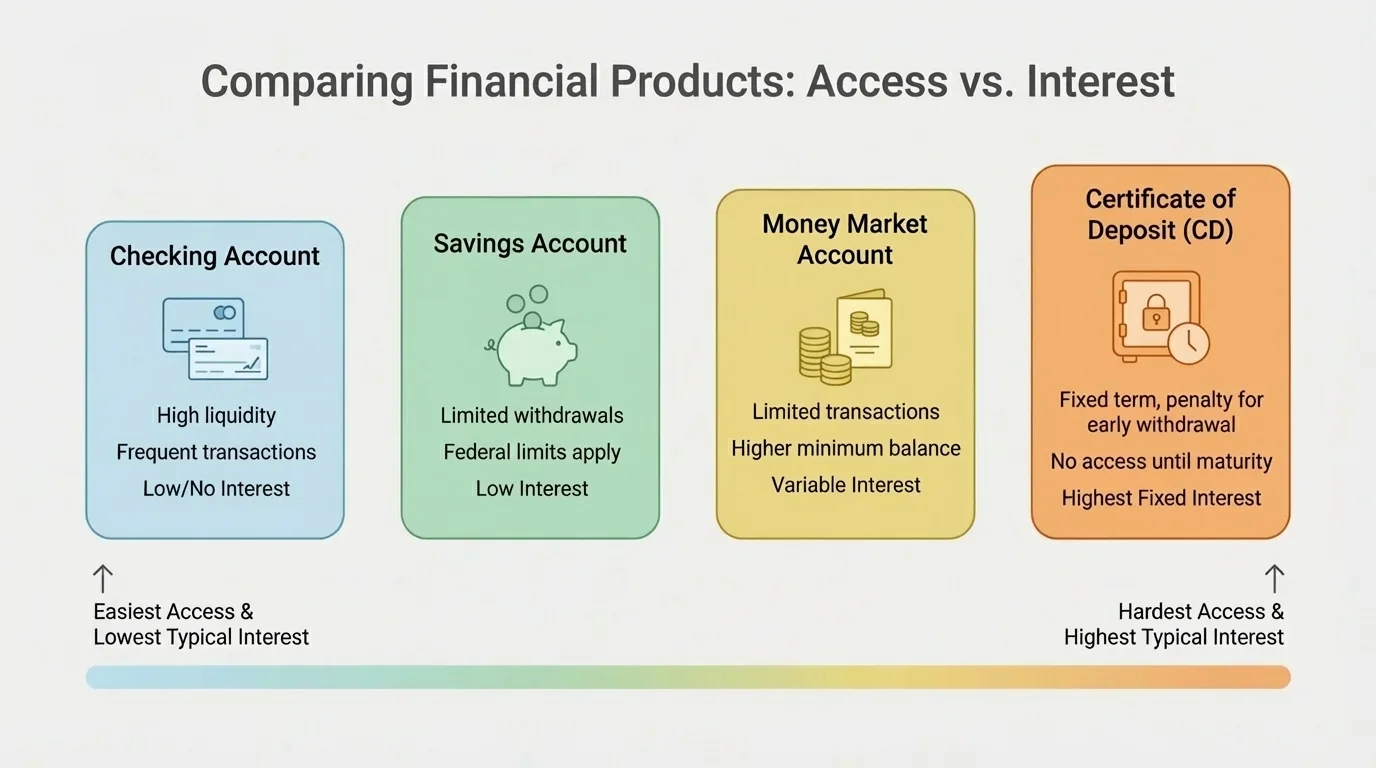

Financial products for daily life usually balance two goals: easy access and growth. In many cases, the more liquid a product is, the less it earns. A visual comparison like [Figure 2] helps show why students and families often use more than one product at the same time instead of expecting one account to do everything well.

A checking account is designed for frequent transactions. It usually comes with a debit card, online bill pay, and direct deposit options. Checking accounts are useful for everyday spending, but they often pay little or no interest. Some charge monthly maintenance fees, overdraft fees, or out-of-network ATM fees.

A savings account is built for storing money rather than constant spending. It usually pays more interest than checking and is a common place for emergency funds or short-term goals. The growth of money in a savings account can be estimated using simple compound growth. If $500 is in an account earning an APY of 4% for one year, the balance is approximately \(500(1.04) = 520\), so the money grows to about $520.

A money market account is a deposit account that may combine features of checking and savings. It often pays a competitive APY and may include limited check-writing or debit access. These accounts sometimes require higher minimum balances.

A certificate of deposit, or CD, usually offers a fixed interest rate for a set period, such as six months or one year. In exchange for the higher rate, you agree to leave the money in the account until the term ends. Withdrawing early may cause a penalty, which reduces liquidity.

Other products also affect spending. Prepaid cards let users spend loaded funds without opening a traditional bank account, but they may have activation or reload fees. Digital wallets store payment information on a phone or device and make transactions faster, but they are tools for access, not complete replacements for all banking functions.

| Product | Main Use | Liquidity | Typical Earnings | Common Costs or Limits |

|---|---|---|---|---|

| Checking account | Daily spending | Very high | Low | Monthly fees, overdraft, ATM fees |

| Savings account | Emergency fund, goals | High | Moderate | Transfer limits or minimums |

| Money market account | Savings with some access | High | Moderate to higher | Higher minimum balance |

| CD | Set-aside savings | Low until maturity | Often higher | Early withdrawal penalty |

Table 1. Comparison of common deposit products used for saving and spending.

When students compare these products, they should ask practical questions. How often will I use this money? Can I leave it untouched? What fees might erase the interest earned? As with the access-versus-earnings tradeoff shown in [Figure 2], the best product depends on the purpose of the money.

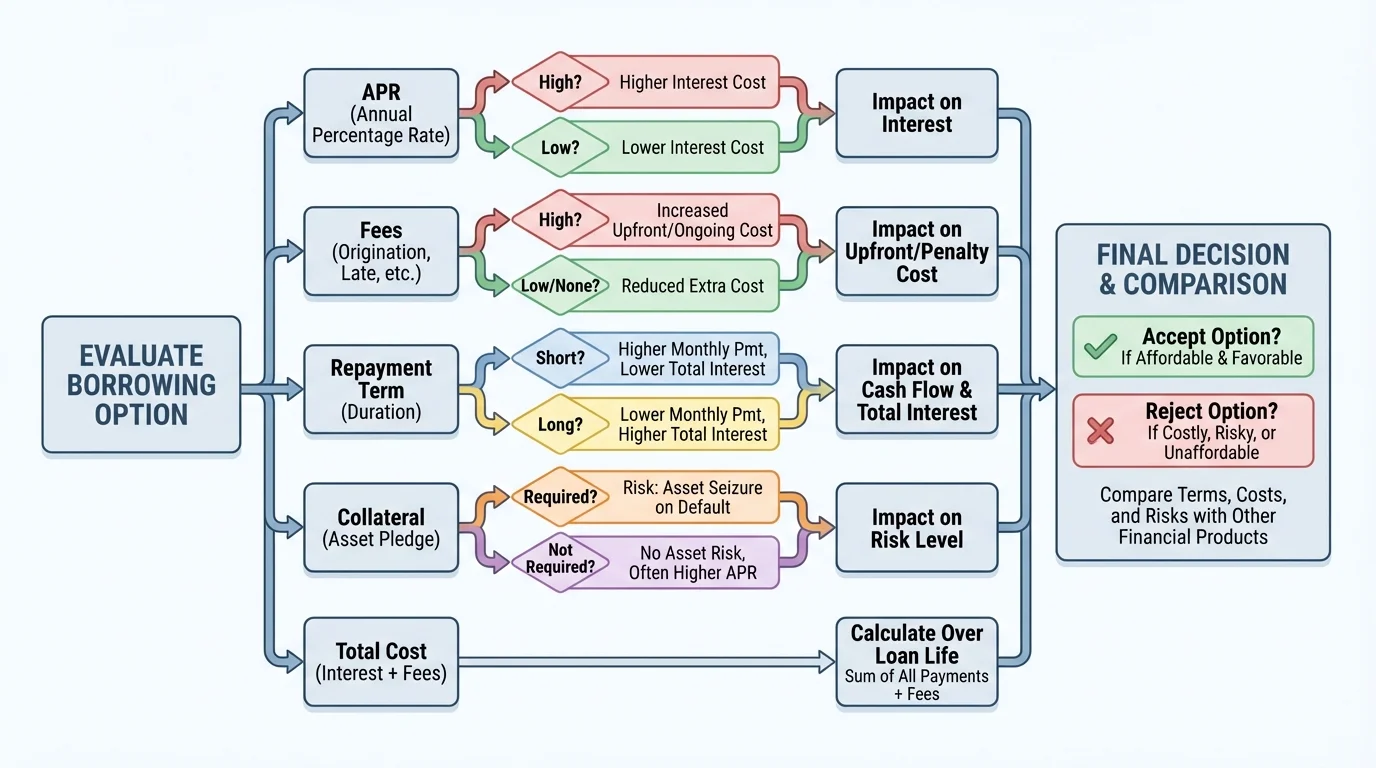

Borrowing can help people pay for large purchases, but it also creates obligations. A loan is not just about whether you can make the monthly payment. It is also about the total cost over time. A decision path like [Figure 3] is useful because two loans with the same monthly payment can have very different APRs, fees, and total repayment amounts.

A credit card lets a person borrow up to a limit and repay later. Credit cards are convenient and can help build credit history when used responsibly, but if the balance is not paid in full, interest charges can become expensive. If a card has an APR of 24% and a balance is carried month after month, the cost grows quickly.

Personal loans usually provide a fixed amount of money repaid in regular installments. Auto loans help finance a car and are often secured by the vehicle itself. Student loans are used for education expenses and may have different repayment rules depending on whether they are federal or private. Mortgages are long-term loans used to buy homes and are secured by the property.

The APR is one of the most important comparison tools because it allows borrowers to compare the yearly cost of loans. For example, suppose Loan A is $1,000 with 12% APR and a $20 fee, while Loan B is $1,000 with 10% APR and no fee. Even though Loan A may advertise a simple rate, the fee can make it more expensive overall. Reliable comparison means reading the disclosure, not just the large print in the ad.

Some borrowing products are especially risky. Payday loans and title loans often advertise fast cash, but they may carry extremely high fees or require risky collateral. A borrower who cannot repay on time may end up in a cycle of repeated borrowing. Products like these may solve an immediate problem while creating a much bigger one.

Comparing two borrowing options

A student needs $600 for an urgent car repair.

Step 1: Option A is a credit card cash advance with a fee of $30 and interest that will add about $18 if repaid quickly.

The estimated total cost is \(600 + 30 + 18 = 648\), so the total repayment is about $648.

Step 2: Option B is a payday loan with a fee of $90 due in two weeks.

The total cost is \(600 + 90 = 690\), so the total repayment is $690 after a much shorter time.

Step 3: Compare not just the payment date, but the overall burden.

Option B costs \(690 - 648 = 42\) more even before considering the risk of renewal fees if the borrower cannot pay on time.

This example shows why the lowest immediate barrier is not always the lowest total cost.

Later, when evaluating long-term debt such as auto loans or student loans, the same logic still applies: compare APR, total repayment, repayment length, and what happens if payments are missed.

Saving protects money, but investing aims to grow it over longer periods. Investing usually involves more risk than keeping cash in a bank account, but it also offers the possibility of higher returns. That tradeoff is a central idea in personal finance.

A brokerage account allows a person to buy and sell investments such as stocks, bonds, mutual funds, and ETFs. A mutual fund pools money from many investors to buy a diversified set of assets. An ETF, or exchange-traded fund, is similar in that it holds a collection of assets, but it trades on an exchange more like a stock.

Diversification means spreading money across different investments to reduce risk. Instead of putting all money into one company, an investor may own many companies through a fund. This does not eliminate risk, but it lowers the damage if one investment performs badly.

Risk and return are connected. Products that promise very high returns with little or no risk should be viewed with caution. In general, safer products such as insured savings accounts offer lower returns, while investments with greater uncertainty may offer higher potential returns over time.

Retirement accounts such as a 401(k) or IRA are designed for long-term investing. Even though many high school students are not opening these accounts yet, understanding them matters because early investing benefits from time. If money grows at 7% annually, then $1,000 becomes approximately \(1{,}000(1.07)^5 \approx 1{,}402.55\) after five years, not because of extra deposits, but because returns build on earlier returns.

Investments are not insured the same way deposits in a checking or savings account are. That distinction is one of the most important differences between institutions that hold cash safely and institutions that help money grow through markets.

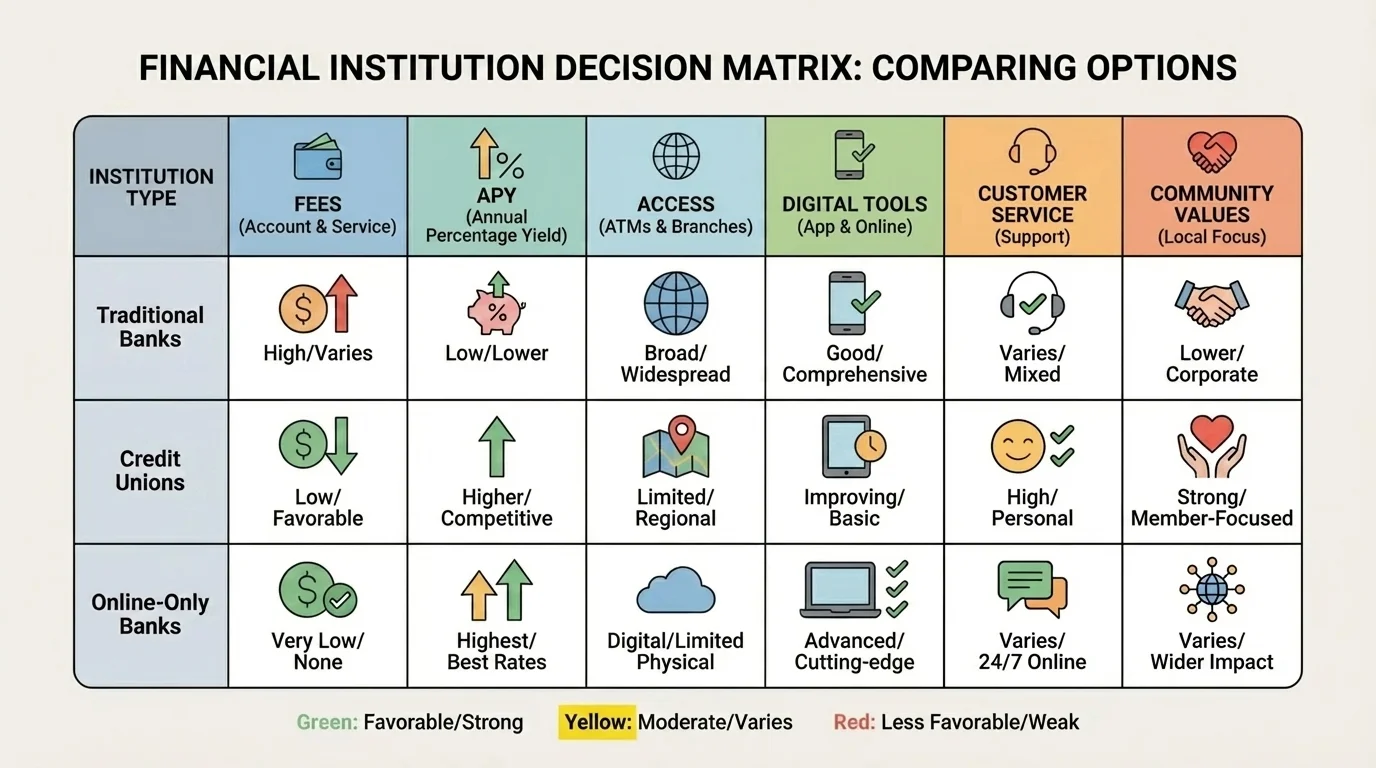

Financial literacy is strongest when it becomes a repeatable process. A comparison matrix such as [Figure 4] helps students move from vague opinions to clear criteria: fees, APY, APR, access, digital tools, customer support, minimum balance requirements, and alignment with personal or community values.

One useful method is to create a list of factors and score each option. For example, a student choosing between two savings accounts might compare monthly fee, APY, minimum deposit, branch access, and mobile app quality. If each factor is rated from \(1\) to \(5\), the student can total the scores and then reflect on which factors matter most.

Suppose Account A has no monthly fee, 4.25% APY, and no branch nearby. Account B has a $5 monthly fee, 3.00% APY, but a branch near school and strong customer service. For one student, Account A may be better because higher growth and no fee matter most. For another, Account B may be worth the cost because in-person help reduces mistakes and stress. Comparison is not only numerical; it also reflects priorities.

Values matter too. Some people prefer local institutions because they want their money circulating in the community. Others want powerful digital tools and nationwide ATM access. Some families prioritize avoiding interest-based debt whenever possible. A financial decision can be mathematically sensible and also connected to personal ethics or cultural values.

Using a simple scoring system

A student compares two checking accounts using four criteria scored from \(1\) to \(5\).

Step 1: Rate each account.

Account X scores \(5\) for fees, \(4\) for ATM access, \(3\) for app quality, and \(2\) for branch access.

Account Y scores \(3\) for fees, \(5\) for ATM access, \(4\) for app quality, and \(5\) for branch access.

Step 2: Add the scores.

Account X total: \(5 + 4 + 3 + 2 = 14\)

Account Y total: \(3 + 5 + 4 + 5 = 17\)

Step 3: Interpret the result.

Account Y has the higher raw score, but if the student cares most about avoiding fees, Account X may still be preferable. Numbers guide the decision, but priorities finalize it.

A smart comparison blends data and judgment. The best choice is not always the one with the biggest ad or the most popular name.

Reliable financial information usually comes from official disclosures, account agreements, government consumer protection sites, and the institution itself. Ads are designed to attract attention, but disclosures explain conditions. A high APY may apply only to balances below a certain amount. A bonus may require direct deposit. A "no fee" account may still charge for overdrafts, paper statements, or foreign transactions.

Students should learn to check the following: whether deposits are insured, what fees apply, how interest is calculated, whether rates are fixed or variable, and what penalties exist for late payment or early withdrawal. Reading this information takes patience, but it prevents expensive surprises.

| What to Compare | For Deposit Products | For Borrowing Products | For Investment Products |

|---|---|---|---|

| Cost | Monthly fees, ATM fees | APR, fees, penalties | Expense ratios, commissions |

| Growth | APY | Not applicable | Expected return, dividends |

| Access | Branches, ATM network, app | Repayment flexibility | Trading access, withdrawal rules |

| Protection | Deposit insurance | Consumer protections, disclosures | Market risk disclosures |

Table 2. Key comparison categories for savings, borrowing, and investing products.

It is also wise to verify information through more than one source. For example, if an app claims "instant cash with no hassle," a consumer should still check independent reviews, fee schedules, and official terms. Reliable information reduces the chance of being persuaded by marketing alone.

Consider three students with different goals. Maya wants a first paycheck account for part-time work. She needs a debit card, direct deposit, and no monthly fee. A checking account at a credit union or online bank may fit well. Jordan wants an emergency fund for unexpected expenses. A high-yield savings account may be better because it earns more while staying relatively accessible. Elena wants to save for a car in one year and knows she will not need the money right away. A CD might be worth considering if the rate is strong and the early withdrawal penalty is acceptable.

Now think about longer-term planning. A student comparing college financing should separate grants, scholarships, savings, work income, and loans. Not all aid is debt, and not all debt has the same cost. Federal student loans may provide protections that some private loans do not. A systematic comparison can affect financial health for years after graduation.

Choosing where to place $1,200 for one year

A student has $1,200 from summer work and wants the money available for next year's school expenses.

Step 1: Compare a savings account at 4% APY with a CD at 5% APY.

Savings estimate: \(1{,}200(1.04) = 1{,}248\)

CD estimate: \(1{,}200(1.05) = 1{,}260\)

Step 2: Calculate the difference.

The CD earns \(1{,}260 - 1{,}248 = 12\) more over one year.

Step 3: Weigh flexibility against earnings.

If the student might need the money early, avoiding a penalty may matter more than earning an extra $12.

This is a strong example of how the best product depends on timing, not just the highest rate.

These cases show that good financial decisions are personal, but they should not be random. They should reflect evidence, goals, and consequences.

Some warning signs appear again and again: promises that sound too good to be true, pressure to act immediately, unclear fee structures, missing contact information, and products that solve short-term problems while creating long-term debt. Predatory products often target people who are stressed, rushed, or unfamiliar with the financial system.

Smart habits include keeping records, checking account statements, turning on account alerts, using strong passwords, monitoring credit reports when older, and asking questions before agreeing to terms. Another good habit is separating wants from needs. Borrowing for a genuine necessity may be understandable. Borrowing for impulse spending can become a lasting burden.

When comparing any financial option, return to the same core questions: What does it cost? What does it help me do? How safe is it? How easy is it to access? Does it fit my goals and values?

The strongest financial decisions combine numerical comparison, careful reading, and self-awareness. Knowing the difference between institutions and products helps people protect their money, avoid traps, and choose options that support both individual goals and community well-being.