Two people can earn the exact same salary and still live very different financial lives. One may feel comfortable, able to save and pay bills on time, while the other struggles to cover rent and groceries. That difference is not just about spending habits. It is also about the economy they live in, the prices around them, and the kind of work they are prepared to do. To understand personal finance, you have to look beyond the paycheck itself and ask a deeper question: What can that paycheck actually buy?

When people talk about income, they often focus on the number printed on a job offer or a pay stub. But income matters in relation to prices. If a person earns $40,000 per year in a town where housing, food, and transportation are affordable, that income may go much further than $40,000 in a city where rent alone takes up most of the budget.

This is where the relationship between the economy and personal financial literacy becomes important. A person's financial choices are shaped by wages, job availability, inflation, taxes, and the local cost of necessities. In other words, personal finance is not only about earning money. It is also about understanding the conditions that determine how far that money stretches.

Income is money received from work, business activity, investments, or government benefits.

Cost of living is the amount of money needed to maintain a certain standard of living in a specific place.

Purchasing power is the amount of goods and services that money can buy.

Inflation is a general rise in prices over time, which reduces the value of money.

A key idea in economics is that money has both a number value and a buying value. If your hourly wage rises from $12 to $14, your income has increased. But if prices also rise sharply, your improved pay may not raise your actual living standard by much. That is why economists compare nominal income, which is income measured in current dollars, with real income, which is income adjusted for changes in prices.

To analyze income and purchasing power clearly, it helps to separate several related ideas. Standard of living refers to the level of material comfort a person or family can maintain. It includes housing quality, access to healthcare, reliable transportation, food choices, technology, and the ability to save or enjoy leisure activities.

Wages are payments for labor, usually by the hour or by salary. Benefits such as health insurance, retirement contributions, paid time off, and tuition support also affect total compensation. A job with a lower salary but strong benefits may provide more overall value than a higher-paying job with no benefits.

Another important term is unemployment rate, the percentage of people in the labor force who want work but do not have a job. A high unemployment rate usually means fewer available jobs and weaker bargaining power for workers. A low unemployment rate often means employers must compete more to attract workers, which can push wages higher.

Nominal income versus real income

Nominal income tells you how many dollars you earn. Real income tells you what those dollars are worth after accounting for price changes. If income rises by a smaller percentage than prices, purchasing power falls. If income rises faster than prices, purchasing power increases.

Suppose a student works part time and earns $10 per hour one year and $10.50 per hour the next year. At first, that seems like a raise. But if average prices increased by about the same percentage, the student's real income stayed almost unchanged. This is why a raise does not always feel like progress.

[Figure 1] The broader economy shapes job opportunities, wage levels, and income growth through the pattern of expansion and recession. When businesses are growing, they often hire more workers, increase hours, and sometimes raise pay to attract employees. When the economy slows, businesses may reduce hiring, cut hours, delay raises, or lay off workers.

Economists often describe these changes through the business cycle, a repeating pattern of expansion, peak, recession, and recovery. In an expansion, production and employment rise. At a peak, the economy is strong but may begin to overheat. In a recession, spending and production fall, and unemployment often rises. During recovery, growth starts again.

These economic shifts affect different industries in different ways. For example, during a recession, people may delay buying new cars, electronics, or homes, so jobs in manufacturing, construction, and retail may weaken. But some services, such as healthcare, repair work, or essential food production, may remain more stable. This means career choice matters not only for income, but also for how secure income is during difficult times.

Labor demand also matters. If a skill is in short supply and many employers need it, wages usually rise. If many people can do the same job and openings are limited, wages may remain low. This helps explain why specialized training in fields such as nursing, welding, computer networking, or engineering can increase earning power.

Interest rates, consumer confidence, and government policy also affect income. When interest rates rise, borrowing becomes more expensive, so people and businesses may spend less. That can slow hiring. When rates fall, borrowing is often cheaper, which may encourage business expansion, home buying, and job growth. These changes may sound abstract, but they influence whether people can find work, negotiate pay, or increase hours.

Some workers experience a decline in purchasing power even when their wage does not change at all. If inflation rises quickly while pay stays the same, the worker can afford fewer goods and services even though the paycheck amount has not gone down.

Young workers are often especially affected by economic conditions because they are newer to the labor market and more likely to work in entry-level jobs. During weak economic periods, employers may cut back on hiring less experienced workers first. That is one reason internships, certifications, work-based learning, and strong job skills can matter so much at the beginning of a career.

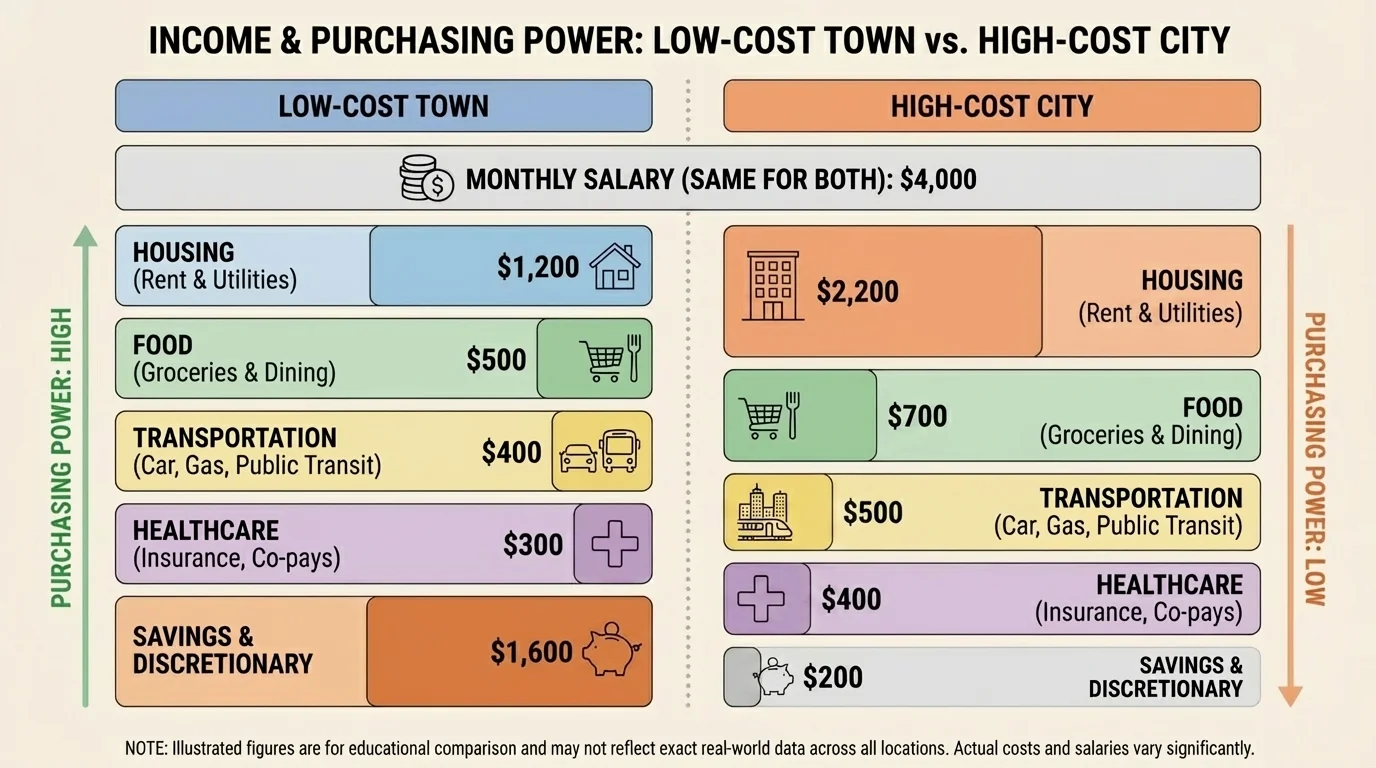

[Figure 2] Even when income is steady, local prices can greatly change financial comfort. The cost of living includes the major expenses people must pay regularly, and these expenses vary from one region to another and from one household to another.

Housing is often the largest expense. Rent or mortgage costs can differ dramatically between rural areas, suburbs, and major cities. A salary that feels adequate in one place may feel tight in another if housing costs double. This is why people comparing job offers should not focus only on salary. They should also compare local housing costs.

Food prices matter too, especially when families face higher transportation costs or when inflation affects groceries. Healthcare, insurance, utilities, internet access, child care, and taxes also shape how much income remains after essentials are paid. Transportation can be a major factor as well. In some places, public transit reduces costs. In others, owning a car is almost necessary, adding fuel, maintenance, insurance, and repair expenses.

Regional differences can be dramatic. A person earning $50,000 in a small town may be able to afford a one-bedroom apartment, transportation, groceries, and savings. The same $50,000 in an expensive metropolitan area may require roommates, longer commutes, and little room for emergencies or savings.

Taxes and public services also affect cost of living. Two locations may have similar prices but different tax structures. One area may have higher taxes but better public transportation, stronger public schools, or lower healthcare costs through local programs. Another may have lower taxes but require more out-of-pocket spending for transportation or services.

Household size changes cost of living too. A single adult and a family with children face different budget pressures. Child care, school supplies, food needs, and healthcare expenses can make a huge difference. Age matters as well. Teenagers planning for the future should recognize that a starting salary may feel manageable while living at home, but much less comfortable when covering full adult expenses independently.

| Expense Category | Low-Cost Area | High-Cost Area |

|---|---|---|

| Monthly rent | $900 | $1,900 |

| Groceries | $300 | $420 |

| Transportation | $350 | $250 |

| Utilities and internet | $220 | $280 |

| Healthcare and insurance | $250 | $320 |

| Total | $2,020 | $3,170 |

Table 1. A comparison of common monthly expenses in lower-cost and higher-cost locations.

This table shows why equal pay does not always mean equal financial freedom. The difference in total monthly expenses here is $1,150, which adds up to $13,800 over one year. That amount could be the difference between building savings and going into debt.

Purchasing power can be thought of as the real value of income. It answers the question, "What can my money buy?" If prices rise faster than income, purchasing power falls. If income rises faster than prices, purchasing power improves.

A simple way to estimate a change in real income is to compare the percentage increase in income to the inflation rate. If income increases by about 3% but prices rise by about 5%, a person is effectively worse off because purchasing power has declined.

Worked example: comparing wage growth to inflation

A worker earns $20 per hour and receives a raise to $21 per hour. During the same period, prices increase by 6%.

Step 1: Find the percentage increase in income.

The wage rises by $1 per hour. The percent increase is \(\dfrac{1}{20} = 0.05\), which is \(5\%\).

Step 2: Compare income growth to inflation.

Income grew by \(5\%\), but prices rose by \(6\%\).

Step 3: Interpret the result.

Because inflation was higher than the wage increase, the worker's real purchasing power fell slightly.

The worker has a higher nominal income, but a lower real income relative to prices.

Another way to compare purchasing power is through a budget. A person may have enough income to meet needs in one place but not in another. That is why employers sometimes offer different wages based on region, and why workers may relocate to improve their financial position.

We can express a simplified real-income idea with the relationship \(\textrm{real income change} \approx \textrm{income growth} - \textrm{inflation rate}\). This is not a perfect formula for every situation, but it is useful for basic analysis.

Worked example: estimating real income change

A salary rises from $36,000 to $38,160 in one year, while inflation is 4%.

Step 1: Find the salary increase.

The increase is $2,160.

Step 2: Convert to a percentage.

\[\frac{2160}{36000} = 0.06 = 6\%\]

Step 3: Compare to inflation.

Real income change is approximately \(6\% - 4\% = 2\%\).

The salary's purchasing power increased by about 2%.

The idea becomes even clearer when we compare how many hours of work are needed to buy something. If a worker earns $15 per hour, a $30 item costs \(\dfrac{30}{15} = 2\) hours of work. If the same item rises to $36 and the worker's wage stays the same, it now costs \(\dfrac{36}{15} = 2.4\) hours of work. That change reflects reduced purchasing power.

Percent increase compares the amount of change to the original amount. The basic structure is \(\dfrac{\textrm{change}}{\textrm{original}}\), then convert to a percent. This skill is essential for analyzing wages, prices, and inflation.

As we saw earlier in [Figure 1], changes in the economy affect income opportunities, while changes in prices affect what that income can buy. Strong personal financial decisions require understanding both sides at the same time.

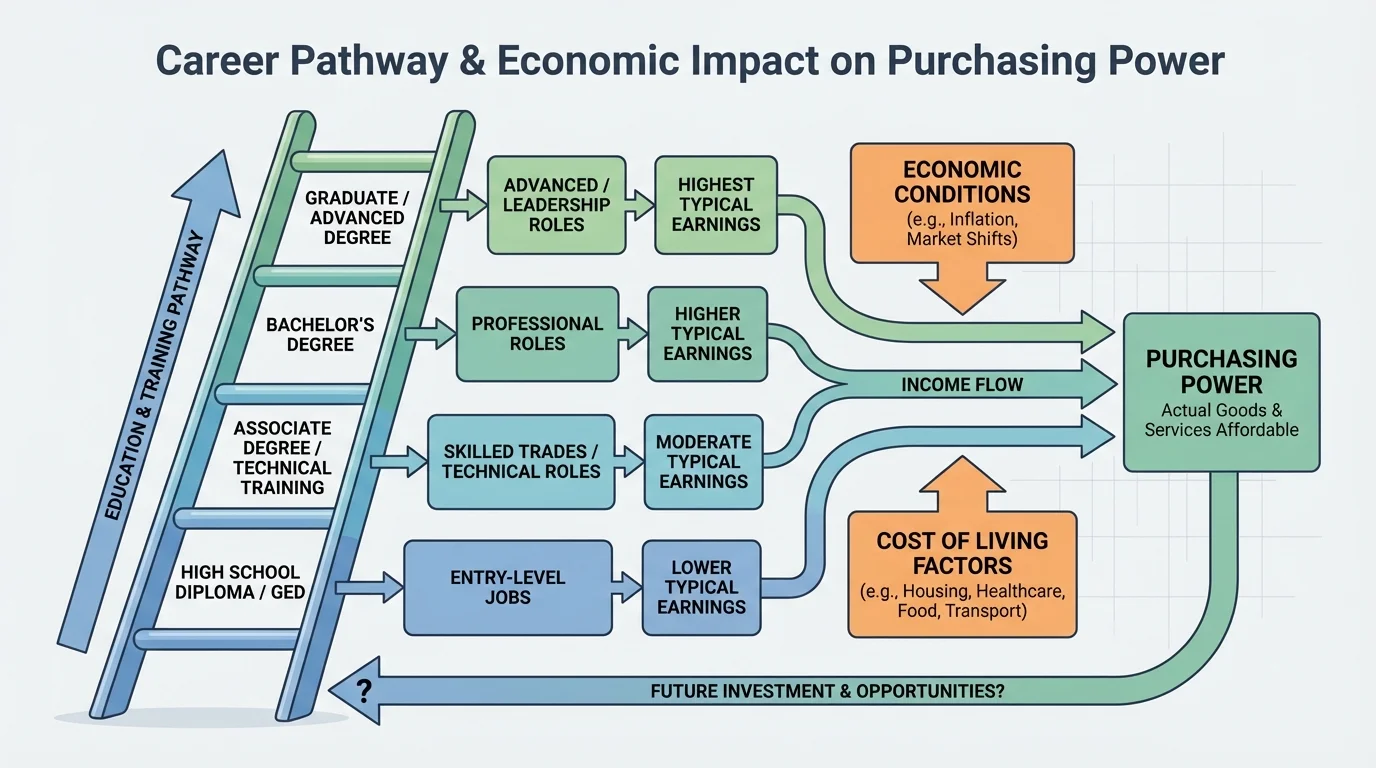

[Figure 3] Career preparation can change both income level and financial stability over time and can be understood as a pathway rather than a single decision. Education does not guarantee wealth, but it often increases access to higher-paying jobs, stronger benefits, and more advancement opportunities.

This preparation can take different forms: high school coursework, career and technical education, apprenticeships, industry certifications, two-year degrees, four-year degrees, and continuing education after entering the workforce. The best path depends on the person's goals, interests, costs, and the labor market.

Workers with specialized skills often have more choices and stronger bargaining power. For example, an electrician with apprenticeship training, a medical technician with certification, or a software developer with strong technical skills may earn more than someone in a job requiring little formal preparation. They may also be more protected when the economy weakens, because their skills are harder to replace.

Continuing education matters because the economy changes. New technology can make some jobs grow and others shrink. A worker who keeps learning may qualify for promotions, switch industries more easily, or adapt to changing demands. This can increase lifetime earning potential, which means the total amount of income a person is likely to earn over a working life.

However, more education is not automatically better in every case. Students should also consider costs, debt, completion rates, and job prospects. A shorter, lower-cost credential in a high-demand field may produce stronger financial results than a more expensive path with uncertain job opportunities. Smart planning means comparing both expected income and expected expenses.

Worked example: comparing two training paths

Student A begins full-time work immediately after high school at $28,000 per year. Student B completes a two-year technical program costing $12,000 total and then starts a job paying $42,000 per year.

Step 1: Find the annual income difference after training.

The difference is $14,000 per year.

Step 2: Estimate how long it takes to recover the education cost.

Divide the total cost by the annual income advantage: \(\dfrac{12000}{14000} \approx 0.86\).

Step 3: Interpret the result.

Student B could recover the cost in less than one year of work after entering the higher-paying job, assuming other factors are similar.

This does not prove one path is always better, but it shows how education can influence long-term earnings.

Later in life, the same principle shown in [Figure 3] still matters. Workers who update skills often remain more competitive, especially in industries shaped by automation, healthcare needs, advanced manufacturing, and digital systems.

Consider two graduates who each earn $48,000. One lives in a smaller city with modest housing costs. The other lives in a large urban area where rent is much higher. On paper, they look equally successful. In practice, their budgets may be very different.

The graduate in the lower-cost area may be able to build an emergency fund, pay down student loans faster, and save for transportation or housing. The graduate in the higher-cost area may still benefit from better transit, stronger networking opportunities, or faster career growth, but may have much less short-term financial flexibility. There is no universal best choice. The key is comparing total opportunity against total cost.

The same reasoning applies to family decisions. Living with relatives for a period of time, using public transportation, sharing housing, or choosing a shorter commute can improve purchasing power without increasing income. In finance, earning more is powerful, but lowering necessary expenses can be powerful too.

Income and purchasing power are not identical

High income does not always mean high purchasing power, and lower income does not always mean financial weakness. The full picture depends on prices, taxes, benefits, debt, savings habits, and local conditions.

This is one reason cost-of-living adjustments exist in some jobs and contracts. Employers and governments sometimes raise wages or benefits to reflect changing prices. Without such adjustments, inflation can steadily reduce real income.

Economic policy affects personal finance more than many people realize. Central banks influence interest rates. Governments make decisions about taxes, spending, public services, education funding, and labor rules. These policies affect inflation, job creation, and household costs.

For example, if inflation becomes very high, policymakers may try to slow spending to bring prices under control. That can help protect purchasing power in the long run, but it may also reduce hiring in the short run. If governments invest in infrastructure, education, or job training, they may create new opportunities and improve future earnings for workers.

Minimum wage laws can raise income for some workers, but local prices and labor market conditions still matter. A higher hourly wage helps, yet if housing and transportation costs rise rapidly, workers may still feel pressure. This is why economic issues are often debated from more than one angle.

Public goods and services also shape purchasing power. Affordable schools, libraries, roads, internet access, and healthcare programs can reduce household costs indirectly. So even when a policy does not put money directly into a paycheck, it can still affect what that paycheck needs to cover.

"It's not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for."

— Robert Kiyosaki

That quote is not a complete economic theory, but it highlights an important truth: income is only one part of financial well-being. Spending patterns, prices, savings, and planning all influence the final outcome.

Students can use these ideas right now. When comparing jobs, ask more than "What does it pay?" Also ask: What benefits are included? What is the local cost of housing? Is the schedule stable? Is there room for advancement? Will this job build skills that increase future earning power?

When thinking about college, technical training, or apprenticeships, compare expected costs with expected opportunities. A wise decision considers tuition, time required, likely debt, job demand, and starting wages. It also considers whether the field offers growth and whether continuing education will be needed later.

Budgeting decisions should also account for inflation. If prices for transportation, food, or housing are rising, households may need to adjust spending, increase savings, or seek higher-paying work. Understanding inflation helps people recognize why a budget that worked last year may not work this year.

Finally, a strong financial plan includes flexibility. Economic conditions change. Industries change. Prices change. The people who are best prepared are often not the ones with the highest starting income, but the ones who understand how income, cost of living, and purchasing power fit together and who keep building valuable skills over time.