A college acceptance letter can feel exciting, but one number can change everything: the cost. Two schools may offer the same major, yet one could leave a student with little or no debt while the other could lead to years of large monthly payments. Postsecondary education can open doors to higher earnings and more career choices, but only if students understand what they are paying for and how they plan to pay for it.

Education after high school is often an investment in future income. In general, more training, stronger credentials, and specialized skills increase access to careers with higher pay. But that does not mean the most expensive option is automatically the best. A smart decision balances career preparation, personal goals, total cost, and realistic payment options.

Many students first look at reputation, sports, campus life, or location. Those things matter, but cost matters too because money affects daily life long after graduation. Borrowing a large amount for school can delay other goals such as moving out, buying a car, saving for emergencies, or starting a business.

At the same time, avoiding all education costs is not always the smartest move either. Some credentials lead to much stronger earnings. If a program helps a student enter a stable, well-paying field, the cost may be worthwhile. The key is to compare what you pay now with what opportunities the credential creates later.

Education as an investment

When people talk about education as an investment, they mean spending money now in order to gain future benefits. Those benefits may include higher wages, better job security, health insurance, chances for promotion, and flexibility to change careers. A good investment is not simply the cheapest choice or the most prestigious choice; it is the option whose benefits are strong enough to justify the costs.

That is why students should investigate cost early, not after they are already emotionally committed to one school. Knowing the likely price can help students build a smarter college list, search for aid sooner, and avoid unrealistic choices.

Postsecondary options include any education or training after high school. These paths are not all the same length, cost, or purpose.

A bachelor's degree usually takes about four years and is common for careers such as engineering, teaching, accounting, and many health or business fields. An associate degree often takes about two years and may lead directly to work or transfer into a four-year program. A certificate or industry credential may take a few months to two years and often prepares students for specific jobs such as welding, medical assisting, coding, automotive technology, or cosmetology. Apprenticeships combine paid work with training, which can reduce education costs while building job experience.

Different pathways can lead to strong earnings. For example, a student who completes a two-year nursing pathway or technical credential in a high-demand trade may begin earning sooner than a student in a four-year program. On the other hand, some careers require a bachelor's degree or more. The best option depends on career goals, required qualifications, and cost.

| Pathway | Typical Time | Common Costs | Potential Advantage |

|---|---|---|---|

| Certificate or credential | 1 year to 2 years | Tuition, tools, fees, transportation | Faster entry into the workforce |

| Associate degree | About 2 years | Tuition, fees, books, living costs | Lower cost than many four-year paths |

| Bachelor's degree | About 4 years | Tuition, housing, books, fees, living costs | Access to many professional careers |

| Apprenticeship | Varies | Usually lower direct school costs | Earn while learning |

Table 1. Comparison of common postsecondary pathways by time, costs, and advantages.

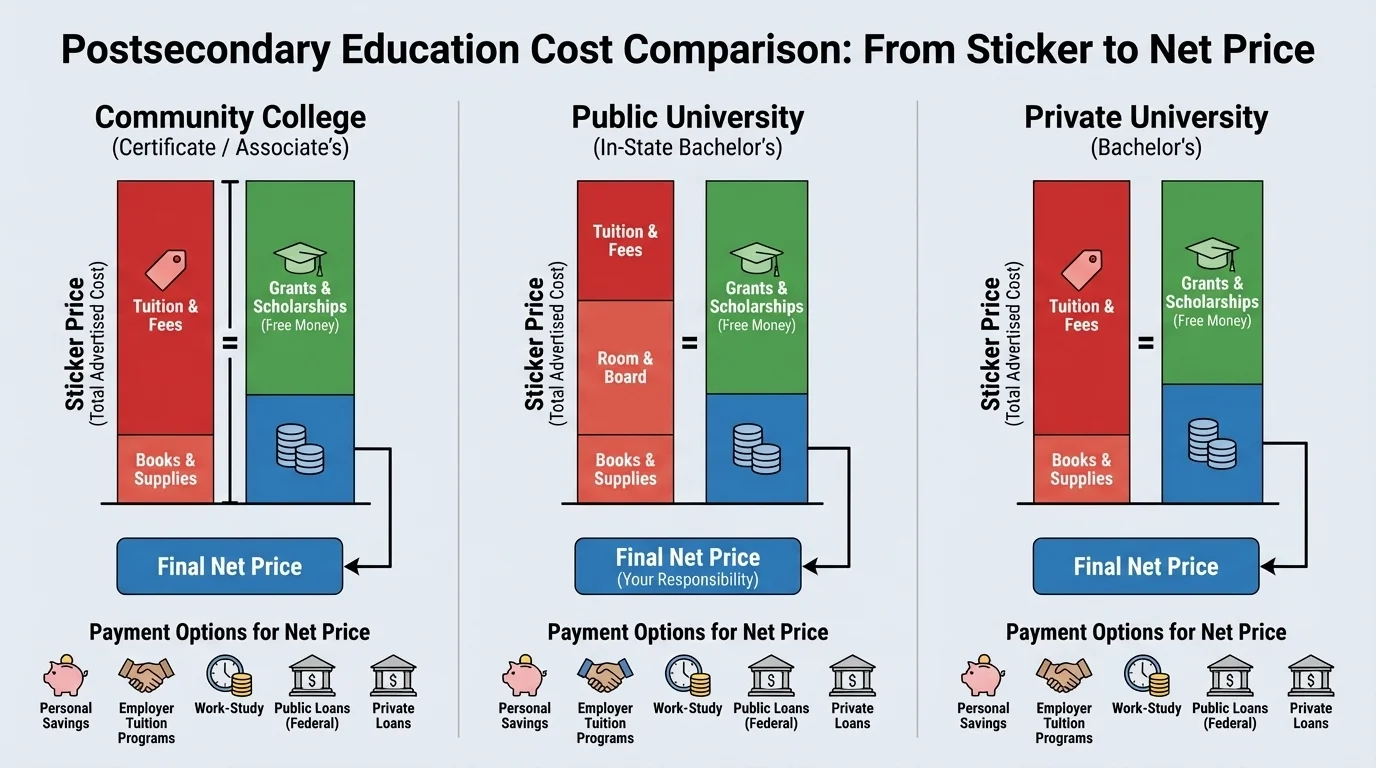

The first cost students often see is tuition, but tuition is only one part of the full bill. The total cost of attendance usually includes tuition, fees, books, supplies, housing, food, transportation, and personal expenses. One school can look expensive at first, but after aid is applied, its overall cost may become more competitive than a school with a lower published price.

This is why students need to know the difference between sticker price and net price. Sticker price is the published cost before financial aid. Net price is what remains after grants and scholarships are subtracted. Net price is usually the more useful number for comparing affordability.

[Figure 1] Suppose School A has a sticker price of $28,000 and offers $12,000 in grants and scholarships. The net price is $16,000 because \(28{,}000 - 12{,}000 = 16{,}000\). School B has a sticker price of $18,000 but offers only $1,500 in grants and scholarships. Its net price is $16,500 because \(18{,}000 - 1{,}500 = 16{,}500\). Even though School B looks cheaper at first, School A actually costs less after gift aid.

Students should also think beyond one year. A program that costs $12,000 per year for four years has a total raw cost of $48,000 because \(12{,}000 \times 4 = 48{,}000\). A two-year program costing $9,000 per year has a total raw cost of $18,000 because \(9{,}000 \times 2 = 18{,}000\). Time in school affects total cost, especially if living expenses continue each year.

Another hidden factor is opportunity cost, which is what you give up by choosing one option over another. If a student spends four years in school full time, that student may delay full-time earnings. If another student completes a shorter program and begins working sooner, the financial picture changes. Opportunity cost does not mean longer education is bad; it means students should compare both direct costs and the timing of earnings.

Cost of attendance is the full estimated yearly cost of going to a school or program, including tuition, fees, books, supplies, housing, food, transportation, and other necessary expenses.

Opportunity cost is the value of the next best alternative you give up when you make a choice.

Location matters too. Living at home while attending a nearby community college may reduce housing and meal costs. Going out of state may increase tuition and travel costs. Some programs require special equipment, uniforms, software, certification exams, or tools. These extra costs can add up quickly.

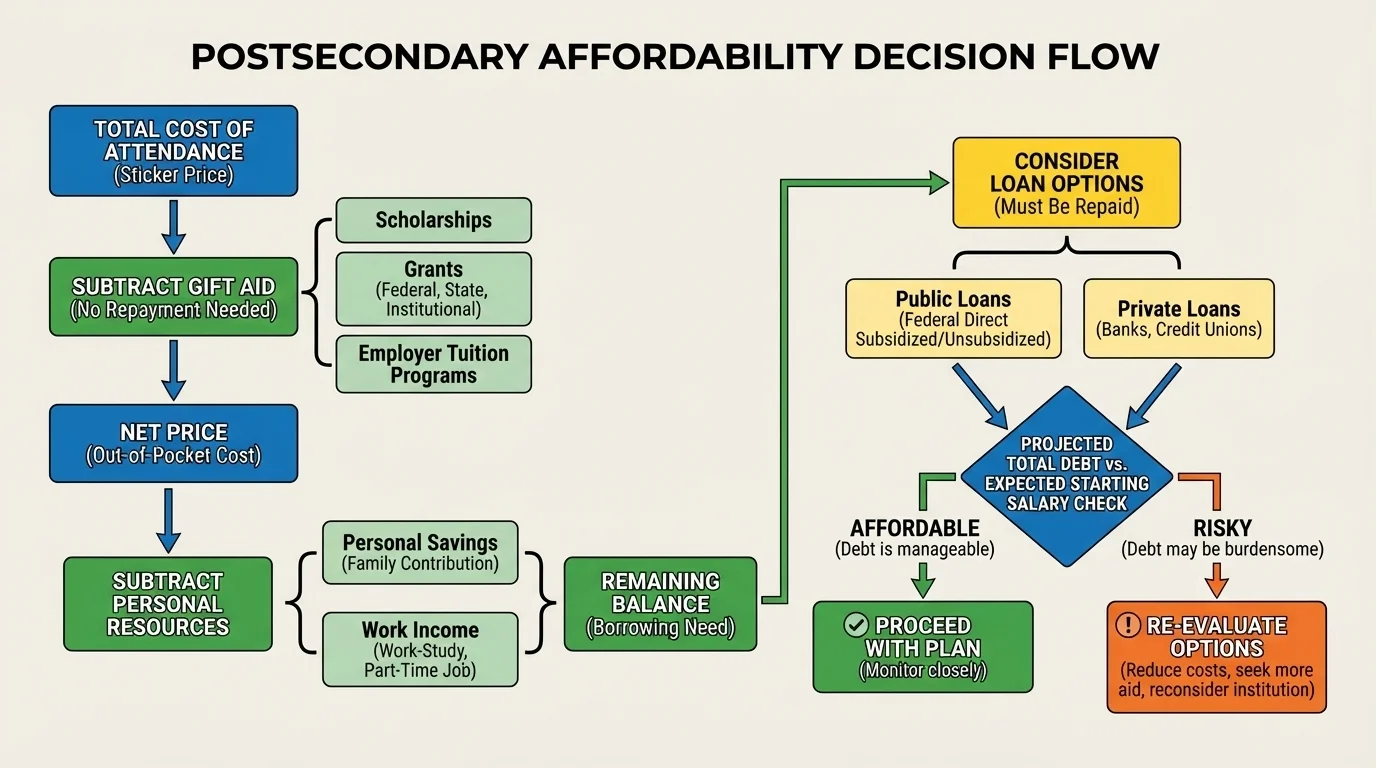

Affordability is not just whether a school accepts you; it is whether you can realistically pay for it without causing serious financial harm. Affordability works like a sequence of questions: What is the net price? How much can be covered by savings, current income, and aid? How much would need to be earned or borrowed? Is that borrowing reasonable compared with likely future income?

[Figure 2] Students and families can ask several practical questions. How much is available from savings? How much aid is gift aid rather than loans? Can the student work a manageable number of hours? Will borrowing be small enough that monthly loan payments after graduation are realistic? Does the chosen field usually provide income strong enough to support repayment?

One common rule of thumb is to avoid borrowing more in total than you expect to earn in your first year of full-time work. This is not a perfect rule, but it helps students notice when debt is becoming risky. For example, borrowing $60,000 for a career that may start around $35,000 per year is much riskier than borrowing $15,000 for a career that may start around $50,000 per year.

Affordability also includes day-to-day life during school. If a student must work so many hours that grades suffer, the plan may not be sustainable. If transportation is unreliable or living costs are unstable, even a school with a low tuition rate may become hard to manage. Financial plans must be realistic, not just optimistic.

Students sometimes assume the most famous school is always the best financial choice, but many graduates build successful careers from community colleges, regional universities, technical programs, and apprenticeships that cost far less.

When comparing options, students should write out a full yearly budget. A simple planning relationship is:

Net amount to cover equals total cost of attendance minus grants, scholarships, savings, and other support. In symbols, \(C - A = R\), where \(C\) is total cost, \(A\) is aid and available resources, and \(R\) is the remaining amount the student must cover through work, payment plans, or loans.

The best funding sources are usually the ones that reduce cost without creating future debt. These include personal savings, scholarships, grants, and some forms of work-study.

Personal savings can come from summer jobs, part-time work, family contributions, or education savings accounts. Savings reduce the amount that must be borrowed. Even a few thousand dollars can make a difference. If a student has $4,000 in savings and faces a $14,000 yearly net cost, the remaining amount drops to $10,000 because \(14{,}000 - 4{,}000 = 10{,}000\).

Scholarships are awards that usually do not need to be repaid. They may be based on grades, activities, athletics, leadership, community service, artistic talent, identity, career interest, or local community connections. Some are one-time awards; others renew each year if the student maintains certain grades or enrollment levels.

Grants also usually do not require repayment. They are often based on financial need and may come from federal or state governments, colleges, or organizations. Grants can dramatically reduce net price, especially for students from lower-income households.

Work-study is a program that allows eligible students to earn money through part-time jobs, often connected to the school. Work-study is useful, but students should remember that it is earned over time. It does not always reduce the first bill immediately in the same way a grant does.

Comparing gift aid and remaining cost

A student is considering a technical college with a total yearly cost of $11,500. The student receives a $3,000 grant, a $2,500 scholarship, and plans to use $2,000 from savings.

Step 1: Add the resources that reduce the amount to cover.

\(3{,}000 + 2{,}500 + 2{,}000 = 7{,}500\)

Step 2: Subtract from the total yearly cost.

\(11{,}500 - 7{,}500 = 4{,}000\)

The student still needs to cover $4,000 through earnings, a payment plan, or borrowing.

Searching for scholarships takes effort, but the hourly payoff can be huge. Winning a $1,000 scholarship after spending five hours applying is financially powerful because it is similar to earning $200 per hour before taxes.

Some funding options involve earning money while studying, and others involve help from employers. These options can be valuable when used carefully.

An employer tuition program is a benefit in which a company pays part or all of an employee's education costs. Some employers pay upfront; others reimburse the employee after courses are completed successfully. These programs are common in some health care, retail, technology, and business settings. They work especially well for students who attend school part time while employed.

Part-time jobs can also help cover books, transportation, food, or a portion of tuition. But students need balance. If a student works too many hours, graduation may be delayed, which can increase the total cost. A job that supports school is helpful; a job that prevents progress can become expensive in the long run.

Some schools offer payment plans that spread tuition across several months instead of requiring one large payment. This does not remove the cost, but it can make cash flow easier to manage. Families must still check whether the plan includes fees.

As we saw earlier in [Figure 1], the most useful comparison is not the published price alone. Students should compare how much each funding source truly lowers the amount they still need to cover.

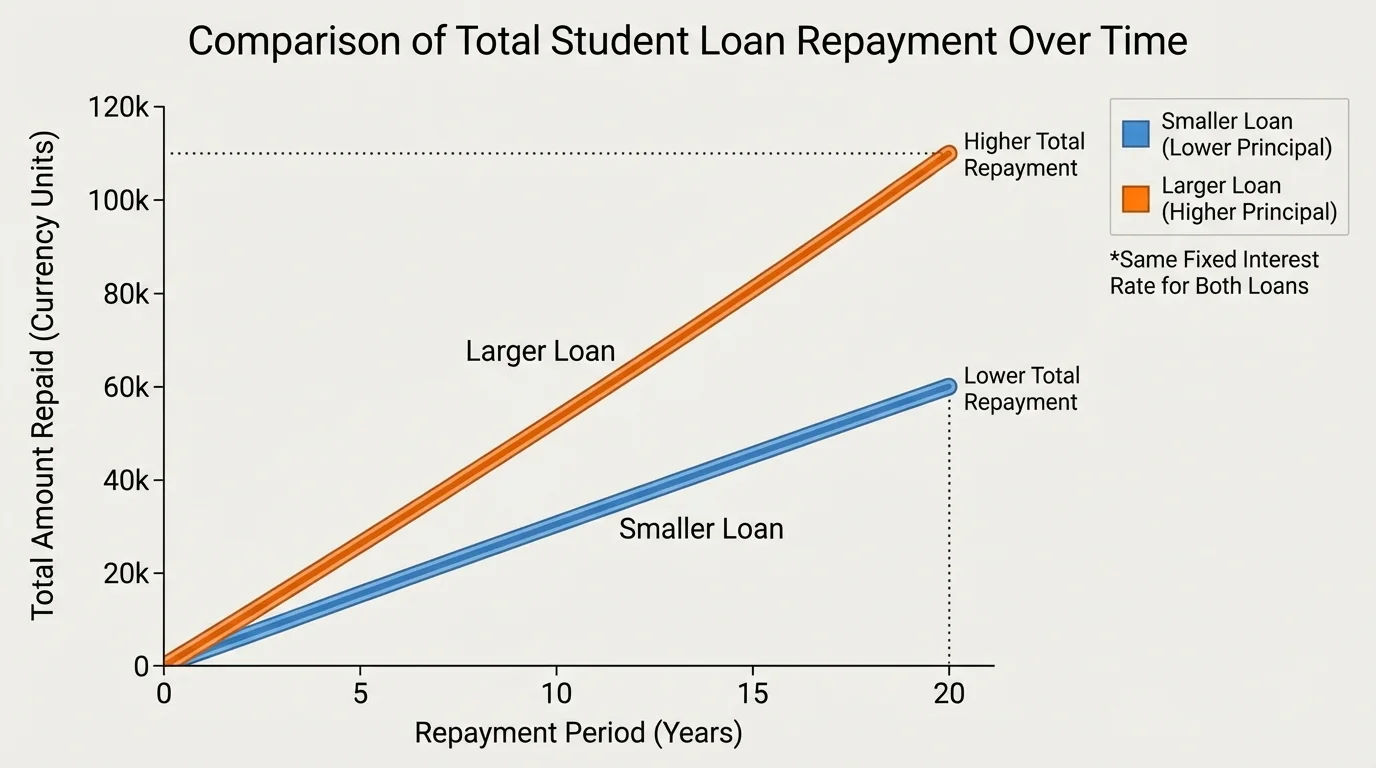

Student loans can make education possible, but they must be understood clearly. Borrowing affects future monthly budgets, as [Figure 3] illustrates, because the amount repaid is often greater than the amount borrowed.

A loan is money that must be repaid, usually with interest. Interest is the cost of borrowing. If you borrow more, or if the interest rate is higher, or if repayment lasts longer, the total repaid increases.

There are two broad categories of student loans: federal loans in the United States and private loans, which come from banks, credit unions, or other lenders. Federal loans often have borrower protections, fixed interest rates, and repayment options connected to income. Private loans may have fewer protections and may require a co-signer. Because of these differences, many financial advisers suggest using federal loans before private loans if borrowing is necessary.

Suppose a student borrows $8,000 for one year. If the student later repays $9,200 in total, then the cost of borrowing was $1,200 because \(9{,}200 - 8{,}000 = 1{,}200\). That extra amount matters because it reduces future money available for rent, transportation, savings, and other goals.

Students should also distinguish between subsidized and unsubsidized public loans when those options exist. In a subsidized loan, the government may cover interest during certain periods, such as while the student is enrolled. In an unsubsidized loan, interest usually begins building earlier. That means two students borrowing the same principal may repay different totals.

Private loans can be especially risky because their terms may depend on credit history, variable interest rates, or co-signer agreements. A co-signer becomes responsible if the student cannot repay. This makes private borrowing a serious family decision, not just a student decision.

Estimating a borrowing need

A university has a net yearly cost of $19,000. A student can use $5,000 in savings, expects to earn $4,000 during the year, and receives $6,000 in grants and scholarships.

Step 1: Add available nonloan resources.

\(5{,}000 + 4{,}000 + 6{,}000 = 15{,}000\)

Step 2: Subtract from the net yearly cost.

\(19{,}000 - 15{,}000 = 4{,}000\)

The remaining amount is $4,000. If the student covers it with a loan each year for four years, the total borrowed would be \(4{,}000 \times 4 = 16{,}000\), not including interest.

That total may be manageable for some careers and risky for others. This is why expected earnings matter. Students should research typical entry-level wages in their intended field and compare them with likely debt.

Numbers become clearer when we compare complete scenarios. Consider three students with different plans.

Student A attends a community college while living at home. Total yearly cost is $8,500. A state grant covers $3,000, a local scholarship covers $1,500, and the student uses $2,000 from savings. Remaining cost is \(8{,}500 - 3{,}000 - 1{,}500 - 2{,}000 = 2{,}000\). If the student earns $2,000 through part-time work, no borrowing is needed.

Student B attends a four-year public university away from home. Net yearly cost after grants and scholarships is $17,000. The student has $3,000 in savings and earns $3,500 per year. Remaining cost is \(17{,}000 - 3{,}000 - 3{,}500 = 10{,}500\) each year. Over four years, borrowing could reach \(10{,}500 \times 4 = 42{,}000\), before interest.

Student C enters an apprenticeship. Direct education costs are low, and the student earns wages while training. Earnings may start lower than those of a fully trained worker, but the student avoids most school debt and gains experience immediately.

Which option looks most affordable?

If Student A expects a starting salary of $42,000, Student B expects $48,000, and Student C expects $38,000 during the transition into full employment, the debt comparison matters as much as the salary comparison.

Step 1: Compare likely borrowing.

Student A: \(0\) debt. Student B: about \(42{,}000\) before interest. Student C: very low or \(0\) education debt.

Step 2: Compare debt with expected income.

Student B may borrow almost as much as the expected first-year salary, which is a warning sign. Students A and C have much lower financial pressure after training.

This does not mean Student B made a wrong choice. It means Student B should be especially sure the degree is required, the career path is solid, and lower-cost alternatives have been considered.

These examples show that affordability is not only about total salary. It is about the relationship between cost, aid, time, and the earnings that follow.

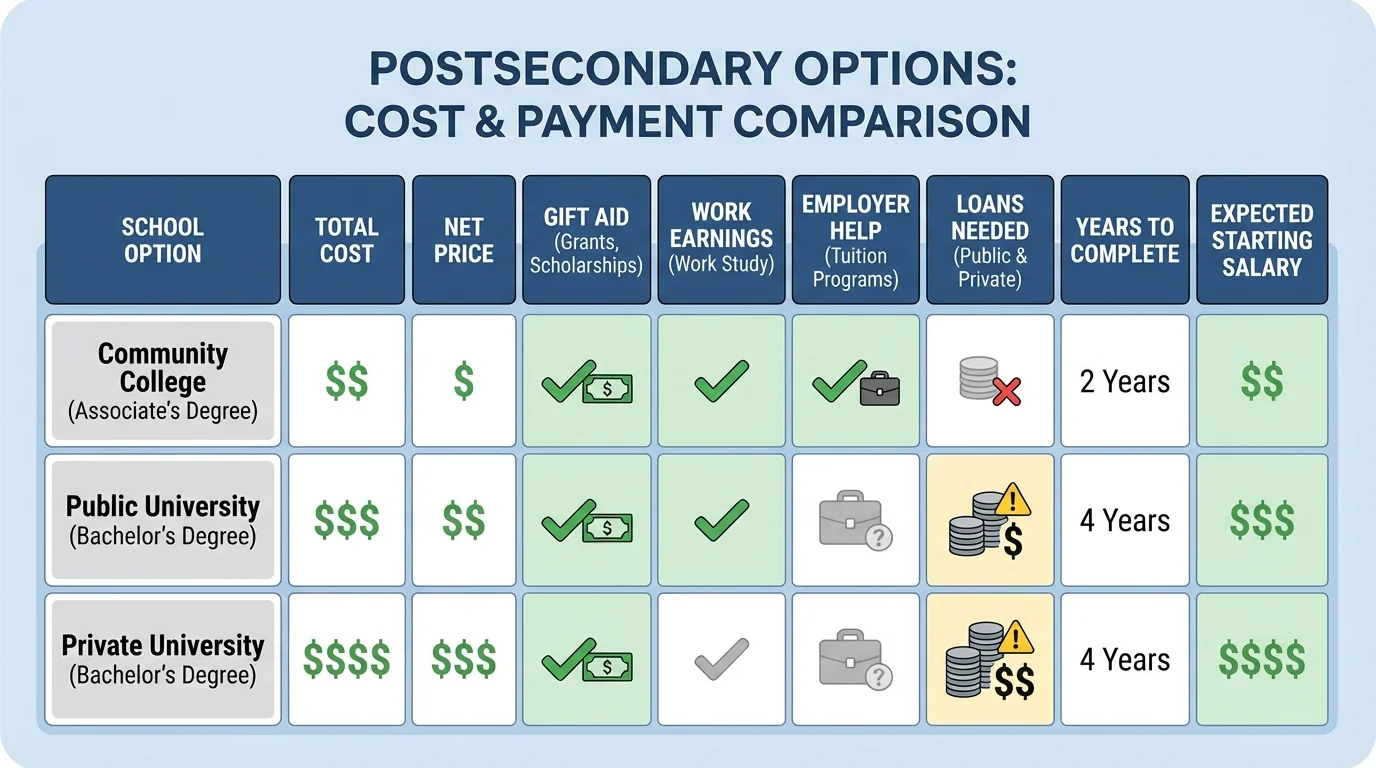

Choosing a school or program is easier when students compare options side by side. A written checklist makes tradeoffs clearer and less emotional.

[Figure 4] Students should compare at least these items: total yearly cost, net price, grants, scholarships, savings available, work-study or job earnings, employer tuition help, loan amount needed, total time to complete the credential, and expected starting salary in the intended field.

It also helps to ask practical questions. Is the school accredited? Does the program have strong graduation rates or job placement rates? Will credits transfer if plans change? Are there lower-cost pathways, such as starting at a community college and transferring later? Does the degree or credential match actual job requirements?

A smart payment plan often follows this order: first use savings and grants, then scholarships, then reasonable earnings from work, then employer tuition assistance if available, and only then consider limited public loans. Private loans should usually be approached with the greatest caution.

Later, when comparing final offers, students can return to [Figure 4] and check whether the higher-cost option truly provides benefits that justify the extra expense. Sometimes it does. Often, it does not.

"The best education choice is not the one with the biggest name. It is the one that prepares you well at a cost you can manage."

Financial literacy matters here because education decisions connect directly to adult income, spending, saving, and debt. A strong plan does more than get a student into school. It helps that student leave school with options, flexibility, and a stable financial future.