A single car crash, medical emergency, apartment fire, or stolen identity can cost far more than most people can pay out of pocket. That is why insurance matters. Insurance is not just a product adults buy and forget about; it is one of the main ways people protect income, property, health, and future financial stability. Even high school students are affected by insurance through family health plans, car insurance, rental situations in the future, and digital risks such as identity theft.

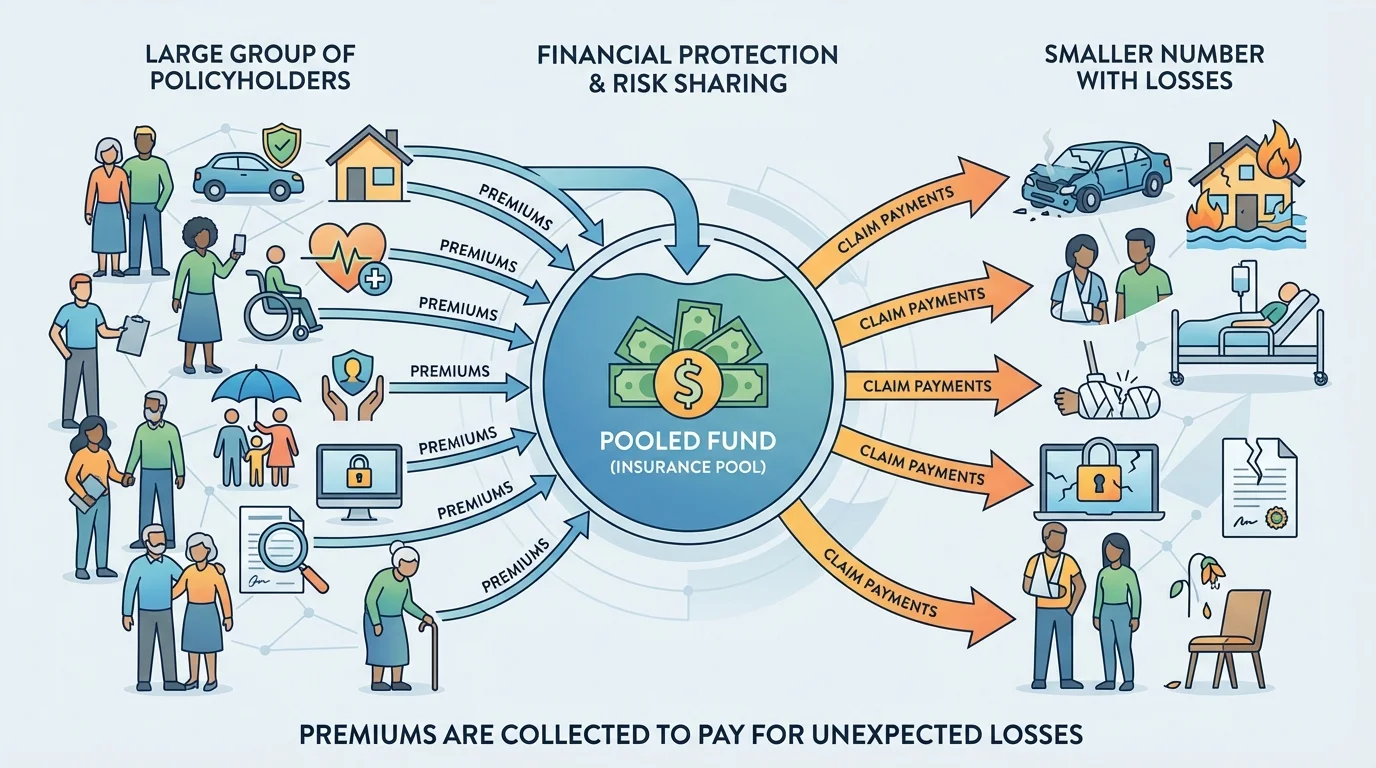

Insurance is a financial arrangement in which a person or business pays money to an insurer in exchange for protection against certain losses. Insurance exists because risk is part of life. A person might not know if a loss will happen, but they can prepare for the possibility that it might. Insurance works by spreading risk across many people, as [Figure 1] illustrates. Many policyholders pay smaller amounts, and the insurer uses that pooled money to help cover the much larger losses experienced by fewer people.

To understand insurance, several terms are essential. A premium is the amount paid for insurance, often monthly or yearly. A deductible is the amount the insured person must pay before the insurance company begins covering certain costs. A claim is a formal request for payment after a covered loss. A policy is the legal contract describing the coverage. A policy limit is the maximum amount an insurer will pay. An exclusion is something the policy does not cover.

Risk management is the process of identifying possible financial losses and choosing ways to reduce them. Insurance is one risk management strategy, but people also reduce risk by saving emergency funds, using safety measures, securing personal information, and avoiding dangerous behavior.

Insurance does not remove danger. It transfers part of the financial risk from the individual to the insurer. For example, if a teen driver causes an accident that leads to $20,000 in damages, a family without insurance could face a major financial crisis. With insurance, the family may still owe a deductible or uncovered amount, but the insurer can pay most of the covered cost up to the policy limits.

Not every risk should be insured. People usually buy insurance for losses that would be difficult or impossible to pay for on their own. Replacing a cracked phone screen might be annoying but manageable for some families. Paying for major surgery, rebuilding a house after a fire, or replacing years of lost income after a disabling injury is a very different situation.

Insurance products are designed for different kinds of risk. Some protect people from liability if they harm others. Some protect property if it is damaged or stolen. Others protect income when a person cannot work. The main categories students should know include automotive insurance, health insurance, disability insurance, long-term care insurance, life insurance, renters or homeowners insurance, identity theft protection, and professional liability insurance.

Each type answers a different question. Auto insurance asks, "What if a vehicle causes damage or is damaged?" Health insurance asks, "What if medical care becomes expensive?" Disability insurance asks, "What if a person cannot earn income?" Life insurance asks, "What happens to the people who depend on my income if I die?" Property insurance asks, "What if belongings or a home are damaged or stolen?" Identity theft protection asks, "What if someone misuses personal information?" Professional liability asks, "What if a person's work causes financial harm to a client or patient?"

| Insurance type | Main purpose | Typical risk covered |

|---|---|---|

| Automotive | Protects against vehicle-related losses and liability | Accidents, theft, vehicle damage, injury claims |

| Health | Helps pay medical costs | Doctor visits, hospital care, prescriptions, surgery |

| Disability | Replaces part of lost income | Illness or injury that prevents work |

| Long-term care | Helps pay for extended care services | Nursing care, assisted living, in-home care |

| Life | Provides money to beneficiaries after death | Loss of income to dependents |

| Renters/Homeowners | Protects property and liability related to a residence | Fire, theft, some disasters, lawsuits |

| Identity theft | Helps with recovery from identity fraud | Stolen personal data, fraudulent accounts |

| Professional liability | Protects workers from claims tied to professional mistakes | Negligence, errors, malpractice claims |

Table 1. Comparison of major insurance types and the risks they are designed to address.

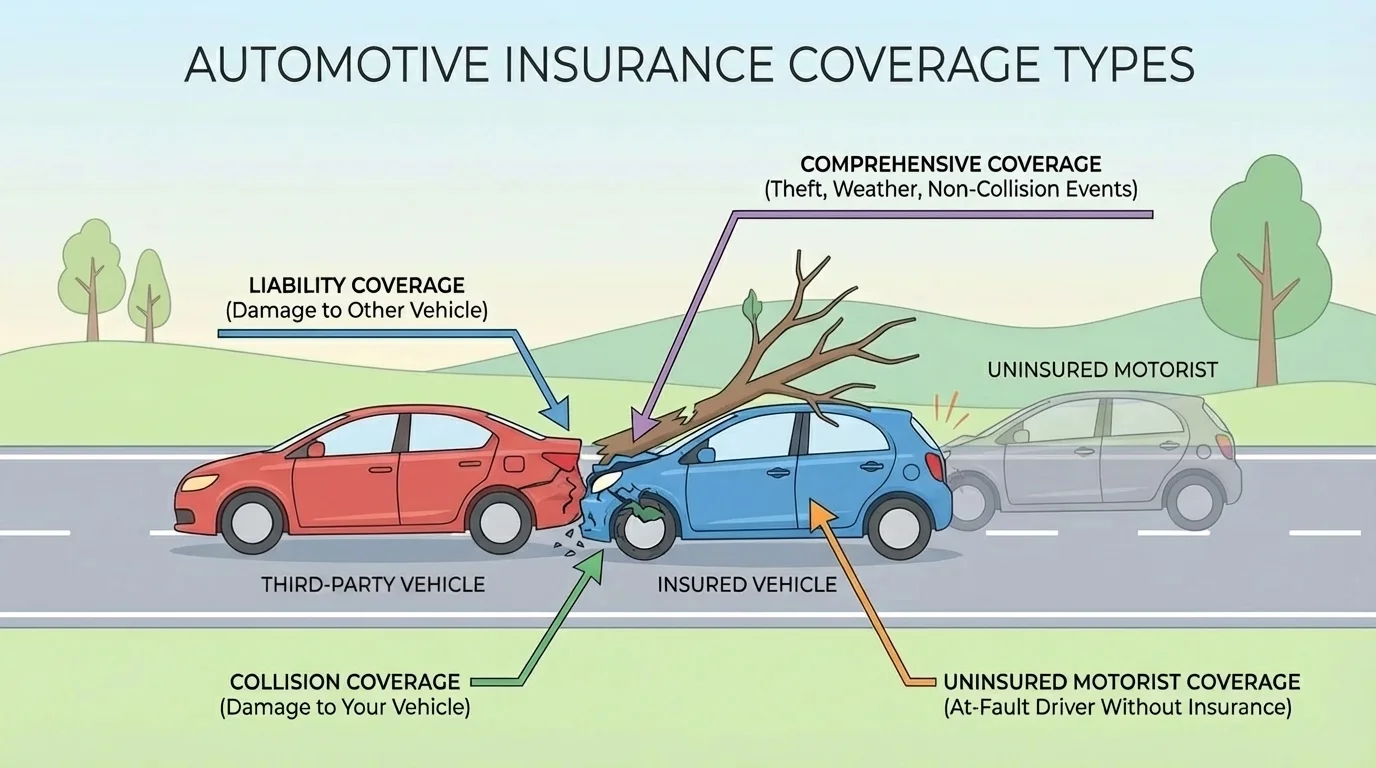

Automotive insurance is one of the most common forms of insurance, and it is especially important for teenagers because driving creates both safety and financial risk. A single auto policy may include several kinds of coverage, as shown in [Figure 2]. These parts are bundled together, but they do not all protect against the same losses.

Liability coverage pays for damage or injuries the driver causes to others. If a driver runs a red light and hits another car, liability insurance may pay for the other driver's repairs and medical bills. In many places, liability insurance is legally required because drivers can cause serious harm.

Collision coverage pays for damage to the insured driver's own car from a crash, regardless of fault in many situations. Comprehensive coverage covers non-collision losses such as theft, vandalism, hail, or hitting a deer. Uninsured or underinsured motorist coverage helps if the other driver has little or no insurance. Some policies also include medical payments or personal injury protection, often called PIP, which help cover medical costs for the insured driver and passengers.

The cost of auto insurance depends on factors such as age, driving record, type of car, location, and coverage amounts. Teen drivers often face higher premiums because insurers view them as higher risk. A higher deductible may lower the premium, but it also means the driver pays more out of pocket after an accident.

Auto insurance example

A driver backs into a pole and causes $3,000 in damage to their own car. Their collision deductible is $500.

Step 1: Identify the covered loss.

The damage is to the insured driver's own car after a collision, so collision coverage applies.

Step 2: Subtract the deductible from the repair cost.

The insurer's payment is the covered loss minus the deductible: \(3,000 - 500 = 2,500\).

Step 3: State who pays what.

The driver pays $500, and the insurer pays $2,500.

This example shows why the deductible matters even when a loss is covered.

Later, when comparing policies, the visual breakdown from [Figure 2] helps explain why a cheaper policy may not always be a better one. A low-cost policy might only include liability coverage and leave the car owner unprotected if their own vehicle is stolen or heavily damaged.

Health insurance helps pay for medical expenses, which can become extremely expensive very quickly. A broken leg, emergency room visit, appendix surgery, or treatment for a chronic illness can cost thousands or even tens of thousands of dollars. Health insurance spreads those costs over a large group instead of forcing one family to absorb the full bill alone.

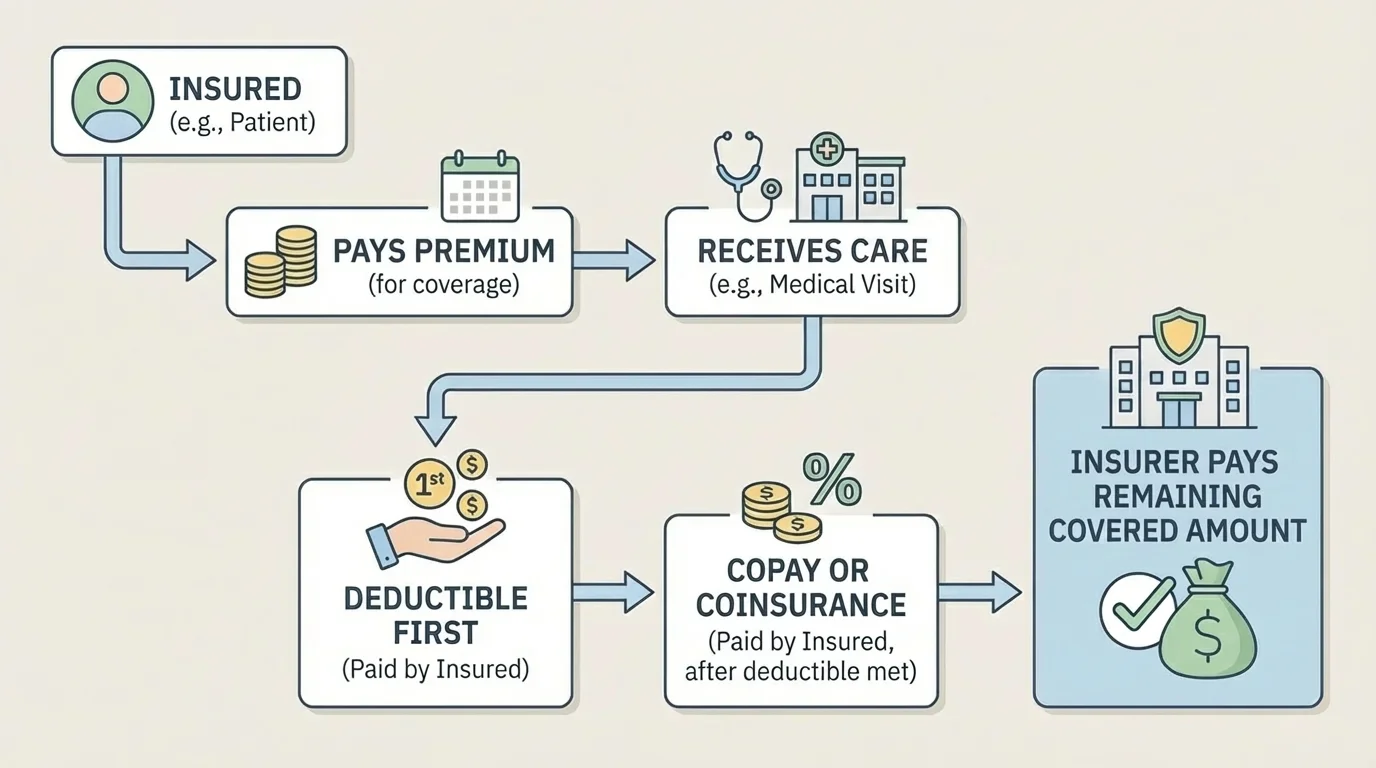

Health insurance often involves several layers of cost-sharing, as [Figure 3] shows. The insured person usually pays a premium to keep the policy active. Then, depending on the plan, the person may need to meet a deductible before the insurer pays much of the cost. After that, the person might pay a copay, which is a fixed fee, or coinsurance, which is a percentage of the bill.

For example, suppose a student's parent has a plan with a $1,000 deductible and then \(20\%\) coinsurance for covered services. If a covered medical procedure costs $6,000 and the deductible has not been met, the patient may pay the first $1,000 and then \(20\%\) of the remaining $5,000, which is \(0.20 \times 5,000 = 1,000\). In that case, the patient pays $2,000 and the insurer pays $4,000, assuming the provider is in-network and the service is covered.

Why networks matter

Many health plans have a network of doctors, clinics, and hospitals that agree to set prices. Going in-network usually costs less. Going out-of-network may mean much higher bills or no coverage at all, depending on the plan.

Health insurance is also important because medical problems often reduce income at the same time they increase expenses. Someone who is seriously ill may miss work while also facing large bills. This is one reason health insurance and disability insurance often work together as parts of a broader financial safety net.

The cost-sharing process in [Figure 3] shows why two plans with the same premium may still feel very different in real life. One plan may have a lower deductible and higher premium, while another has a lower premium but much higher out-of-pocket costs before coverage helps significantly.

Disability insurance protects a person's income if illness or injury prevents them from working. Many people focus on insuring cars and homes, but their future earnings may actually be their most valuable financial asset. A worker might earn hundreds of thousands or even millions of dollars over a lifetime, so losing the ability to work can be financially devastating.

There are two broad forms of disability insurance. Short-term disability insurance covers temporary periods when a person cannot work, often for weeks or months. Long-term disability insurance covers longer-lasting disabilities, sometimes for years or until retirement age. Policies usually replace only part of income, not all of it.

Long-term care insurance is different. It does not mainly replace wages. Instead, it helps pay for services people may need if they cannot perform everyday activities independently because of age, illness, or disability. These services may include home health aides, assisted living, or nursing home care.

Many people assume health insurance automatically pays for all long-term assistance needs. In reality, health insurance often covers medical treatment but not extended custodial care, which is why long-term care insurance exists.

Consider the difference: if an injured person cannot work for six months, disability insurance may replace part of their paycheck. If an elderly person needs help bathing, dressing, and eating every day for years, long-term care insurance may help pay for that support. The risks are related, but the purpose of each product is different.

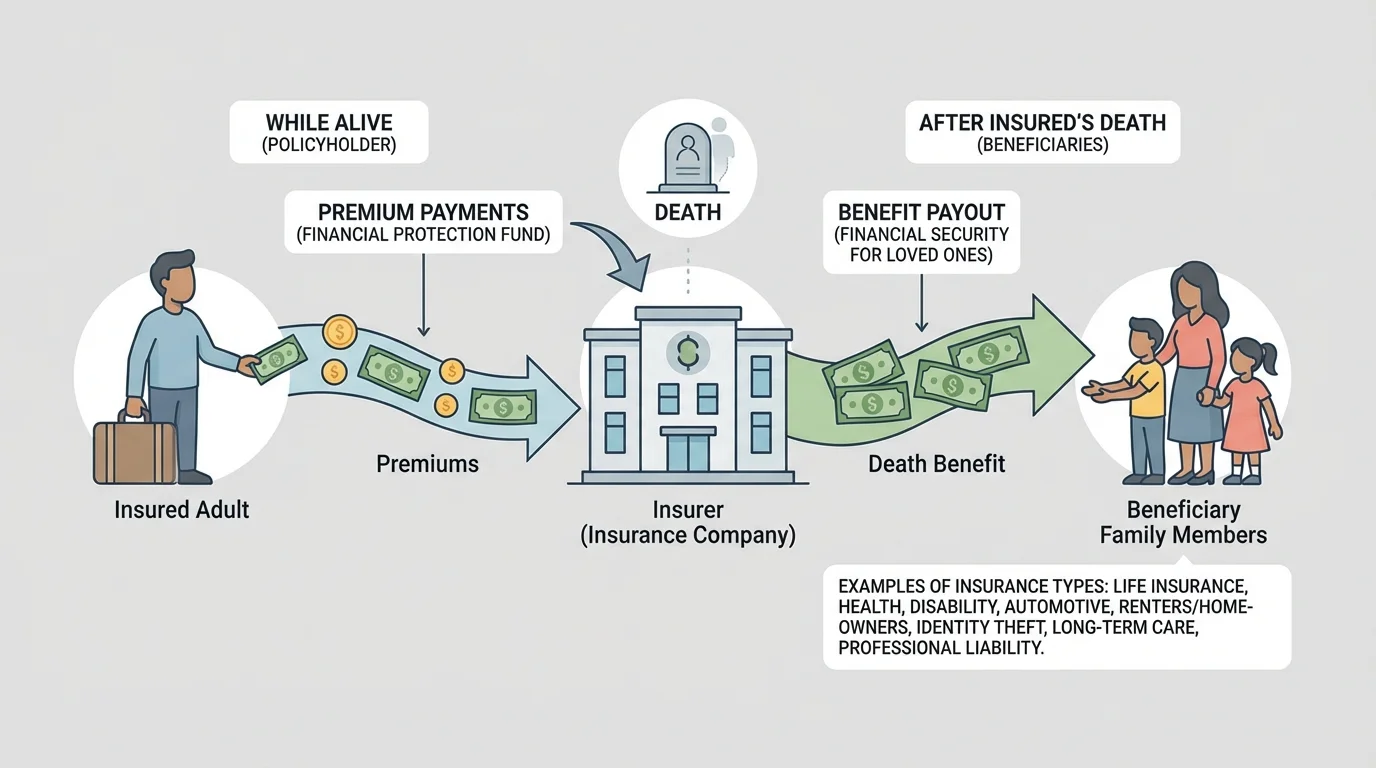

Life insurance is designed to provide money to selected people after the insured person dies. The people who receive the money are called beneficiaries. Life insurance matters most when others rely on someone's income, as [Figure 4] shows. For example, if a parent dies unexpectedly, life insurance can help surviving family members pay for housing, food, childcare, education, or debt.

Two common forms are term life insurance and whole life insurance. Term life insurance lasts for a specific period, such as 10, 20, or 30 years. It is usually simpler and less expensive. Whole life insurance lasts for a person's lifetime as long as premiums are paid and may build cash value, but it is usually more expensive and more complex.

Life insurance is usually less urgent for teenagers because most teens do not have dependents. However, understanding its purpose is important. The key question is not "Will everyone die eventually?" The key question is "Would someone face serious financial hardship if this person died?" If the answer is yes, life insurance may be necessary.

Life insurance case study

A household depends on one parent who earns $50,000 per year. That parent dies unexpectedly.

Step 1: Identify the financial problem.

The family loses an important source of income, but housing, food, and other bills still continue.

Step 2: Identify the purpose of insurance.

A life insurance benefit can provide money to cover immediate expenses and support the family while they adjust financially.

Step 3: Connect the insurance to risk management.

Life insurance does not remove emotional loss, but it reduces the financial shock created by the death.

This is why life insurance is often described as income protection for dependents.

The flow of protection shown in [Figure 4] makes an important point: life insurance primarily protects the people left behind, not the person who has died.

Renters insurance protects a tenant's personal belongings and often includes liability coverage if someone is injured in the rented space. Many students assume a landlord's insurance covers everything in an apartment building, but the landlord's policy generally protects the building itself, not the renter's clothes, laptop, furniture, or bicycle.

Homeowners insurance covers the house structure, personal property, and liability, subject to the policy's rules. It often protects against fire, theft, wind damage, and some other hazards, but it may exclude certain events such as floods or earthquakes unless separate coverage is purchased. This is a strong reminder that reading exclusions matters.

Identity theft happens when someone uses another person's personal information without permission, often to open accounts, make purchases, file false tax returns, or commit other fraud. Identity theft protection services may monitor credit reports, alert customers to suspicious activity, and provide help restoring accounts and records. Some plans also reimburse certain recovery-related costs, though the exact protection varies.

Digital security habits are part of risk management too. Strong passwords, two-factor authentication, careful sharing of personal data, and checking account statements regularly can reduce the chance that identity theft will happen in the first place.

For a teenager, identity theft may sound like an adult problem, but it can affect anyone with a Social Security number, bank account, mobile payment app, or online shopping account. Young people can be targets because they may not check credit activity often, giving thieves more time before the fraud is discovered.

Professional liability insurance protects workers whose professional advice, decisions, or services could financially harm a client or patient if a mistake is made. Doctors may carry malpractice insurance. Lawyers, accountants, architects, and consultants may carry similar protection. It is often called errors and omissions insurance in some professions.

This type of insurance differs from ordinary liability coverage. If a doctor leaves a patient with an injury because of negligent care, the claim is tied to professional skill and judgment. If a visitor slips on a wet floor in the office lobby, that is more likely a general liability issue. The details vary by job, but the core idea is the same: some careers create risks that ordinary personal insurance does not cover.

Professional liability example

An accountant gives incorrect tax advice to a client, and the client faces large penalties.

Step 1: Identify the source of harm.

The harm comes from professional advice, not from physical damage to property.

Step 2: Match the risk to the insurance type.

This is the kind of risk professional liability insurance is designed to address.

Step 3: Explain why it matters.

Without this insurance, the professional might have to pay legal costs or damages personally.

As students move toward careers, they should understand that insurance needs can change with occupation.

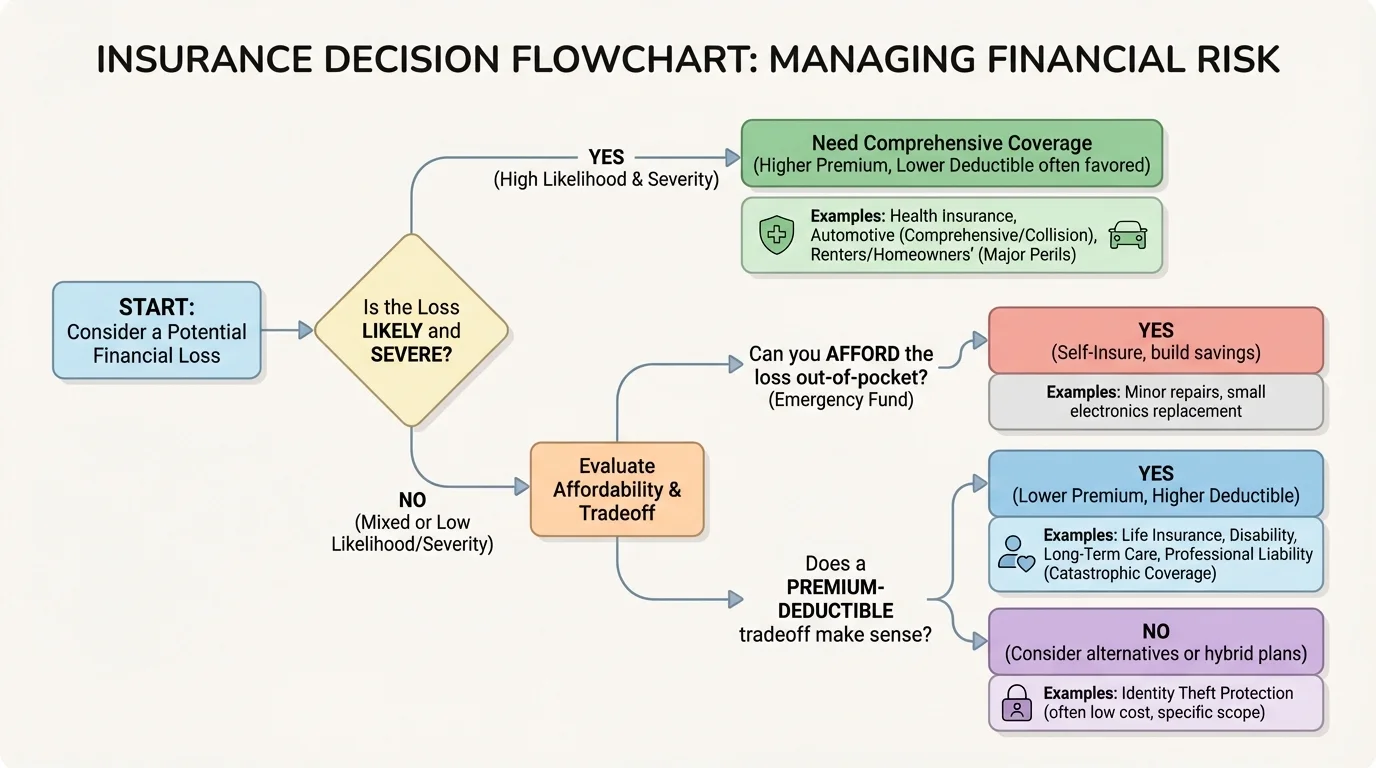

Good insurance choices come from matching coverage to risk, not from buying every product or choosing the cheapest option automatically. A smart strategy asks two main questions: How likely is the loss? and How severe would the financial damage be? This decision process becomes clearer in [Figure 5], which compares the probability of loss with the size of the possible cost.

Insurance is especially useful for losses that are not very predictable for one person but are extremely expensive when they happen. Most people do not know whether they will have a major car crash, need emergency surgery, become disabled, or lose a home in a fire. They buy insurance because paying a known premium is safer than facing a huge uncertain bill alone.

People should compare more than just premium cost. They should also examine deductibles, policy limits, exclusions, networks, waiting periods, and whether replacement cost or actual cash value applies. For example, replacing a three-year-old laptop under one policy might result in a payment based on its depreciated value, while another policy might cover the cost of a new comparable item.

A useful rule is this: if paying for the loss out of pocket would seriously damage your finances, insurance deserves strong consideration. If the loss would be small and manageable, self-insuring through savings may be more efficient. The decision tree in [Figure 5] shows why both likelihood and severity matter; high-cost losses are usually more important to insure than minor, routine expenses.

One common mistake is being underinsured, which means the coverage is too small for the actual risk. A person may choose minimum auto liability limits to save money, only to discover after a serious crash that the policy does not cover all the damages. Another mistake is ignoring exclusions and assuming a policy covers every possible event.

Another problem is failing to document property. After theft or a fire, it is much easier to file a claim if the person has photos, receipts, serial numbers, or an inventory of belongings. People also make mistakes when they do not update their insurance after major life changes such as moving, buying a car, getting married, having children, or starting a business.

Fraud is another issue. Insurance fraud raises costs for everyone. At the same time, consumers should watch for scams, fake insurers, or misleading offers. Reading the policy carefully, asking questions, and working with reputable companies are basic but powerful habits.

"Insurance is not meant to make people rich after a loss; it is meant to make devastating losses manageable."

Understanding insurance products helps people make responsible choices long before a crisis happens. The most effective risk management plan combines prevention, savings, and the right insurance coverage for the risks that could cause the greatest financial harm.