A single bad financial decision can cost more than a new phone, a month of groceries, or even a month of pay. A fake text from a "bank," a misleading insurance ad, or an outdated article about medical costs can push someone into losing money, buying the wrong protection, or sharing personal information with a scammer. In everyday life, people constantly face financial information, but not all of it deserves trust.

When people choose how to protect themselves from lost income, damaged property, health expenses, or identity fraud, they depend on information. That information might come from an insurance company, a bank app, a social media influencer, a news story, a government website, or a friend. Some of it is helpful. Some of it is incomplete. Some of it is designed to persuade rather than inform.

Good financial decisions require three tests: relevance, credibility, and accuracy. A source may be true but not useful for your situation. A source may be useful but biased. A source may sound professional but include outdated or incorrect facts. Strong decision-making means checking all three.

Relevance means information directly relates to the decision you are making. Credibility means a source is trustworthy because it has expertise, transparency, and reliable evidence. Accuracy means the information is factually correct, precise, and up to date.

These ideas matter especially in personal financial literacy because risk management depends on informed choices. If someone misunderstands a deductible, ignores a policy exclusion, or trusts a fake fraud alert, the consequences can be expensive and stressful.

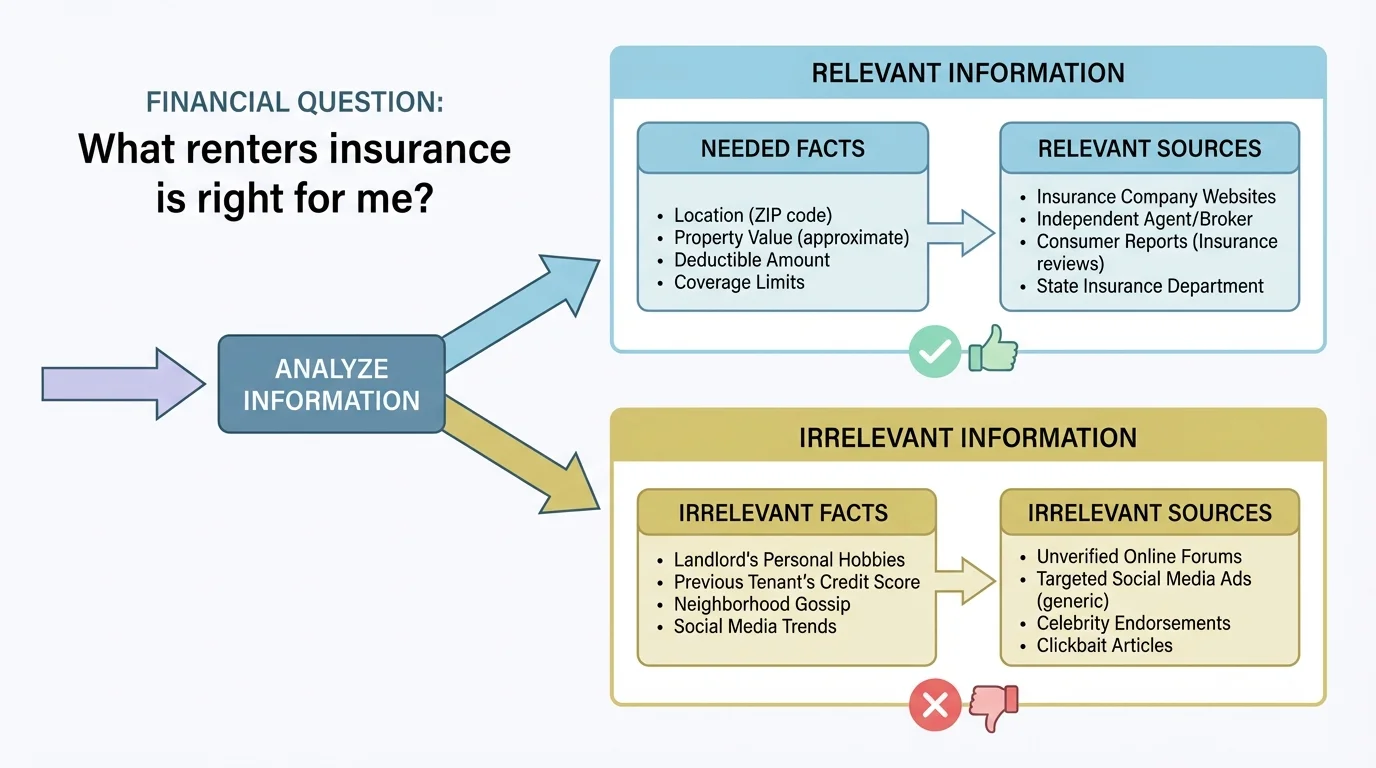

Before asking whether a source is trustworthy, ask whether it actually answers your question. A financial decision starts by matching the problem to the information needed, as shown in a simple decision filter. If you want to compare renters insurance, an article about car repair costs may be interesting, but it is not relevant. If you are deciding whether to freeze your credit after identity theft, a general savings tip video is not enough.

[Figure 1] Relevance depends on purpose, timing, and personal situation. A grade 11 student with a part-time job may need information about direct deposit security, debit card fraud, and emergency savings. A family choosing health insurance may need different information, such as premium costs, network restrictions, and out-of-pocket maximums. The same source can be relevant to one person and not to another.

To judge relevance, ask questions such as: What decision am I making? What facts do I need? Is this source about my age group, income level, location, and type of risk? Does it discuss the specific product or issue I am facing?

Suppose Maya is moving into her first apartment for college and wants to protect her laptop, clothes, and bike. A blog post about homeownership insurance is not the best match because homeowners and renters face different risks. A renters insurance guide from a state insurance department is more relevant because it addresses the exact product she is considering.

Relevance also includes scale. If a source discusses average hospital bills across the nation, that may not help much unless it connects to the insurance network in your area. Likewise, identity theft advice from ten years ago may not cover modern threats such as app-based scams or data breaches tied to online accounts.

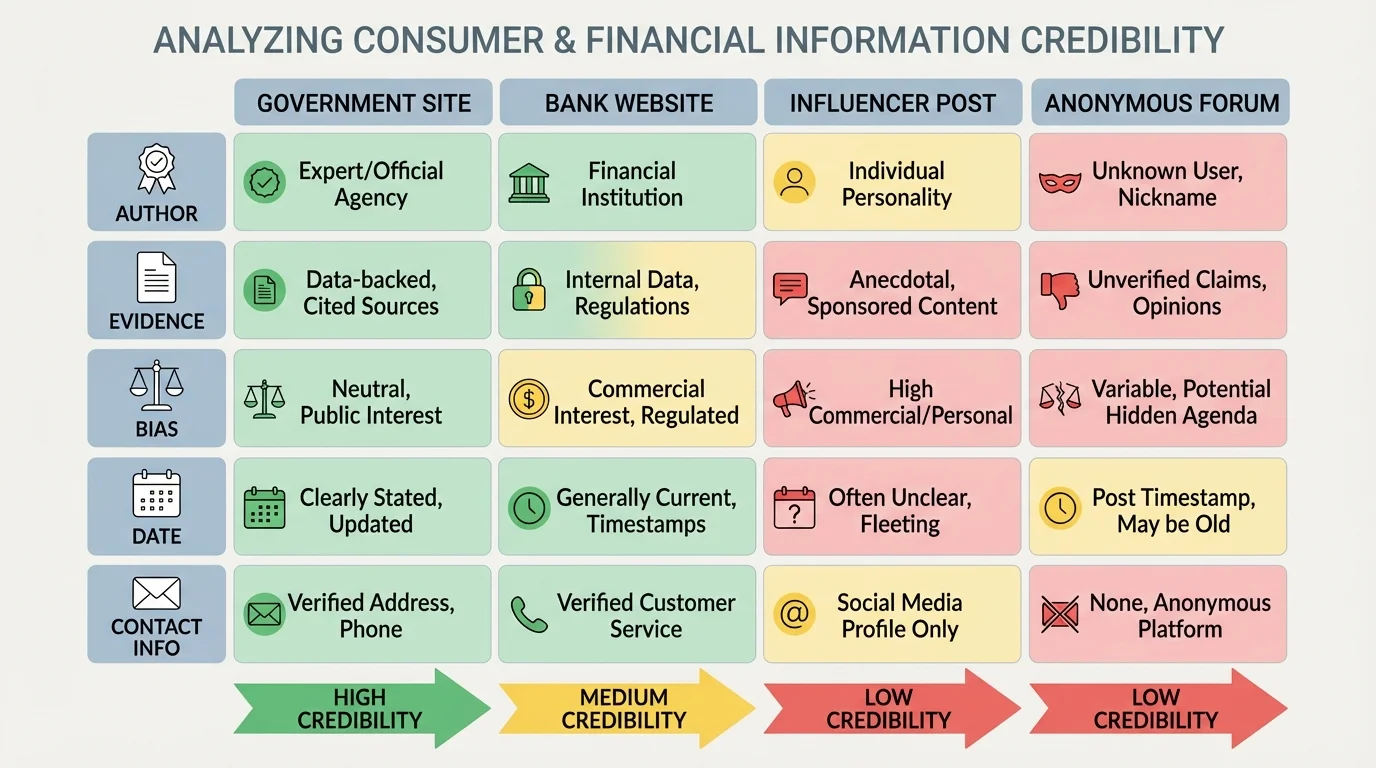

Once information is relevant, the next question is whether the source deserves trust. Trustworthy sources usually show expertise, explain where their information comes from, and clearly separate facts from opinions, as [Figure 2] illustrates through source comparison. A state insurance regulator, a federal consumer protection agency, or a bank's official fraud center often provides more reliable guidance than an anonymous social media account.

Credibility does not mean a source is perfect. It means the source has good reasons to be believed. A credible source often includes the author's name, qualifications, date of publication, cited evidence, and contact information. It also avoids exaggerated promises such as "guaranteed wealth," "zero risk," or "free money."

Bias is an important part of credibility. A company selling insurance has useful information about its own products, but it also has an incentive to persuade customers to buy. That does not automatically make the company dishonest. It does mean students should read carefully, compare multiple sources, and pay attention to what is emphasized or omitted.

Watch for these credibility signals: expert authors, official institutions, transparent methods, current publication dates, references to laws or regulations, and balanced explanations of benefits and limitations. Watch for these warning signs: no author, no date, emotional language, pressure to act immediately, hidden sponsorship, and claims without evidence.

Consider four sources about preventing identity theft: a Federal Trade Commission page, a bank's official website, a finance influencer's short video, and an anonymous online comment thread. The government page is often strongest on public guidance and legal rights. The bank page may be helpful for account-specific security features. The influencer video may be engaging but could simplify too much or be sponsored. The anonymous thread may include personal stories, but those stories are not enough to establish reliability.

Later, when comparing scam warnings, the same credibility test still applies. Just as [Figure 2] compares source quality, students should ask who benefits from a claim and what evidence supports it.

Many financial scams work not because the fake message looks perfect, but because it creates panic. When people feel rushed, they are less likely to question the source.

Credibility can also be strengthened by agreement across multiple independent sources. If a medical billing rule, insurance term, or fraud alert appears in several reliable places, confidence increases. If only one dramatic source makes the claim, caution should increase.

Accuracy is about correctness. Even a credible source can contain mistakes, and even relevant information can become outdated. Financial rules, prices, coverage limits, and fraud tactics change over time. A trustworthy student checks whether the information is current and exact.

Start by checking dates. A report on credit card fraud from several years ago may not reflect current protections or current scam methods. Then check specific numbers and wording. If one health plan says the deductible is $1,500 and another source says it is $1,000, that difference matters. If a website says "coverage available" but the policy document lists several exclusions, the exact language in the official document matters more.

Accuracy also involves understanding what numbers mean. For example, a low monthly insurance premium may sound attractive, but it may come with a high deductible. If a plan costs $18 per month, the yearly premium is calculated as \(12 \times 18 = 216\), so the annual cost is $216 before any claim is made. If the deductible is $1,000, the customer may still pay a large amount out of pocket before insurance starts covering losses.

Precision matters in loans as well. A loan ad may highlight one number while downplaying another. The APR, or annual percentage rate, includes interest and certain fees, so it usually gives a clearer picture of borrowing cost than interest rate alone. If one lender offers a lower interest rate but much higher fees, the cheaper-looking offer may not actually be cheaper.

Checking a financial claim

A phone plan ad says, "Device protection for only $12 a month." A student wants to know the yearly cost and whether that amount is worth it.

Step 1: Convert the monthly cost to a yearly cost.

Use \(12 \times 12 = 144\). The yearly cost is $144.

Step 2: Compare that cost with the item being protected.

If the phone would cost $300 to replace, paying $144 each year may or may not be worthwhile depending on the deductible, exclusions, and likelihood of damage.

Step 3: Check the exact terms.

If the policy has a $99 deductible and excludes water damage, the offer may protect less than the ad suggests.

The claim is not fully evaluated until the numbers and conditions are both checked.

Cross-checking improves accuracy. Compare an advertisement to an official disclosure form. Compare a news article to the original government report. Compare a quoted fee to the actual account agreement. Accuracy grows stronger when facts match across documents.

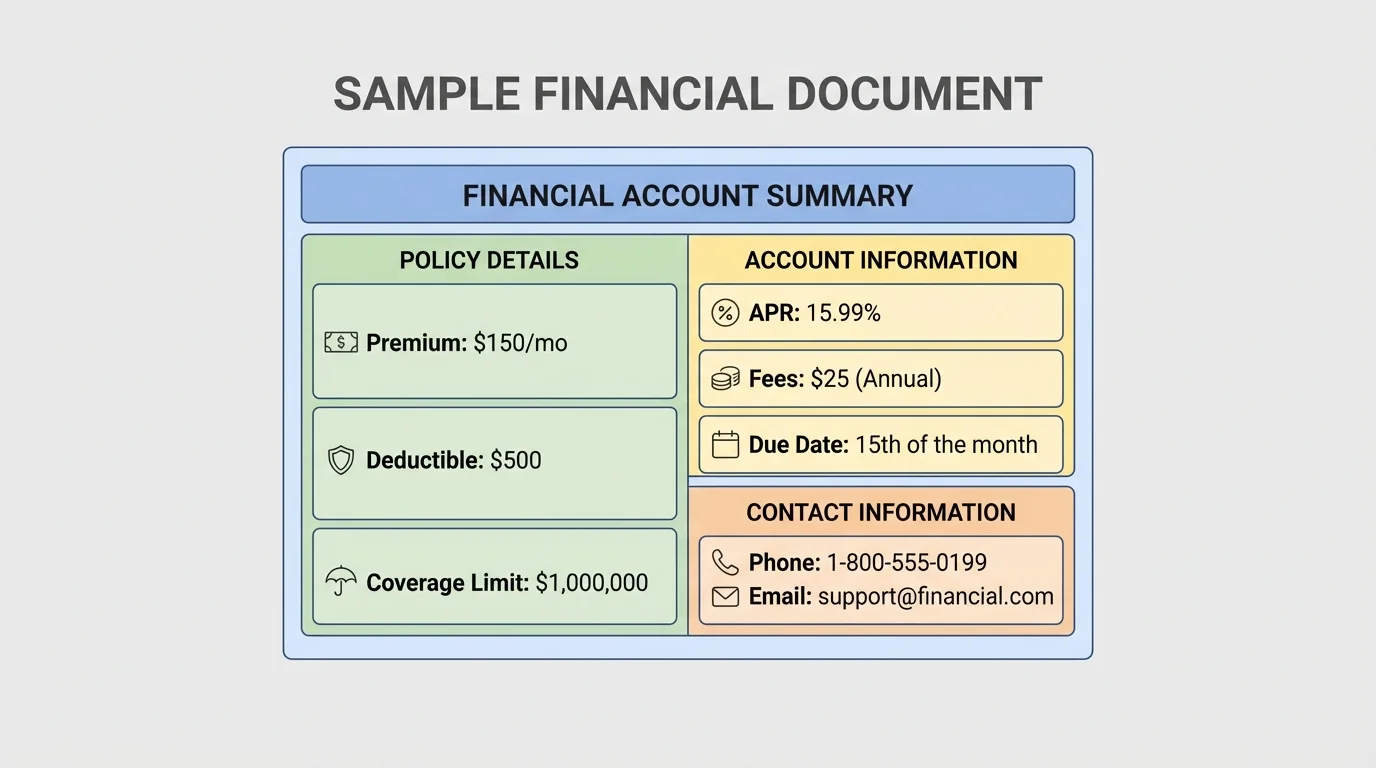

Financial documents often look complicated because they are dense, formal, and full of specialized terms. But they become much easier to interpret when you know where key information appears, as shown on a sample document layout. Important consumer documents include bank statements, insurance declarations pages, Explanation of Benefits (EOB) forms, credit reports, billing statements, and loan disclosures.

[Figure 3] Students should learn to search for key parts: who issued the document, date, due date, amount owed, coverage limit, deductible, premium, exclusions, contact information, and dispute instructions. In financial literacy, reading carefully is a protective skill. Missing a due date can trigger fees. Missing an exclusion can lead to denied coverage. Missing a fraud notice can delay a response to identity theft.

For insurance, one of the most important distinctions is between premium and deductible. The premium is the amount paid for the policy, often monthly or yearly. The deductible is the amount the policyholder pays before insurance coverage begins for a claim.

Suppose a renters insurance policy has a $240 annual premium and a $500 deductible. If a stolen laptop leads to a covered claim of $1,200, the student pays the first $500 and the insurer may cover the remaining $700, depending on the policy terms. The lower premium is not always the better choice if it comes with much weaker coverage.

Medical and health-related documents also require careful analysis. A bill is not always the same as an explanation of benefits. An explanation of benefits often shows what a provider charged, what the insurer allowed, what the insurer paid, and what the patient may owe. Students should not assume every mailed amount is final without checking whether it is a bill, a notice, or a summary statement.

| Document type | Key questions to ask | Why it matters |

|---|---|---|

| Bank statement | Do I recognize every transaction? Are there fees? | Helps catch fraud and account errors quickly. |

| Insurance policy | What is covered? What is excluded? What is the deductible? | Prevents false assumptions about protection. |

| Loan disclosure | What is the APR? What are the fees? When are payments due? | Shows the real cost of borrowing. |

| Medical notice | Is this a bill or an explanation of benefits? What amount is my responsibility? | Avoids overpaying or ignoring a real charge. |

| Credit report | Are the accounts mine? Are there errors or signs of identity theft? | Protects credit history and personal identity. |

Table 1. Common consumer and financial documents and the questions students should ask when reviewing them.

When students later compare scams and official notices, the labeled features from [Figure 3] still matter: legitimate documents usually identify the issuer clearly, use consistent account information, and explain next steps without hiding basic details.

Analyzing financial information is not just an academic skill. It directly affects risk management. People use financial products to reduce the impact of losses that might otherwise be overwhelming. These losses can involve income, property, health, or identity.

An emergency fund helps with small or medium unexpected costs. Insurance helps with larger losses that would be hard to cover alone. Fraud monitoring, strong passwords, two-factor authentication, and careful review of accounts reduce identity-related risk. The right mix depends on age, income, responsibilities, and what a person owns.

For example, someone with a car may compare liability coverage, collision coverage, and deductibles. A student living in an apartment may decide renters insurance is relevant because replacing electronics, clothing, and textbooks would be expensive. A worker who depends on regular wages may consider how lost income from illness or injury could affect rent, food, and transportation.

Risk management as decision-making under uncertainty means preparing for events that may or may not happen but could cause serious financial harm if they do. Good risk management does not eliminate all risk. Instead, it asks which risks can be reduced, shared, insured, or planned for in advance.

Comparing options often means weighing cost against protection. If Plan A costs $20 per month with a $250 deductible and Plan B costs $12 per month with a $1,000 deductible, the cheaper monthly choice may expose the customer to much higher out-of-pocket costs after a loss. Students should compare the total structure of the offer, not just the first number they see.

Comparing two protection plans

A student compares two laptop protection options.

Step 1: Find the annual premium for each plan.

Plan A: \(12 \times 20 = 240\), so the annual cost is $240.

Plan B: \(12 \times 12 = 144\), so the annual cost is $144.

Step 2: Compare deductibles.

Plan A has a $250 deductible. Plan B has a $1,000 deductible.

Step 3: Consider a covered loss of $1,200.

Under Plan A, the student pays $250 first, and insurance may cover the remaining $950.

Under Plan B, the student pays $1,000 first, and insurance may cover only the remaining $200.

The lower monthly price does not automatically mean better financial protection.

This kind of comparison matters for health plans, auto coverage, and other protections. The best choice depends on what losses a person can realistically absorb and what losses would be financially devastating.

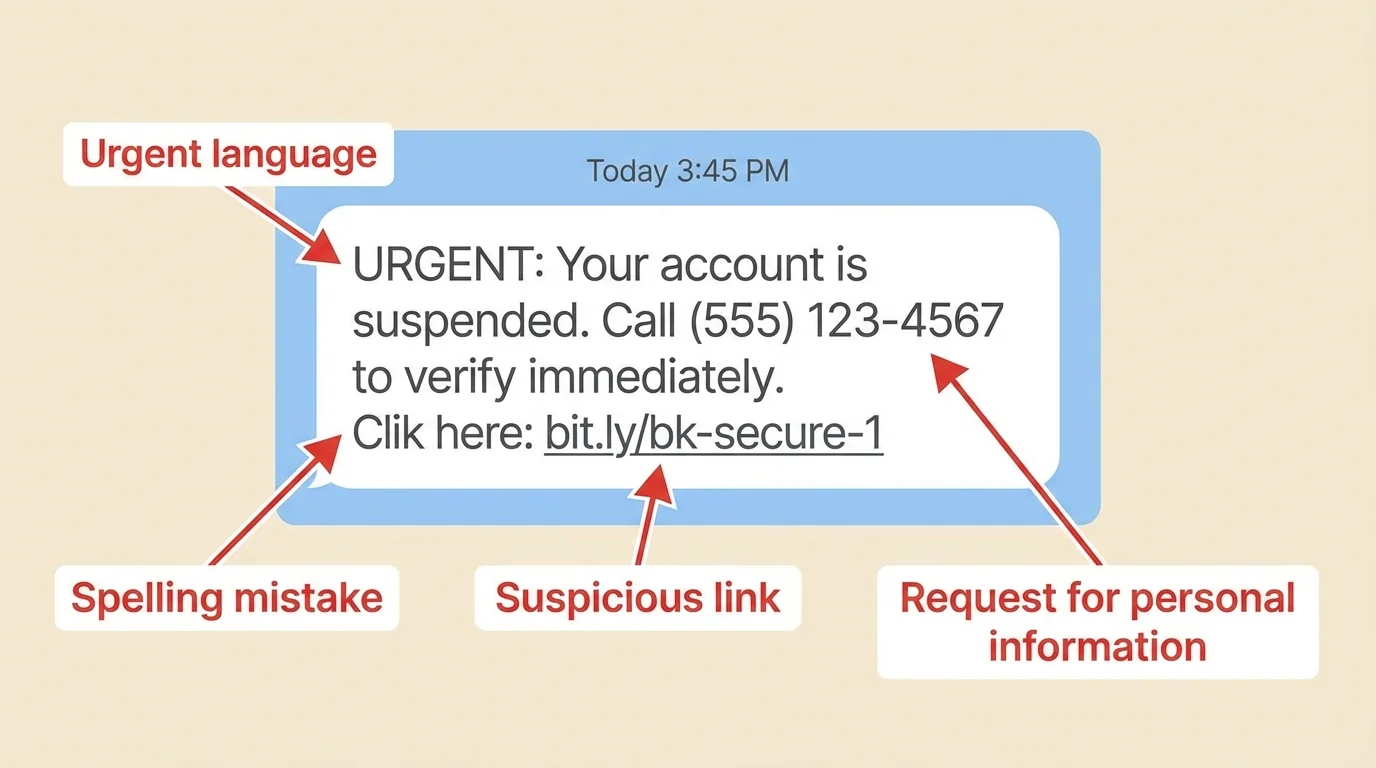

Fraudsters understand psychology. They know people react quickly to fear, urgency, and authority. Scam messages often combine these pressures with requests for personal information, as a fake alert demonstrates. A text may claim your account is locked. An email may say your refund is waiting. A caller may pretend to be from a bank, delivery company, or government agency.

[Figure 4] Common red flags include urgent deadlines, threats, strange links, spelling errors, requests for passwords or full Social Security numbers, and instructions to pay with gift cards, wire transfers, or cryptocurrency. Real institutions sometimes send urgent alerts, but they do not usually ask customers to verify sensitive information through random links in a text message.

Scam detection depends on relevance, credibility, and accuracy all at once. Is this message relevant to an account you actually have? Is it from a credible sender using an official channel? Is the information accurate when checked against your account app or the company's real website?

For example, if a student receives a text saying, "Your bank account will be frozen in \(24\) hours, click now," the student should not click. Instead, they should open the official banking app or call the number on the back of the bank card. The urgency shown in [Figure 4] is a warning sign, not proof that the message is legitimate.

Identity theft can also appear through unfamiliar charges, accounts you never opened, sudden drops in credit score, or bills for services you never used. Reviewing statements and reports regularly is one of the simplest defenses.

When students face a financial claim, ad, or document, they can use a short review process. First, identify the decision. Second, collect relevant sources. Third, test credibility. Fourth, verify accuracy. Fifth, compare options before acting.

One way to remember the process is to ask: What is the claim? Who is making it? What evidence is given? What details are missing? What does the official document say? What are the costs, risks, and protections?

This process works for many situations: deciding whether a warranty is worth buying, checking whether a "limited-time offer" is actually a good deal, comparing insurance plans, reading a billing notice, or responding to a possible fraud alert.

Earlier financial literacy skills still matter here: budgeting helps students know what losses they could pay themselves, saving helps them build an emergency cushion, and understanding opportunity cost helps them compare protection choices.

The strongest decisions usually come from slowing down. Fast choices are useful in sports, but in finance, speed often benefits the seller or the scammer more than the consumer.

Not all sources play the same role. Some provide official rules, some provide product details, and some provide personal experiences. Smart consumers know how to combine them without confusing them.

| Source type | Best use | Main limitation |

|---|---|---|

| Government agency | Rules, rights, warnings, consumer protection guidance | May not compare every private product in detail |

| Company website | Specific product terms and account services | May emphasize selling points |

| News report | Recent events and broad trends | May simplify complex details |

| Nonprofit consumer group | Independent education and comparison help | Quality varies by organization |

| Social media creator | Accessible explanations and examples | Possible sponsorship, oversimplification, or lack of expertise |

| Friend or family member | Personal experience | Experience may not apply to your situation |

Table 2. Different source types, what they are useful for, and the limits students should recognize.

Suppose two websites disagree about whether renters insurance covers a stolen bicycle. The best response is not to guess. Check the actual policy language, especially coverage limits, exclusions, and whether the item is covered away from home. Personal stories may help raise questions, but the contract decides the claim.

"Trust, but verify."

— A principle of careful decision-making

That principle captures the goal of consumer financial analysis. People do not need to become suspicious of everything. They need to become skilled at checking what matters before committing money, signing an agreement, or sharing private information.