Every day, people trade things without always thinking about it as economics. When a family buys bread, when a parent goes to work, or when someone puts money into a bank account, they are taking part in a market. A market is any place or system where buyers and sellers come together to exchange goods, services, labor, or money. Markets can be physical places, like a farmers market, or digital places, like an online store or banking app.

In economics, people and businesses can switch roles depending on the market. In one situation, a person may be a buyer. In another, the same person may be a seller. For example, when you buy a notebook, you are a buyer in a product market. If you mow a neighbor's lawn for money, you are acting as a seller of labor in a labor market. If you place savings in a bank account, you are supplying money in a financial market.

These ideas help explain how consumers and businesses work together. Consumers are people who buy goods and services for their own use. Businesses are organizations that produce or sell goods and services. Both are important because neither side can function alone. Buyers want products, jobs, and places to save or borrow money. Sellers want customers, workers, and financial support.

Product market is a market where goods and services are bought and sold.

Labor market is a market where workers offer their skills and time to employers in exchange for wages.

Financial market is a system in which money is saved, borrowed, invested, and lent.

To understand these markets clearly, it helps to ask the same two questions each time: Who is buying? and Who is selling? The answer changes depending on the market.

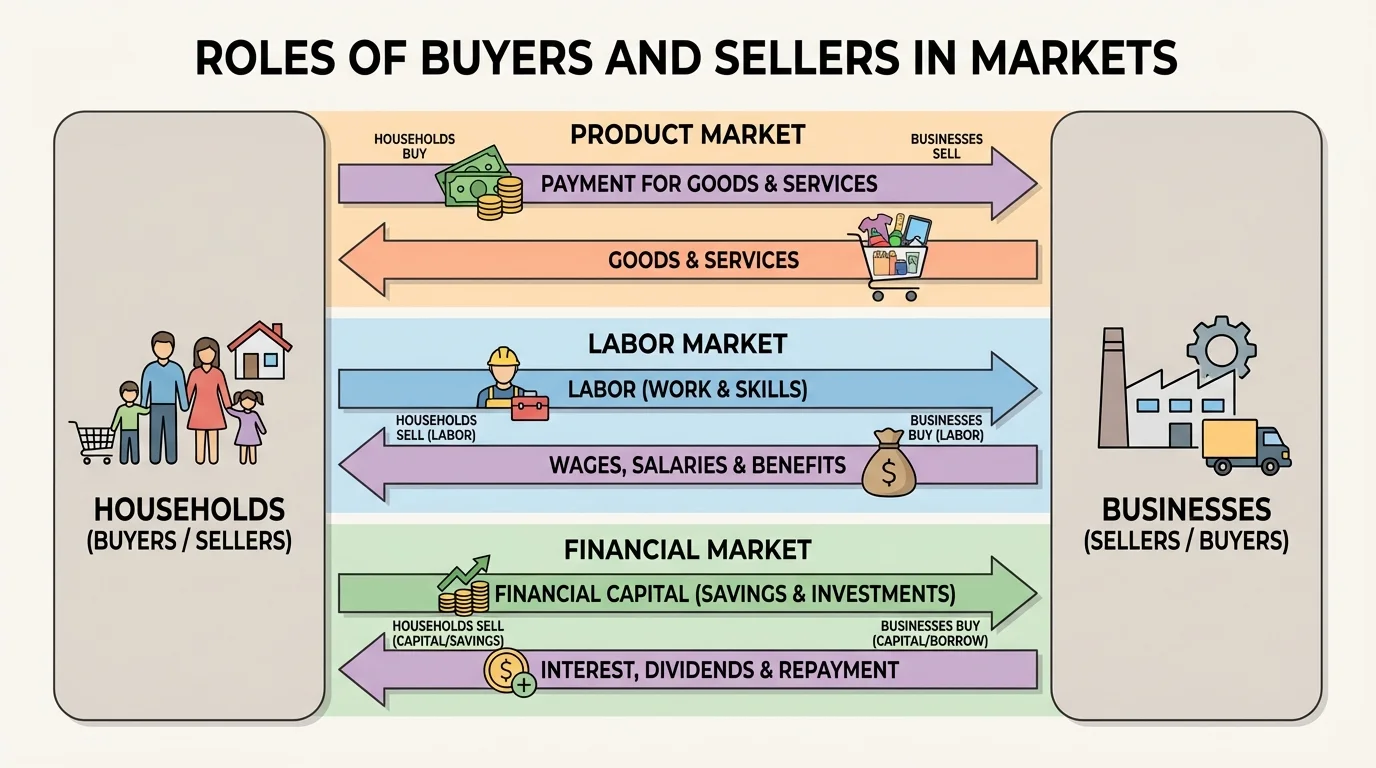

In a product market, buyers are usually consumers and sellers are usually businesses. [Figure 1] shows this exchange clearly: goods move to households, and money moves to businesses. A student buying a snack at a corner store, a family paying for a bus ride, or a person ordering shoes online are all examples of buyers in product markets. The business sells the good or service, and the buyer pays money to receive it.

Product markets include many kinds of sellers. Some are very small, such as a local bakery in Jamaica or a street vendor in Mexico City. Others are huge companies, such as car manufacturers in the United States or online retailers serving customers across Canada and Brazil. No matter the size, the seller's role is to offer something people want to buy.

Buyers in product markets make choices. They compare price, quality, location, and even brand reputation. If one store sells a backpack for $20 and another sells a similar one for $25, many buyers may choose the lower-priced option. Sellers pay attention to those choices because they want to attract more customers.

Businesses also act as buyers in product markets. A restaurant buys vegetables, bread, tables, and cleaning supplies. A clothing company buys fabric and sewing machines. In those cases, another business may be the seller. This is why product markets include both consumer purchases and business-to-business purchases.

Services are part of product markets too. Haircuts, streaming subscriptions, medical checkups, and phone repair are not physical objects, but they are still products in an economic sense because they are sold to buyers.

Example: A grocery store in a product market

Step 1: A grocery store offers apples for sale.

Step 2: A shopper decides the apples are worth the price and buys them.

Step 3: The shopper receives the apples, and the store receives money.

The shopper is the buyer, and the grocery store is the seller.

In many countries of the Western Hemisphere, product markets connect local life to global trade. A store in the United States may sell bananas grown in Central America. A family in Chile may buy electronics assembled in Mexico. A shop in Canada may sell coffee from Colombia. Product markets connect regions, producers, transport workers, and consumers.

A market does not work well unless buyers and sellers can respond to information. One of the most important signals is price. A price tells buyers how much they must give up to get a good or service. It also tells sellers how much money they may earn.

If many people want a product, businesses may try to produce more of it. If almost no one wants it, sellers may lower the price or stop offering it. This relationship is tied to two major ideas: supply and demand. Supply is the amount sellers are willing and able to offer. Demand is the amount buyers are willing and able to purchase.

How prices send signals

When demand rises, sellers notice that more people want the product. That may encourage businesses to make or sell more. When supply rises, buyers often have more choices, and prices may stay the same or fall. Prices help coordinate decisions even when millions of people are involved.

Competition matters too. If many sellers offer similar products, buyers often benefit because businesses work harder to lower prices or improve quality. But if there are very few sellers, buyers may have fewer options.

Think about bottled water after a big sports event. If many people want water at once, the seller may quickly run low. That shortage tells the seller to restock more next time. Buyers and sellers constantly react to one another through prices and choices.

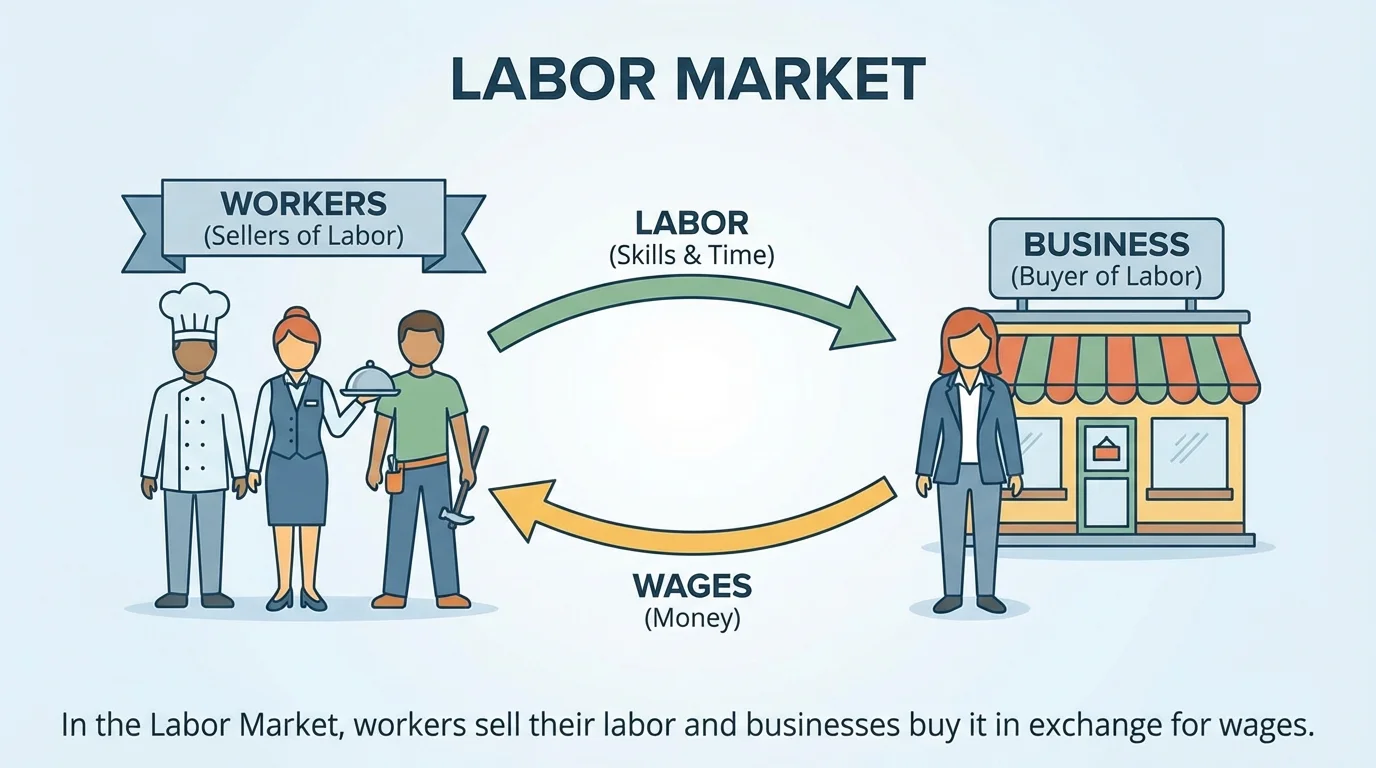

The labor market may feel different at first, but it follows the same basic idea of exchange. [Figure 2] shows that labor moves from workers to businesses, and wages move from businesses to workers. In this market, workers are the sellers because they sell their time, effort, and skills. Employers are the buyers because they pay to use that labor.

This can seem backwards because businesses are often sellers in product markets. But in labor markets, the business is buying something: labor. A worker may sell cooking skills to a restaurant, repair skills to a garage, or teaching skills to a school.

The payment workers receive is called a wage. Wages can be paid by the hour, by salary, or sometimes by the job. If a worker earns $15 per hour and works for 4 hours, the earnings are found by multiplication: \(15 \times 4 = 60\). The worker earns $60.

Different jobs pay different wages because not all labor is the same. Some jobs require more training, education, experience, or risk. A skilled airplane mechanic usually earns more than a beginner doing simple tasks because the mechanic's labor is more specialized.

Employers also make choices in labor markets. If a business needs more workers, it may raise wages or improve working conditions to attract applicants. If fewer workers are needed, the business may hire less. Workers make choices too. They may choose jobs based on wages, hours, safety, location, or benefits.

Example: A local restaurant in a labor market

Step 1: A restaurant owner needs someone to prepare food and serve customers.

Step 2: A worker applies and offers time and skills.

Step 3: The owner hires the worker and agrees to pay a wage.

The restaurant owner is the buyer of labor, and the worker is the seller of labor.

Labor markets affect families directly. When adults in a household earn wages, that money can then be used in product markets to buy food, clothing, transportation, and housing. That is one reason the labor market is closely tied to the product market.

Later in the lesson, the connection becomes even clearer. A business that grows and sells more products often needs more workers, just as we saw with the flow in [Figure 2]. More demand in product markets can lead to more hiring in labor markets.

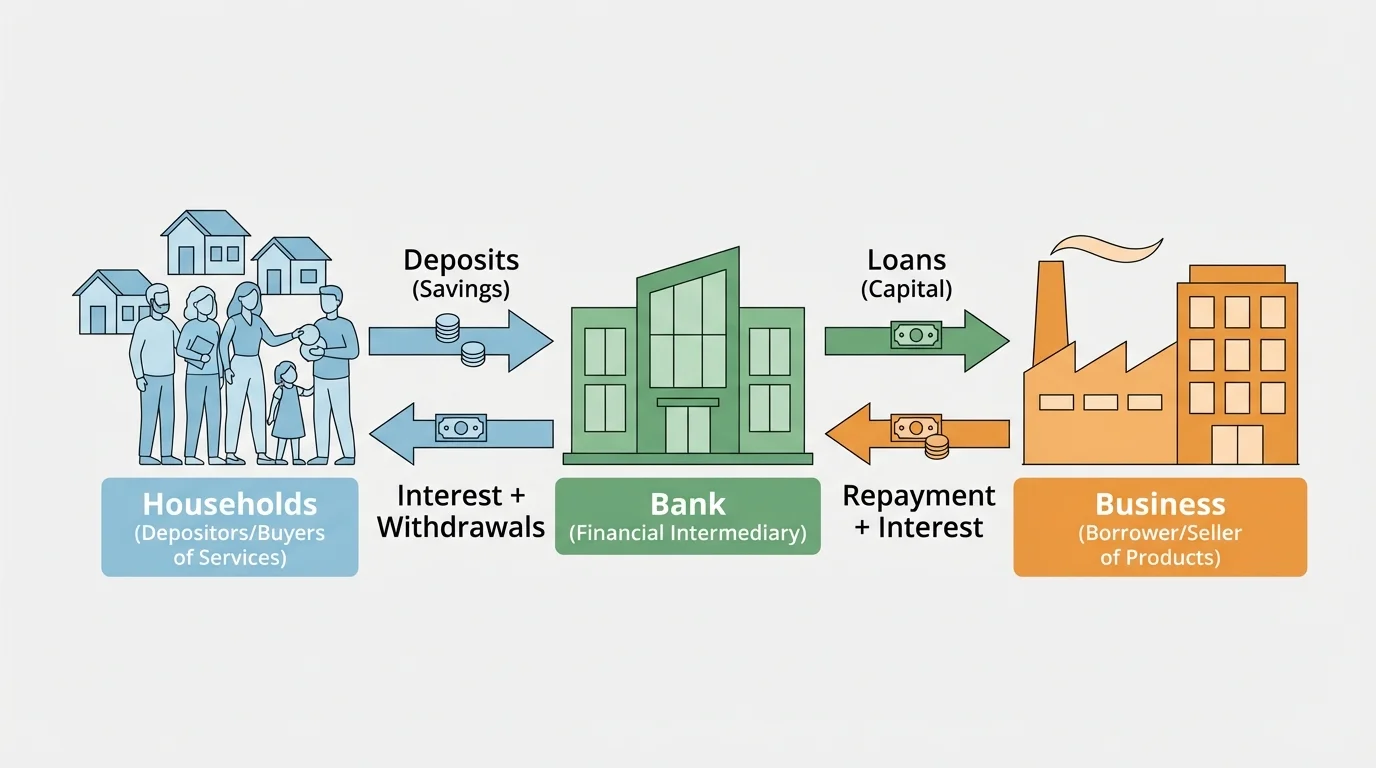

The financial market is where money itself is supplied, borrowed, saved, and invested. [Figure 3] shows how money moves through this system. In this market, the roles can be more complex. People who save money are supplying funds. Banks and other institutions gather those savings and move money to borrowers. Borrowers may include families buying homes, students paying for education, or businesses trying to expand.

A bank is a familiar part of the financial market. When a person deposits money, the bank is receiving funds that can later be loaned out. If a small business wants to buy new ovens, trucks, or computers, it might borrow money from the bank. In that example, savers help provide funds, the bank connects savers and borrowers, and the business becomes a buyer of financial capital.

Another important idea is interest. Interest is the cost of borrowing money or the reward for saving it. If a bank pays $2 of interest on $100 saved for a certain time, the saver ends up with $102. That can be written as \(100 + 2 = 102\).

Financial markets do more than store money. They help businesses grow. A company may need money before it can open a new store, buy equipment, or invent a new product. Borrowing or receiving investment gives that business a chance to expand. Expansion can then create jobs in the labor market and more goods in the product market.

People also act as buyers in financial markets when they borrow money. A family taking out a loan to buy a house is receiving funds now and agreeing to repay them later, usually with interest. A business taking a loan to purchase machinery is doing something similar.

Some of the money saved in one community can help a business far away. A deposit in a bank in one city may become part of a loan that helps a business grow in another part of the country.

Investors are also part of financial markets. An investor gives money to a business or project, hoping to earn a return in the future. This involves risk because the business may do well or poorly. Even though this idea is more advanced, the basic role is still about moving money from those who have it to those who can use it.

The connections in [Figure 3] help explain why financial markets matter to daily life. Savings accounts, loans, and investments support spending, hiring, and production across the economy.

These three markets are not separate worlds. They are linked like parts of one system. A business may borrow money in a financial market, use that money to buy equipment, hire workers in the labor market, and then sell products in a product market.

Consider a bakery. First, the owner might get a bank loan to buy ovens. Next, the bakery hires workers to bake bread and serve customers. Finally, customers come in and buy bread, cakes, and drinks. One business has now participated in all three markets.

Households connect the markets too. A parent may work at a hospital and earn wages in the labor market. The family uses part of that income to buy groceries in the product market. They may also save part of the income in a bank or borrow money for a car in the financial market.

| Market | Main Buyers | Main Sellers | What Is Exchanged |

|---|---|---|---|

| Product market | Consumers and businesses | Businesses and producers | Goods and services for money |

| Labor market | Businesses, schools, governments | Workers | Labor for wages |

| Financial market | Borrowers and investors | Savers, lenders, investors | Money for interest or future return |

Table 1. Comparison of buyers, sellers, and exchanges in the three main markets.

This comparison shows why understanding roles is so important. The same person or business can be a buyer in one market and a seller in another. Economics is not just about one action. It is about relationships.

Across the Western Hemisphere, consumers and businesses depend on one another. In Canada, businesses sell energy products, technology, and services to buyers at home and abroad. In Brazil, businesses may sell coffee, airplanes, or digital services. In Mexico, factories produce cars, electronics, and household goods that are sold in product markets across North America and beyond.

Consumers influence these businesses with their choices. If people want more electric vehicles, businesses may produce more of them. If families spend more on online entertainment, companies may invest more in streaming and internet services. Consumer demand helps shape what businesses decide to make, hire for, and finance.

Consumers and businesses depend on each other

Consumers need businesses to provide goods, services, jobs, and financial opportunities. Businesses need consumers to buy products and often to work as employees. This dependence stretches across countries through trade, tourism, banking, and transportation.

Tourism gives another clear example. In Caribbean nations, visitors buy hotel stays, meals, and activities in product markets. Hotels and tour companies hire workers in labor markets. Many of those businesses also borrow or invest money in financial markets to maintain buildings, boats, or transportation services.

Farms in Argentina, software companies in the United States, and shipping businesses in Panama all participate in these same basic market relationships, even though the products and services are very different.

Understanding buyers and sellers helps people make smarter choices. As a consumer, you can compare products and prices. As a future worker, you can think about how skills and education affect wages. As a saver or borrower, you can understand why banks pay interest on savings and charge interest on loans.

It also helps explain news about jobs, prices, and business growth. If stores are busy and sales rise, businesses may hire more workers. If borrowing becomes expensive, some businesses may delay expansion. If workers gain new skills, they may qualify for better-paying jobs.

Money does not only buy things. It also acts as a signal and a tool. Prices in product markets, wages in labor markets, and interest in financial markets all help guide decisions.

Markets are not perfect, and sometimes problems happen. Prices can rise too fast, jobs can be hard to find, and loans can be difficult to repay. But the basic roles of buyers and sellers still help us understand what is happening.

Once you can identify who is buying, who is selling, and what is being exchanged, the economy becomes much easier to read. A store sale, a job posting, and a bank loan may seem unrelated at first, but each one is part of the same larger economic system.