Plenty of people say they want to "be their own boss," but far fewer are ready for what that actually means. The hard part is usually not the idea. It is whether you can deliver a product or service consistently, attract paying customers, manage money, follow the rules, and keep going when something goes wrong. Real readiness is not about confidence alone. It is about being honest with yourself before you invest time, money, and energy.

Self-employment and entrepreneurship can be exciting because they give you more control over your work. They can also be stressful because there is no guaranteed paycheck, no manager organizing your schedule, and no one automatically fixing your mistakes. If you prepare well, you give yourself a much better chance of building something stable. If you rush in without checking the basics, you can lose money, damage your reputation, or burn out fast.

Being "ready" does not mean being perfect. It means you understand what you can already do, what you still need to learn, and what risks you are taking. A student who bakes excellent custom cookies from home might be talented, but talent alone is not enough. If orders arrive late, ingredients are underpriced, or local food-sale rules are ignored, the business can fail even if customers like the product.

On the other hand, a person with average talent but strong planning can often build something reliable. For example, someone offering phone repair, lawn care, video editing, tutoring, or social media management can begin small, learn from feedback, and improve. The important question is not "Would it be cool to own a business?" The better question is "Am I prepared to solve a real problem in a way that people will pay for, again and again?"

Self-employment means working for yourself instead of earning wages from an employer. You may sell your own labor or skill directly, such as tutoring, photography, hair styling, or repair services.

Entrepreneurship means building a business around an opportunity, often with the goal of growth beyond your own time and labor. An entrepreneur may create systems, hire help, or develop a product that can scale.

These two paths overlap, but they are not exactly the same. If you design logos for clients online and get paid for your own work, that is self-employment. If you build a brand studio, bring in other designers, and create systems so the business grows beyond you, that becomes entrepreneurship. Some people start with self-employment and later move into entrepreneurship.

Before you decide whether you are ready, figure out which path you are actually considering. Self-employment usually depends heavily on your time and skill. If you stop working, income often stops too. Entrepreneurship usually requires more planning at the beginning, but it may eventually allow the business to run with systems, products, or a team.

Neither path is "better." A freelance video editor who wants flexible income may be making a smart choice. A student developing a small clothing brand with an online store may be testing an entrepreneurial idea. What matters is fit. Your goals, tolerance for uncertainty, available time, and current responsibilities all affect what makes sense for you right now.

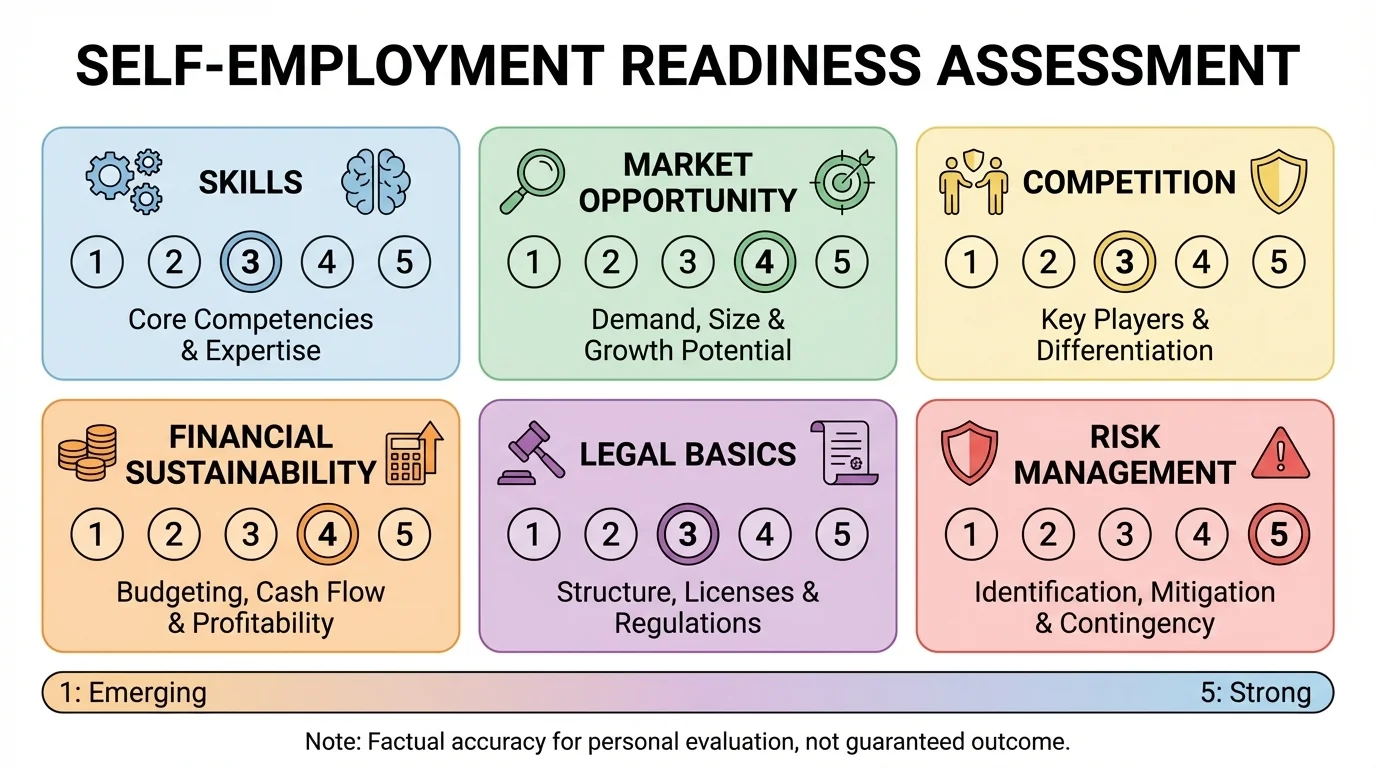

To evaluate your readiness, start with a self-assessment. In this kind of review, you rate the areas that matter most for working for yourself, as shown in [Figure 1]. Most students need to look at six categories: technical skill, communication, time management, money management, resilience, and customer service.

Technical skill is your ability to do the actual work. If you want to tutor algebra, can you explain it clearly? If you want to sell handmade jewelry, is the quality consistent? If you want to manage social media for small businesses, can you create strong posts, schedule content, and read performance data?

Communication matters because you will answer questions, explain prices, handle complaints, and follow up with people. A weak communicator loses trust fast. You do not have to be flashy, but you do need to be clear, respectful, and reliable online, by message, by email, or in video calls.

Time management is often where people struggle. When you work for yourself, nobody stands over you and says, "Start now." You must plan your own schedule, meet deadlines, and keep promises. If you regularly procrastinate on school assignments, forget messages, or miss due dates, that is a warning sign. It does not mean you can never run a business. It means you should improve that habit before taking on paying customers.

Money management includes tracking income, saving for expenses, pricing correctly, and avoiding the mistake of spending business money as if it were personal money. Resilience means handling rejection and problems without quitting immediately. Customer service means treating people professionally, fixing mistakes when possible, and protecting your reputation.

One useful way to assess yourself is to rate each area from 1 to 5. For example, if your ratings are 4, 3, 2, 2, 4, and 3, the total is \(4 + 3 + 2 + 2 + 4 + 3 = 18\) out of 30. That does not "prove" whether you should start, but it shows where you need work. A low score in time or money management often causes more damage than a low score in creativity.

Readiness check example

A student wants to start a weekend sneaker-cleaning service.

Step 1: Rate the six key areas

Technical skill = 4, communication = 3, time management = 2, money management = 2, resilience = 4, and customer service = 3.

Step 2: Add the scores

\(4 + 3 + 2 + 2 + 4 + 3 = 18\)

Step 3: Interpret the result

A score of 18 suggests some strong potential, but also clear risk areas. The student should improve scheduling and budgeting before taking many orders.

The best next move is not "quit the idea." It is "start small while improving weak areas."

If you looked again at the rating categories in [Figure 1], you would notice that several of them are not about talent at all. They are about habits. That matters because habits can be changed. You can practice replying to messages professionally, keeping a calendar, using a spreadsheet, and following a simple workflow.

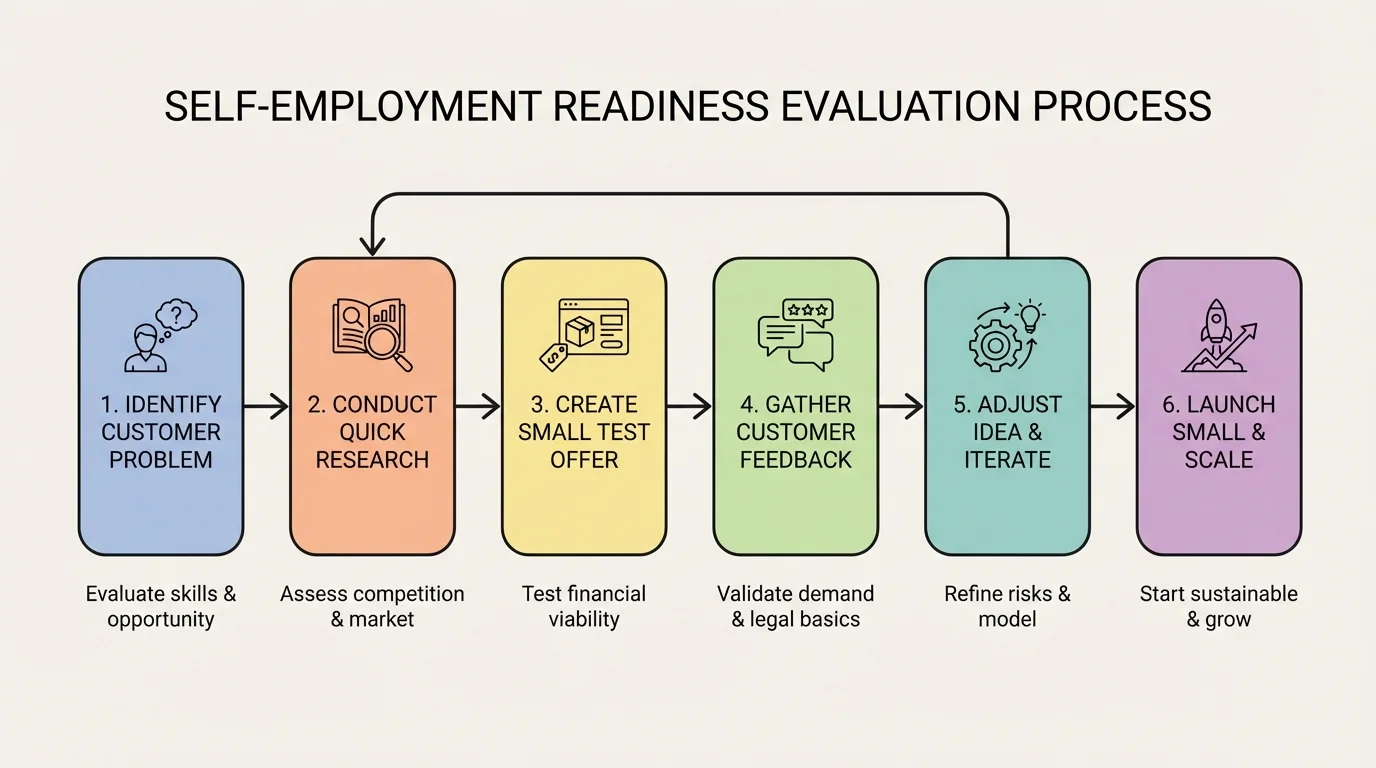

A strong idea solves a real problem for real people. That is your market opportunity: a chance to offer something people want, need, and will pay for. The basic process in [Figure 2] starts with the customer's problem, not your excitement about the idea.

Ask practical questions. Who exactly would buy this? What problem does it solve? How often does that problem happen? Are people already spending money on solutions? If the answer is vague, your idea may still be too weak. "Everyone would want this" is usually a sign that you have not identified a real target customer.

Suppose you want to start a note-taking service for busy students. You should test whether students actually trust someone else to organize notes, whether schools or families would object, and whether there are easier free options. Compare that with a resume-editing service for teens applying to jobs. That solves a clearer problem for a specific group and may be easier to test honestly.

You do not need expensive research. You can validate demand by reading reviews, checking local listings, searching online platforms, asking people in your community, running a small preorder, or offering a limited test version. Validation is simply checking whether interest is real before you invest too much. Too many beginners confuse compliments with demand. Someone saying, "That's a cool idea" is not the same as someone paying $25.

Watch out for a common trap: building for yourself instead of the customer. You may love designing custom planners, but if your ideal buyers prefer digital tools, your excitement does not create demand. Good entrepreneurs listen for repeated problems. They notice what people complain about, what tasks they avoid, and what they already pay to solve.

Many small businesses fail not because the owner lacks motivation, but because they try to sell something people do not urgently want, need, or trust.

Another practical test is pricing. If your likely customer says your service is useful but "too expensive," that does not always mean you should lower the price. It may mean your customer is not the right fit, your value is unclear, or your costs are too high. Market opportunity is not just about whether people like the idea. It is also about whether enough people will buy at a price that keeps you going.

Competition is not automatically bad. In fact, some competition is a sign that customers already exist. The key is understanding your direct competitors and your indirect competitors. A direct competitor offers nearly the same thing to the same people. An indirect competitor solves the same problem differently.

For example, if you offer dog walking in your neighborhood, another local dog walker is a direct competitor. A dog daycare center is an indirect competitor. If you sell custom phone cases online, direct competitors may be other custom-case sellers, while indirect competitors include plain budget cases from major retailers.

Study competitors with open eyes. What do they charge? How fast do they respond? What do customers like and dislike in their reviews? What seems missing? This helps you find your unique value proposition, which is the specific reason someone should choose you instead of another option. Maybe you offer faster delivery, eco-friendly materials, a student-friendly price, more customization, better communication, or a niche focus.

Do not assume "I have no competition" is a good sign. Usually it means one of two things: either you have discovered a truly rare opening, or there is no demand. Most of the time, it means you need to research more carefully.

| Question | Weak Answer | Stronger Answer |

|---|---|---|

| Who is my customer? | Everyone | Local pet owners who work late and need weekday walking help |

| Why would they choose me? | My service is good | Same-day booking, photo updates, and lower intro pricing |

| Who else solves this problem? | Nobody | Two local walkers and one daycare center |

| What gap do I fill? | I just want to try it | Flexible short walks for people who cannot commit to daycare packages |

Table 1. Comparison of weak and strong answers when analyzing market position and competition.

When you compare your offer with others, be realistic. If a larger competitor has lower prices, better equipment, and strong reviews, you probably will not beat them by copying them. You may compete better by being more personal, more local, more specialized, or more convenient.

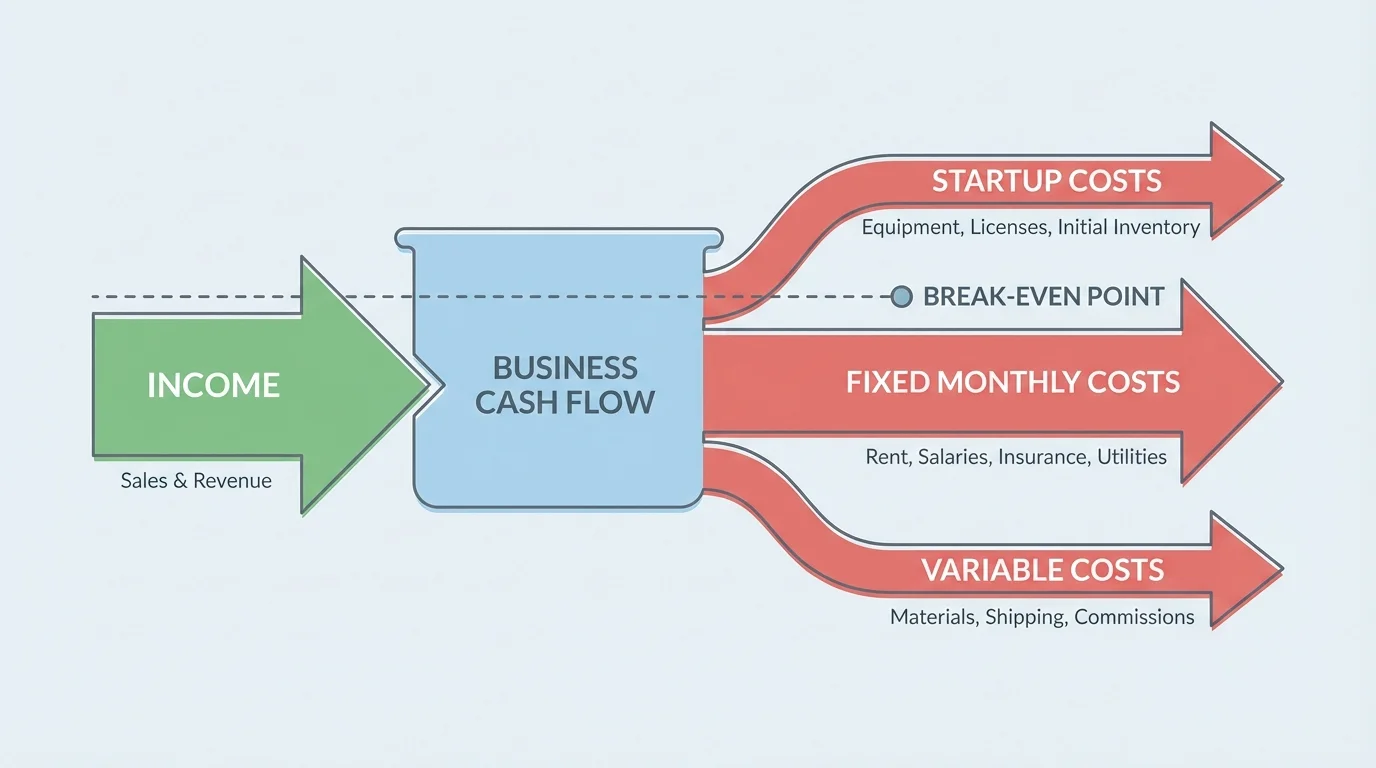

A business idea may sound exciting, but if the numbers do not work, it becomes a stressful hobby instead of reliable income. At a big-picture level, as shown in [Figure 3], money comes in, and money also flows out through startup costs, fixed monthly costs, and changing costs tied to each sale. You need enough money left over to keep operating.

Start with startup costs. These are one-time or early expenses such as tools, equipment, packaging, a website domain, permits, cleaning supplies, or ingredients. Then look at monthly costs like internet, software subscriptions, transportation, replacement materials, and advertising. Finally, think about variable costs, which rise as you sell more.

Now consider cash flow, which is the timing of money moving in and out. A business can look profitable on paper and still fail if money comes in too slowly. For example, if you spend $200 on supplies today but customers pay you two weeks later, you need enough cash to survive the gap.

One practical idea is the break-even point. This is the point where your income matches your costs. If you charge $20 per service and each service costs you $8 in supplies and transport, then you keep $12 before covering fixed monthly costs. If monthly fixed costs are $120, you need \(120 \div 12 = 10\) sales to break even.

Simple break-even example

A student offers basic lawn mowing.

Step 1: Identify the selling price and variable cost

Price per job is $30. Fuel and supplies per job cost $10. The amount left after each job is \(30 - 10 = 20\) dollars.

Step 2: Identify monthly fixed costs

Equipment maintenance and advertising total $100 per month.

Step 3: Calculate break-even jobs

\(100 \div 20 = 5\)

The student needs 5 jobs per month to break even on those monthly fixed costs.

This kind of calculation is simple, but it changes your decisions. If getting five jobs every month seems easy, the idea may be financially realistic. If getting five jobs seems unlikely, you may need to raise prices, lower costs, or target a different market.

Also think about your personal situation. If you need regular money for bills, food, transportation, or family support, self-employment can be risky unless you have savings or another income source. A good rule is to avoid depending immediately on a brand-new business for essential living costs. Starting small can protect you while you test the idea.

As the cash-flow picture makes clear, survival is not just about total profit. Timing matters. Late-paying customers, surprise expenses, damaged tools, and slow weeks can hurt even when your prices seem fine.

You already use financial thinking in everyday life when you budget for gas, food, phone bills, or entertainment. Business finances use the same core habit: know what is coming in, know what is going out, and leave room for surprises.

You do not need to become a lawyer before starting a small business, but you do need to know the basics. Legal mistakes can cost money fast. Depending on where you live and what you sell, you may need a permit, a license, tax registration, insurance, or permission to operate from home. Rules can differ for selling food, offering child care, doing beauty services, repairing electronics, or running online stores.

One useful term is sole proprietorship. This is a common basic business structure where one person owns the business and is personally responsible for it. It is often simple to start, but it may not protect your personal finances if something goes wrong. Other business structures may offer more protection, but they are usually more complex. If you get serious about starting, check your local rules and ask a qualified adult, government office, or legal professional for guidance.

Taxes matter too. If you earn money, you may need to report income, keep records, and set aside part of what you make. A common beginner mistake is spending everything that comes in and forgetting that some of it may need to go toward taxes later. Even a simple spreadsheet with date, customer, amount earned, and expense amount can save major trouble.

Contracts and written agreements are another basic protection. If you are offering a service, write down what the customer gets, the price, deadlines, cancellation rules, and how disputes are handled. It does not have to be fancy. It has to be clear. This protects both sides and reduces misunderstandings.

If you collect names, phone numbers, addresses, or payments online, privacy and digital security matter. Use secure platforms, strong passwords, and professional communication. Losing customer data or mishandling payment information can ruin trust quickly.

Legal basics are really about responsibility

When you work for yourself, you are not just making money. You are taking responsibility for safety, fairness, records, and promises. The more your business affects other people's money, time, health, or personal information, the more careful you need to be.

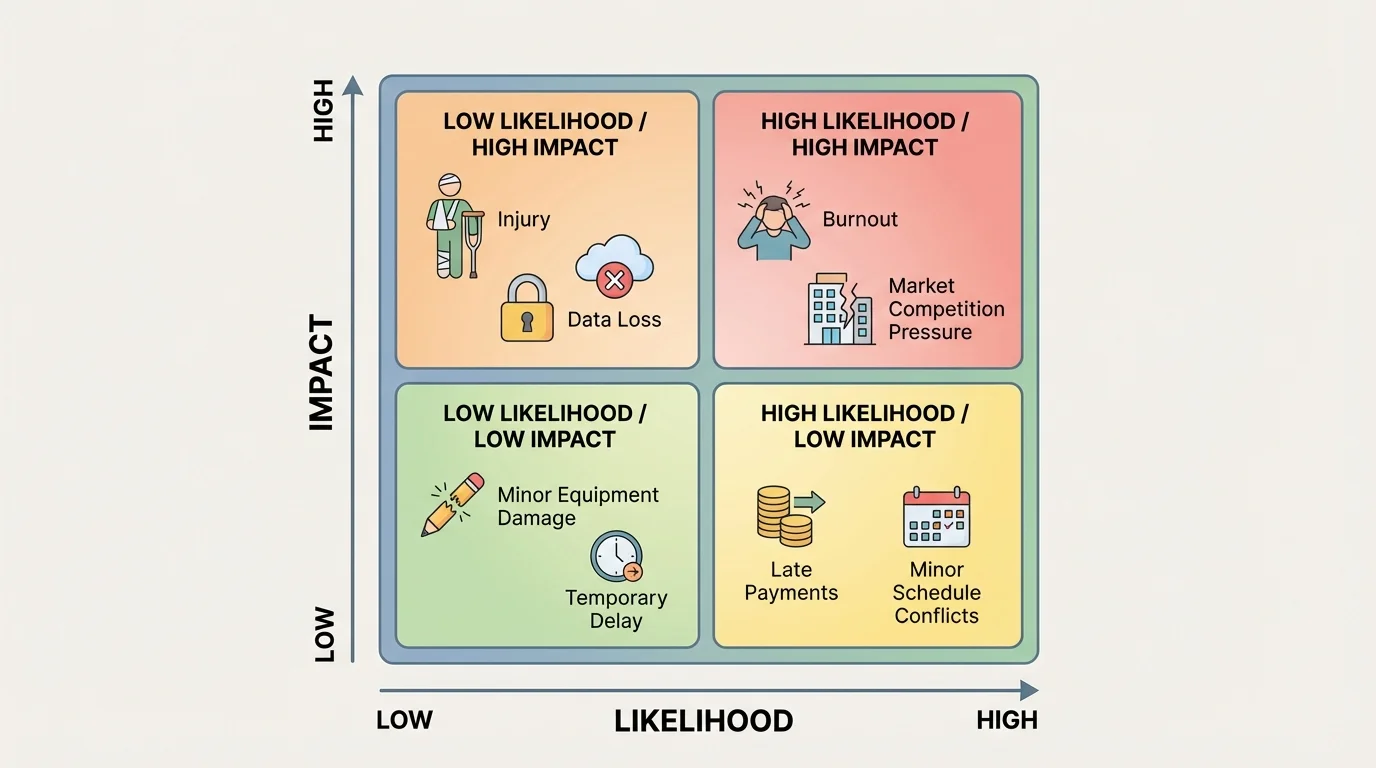

Every business has problems. The goal of risk management is not to remove all risk. It is to notice likely problems early, reduce the chance of damage, and have a plan if something goes wrong. In [Figure 4], risks are sorted by how likely they are and how serious the damage could be.

Some risks are small but common, like late replies, missed appointments, or one unhappy customer. Some are less common but much more serious, like injury, legal complaints, data loss, or major equipment damage. You should handle the high-likelihood and high-impact risks first.

Examples of risk management include requiring deposits before custom work, backing up files, using clear written policies, saving emergency funds, checking equipment before use, separating business and personal money, and setting realistic order limits so you do not promise more than you can deliver.

Burnout is a real risk, especially for students. If you are balancing schoolwork, family responsibilities, a social life, and a business, overloading yourself can harm all of them. If you start snapping at customers, missing deadlines, or losing sleep constantly, your business model may need adjustment. Sometimes the strongest move is setting fewer slots, raising prices, or pausing new orders instead of pushing until everything falls apart.

Fraud and scams are another risk. Be careful with suspicious payment methods, fake urgent requests, or customers who overpay and ask for refunds in strange ways. Protect your reputation by communicating clearly, documenting transactions, and trusting warning signs.

The priority system in [Figure 4] helps you avoid wasting energy on tiny worries while ignoring major threats. A late text reply matters, but unsafe food handling, poor recordkeeping, or unsecured payment links matter much more.

After looking at skills, demand, competition, finances, legal basics, and risk, ask yourself a tougher question: Am I ready now, or am I only excited now? Those are not the same thing.

A practical readiness checklist includes questions like these:

If most of your answers are "yes," you may be ready to start small. If several answers are "not yet," that is not failure. It is useful information. You may need more training, savings, research, or structure before launching.

Decision example

A student wants to sell custom cakes from home.

Step 1: Strengths

The cakes look excellent, and friends are asking to buy them.

Step 2: Gaps

The student has not checked food-sale rules, has underpriced ingredients, and cannot always meet tight deadlines.

Step 3: Decision

The student is not ready for full launch but is ready to prepare by learning rules, calculating true costs, and accepting only a few planned orders.

This is what smart readiness looks like: not rushing, but not freezing either.

If you are interested in self-employment or entrepreneurship, the best move is usually a small, low-risk start. That could mean testing one service, taking two paying clients, selling a tiny first batch, or creating one clear offer instead of ten confusing ones.

Try This: Write one sentence that explains your idea in plain language: who it helps, what problem it solves, and why someone would choose you. If you cannot explain it simply, the idea may still be too unclear.

Try This: List your expected first-month costs and your expected first-month sales. Even a rough estimate forces you to think realistically. If your expected sales are 8 and your break-even number is 10, you already know something needs to change before launch.

Try This: Ask three trusted adults or potential customers one question: "What would make you hesitate before buying this from someone new?" Their answers may reveal issues with trust, price, speed, quality, or safety.

Try This: Set a basic rule for yourself before starting: reply within 24 hours, track every sale, and never promise what you cannot deliver. Small rules create professional habits.

Readiness is not a personality trait. It is a combination of honesty, preparation, and action. You do not need to know everything before you begin. But you do need enough skill, evidence, planning, and self-control to begin responsibly.