Two students can earn the same degree and leave with very different futures. One graduates with manageable debt and options. The other spends years trying to catch up on payments, delaying moving out, buying a car, or building savings. That difference often starts before school begins, when you decide what you will pay, what you will borrow, and what you are giving up by choosing one path over another.

Postsecondary decisions include more than choosing a college. You might be comparing a four-year university, community college, a trade program, a certificate, an apprenticeship, military service, or going straight into work while training later. None of these options is automatically "best." The best choice is the one that matches your career goals, your learning style, and your financial reality.

If you borrow money for school, you are making a promise about your future income. That is why it is important to think like an adult consumer, not just an excited applicant. You are not only asking, "Do I want to go here?" You are also asking, "What will this cost me each month later?" and "What else could I do with this money, time, and energy?"

Borrowing means taking money now with a legal obligation to repay it later, usually with interest.

Repayment is the process of paying back what you borrowed according to the loan terms.

Opportunity cost is the value of what you give up when you choose one option instead of another.

These ideas connect directly. The more you borrow, the more repayment matters. The more money and time one option requires, the higher the opportunity cost may be compared with another option.

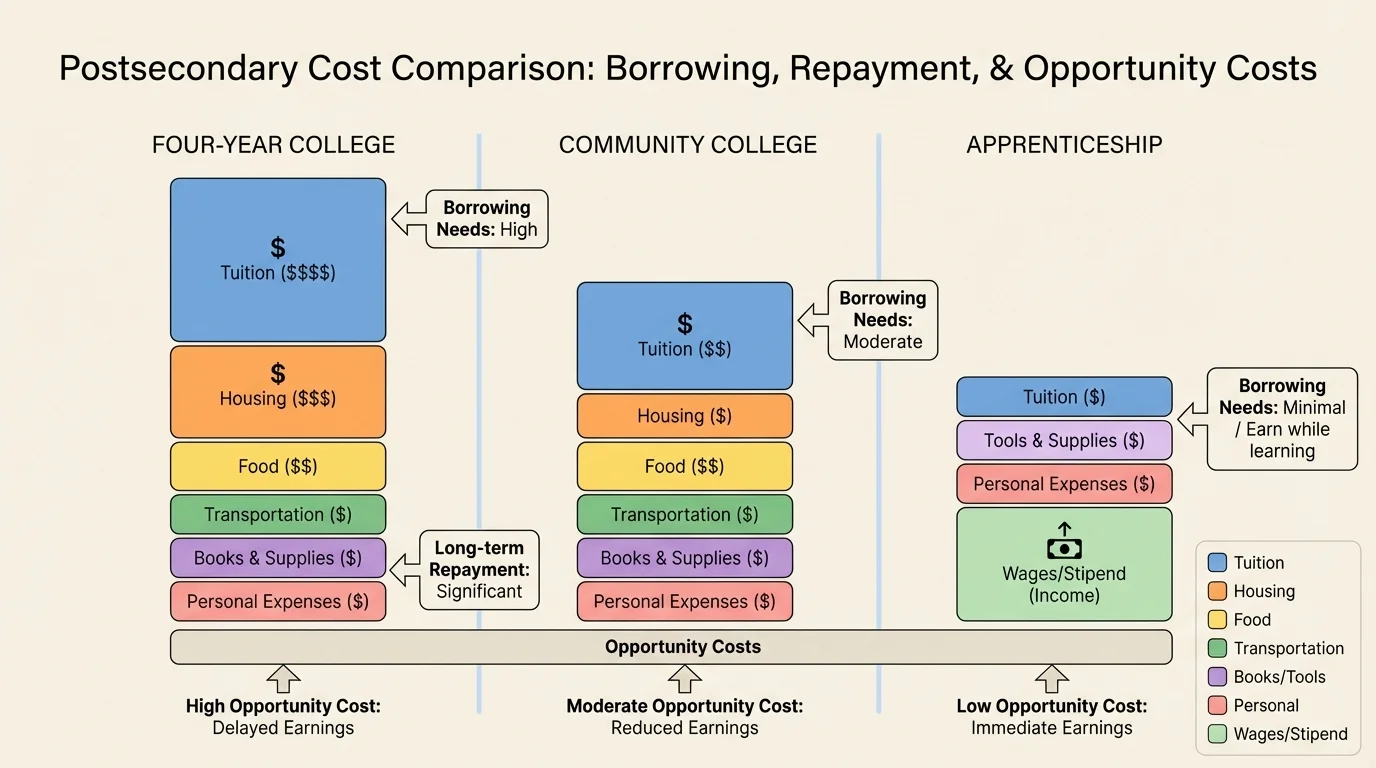

One of the biggest mistakes students make is focusing only on tuition. Your actual cost is broader. A school or training program may list tuition and fees, but your real yearly cost can also include housing, food, transportation, books, supplies, technology, test fees, work clothing, tools, and personal expenses. The total cost can look very different depending on the path, even when the sticker price first catches your attention.

As [Figure 1] suggests, suppose a university lists tuition and fees of $12,000 for the year. That sounds like the number to beat. But if housing is $9,000, food is $4,000, transportation is $1,500, books and supplies are $1,200, and personal expenses are $2,000, your estimated yearly cost becomes much higher. The total is \[12{,}000 + 9{,}000 + 4{,}000 + 1{,}500 + 1{,}200 + 2{,}000 = 29{,}700\]

So the actual annual cost is $29,700, not $12,000.

Hidden costs matter too. A program that requires special equipment, unpaid clinical hours, commuting, or licensing exams may cost more than expected. If you plan to live at home, you may reduce housing costs, but you could increase transportation costs. If you study online, you may save on commuting but need reliable internet and a computer upgrade.

Before you compare options, make a simple cost sheet for each one. Use the school's official cost of attendance if available, then edit it to fit your real situation. If you know you will live at home, change the housing number. If you will need a car, estimate gas, insurance, parking, and maintenance. Make the numbers honest.

A smart decision starts with a realistic total, not a hopeful guess. If your estimate is too low, you may borrow more later under pressure, which is when people make expensive mistakes.

Once you know the total cost, the next question is how you will cover it. Not all money for school works the same way. Some money never has to be repaid. Some is earned through work. Some is borrowed and must be repaid with interest.

Grant and scholarship money are usually the best first sources because they reduce what you owe without creating debt. Work-study, part-time jobs, savings, and family support can also lower how much you need to borrow. Principal is the original amount you borrow, and that number matters because interest is calculated on it.

Use money in the right order

A practical way to think about paying for school is this: use free money first, then your own money or earned income, and borrow only what is still necessary. Borrowing should fill a gap, not fund a lifestyle upgrade.

Suppose your yearly cost is $29,700. You receive a $6,000 scholarship, a $3,500 grant, and plan to earn $4,000 through part-time work. Your family can help with $2,000. The remaining amount is \[29{,}700 - 6{,}000 - 3{,}500 - 4{,}000 - 2{,}000 = 14{,}200\]

That means you may need to cover $14,200 through savings, a payment plan, a less expensive option, or loans.

This is where a lot of students stop thinking carefully. They see a gap and immediately borrow the full amount. But that gap is your signal to compare choices again. Could you lower housing costs? Start at a community college? Attend a local program? Work more during summers? Delay a nonessential purchase? Every dollar you do not borrow is a dollar that will not collect interest later.

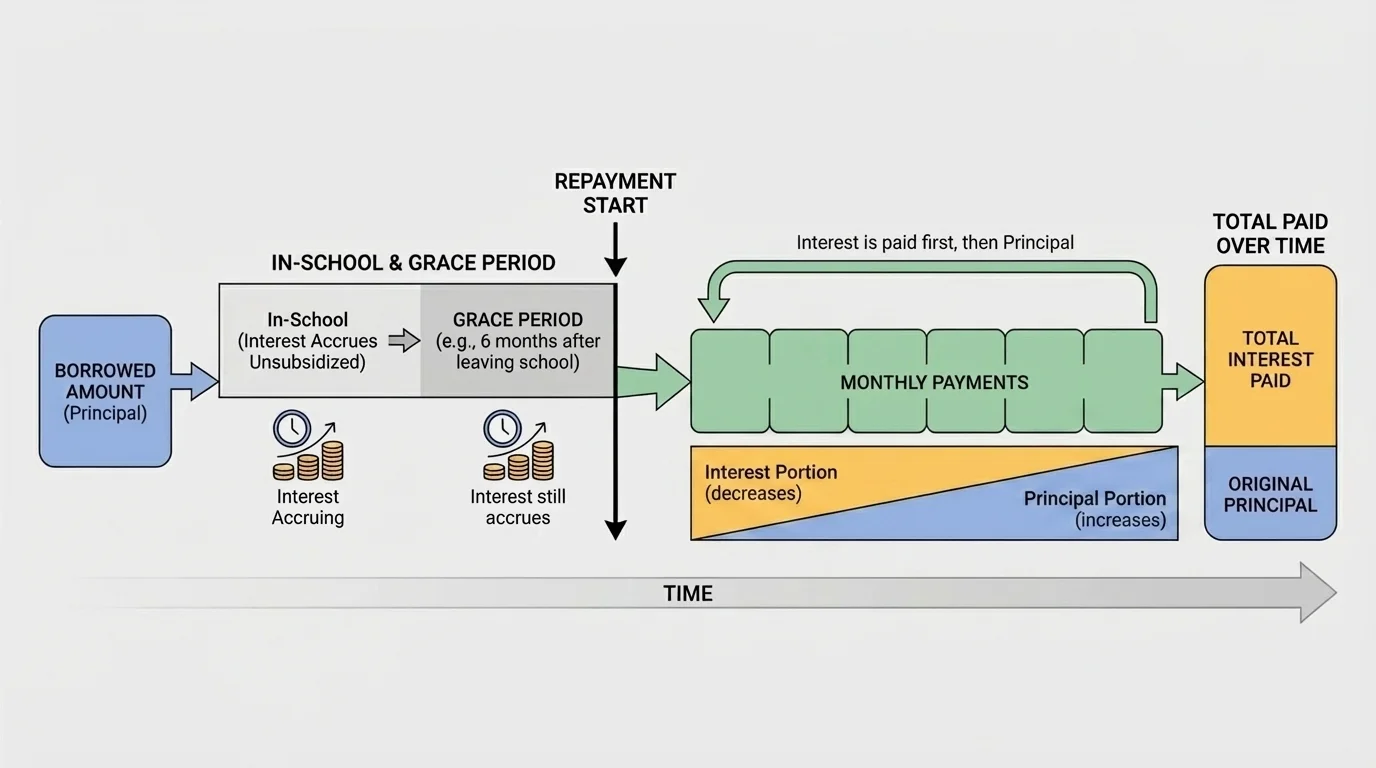

A student loan is not just "money for school." It is a contract with terms. The process usually starts when funds are disbursed to help pay school costs, then moves through a grace period after you leave school, and finally into repayment with scheduled monthly bills. To judge whether borrowing is manageable, you need to understand a few key parts of the loan.

As [Figure 2] shows, Interest is the extra amount charged for borrowing money. The loan term is how long you have to repay. A longer term can lower the monthly payment but usually increases the total amount paid over time. A grace period is the time after leaving school before regular payments begin. Some loans are federal, some are private, and the rules can be very different.

Here is the basic repayment idea: if you borrow more, or if the interest rate is higher, or if you repay for a longer time, the total cost rises. Even if the monthly bill looks manageable, the long-term total may be much larger than what you originally borrowed.

This is why you should always ask four questions before accepting a loan: How much am I borrowing? What is the interest rate? When does repayment start? How much will I pay in total, not just each month?

Worked example: estimating a simple monthly repayment

You borrow $10,000 and repay about $120 per month for 10 years.

Step 1: Find the total number of payments.

There are 10 years, so the total number of monthly payments is \[10 \times 12 = 120\]

Step 2: Estimate the total repaid.

If the payment is about $120 each month, the total repayment is \[120 \times 120 = 14{,}400\]

Step 3: Compare total repaid with amount borrowed.

The loan principal was $10,000, but the estimated total paid is $14,400. The extra amount is \[14{,}400 - 10{,}000 = 4{,}400\]

This means the loan may cost about $4,400 beyond the amount originally borrowed.

This example is simplified, but it makes the real point: monthly payments can hide the true cost. A bill that seems "not too bad" each month can still become a major expense over years.

Now compare three realistic borrowing choices. The goal is not to memorize formulas. The goal is to see how different decisions affect your life after graduation.

If one program requires borrowing $6,000 per year for four years, the total borrowed is \[6{,}000 \times 4 = 24{,}000\]

If another pathway requires borrowing $3,000 per year for two years, the total borrowed is \[3{,}000 \times 2 = 6{,}000\]

Those two paths may lead to similar careers, but the repayment pressure will be very different.

| Option | Years borrowing | Amount borrowed per year | Total borrowed | Estimated monthly payment |

|---|---|---|---|---|

| Four-year university path | 4 | $6,000 | $24,000 | About $275 |

| Community college + transfer | 2 | $3,000 | $6,000 | About $70 |

| Certificate program | 1 | $4,500 | $4,500 | About $50 |

Table 1. A simplified comparison of how total borrowing can affect estimated monthly repayment.

These monthly payment estimates are general examples, not official quotes, but they help you think practically. A payment of about $275 per month may not sound huge until you add rent, car insurance, groceries, phone service, and emergency expenses. If your first job pays modestly, that loan payment can shape many other choices.

Many borrowers do not struggle because they borrowed for a dream career. They struggle because they borrowed more than necessary for housing, transportation, or a school name that did not change their job options much.

A useful reality check is to compare your expected starting income with your possible monthly debt payment. If the payment would feel stressful on an entry-level income, your plan may need revision now instead of later.

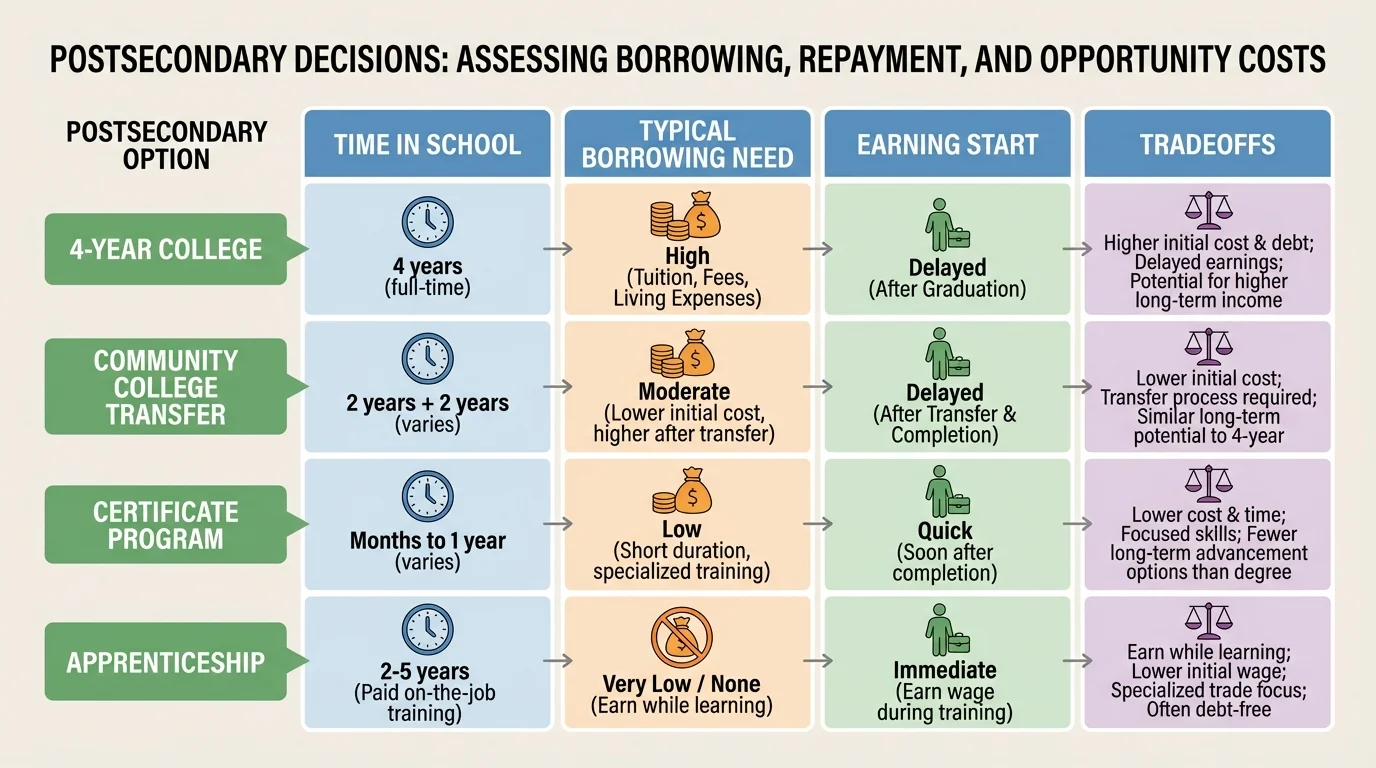

As [Figure 3] shows, Opportunity cost is easy to ignore because it is about what you do not choose. But it matters just as much as tuition. Different postsecondary paths come with different tradeoffs in time, borrowing, speed to income, and flexibility.

For example, if you choose a four-year residential college, you may gain a campus network, a degree path, and a traditional college experience. But you may also give up years of full-time earnings and take on more debt. If you choose a local community college while living at home, you may save tens of thousands of dollars, but you may give up the experience of relocating right away. If you enter an apprenticeship, you may begin earning earlier and avoid heavy debt, but the path may be narrower or more specialized.

Opportunity cost is not only about money. It includes time, flexibility, stress, risk, and alternatives. A costly program might be worth it if it strongly improves your chances in a field that requires that credential. But if a cheaper route gets you to the same job, the more expensive route may carry a high opportunity cost.

Think about these comparisons: If you spend two extra years in a higher-cost program, what income are you giving up by not working sooner? If you borrow heavily, what future choices are you giving up because of monthly debt? As we saw earlier in [Figure 1], total cost is built from many categories, so the opportunity cost of "going away for school" may be driven more by housing and living expenses than by tuition itself.

Case study: comparing two paths to a similar career goal

Jordan wants to work in digital design.

Option A: Private college

Total yearly cost is $34,000. Scholarships cover $8,000 per year, leaving $26,000 each year. Over four years, the remaining cost is \[26{,}000 \times 4 = 104{,}000\]

If Jordan cannot cover much from savings or earnings, borrowing could be very high.

Option B: Community college plus transfer

The first two years cost $8,000 each while living at home. The final two years at a public university cost $18,000 each. The total is \[8{,}000 + 8{,}000 + 18{,}000 + 18{,}000 = 52{,}000\]

Step 3: Compare the difference.

The cost difference is \[104{,}000 - 52{,}000 = 52{,}000\]

If both pathways can lead to a strong portfolio and similar job opportunities, Option B may cut borrowing dramatically. That lower debt can create freedom after graduation.

The key question is not "Which path sounds most impressive?" It is "Which path gives me the best long-term value for the career I want?"

When offers and options begin to blur together, use a simple decision process. This keeps emotion from taking over when deadlines get close.

Step 1: List each option you are seriously considering. Include school, program, certificate, apprenticeship, military path, or direct-to-work plan.

Step 2: Write the realistic annual cost for each option. Include tuition, housing, food, transportation, books, supplies, and personal expenses.

Step 3: Subtract free money first. Remove grants and scholarships from the total.

Step 4: Subtract what you can reasonably pay from savings, summer work, part-time work, or family support. Be honest, not overly optimistic.

Step 5: Estimate the borrowing gap. That is the amount still uncovered.

Step 6: Estimate what repayment might feel like. Even a rough estimate can tell you whether the plan seems manageable.

Step 7: Compare opportunity costs. Ask what you gain and what you give up in each option.

Step 8: Choose the option that fits both your career goal and your financial reality.

A lower price does not automatically mean a better value, and a higher price does not automatically mean better results. What matters is the relationship between cost, borrowing, completion likelihood, and career payoff.

You can also create a short comparison table for yourself.

| Question | Option 1 | Option 2 | Option 3 |

|---|---|---|---|

| Total yearly cost | |||

| Free money received | |||

| Amount you can pay | |||

| Estimated amount to borrow | |||

| Time to complete | |||

| Expected starting income | |||

| Main opportunity cost |

Table 2. A decision-making template for comparing postsecondary pathways side by side.

Try This: Build this chart in a notes app or spreadsheet and fill in real numbers from your top choices. If a school has not given you enough details to complete the chart, that is a sign you need more information before committing.

Some borrowing is manageable and useful. Some borrowing is risky. Learn to spot the difference.

Warning sign 1: You do not know your total borrowing amount across all years. Students sometimes accept loans one year at a time without adding them together. A yearly loan can feel small until the four-year total becomes large.

Warning sign 2: You are considering private loans before fully understanding federal aid options. Private loans may have less flexible repayment terms and may require a cosigner.

Warning sign 3: You are borrowing for extras instead of essentials. Upgraded housing, frequent travel, and lifestyle spending can quietly become debt you will still be paying years later.

Warning sign 4: You are entering a program without checking completion rates, transfer policies, licensing requirements, or job placement information. Debt is especially dangerous if you borrow for a path you are unlikely to finish.

Warning sign 5: The plan only works if everything goes perfectly. Real life includes setbacks: reduced work hours, family emergencies, health issues, or changing majors. A financially safe plan leaves room for uncertainty.

Smart habits look different. Borrow only what you truly need. Recheck the total each year. Keep living costs as low as you reasonably can. Ask schools direct questions in writing. Read loan terms before accepting them. And remember the loan flow in [Figure 2]: money arrives now, but repayment comes later when your budget may already be crowded by adult expenses.

"The best loan is often the one you never needed to take."

That does not mean avoiding education or training. It means choosing a path strategically so your education expands your future instead of restricting it.

You do not need every answer today, but you do need real numbers. Start by collecting cost-of-attendance information for each option you are considering. Then list grants, scholarships, and realistic work income. Estimate the borrowing gap for each path. Compare that with likely starting pay and with what you would give up by choosing one route over another.

Try This: For each option, write one sentence that begins, "This path is worth the cost if..." If you cannot clearly finish that sentence, you may not yet have a strong reason to choose that option.

Try This: Ask an adult you trust to review your numbers with you on a call or shared document. A second set of eyes can catch missing costs, overly optimistic assumptions, or borrowing that looks manageable now but risky later.

The goal is not to find a perfect path with zero tradeoffs. The goal is to make a choice you understand. When you assess borrowing, repayment, and opportunity costs honestly, you give yourself more control over your future.