What happens if your headphones stop working, your pet needs food, or you want to buy a gift for someone later? Money can help with those things, but only if some of it is ready when you need it. That is why saving matters. Saving helps you prepare for tomorrow, not just today.

When you save, you put aside some money now so you can use it later. You do not spend all your money right away. Instead, you keep part of it for a reason. That reason might be something important, something helpful, or something unexpected.

Saving means keeping some money to use in the future instead of spending it now. A future need is something you may need later, like school supplies, a replacement item, a gift, or help during an emergency.

[Figure 1] Saving is a smart life skill because life does not always happen exactly as you expect. Sometimes things break. Sometimes plans change. Sometimes something important comes up. If you have saved money, you are more ready.

Save does not mean hiding money and never using it. It means making a plan for your money. You choose to keep some of it safe until the right time. That way, your money can help you later.

You might get money from doing chores at home, receiving a gift, or earning a small amount for helping with a family job. If you spend all of it at once on candy or a small toy, it is gone. But if you keep some, you have choices later.

Think of saving like putting seeds in the ground. One coin may not seem like much. But when you keep adding more, your savings can grow. If you save $1 one day and $1 another day, then you have \(1 + 1 = 2\). Little bits can become enough for something useful.

Some people save using a jar, some use envelopes, and some keep track with a grown-up in a bank account. The place can be different, but the idea is the same: keep money for later.

Saving also helps you feel calmer. If you know you have some money set aside, you may worry less when a need comes up. Being prepared can help you make better choices.

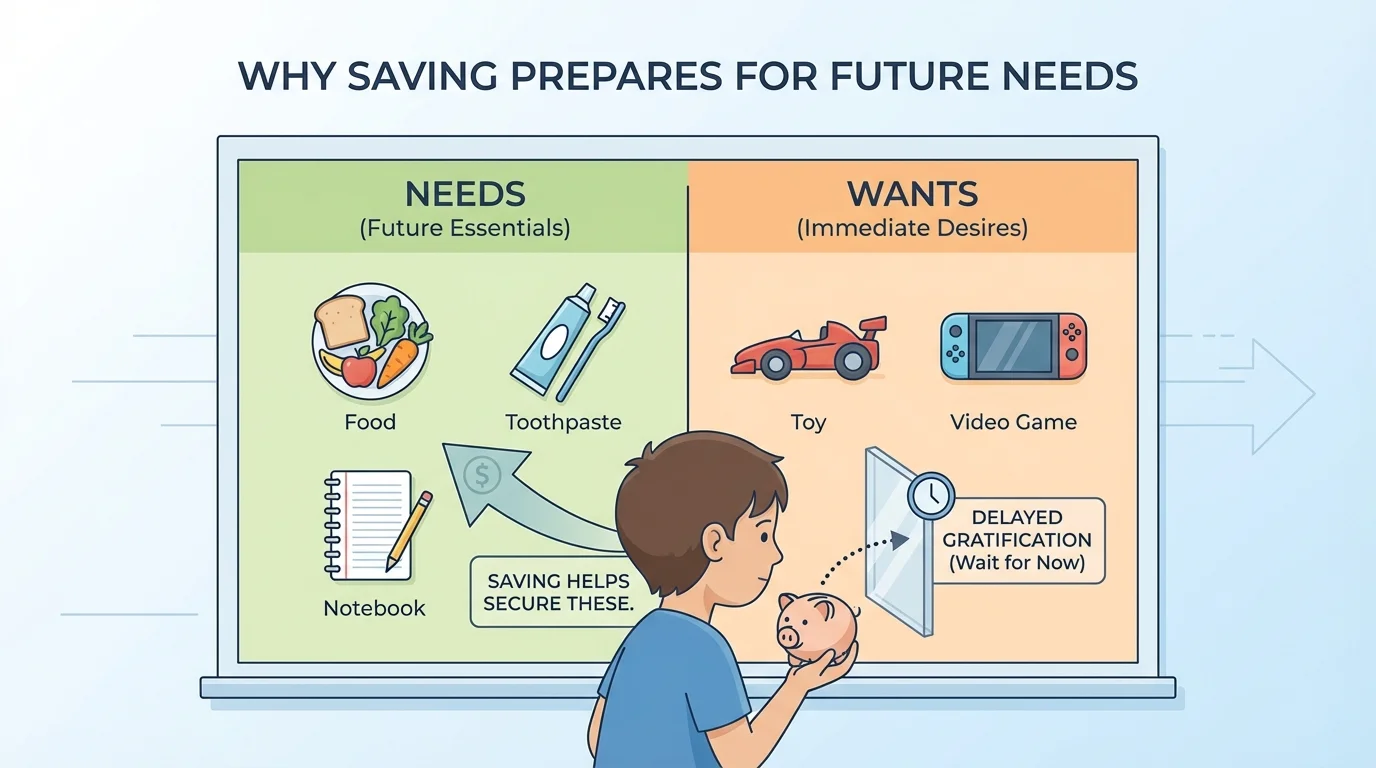

Not everything you want right now is something you truly need. A need is something important for living, learning, health, or safety. A want is something nice to have but not necessary right away. It helps to sort money choices by asking, "Do I need this now, or do I just want it?"

For example, toothpaste, warm clothes, or supplies for your online lessons can be needs. A new game, extra stickers, or a fancy snack may be wants. Wants are not bad. But if you spend all your money on wants, you may not be ready for needs later.

Here is a simple way to think about it: needs should come first. Saving helps make sure money is ready for those first things. Then, if money is left, you can think about wants.

Sometimes a future need is not an emergency. It may just be something you know is coming. Maybe a family birthday is next month and you want to buy a card and small gift. Maybe your art supplies are getting low. Maybe your bike helmet is getting too small. Saving helps you get ready before the moment arrives.

Needs first, wants next

People make stronger money choices when they remember this order: first cover needs, then think about wants. Saving supports this order because it protects money for what matters most.

[Figure 2] If a person never saves, they may feel stuck later. They might say, "I wish I had kept some of my money." Saving gives you more power over your choices.

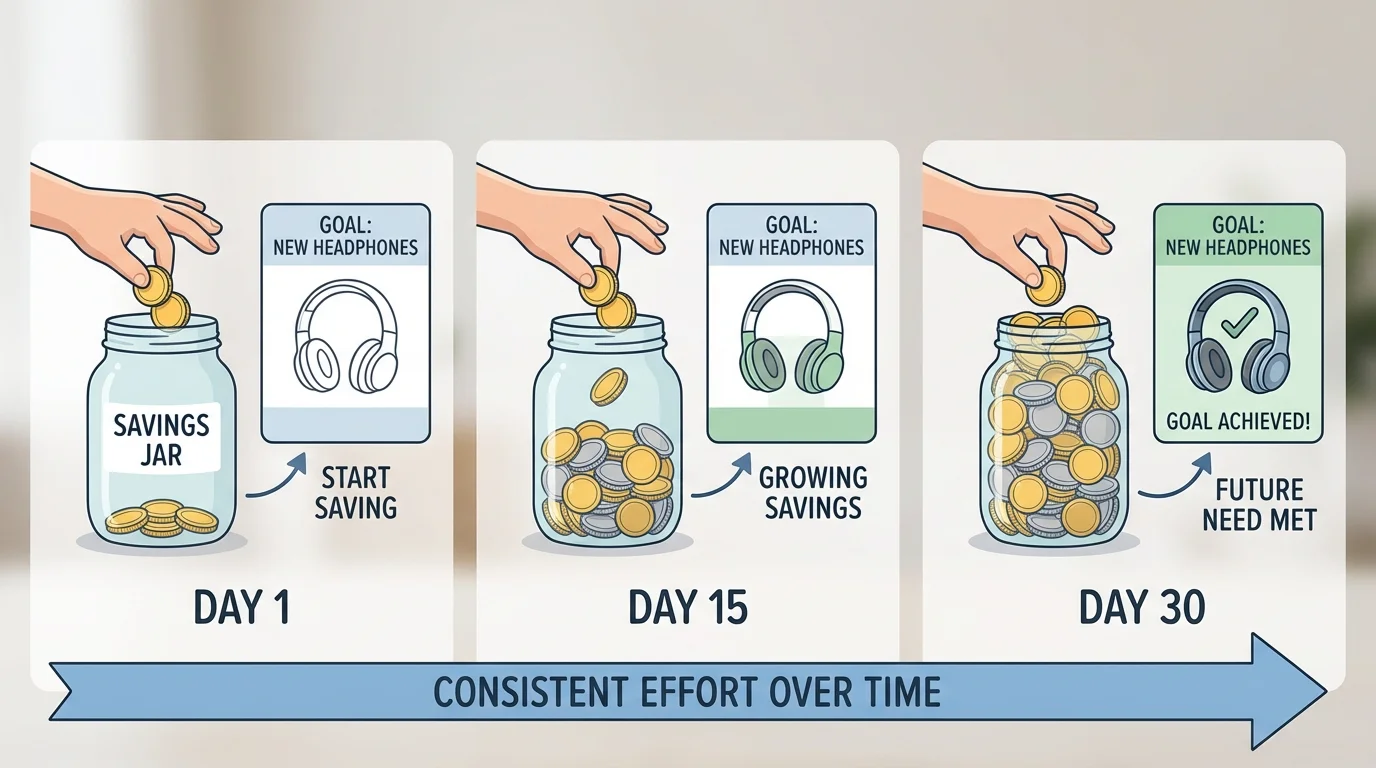

Saving for a goal works well because it gives your money a job. Small amounts saved over time can help you reach something important. Your goal could be a future need, like replacing lost gloves, buying a notebook, or helping pay for something special.

Let's say you want a pair of headphones for your online classes that costs $10. If you save $2 each week, then after five weeks you will have \(2 + 2 + 2 + 2 + 2 = 10\). You do not need all the money at once if you plan ahead.

Now think about a different situation. You spend $2 as soon as you get it every week. After five weeks, you have spent all $10 on small things, and when your old headphones stop working, you have nothing saved. The difference is not how much money came in. The difference is the choice to save.

Saving can also help with surprises. Maybe a water bottle gets lost during an activity outside the home. Maybe a zipper breaks on your backpack. Maybe your pet needs more food sooner than expected. These are times when saved money can be helpful.

When people save, they are preparing for both emergencies and regular plans. An emergency is a sudden problem that needs attention fast. Kids do not usually handle big emergencies alone, but learning to save for small surprises is great practice.

Real-life example: saving for a replacement item

Your pencil case breaks, and a new one costs $6.

Step 1: Check how much money you already have.

You have $2 saved.

Step 2: Find how much more you need.

\(6 - 2 = 4\)

Step 3: Make a simple plan.

If you save $1 each week, then in four weeks you will save \(1 + 1 + 1 + 1 = 4\).

Saving a little at a time helps you solve a real problem.

[Figure 3] Later, the same idea still matters: money grows when you leave it alone and keep adding to it. Saving is not about speed. It is about steady steps.

Saving works best when you follow clear steps. The process shows that saving is something you can do one part at a time, even if you are just beginning.

Step 1: Choose a reason to save. Pick something real. Maybe you want backup markers for art, a birthday gift for a cousin, or money set aside in case something you use often breaks.

Step 2: Decide how much to keep. You do not have to save all your money. Even saving part of it helps. If you get $4, maybe you save $1 and use $3. That is a start because \(4 - 1 = 3\).

Step 3: Put savings in a safe place. A jar, envelope, or box with your name can work at home. A grown-up may also help you use a bank account. The important part is that the money is kept safe and is not mixed with spending money.

Step 4: Keep track. You can make a small chart and color a square each time you save $1. Watching your progress can help you stay excited.

Step 5: Wait until the right time to use it. This is a big part of saving. If you keep taking the money out for little wants, it will not be there for the future need.

Try This

Ask a grown-up for a small container and give it a label such as "future needs," "gift money," or "replace broken things." Then each time you get money, choose one small part to put inside.

These steps are simple, but they are powerful. A plan, a safe place, and patience can turn small coins into useful help.

Sometimes the hardest part of saving is waiting. You may want to spend money right away because something looks fun in the moment. But stopping to think can help.

Ask yourself a few questions: Do I need this now? Will I still want it later? Am I saving for something more important? If the answer is "I am saving for something important," then waiting may be the smarter choice.

| Choice | What happens now | What happens later |

|---|---|---|

| Spend all your money | You get a small item right away | You may not be ready for a future need |

| Save part of your money | You may buy less today | You are more prepared later |

| Save regularly | It takes patience | Your money grows for a real purpose |

Table 1. Comparison of spending choices and their future results.

It is also smart to talk with a trusted grown-up before spending all your money. They can help you think about needs, prices, and saving goals. This does not mean they choose everything for you. It means they help you practice good decisions.

"A little saved today can help a lot tomorrow."

Being careful with money does not mean never having fun. It means using your money on purpose. You can enjoy some now and save some for later.

A budget is a simple plan for how to use money. For a child, that might simply mean deciding: "Some to spend, some to save." It does not need to be complicated.

Habits grow through repetition. If each time you get money, you save a small part first, saving starts to feel normal. Over time, that habit can help you all through life.

You do not need a lot of money to be a saver. Even small amounts count. If you save $1 each week for six weeks, then you will have \(1 + 1 + 1 + 1 + 1 + 1 = 6\). That could help with a small need, a gift, or part of a bigger goal.

Money choices have results. When you plan ahead, you usually have more options later. When you spend without thinking, choices can feel smaller later.

Saving teaches patience, planning, and responsibility. These are money skills, but they are also life skills. They help you prepare, stay calm, and make thoughtful choices.

And that is the big reason saving matters: it helps people prepare for future needs. Saving gives you a way to help your future self. It turns "I hope I'm ready" into "I have a plan."