Two people can both say, "I made $40,000 this year," and still be in completely different financial situations. One may have earned every dollar by working hourly shifts. Another may have received some from a salary, some from investments, and some from renting out property. The amount is only part of the story. Where income comes from matters because different income sources come with different levels of effort, risk, stability, and long-term opportunity.

Understanding income is one of the most important parts of personal financial literacy. As you move toward college, technical training, military service, entrepreneurship, or a career, you will need to know not just how to earn money, but how compensation works and how people build wealth over time. Some income is earned through labor. Some comes from owning assets. Some is steady and predictable. Some can rise quickly or disappear just as fast.

Many teenagers first encounter income through a part-time job, such as working at a restaurant, store, or summer camp. That is a useful beginning, but it is only one form of income. Adults often receive money from multiple sources at the same time. A teacher may earn a salary, receive interest from savings, and earn dividend income from investments. A musician may teach lessons for earned income and collect royalties from songs. A small business owner may earn profit income instead of a traditional paycheck.

Each source of income affects financial planning. A steady paycheck can make budgeting easier. Investment income can grow wealth over time, but it may be uncertain. Business profit can be rewarding, but it often requires risk and hard work before any money is made. Learning to compare these sources helps you understand real career choices and long-term financial independence.

Income is money received from work, investments, business activity, or ownership of assets.

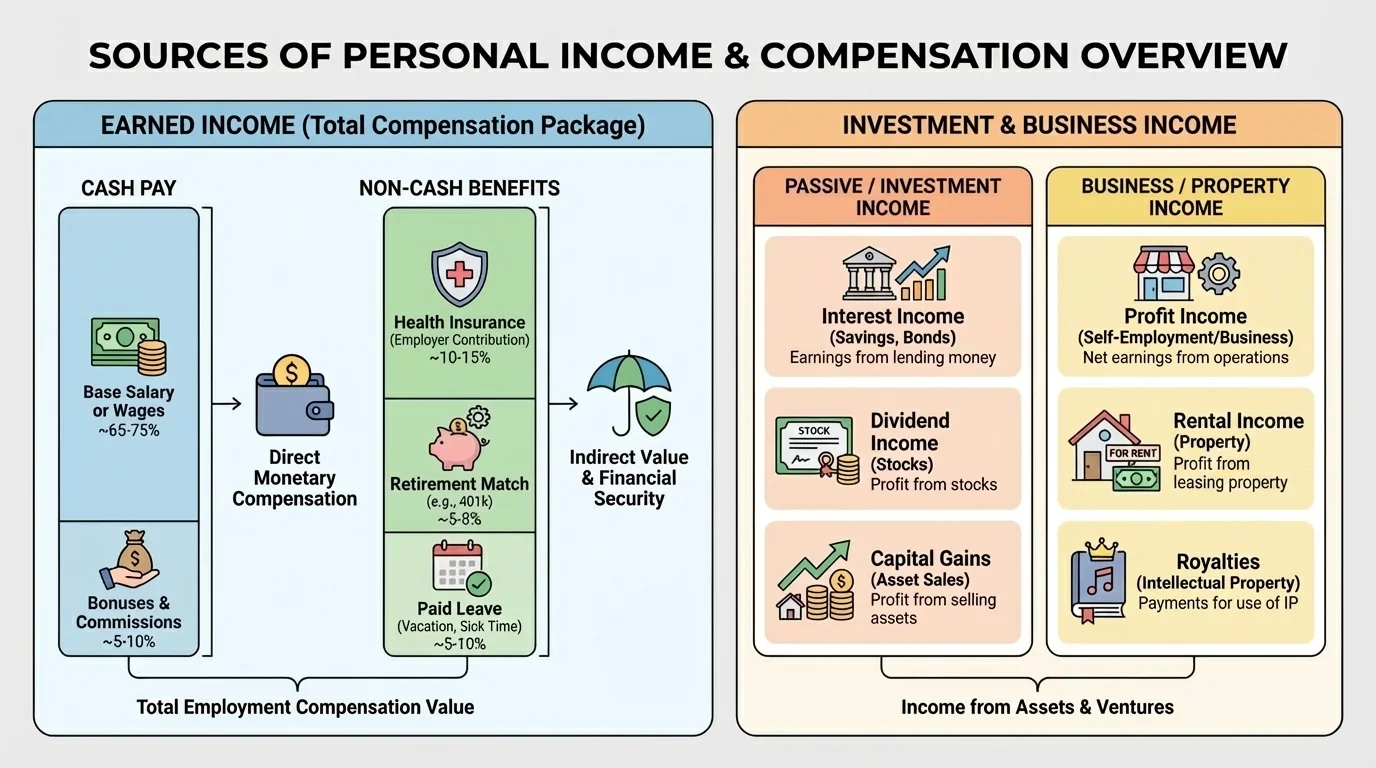

Compensation is the total value a person receives in exchange for work. It includes cash pay and may also include benefits such as health insurance, retirement contributions, or paid time off.

Gross income is income before taxes and deductions. Net income is the amount left after taxes and other deductions are taken out.

When people compare jobs, they often focus only on wages or salary, but that can be misleading. [Figure 1] A job paying $45,000 with strong benefits may be more valuable than a job paying $48,000 with no benefits. Total compensation includes both direct pay and non-cash benefits, which can significantly change the real value of a job.

Salary and wages are both forms of earned pay, but they work differently. A salary is a fixed amount paid over a year, often divided into monthly or biweekly paychecks. Wages are usually based on hours worked. For example, if a student earns $15 per hour and works 20 hours in a week, gross weekly pay is $300 because \(15 \times 20 = 300\).

Compensation can include much more than a paycheck. Employers may offer health insurance, retirement matching, tuition assistance, paid sick days, paid vacation, bonuses, or commissions. For some careers, these benefits are worth thousands of dollars each year. That is why comparing only base pay can lead to poor decisions.

Another useful distinction is between earned income and passive income. Earned income usually requires your ongoing time and labor. A paycheck from a job is earned income. Passive income generally comes from owning something that continues to generate money with less day-to-day effort, such as investments or royalties. However, "passive" does not mean "effort-free." Rental property, for example, may still require management and repairs.

As students think about the future, one major question is this: do you want income that depends mainly on your time, or income that can continue because you own assets or legal rights? Most adults use a combination of both.

Many high-income careers do not simply pay more per hour; they also include stronger benefits, more predictable schedules, and better opportunities for raises over time. That means the gap in lifetime earnings can become much larger than the starting salary difference suggests.

The value of compensation also depends on taxes and deductions. If someone earns gross pay of $800 in a week and $150 is taken out for taxes and other deductions, net pay is $650 because \(800 - 150 = 650\). A worker spends net income, not gross income, so both numbers matter.

Earned income is money received from labor. This includes wages, salary, tips, commissions, bonuses, and self-employment earnings. For most people, earned income is the first and largest source of money. It is also usually the most predictable, especially when someone works a regular schedule or has a salaried position.

There are several common forms of earned income. Hourly wages pay a set amount for each hour worked. Salaries pay a fixed annual amount. Tips are common in service jobs. Commissions reward workers based on sales. Bonuses may be paid for strong performance or company success. Some jobs combine these. A car salesperson, for example, may receive a base salary plus commissions.

Earned income often increases with skill, experience, and education. A certified welder, a registered nurse, a software developer, and an electrician can all earn more than entry-level workers because their jobs require training and specialized ability. This does not mean every college degree leads to high income or that every skilled trade pays less than a four-year degree. It means preparation matters. People who build in-demand skills usually have stronger earning power.

Earned income has strengths and limits. Its main strengths are stability and clarity. You usually know when you will be paid and roughly how much to expect. Its main limit is that income is tied closely to time and work. If you stop working, the income often stops too.

Comparing hourly pay and annual salary

A student is deciding between two early-career opportunities. One job pays $18 per hour for 40 hours per week over 50 weeks. Another offers a salary of $39,000.

Step 1: Find the yearly pay for the hourly job.

\(18 \times 40 = 720\) dollars per week.

\(720 \times 50 = 36{,}000\) dollars per year.

Step 2: Compare the totals.

The hourly job produces $36,000, while the salary job pays $39,000.

Step 3: Think beyond the numbers.

If the salary job also includes health insurance or paid vacation, its total compensation may be worth even more.

The salary job pays more in direct annual income, but the full comparison should include benefits, schedule, and opportunities for advancement.

As shown earlier in [Figure 1], cash earnings are only part of total compensation. That matters especially when comparing careers that offer retirement plans, professional development, or employer-paid insurance.

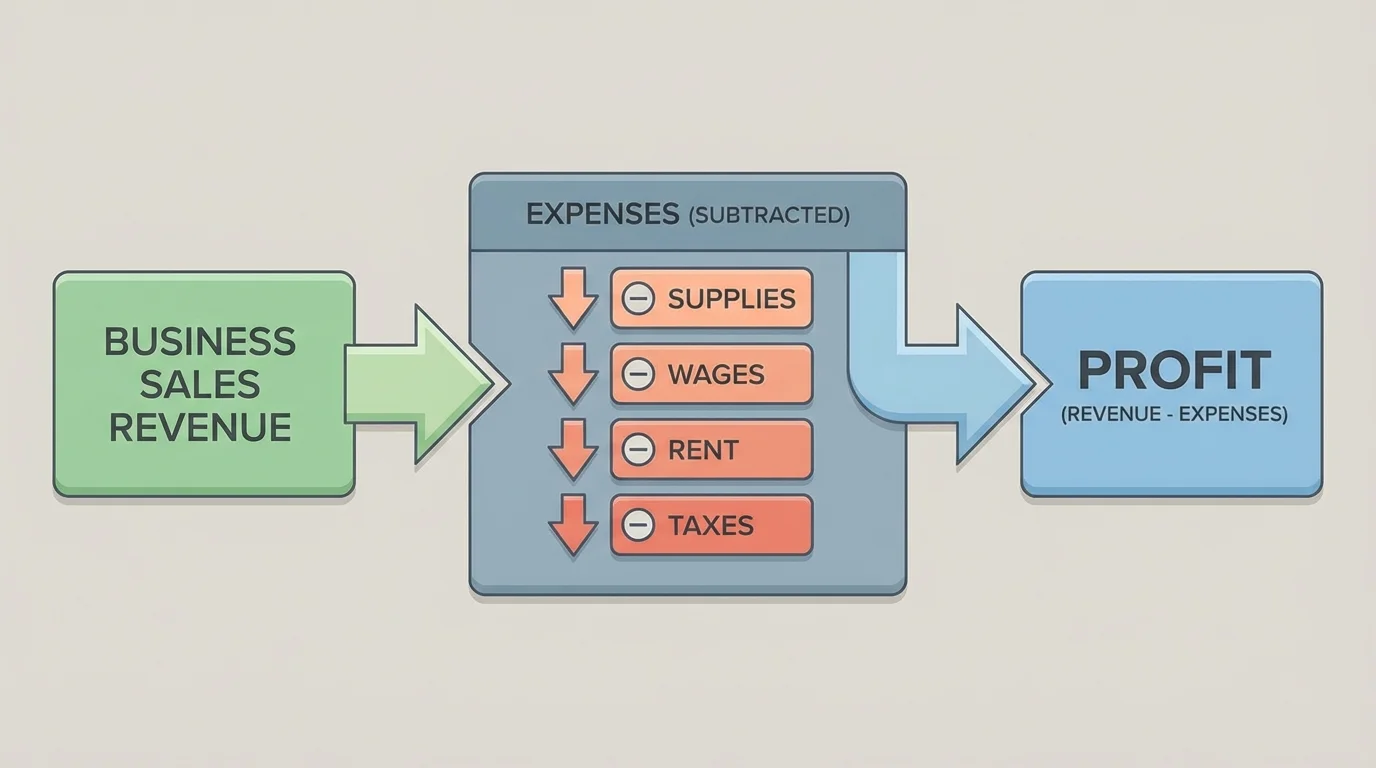

Profit income comes from operating a business. It is the money left after a business subtracts expenses from revenue. The core relationship is simple: revenue comes in from sales, expenses go out for costs, and the remaining amount is profit.

[Figure 2] If a student runs a small lawn-care business and earns $2,000 from customers in a month, that amount is revenue. If fuel, equipment repairs, advertising, and supplies cost $600, then profit is $1,400 because \(2{,}000 - 600 = 1{,}400\). That profit can be used as personal income, saved, or reinvested in the business.

Profit income can be powerful because it is not strictly limited by hourly pay. A successful business can grow beyond what one person can earn by trading time for money. However, profit income is also riskier than a paycheck. Sales may vary from month to month. Owners may lose money if expenses are too high or demand drops.

Entrepreneurship appeals to people who want independence, innovation, and possibly high rewards. But business ownership usually requires planning, market knowledge, discipline, and resilience. A business owner may work very hard before earning consistent profit.

Why profit income differs from earned wages

When someone is an employee, the employer usually carries much of the business risk. The employee receives wages or salary even if sales are temporarily weak. When someone owns the business, that person may gain more if the business succeeds, but also bears more of the losses if it fails. Profit income therefore offers higher upside and higher uncertainty.

Career preparation matters here too. Business courses, accounting knowledge, digital marketing, communication, and industry-specific skills can increase the chances that a business becomes profitable. Continuing education can help entrepreneurs adapt when markets or technology change.

Interest income is money earned from lending money or depositing it in interest-paying accounts. Banks may pay interest on savings accounts or certificates of deposit. Governments and companies may pay interest to people who buy bonds. In simple terms, interest is the price paid for using someone else's money.

Suppose you deposit $1,000 in a savings account that pays \(4\%\) annual interest. After one year, simple interest would be $40 because \(1{,}000 \times 0.04 = 40\). Your total would become $1,040. Interest income is usually more stable than stock-market gains, but the return is often lower.

Interest is important because it rewards saving and patience. However, inflation can reduce its real value. If your savings earn \(2\%\) interest but prices rise by \(3\%\), your money grows in dollars but loses purchasing power. That is why savers compare interest rates to inflation.

Interest income is usually considered more predictable than profit income or capital gains, but it rarely creates rapid wealth by itself unless a person has a large amount of money invested. For many people, it functions as a steady but modest income source.

Dividend income comes from owning shares of certain companies. A dividend is a payment a corporation gives to shareholders, usually from profits. Not all companies pay dividends. Some reinvest earnings back into the business instead.

If an investor owns 100 shares of a company and the company pays a dividend of $1.20 per share for the year, total dividend income is $120 because \(100 \times 1.20 = 120\). That income may be spent or reinvested to buy more shares, which can increase future dividend income.

Dividend income can be attractive because it combines ownership with the possibility of regular payments. However, dividends are not guaranteed. A company can reduce or eliminate them if profits decline or if leadership decides to use the money elsewhere.

Dividend-paying investments are common in long-term wealth-building strategies. They may appeal to people who want income from assets they own rather than from direct labor. Still, stock prices can fall, so dividend income carries risk along with opportunity.

Comparing interest income and dividend income

A student has $2,000 to invest. Option A is a savings account paying \(3\%\) annual interest. Option B is a stock investment expected to pay a \(4.5\%\) annual dividend, though the stock price may change.

Step 1: Find the interest income for Option A.

\(2{,}000 \times 0.03 = 60\)

Interest income is $60 for one year.

Step 2: Find the expected dividend income for Option B.

\(2{,}000 \times 0.045 = 90\)

Expected dividend income is $90 for one year.

Step 3: Compare risk.

The dividend income is higher, but the stock value may rise or fall. The savings account is usually more stable.

Higher potential income often comes with higher uncertainty.

This pattern appears across many financial choices: lower-risk income is often lower-return, while higher-return opportunities often involve more uncertainty.

Rental income is money earned from allowing someone else to use property you own, such as an apartment, house, farmland, storage unit, or equipment. At first glance, rental income may seem simple because a tenant pays rent every month. In reality, the owner must subtract costs to find the true income.

If a property brings in $1,200 per month in rent, that is gross rental income. But suppose maintenance costs are $150, property taxes and insurance average $200 per month, and other expenses total $100. Net rental income is $750 because \(1{,}200 - 150 - 200 - 100 = 750\).

Rental income can be a strong long-term income source because the owner may receive monthly cash flow while also holding an asset that could increase in value. But it has risks. Tenants may leave, repairs may be expensive, and property values can decline. Rental income also often requires management, even when a property manager is hired.

For many adults, rental income becomes possible only after years of saving, borrowing carefully, and learning about the real estate market. It is not "easy money." It is ownership-based income that can be rewarding when managed well.

Capital gains occur when an asset is sold for more than its purchase price. Assets can include stocks, bonds, real estate, collectibles, or even a business. If someone buys an investment for $500 and later sells it for $650, the capital gain is $150 because \(650 - 500 = 150\).

A key idea is the difference between realized and unrealized gains. If the asset has increased in value but has not been sold, the gain is unrealized. Once it is sold, the gain becomes realized. This matters because price increases on paper are not the same as money actually received.

Capital gains can be significant, especially over long periods. For example, a stock or property may grow in value for years. But this income source is less predictable than earned income. Prices can rise, stay flat, or fall. Someone depending only on capital gains may have an uncertain financial life.

Capital gains are also different from dividends and interest. Dividends and interest can produce income while you continue owning the asset. Capital gains generally require selling the asset to receive the gain.

Royalties are payments made to someone for the use of property they created or own, especially intellectual property. This can include music, books, photography, inventions, software, trademarks, patents, and mineral rights.

A songwriter might earn royalties each time a song is streamed or used in a commercial. An author might earn royalties on each book sold. An inventor may receive royalties when a company licenses a patent. This means a person can continue earning income long after the original work was created.

Royalties are interesting because they connect income to creativity and ownership. A person may do the hard work once, then receive income repeatedly if others keep using the work. But royalty income is often uncertain. Many creative products earn little or nothing, while a few become very successful.

In the modern economy, royalties matter even more because digital media, apps, online content, and licensing agreements create new ways for people to earn from ideas. Education in technology, law, design, engineering, or the arts can make this kind of income more possible.

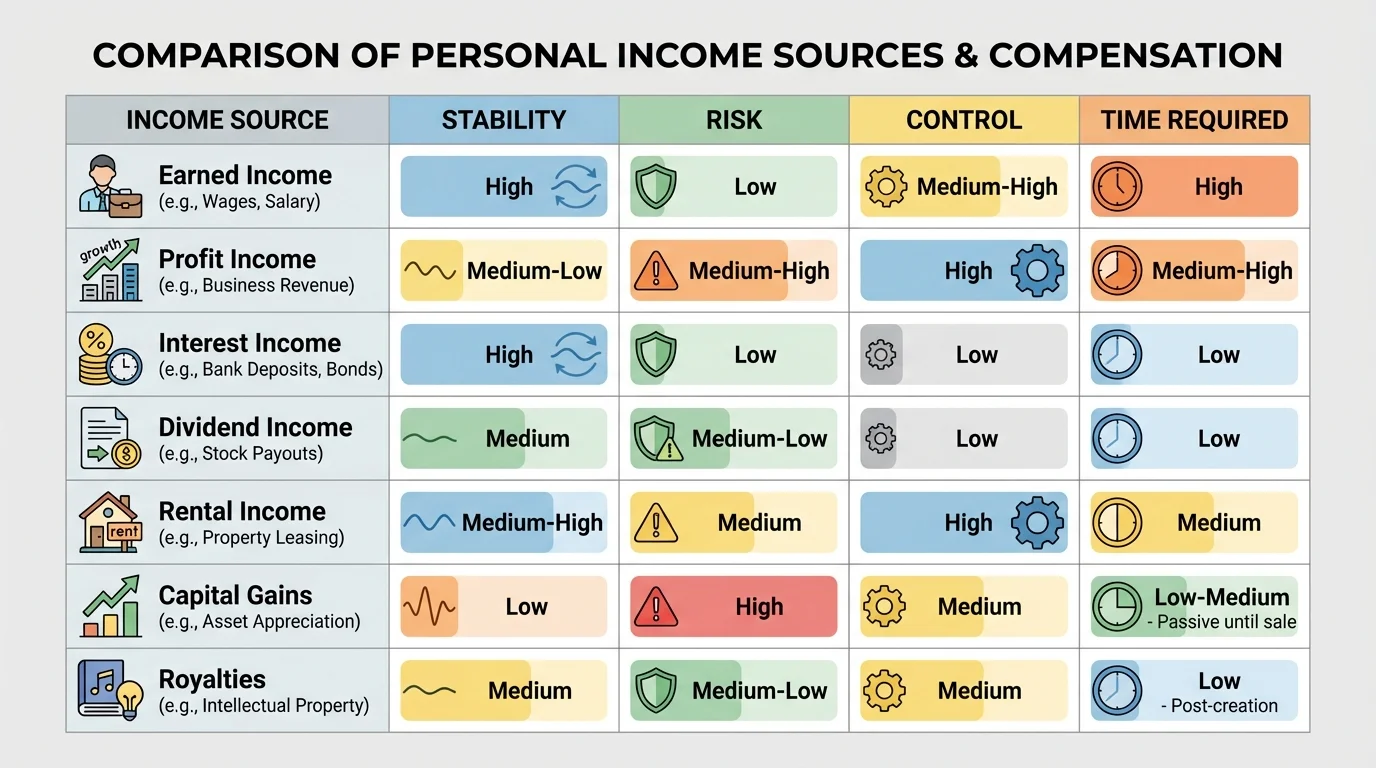

Looking at these categories side by side makes the differences clearer. The comparison in [Figure 3] organizes the major trade-offs: some income sources are stable but limited, while others offer greater growth potential but also more uncertainty.

| Income source | Where it comes from | Typical stability | Typical risk | Time involvement |

|---|---|---|---|---|

| Earned income | Labor and work | Usually high | Usually lower | High ongoing involvement |

| Profit income | Business ownership | Varies | High | High involvement, especially early |

| Interest income | Savings or lending | Usually high | Usually lower | Low involvement |

| Dividend income | Ownership of stock | Moderate | Moderate | Low involvement |

| Rental income | Property ownership | Moderate | Moderate to high | Moderate involvement |

| Capital gains | Asset value increase | Low predictability | Moderate to high | Low daily involvement |

| Royalties | Intellectual property rights | Varies widely | High uncertainty | Low after creation, high upfront effort |

Table 1. Comparison of major personal income sources by origin, stability, risk, and time commitment.

None of these income sources is automatically "best." The best choice depends on goals, age, skills, risk tolerance, and available resources. A young adult may rely mainly on earned income while building savings. Later, that person may add dividends, interest, or rental income. Someone with a strong business idea may focus on profit income. A creative professional may combine wages with royalties.

Notice that control also differs. Employees may have less control over pay structure but more predictable income. Business owners and investors may have more control over decisions but face more financial uncertainty. Income sources often trade stability for flexibility or growth potential.

Earlier financial literacy topics often stress budgeting and saving. Those skills still matter here. The ability to manage earned income well is often what makes future investing, business ownership, or asset building possible.

Another important difference is scalability. Earned income often grows step by step through raises and promotions. Asset-based income, such as dividends or rental income, may scale more as ownership expands. That is one reason people who save and invest consistently may develop more income options over time.

Your future income is shaped not only by what job you choose, but by how well you prepare for it and how willing you are to keep learning. Career preparation includes education, technical training, certifications, internships, apprenticeships, networking, and building professional habits. These investments can increase both starting income and future opportunities.

Suppose one graduate enters a job paying $32,000 per year and receives small raises, while another completes specialized training and begins at $45,000 with stronger promotion opportunities. Over many years, the difference can become very large. Lifetime earning potential is not just one paycheck; it is the total income a person can reasonably earn across decades.

Continuing education matters because economies change. New technology can increase demand for some skills and reduce demand for others. Workers who update their knowledge often stay more competitive. This may involve college courses, trade certifications, employer training, online courses, industry licenses, or learning new software and tools.

How additional training can affect income

Two workers start in related fields. Worker A earns $35,000 and receives annual raises of $1,000. Worker B spends time on advanced certification, begins at $40,000, and receives annual raises of $1,500.

Step 1: Write each worker's pay after 5 years.

Worker A: \(35{,}000 + 5(1{,}000) = 40{,}000\)

Worker B: \(40{,}000 + 5(1{,}500) = 47{,}500\)

Step 2: Compare the difference after 5 years.

\(47{,}500 - 40{,}000 = 7{,}500\)

Step 3: Think long term.

If this pattern continues over decades, the total lifetime earnings gap can become much larger.

Education and training do not guarantee wealth, but they often increase access to higher-paying and more adaptable careers.

Career preparation can also affect which types of income are available to you. A person with strong financial knowledge may be more comfortable investing. A skilled entrepreneur may be able to create profit income. A software developer or musician may create products that earn royalties. Better preparation widens options.

Whenever you evaluate a job, side hustle, business, or investment, ask careful questions. Is the income stable or unpredictable? How much time does it require? What expenses reduce the true amount earned? What risks exist? Does the opportunity build useful skills or future options?

For example, an hourly job paying $17 per hour may seem better than one paying $15, but if the lower-paying job offers tuition support, a safer work environment, and better advancement opportunities, it might have greater long-term value. In the same way, an investment promising high returns may not be wiser if the risk of loss is extremely high.

Students should also be cautious about claims of "easy passive income." Most reliable income sources involve one or more of the following: labor, skill, ownership, risk, time, or capital. If an opportunity promises large profits with no effort, no risk, and no expertise, that is usually a warning sign rather than a shortcut to wealth.

"Do not save what is left after spending, but spend what is left after saving."

— Warren Buffett

Building financial strength usually begins with earned income, wise spending, and steady saving. Over time, those habits can make room for investment income, business ownership, or other forms of compensation and wealth creation. The goal is not just to make money today, but to create choices for the future.