A loan can open a door or trap someone in a cycle of payments. The same tool that helps one person buy a reliable car or attend college can push another person into expensive debt that lasts for years. That is why borrowing is never just about getting money now. It is about deciding whether the future cost, risk, and purpose make sense.

People borrow for many reasons: school, transportation, housing, emergencies, and major purchases. Some loans are designed for long-term goals and usually come with lower costs. Others are meant for short-term cash needs but can become extremely expensive. A smart borrower compares the purpose of the loan, the cost of the loan, the payoff plan, and the tradeoffs involved before signing anything.

Borrowing allows a person to use money now and repay it later. That can be helpful when the item being purchased is important, lasts a long time, or may increase future opportunities. For example, borrowing for education or a home may have long-term value. Borrowing for a fast purchase with no lasting benefit can be much harder to justify.

Not all debt is the same. A low-interest student loan used to earn a degree is different from a high-cost payday loan used to cover a few days of expenses. Even if both involve borrowing money, they differ in purpose, structure, and risk. Good financial decisions depend on understanding those differences instead of treating every loan as if it works the same way.

Principal is the amount of money borrowed. Interest is the price paid for borrowing that money. APR, or annual percentage rate, is a broader measure of borrowing cost that usually includes interest and may include certain fees. Term is the length of time given to repay the loan. Collateral is property a borrower promises to the lender, such as a car or house, that can be taken if the loan is not repaid.

These terms matter because borrowers often focus only on the monthly payment. But the monthly payment is just one piece of the decision. A smaller payment may seem attractive while hiding a longer term, more interest, and a much higher total cost.

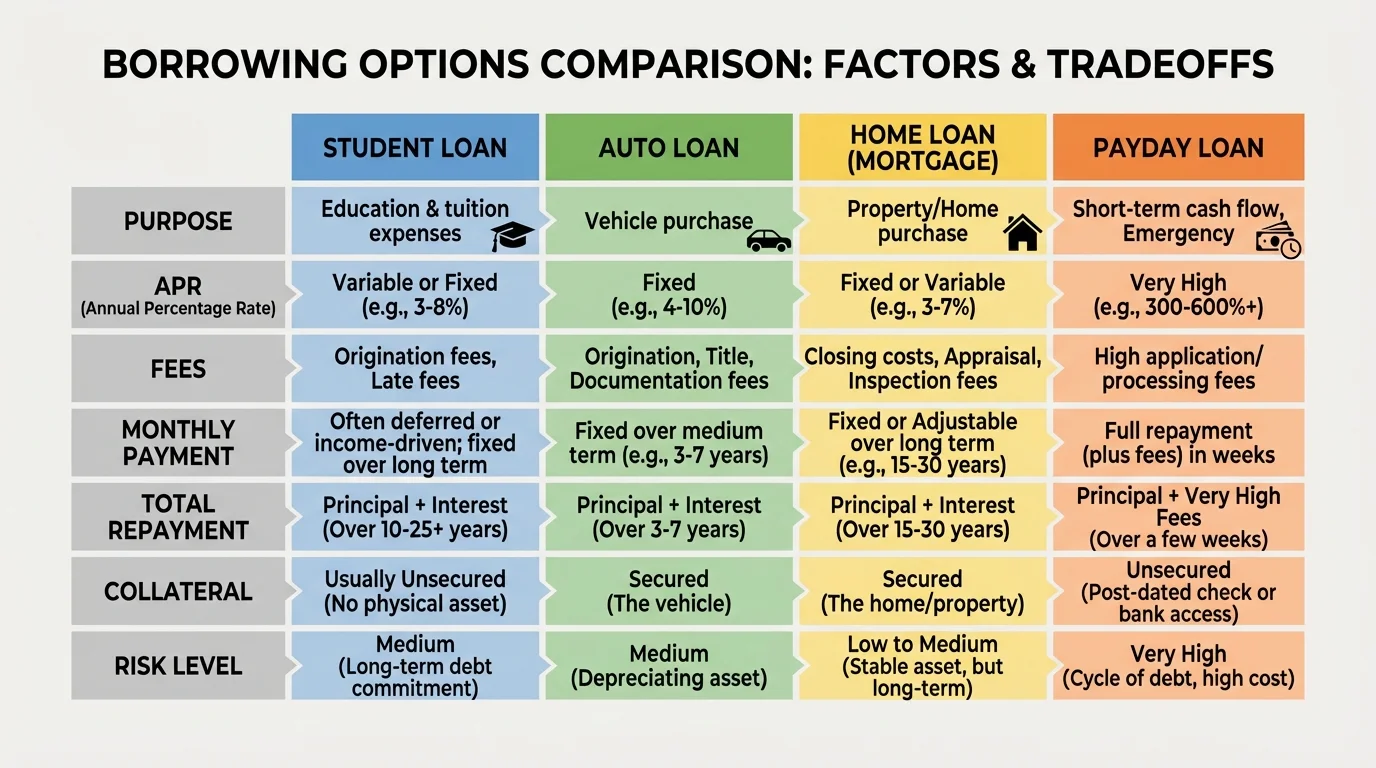

When comparing loans, a borrower should look at several factors together, as [Figure 1] illustrates: the reason for borrowing, the interest rate, the fees, the length of repayment, whether collateral is required, and the total amount that will eventually be paid back. Looking at only one factor can lead to a poor choice.

The first major factor is APR. A lower APR generally means borrowing costs less over time, although the exact total still depends on the amount borrowed and the term. The second factor is fees. Some loans include origination fees, late fees, service charges, or penalties. A loan with a moderate interest rate but many fees may cost more than expected.

A third factor is relevance. A loan should fit the purpose. Borrowing for a house usually requires a long-term mortgage because homes are expensive and last for decades. Borrowing for a small emergency with a payday loan may seem relevant because it is fast, but the cost can be so high that it creates a bigger problem than the original emergency. Relevance means asking, "Is this type of loan designed for this need, and is there a better option?"

A fourth factor is the repayment plan. Borrowers need to know how much they will pay each month, how long repayment will last, and how much of their future income will be tied up. If a loan payment makes it hard to cover food, transportation, or savings, then the loan may be unaffordable even if approval is possible.

A fifth factor is tradeoffs. Every borrowing choice involves giving something up. A longer term often lowers the monthly payment, but it usually increases the total amount repaid. A secured loan may offer a lower interest rate, but it puts property at risk. Fast approval may come with very high costs. There is rarely a perfect option; the goal is to choose the least harmful and most useful one.

Monthly payment is not the whole story. Borrowers sometimes choose the loan with the lowest monthly bill because it feels easier to manage. However, if that lower payment comes from stretching the loan over more months, the borrower may pay far more in total. Financially, the best loan is often the one that balances affordability with the lowest reasonable total cost.

Another important consideration is how borrowing affects a person's credit score. Making payments on time can help build credit history. Missing payments can damage credit, making future borrowing more expensive or harder to get. In that sense, one borrowing decision can shape many future financial opportunities.

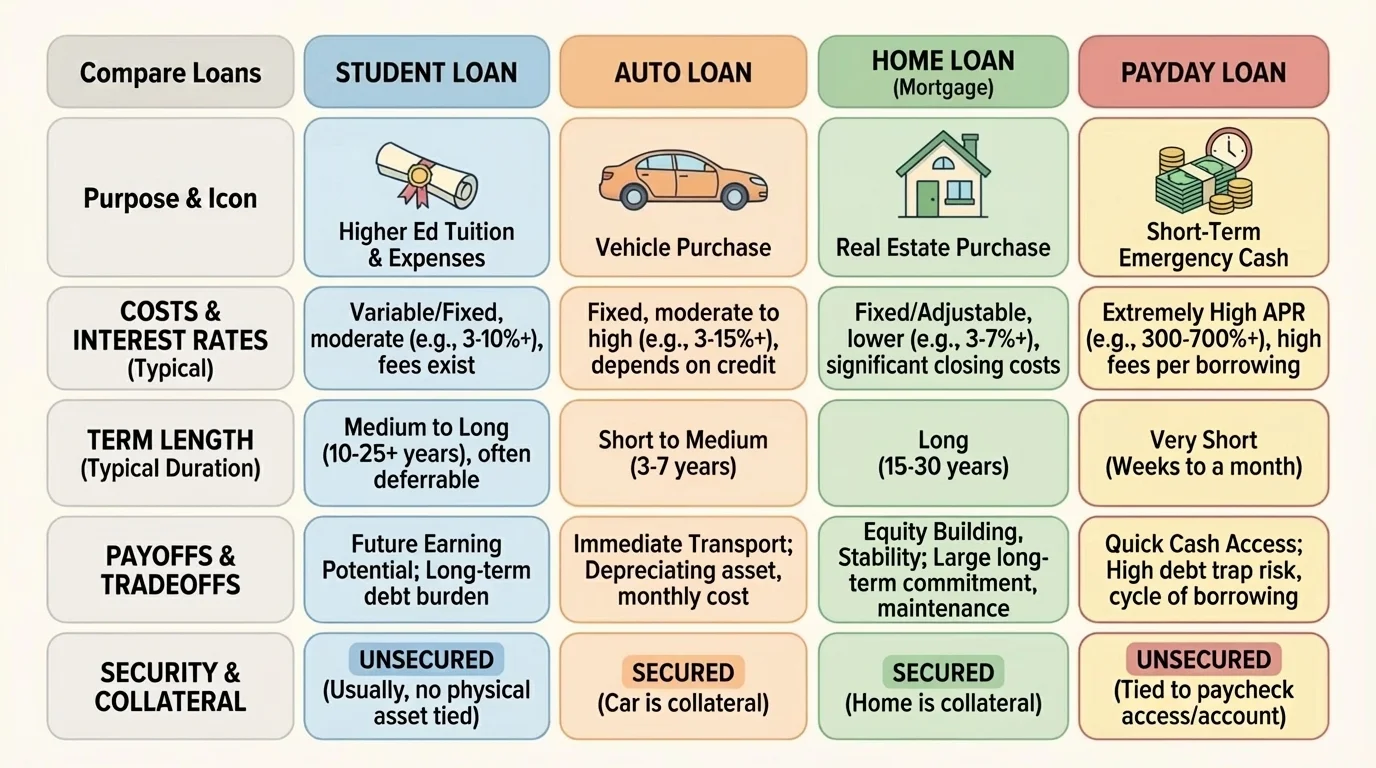

Different loan types exist because people borrow for different reasons. Student, auto, home, and payday loans serve very different purposes, as [Figure 2] shows, and they should not be compared only by how quickly money is available. Their terms, risks, and expected uses are very different.

Student loans are usually used to pay for education-related costs such as tuition, books, housing, and fees. Federal student loans often have lower interest rates than many other unsecured loans and may offer flexible repayment options. Their relevance can be high if the education increases earning potential. However, the payoff may take many years, and borrowing too much can create major stress after graduation.

Auto loans are used to buy a vehicle. They are often secured by the car itself, meaning the lender can repossess the car if payments are missed. Auto loans can be useful when reliable transportation is necessary for school or work. Still, cars lose value over time, so borrowing too much for a car can mean paying for an asset that is depreciating.

Home loans, often called mortgages, are usually the largest loans people take. They are secured by the house. Mortgages often have lower interest rates than many other loans because the lender has strong collateral, but the term may be very long, such as 15 or 30 years. A home loan may be relevant when buying a home is realistic and stable income exists, but it also creates a long-term obligation.

Payday loans are short-term loans typically meant to be repaid by the borrower's next paycheck. They may seem convenient, but they often have extremely high fees and very high effective annual borrowing costs. They are one of the clearest examples of a risky borrowing option because a small loan can quickly become difficult to repay, leading borrowers to renew or roll over the debt.

| Loan type | Common purpose | Typical term | Secured? | Risk level | Key tradeoff |

|---|---|---|---|---|---|

| Student loan | Education costs | Several years | Usually no | Moderate | May improve future income, but repayment can last a long time |

| Auto loan | Vehicle purchase | 5 to 7 years | Usually yes | Moderate | Provides transportation, but the car loses value |

| Home loan | Home purchase | 15 to 30 years | Yes | Moderate to high | Builds ownership over time, but creates a long obligation |

| Payday loan | Short-term cash need | Days or weeks | Usually no | Very high | Fast cash, but extremely expensive |

Table 1. Comparison of major loan types by purpose, term, collateral, risk, and tradeoffs.

Notice that the "best" loan depends on the situation. A mortgage is not better than a student loan in every case, and an auto loan is not automatically wise just because it is common. The right question is whether the loan fits the goal and whether the borrower can handle the future payments without harming other financial needs.

Cost includes more than the amount borrowed. It includes interest and fees over time. One simple way to estimate interest in basic comparisons is to think of it as principal multiplied by rate and time. In a simplified form, the idea is \[\textrm{Interest} = \textrm{Principal} \times \textrm{Rate} \times \textrm{Time}\]. Although real loans often use more complex calculations, this basic relationship helps students see why larger balances, higher rates, and longer terms all increase cost.

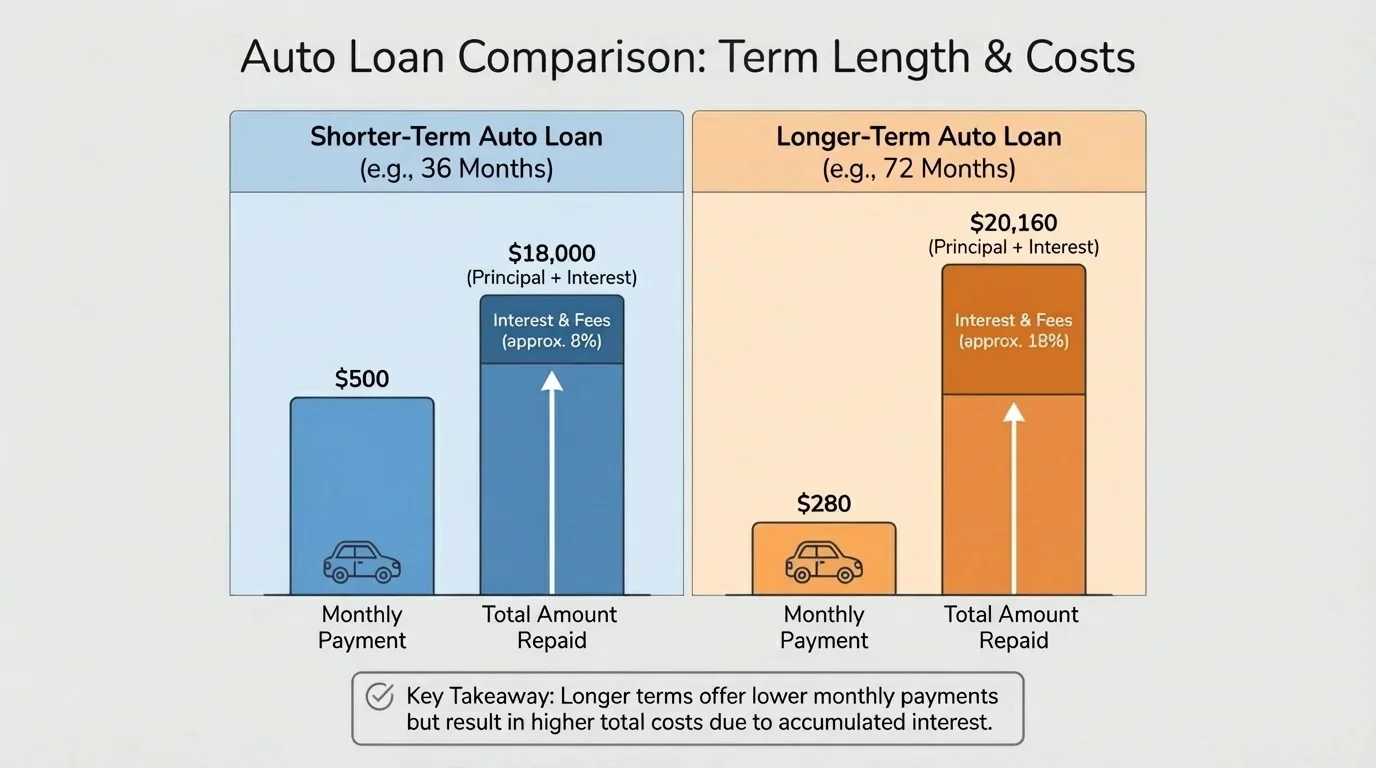

Suppose a borrower takes a $20,000 auto loan. If one option leads to total repayment of $22,400 and another leads to total repayment of $25,600, the second option costs $3,200 more overall, even if its monthly payment is lower. This is exactly the kind of tradeoff shown earlier in [Figure 1]: affordability in the short run can increase cost in the long run, and [Figure 3] compares this pattern in a shorter-term and a longer-term auto loan.

Worked example: comparing two auto loans

A borrower needs $20,000 for a car and is choosing between two options.

Step 1: Identify the total repayment for each option.

Loan A requires 48 monthly payments of $470. Loan B requires 72 monthly payments of $355.

Step 2: Calculate total repayment.

For Loan A, total repayment is \[48 \times 470 = 22{,}560\]. For Loan B, total repayment is \[72 \times 355 = 25{,}560\].

Step 3: Compare the extra cost.

The difference is \[25{,}560 - 22{,}560 = 3{,}000\]. Loan B costs $3,000 more overall.

Loan B feels easier each month, but Loan A is cheaper in total if the higher monthly payment fits the budget.

The lower monthly payment does not automatically mean the better deal. This is one of the most common mistakes borrowers make when shopping for cars, furniture, phones, and other financed purchases.

Fees also matter. A loan with a low advertised rate may include application charges, origination fees, late penalties, or add-on products such as credit insurance. Borrowers should ask for the full repayment schedule and read the agreement closely. If key costs are hard to find, that is a warning sign.

Payday loans are especially important to examine closely. A borrower might take a $300 payday loan and owe a fee of $45 in just two weeks. That sounds small at first, but it means paying $45 to borrow only $300 for a very short time. If the borrower cannot repay on time and must borrow again, the fees can pile up fast. This is why many financial experts view payday lending as a last resort or something to avoid entirely.

Many borrowers focus on whether they can make the next payment, not on how much the loan will cost in total. Lenders know this, which is why advertisements often emphasize "low monthly payments" more than full repayment amounts.

Student loans also require careful cost analysis. If a student borrows $8,000 per year for four years, the total principal borrowed is \[4 \times 8{,}000 = 32{,}000\]. That does not include the interest that may be paid later. Borrowing for education can be worthwhile, but students should compare expected debt to likely earnings, graduation plans, and other financial aid options.

The word opportunity cost means the value of what a person gives up by choosing one option over another. In borrowing, this can mean lost chances to save, invest, or spend on other priorities because income must go toward debt payments.

For example, if a graduate pays $350 each month on student loans, that $350 cannot also go to an emergency fund, retirement savings, or rent. If someone takes on a large auto payment, that may limit the ability to travel, move out, or handle surprise expenses. Borrowing is never only about the present purchase; it changes future choices.

Paying off a loan early can reduce total cost. If a loan does not charge a prepayment penalty, making extra payments can reduce how much interest accumulates over time. This strategy is often useful for high-interest debt because extra money goes toward reducing the balance faster.

Still, early payoff is not always the first priority. A borrower also needs emergency savings and enough cash to cover basic bills. Sending every extra dollar to debt while having no emergency cushion can cause a new borrowing problem later. Good financial judgment requires balancing debt payoff with savings and everyday needs.

For secured loans, repayment risk includes property risk. Missing auto payments can lead to repossession. Missing mortgage payments can lead to foreclosure. That makes these loans potentially lower in interest than unsecured borrowing, but higher in consequences if the borrower falls behind.

Some lenders are transparent and regulated. Others use confusing language, pressure tactics, or expensive terms that borrowers may not fully understand. A predatory lending practice is one that takes unfair advantage of borrowers through excessive fees, misleading terms, or structures that make repayment unusually difficult.

Warning signs include guaranteed approval without checking ability to repay, pressure to sign quickly, unclear fees, repeated refinancing offers, and loans that solve a short-term problem by creating a larger long-term debt burden. Payday loans often raise these concerns because they are easy to access but very costly.

Budgeting matters before borrowing. A borrower should already know roughly how much income comes in each month, how much is committed to fixed expenses, and how much flexibility remains. Without a budget, it is hard to tell whether a loan payment is realistic.

Smart borrowing habits include comparing multiple lenders, checking the APR, asking about all fees, reading the full contract, understanding the monthly payment, and calculating the total repayment. It is also wise to ask whether saving first, buying used, delaying the purchase, or using an emergency fund would avoid the need to borrow at all.

Another good habit is matching the loan to the life of the item. It usually makes little sense to keep paying for something long after it has lost its usefulness. For example, financing a rapidly depreciating item for too many years can lead to paying for value that is already gone.

A practical borrowing decision can be made by following a sequence of steps. First, identify the need. Is it education, transportation, housing, or a temporary cash shortage? Second, ask whether borrowing is necessary or whether another strategy is possible. Third, compare loan types that actually fit the purpose. Fourth, compare total costs, not just monthly payments. Fifth, consider the consequences if income drops or an emergency happens.

Suppose a student needs transportation to get to a part-time job and school. A reasonable comparison might include buying a less expensive used car with a small auto loan, saving longer before buying, or using public transportation temporarily. A payday loan would usually be irrelevant and dangerous for this goal because it is short-term, costly, and not designed to finance a car purchase.

Case study: choosing among borrowing options

Tiana needs reliable transportation for work. She has three choices: a $6,000 used car with a small auto loan, a $14,000 car with a larger auto loan, or a payday loan to cover a down payment gap.

Step 1: Check relevance.

An auto loan matches the purpose because it is designed for vehicle purchases. A payday loan does not match the purpose well because it is short-term and very expensive.

Step 2: Compare affordability and total cost.

The smaller car loan may produce a lower balance and lower total repayment. The larger car may have features she wants, but it ties up more monthly income.

Step 3: Consider tradeoffs.

The cheaper car may be less attractive now, but it may leave room in her budget for insurance, fuel, repairs, and savings. That tradeoff may be more financially sound.

The most responsible choice is likely the modest auto loan if the car is dependable and the payment fits her budget.

The same logic applies to student borrowing. A student should compare the expected return of the education path with the likely debt burden. Borrowing a manageable amount for a program that leads to a strong job market may be reasonable. Borrowing heavily without a clear completion plan or career path raises the risk.

Earlier, [Figure 2] distinguished loan types by purpose and risk. That distinction matters because selecting the wrong category of loan can be just as harmful as selecting the wrong lender. Even before comparing rates, the borrower should make sure the type of borrowing fits the goal.

Finally, wise borrowers recognize that the best borrowing option is sometimes no borrowing at all. Delaying a purchase, choosing a cheaper version, applying for scholarships, increasing savings, or building an emergency fund can reduce dependence on loans and protect future freedom.

"The real cost of borrowing is not what you get today. It is what tomorrow's income must pay for."