Have you ever seen coins in a jar, money at a store, or a grown-up paying for groceries? Money helps people get things they need and things they want. But here is something important: people cannot buy everything at once. They have to choose. Those choices are called money choices.

People earn money by doing work. Then they decide how to use that money. A family may use money to buy food, pay for housing, buy clothes, or pay for bus fare. Sometimes people also use money for fun things, like a toy, a book, or a special treat.

Because money is not endless, people make decisions. A financial decision is a choice about money. It can be a small choice, like buying one apple or one banana. It can also be a bigger choice, like saving for a bicycle.

Money choices are the different things people decide to do with the money they earn. People may spend money, save money, or share money to help others.

Different people make different choices. One person may buy a raincoat. Another person may save the same money for later. Both are using money, but they are using it in different ways.

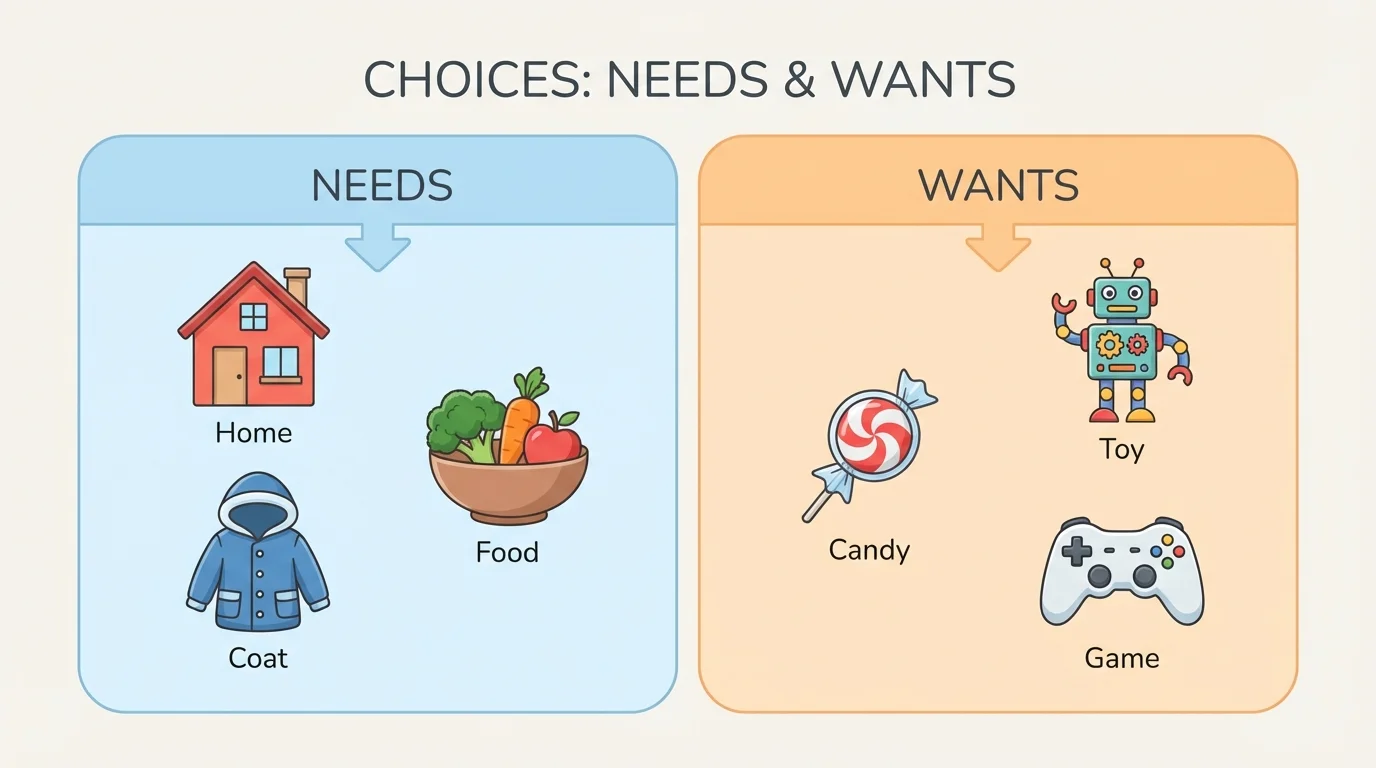

One helpful way to think about money is to sort things into needs and wants, as shown in [Figure 1]. A need is something people must have to live safely and stay healthy. Food, water, a place to live, and clothes for the weather are needs.

A want is something people would like to have, but do not have to have right away. A stuffed animal, a new game, or candy can be wants. Wants can be nice, but needs usually come first.

Sometimes one thing can feel very important, but it is still a want. For example, a shiny new toy may seem exciting, yet dinner comes first. Families often use money for needs before they use money for wants.

People all around the world make money choices every day. Even very small spending choices, like buying water instead of juice, are part of using money carefully.

When we think about needs and wants, we learn how to make better choices. Later, when we look at saving and spending, the same idea from [Figure 1] still helps us decide what should happen first.

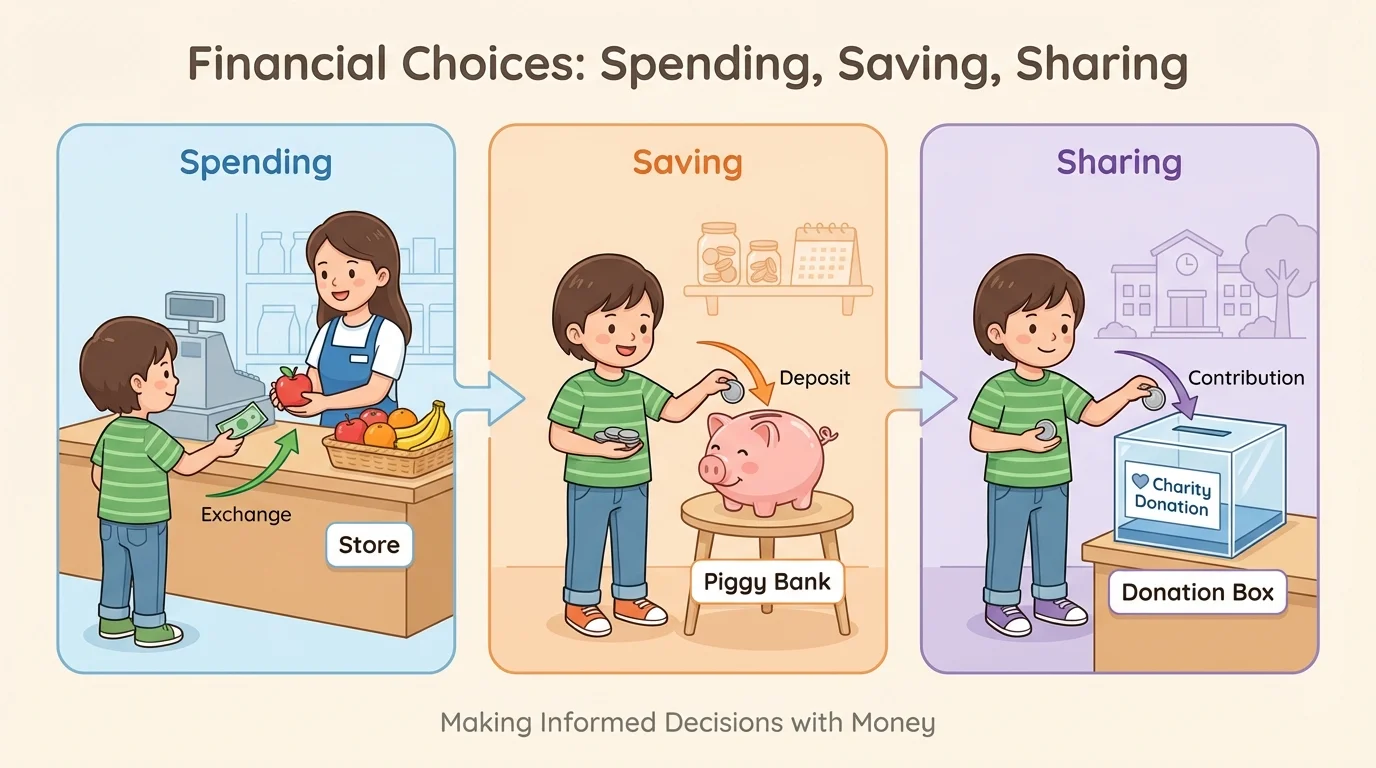

People use money in a few main ways, and [Figure 2] shows three simple ones. They can spend money to buy something now, save money for later, or share money to help someone else.

When people spend money, they use it right away. Buying bread, milk, or a bus ticket is spending. Buying a ball or crayons is also spending.

When people save money, they keep it to use later. A child may save coins in a jar for a puzzle. A family may save money for a big need, like fixing a car.

When people share money, they give some to help others. They may give to a church, a shelter, a food drive, or a person in need. Sharing is another thoughtful money choice.

Sometimes people do all three. They may spend some money on food, save some money for later, and share a little to help someone. There is not just one way to use money.

Good money choices often happen when people stop and think first. A choice means picking between two or more things. Before buying something, a person may ask simple questions, and [Figure 3] lays out this thinking step by step.

They might ask: Do I need this now? Do I want this, but can wait? Do I have enough money? Should I save my money for something else? These questions help people make careful decisions.

People also compare. If one snack costs $1 and another snack costs $2, they may choose the one they like better or the one they can afford. If they only have $1, they know they can choose just one. They cannot choose both because the money is only enough for one item.

Sometimes the answer is, "Not now." That can be a smart choice. Waiting and saving can help people get something important later. The steps in [Figure 3] show that choosing is not only about wanting something. It is also about thinking ahead.

Thinking before spending means looking at what you need, what you want, and how much money you have. This helps people make calm, careful decisions instead of rushing.

Here are some simple examples. A family has enough money to pay for groceries and a movie. They choose groceries first because food is a need. The movie can wait.

A child has $3 in a coin jar. The child sees a sticker for $1 and a small book for $3. If the child buys the sticker now, only $2 will be left. If the child wants the book more, saving all $3 is the better choice.

Example: choosing between now and later

Mia has $2. She wants a cookie for $2, but she also wants to save for a coloring book that costs $5.

Step 1: Think about the two choices.

Mia can spend all $2 now on the cookie, or keep the $2 and save it.

Step 2: Ask what happens next.

If Mia buys the cookie, she has $0 left. If Mia saves, she still has $2 and is closer to $5.

Step 3: Make a decision.

If the coloring book is more important to Mia, saving is a smart money choice.

This is a good example of a financial decision.

Another child may make a different choice, and that is okay. Money choices can be different because people have different needs, wants, and plans.

Careful money choices help people take care of themselves and others. Needs often come first. Wants can wait. Saving helps with future plans. Sharing helps other people.

Adults make many money choices for their families, but children can start learning too. Choosing to save birthday money, deciding between two treats, or giving a coin to help others are all early lessons in using money wisely.

When people understand needs, wants, spending, saving, and sharing, they are better at making good choices. The ideas we saw in [Figure 2] and [Figure 1] work together: first think about what matters most, and then decide how to use money.