If two people invest the same total amount of money, the one who starts earlier often ends up with far more. That sounds unfair, but it is one of the most important truths in personal finance: time can matter as much as how much you invest. When you understand how investing, growth, and risk work together, you can make better choices about college costs, a car, moving out, emergencies, and long-term goals like retirement.

Future planning is really about making decisions now that benefit your future self. That does not mean you need to become a finance expert at age 16. It means learning how money grows, what can go wrong, and how to choose an approach that fits your goals instead of copying trends from social media or taking random advice from influencers.

When you are young, money can feel immediate: food, clothes, subscriptions, gas, saving for a phone, or building up spending money from a part-time job. But some decisions have effects years later. If you save everything in cash, your money is safe from market drops, but it may grow slowly. If you invest everything in something risky because it looks exciting, you might lose money right when you need it. Good future planning means balancing risk, growth, and timing.

A smart plan is not about getting rich fast. It is about making your money do a job. Some money should stay available for short-term needs. Some can be set aside for medium-term goals. Some can be invested for years so it has time to grow. That is where investing becomes useful.

Investing means putting money into something with the expectation that it may grow in value or produce income over time.

Compound growth happens when your money earns growth, and then that growth also starts earning growth.

Return is the gain or loss on your money over time.

Time horizon is how long you expect to leave money untouched before you need it.

Liquidity means how quickly and easily you can turn something into cash without losing value.

One more idea matters in real life: inflation. If prices rise over time, money that sits still can lose purchasing power. If a meal costs $10 today and costs $12 later, the same amount of cash buys less. That is one reason people invest for long-term goals instead of leaving every dollar uninvested.

When people talk about growing money, they usually mean one of two paths: saving or investing. Saving is useful when you need safety and fast access. Investing is useful when you can give money time and accept some ups and downs in exchange for possible growth.

A savings account might earn a small amount of interest and keep your balance steady. Investments such as stock funds, bond funds, or money invested through retirement accounts can rise and fall in value, sometimes sharply. Over long periods, many investments have historically grown more than cash, but they do not do so in a straight line.

This is why future planning is not one-size-fits-all. Money for next month, next year, and ten years from now should not always be treated the same. The best choice depends on when you need the money and how much uncertainty you can handle without panicking.

A relatively small amount invested early can sometimes beat a much larger amount invested later. The reason is not magic. It is simply that earlier money gets more years to compound.

Another key term is diversification. Instead of putting all your money into one company, one app recommendation, or one trend, diversification means spreading money across different investments. This helps reduce the damage if one part performs badly.

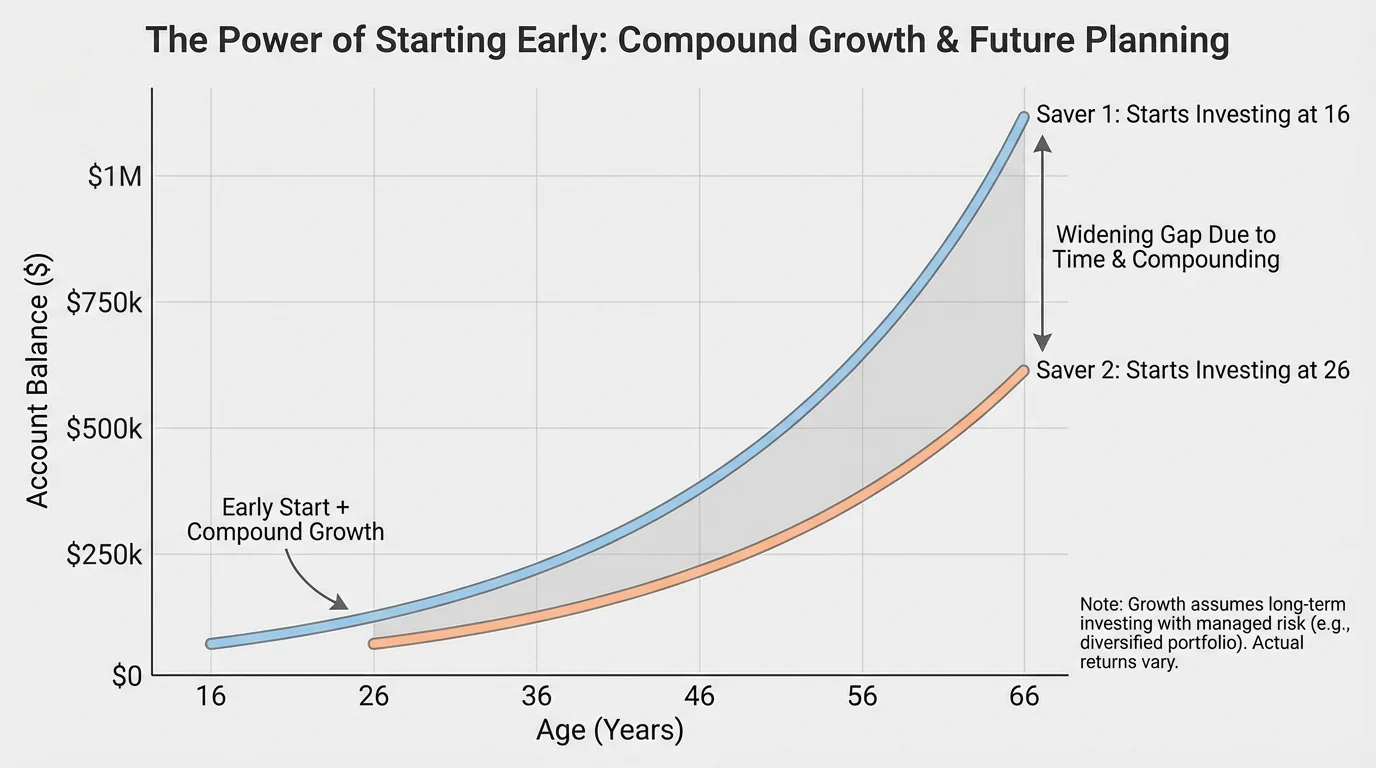

[Figure 1] Compound growth is one of the strongest arguments for starting early, even with small amounts. Over time, growth builds on previous growth, and the change becomes bigger each year. At first the increase may look slow, which is why many people underestimate it.

Suppose you invest $50 each month starting now. That may not feel impressive. But if your money earns a positive average annual return and stays invested for years, each contribution has more time to grow. A dollar invested earlier usually does more work than a dollar invested later.

Here is a simple example. Person A invests $100 per month from age 16 to age 26, then stops. Person B waits until age 26 and then invests $100 per month for many more years. Even if Person B puts in more money overall, Person A may still end up with a similar amount or more, depending on the rate of growth, because Person A gave the money a ten-year head start.

You do not need to calculate every detail by hand to understand the lesson. The practical point is this: waiting has a cost. If you delay for years because you think you need a lot of money to begin, you lose the most valuable ingredient, which is time.

Practical comparison: starting early vs waiting

Assume an investment grows at about 8% per year on average.

Step 1: Start early with a small amount.

If you invest $1,200 per year from age 16 to age 21, that is six years of contributions for a total of $7,200.

Step 2: Let it keep growing.

Even after you stop contributing, the money can continue to grow because earlier gains stay invested and also earn returns.

Step 3: Compare with a later start.

If someone else waits until age 26 and then invests $1,200 per year for many years, they may have to contribute much more money just to catch up.

The exact totals depend on market performance, but the direction is clear: earlier contributions usually have the biggest long-term impact.

That does not mean you should ignore current needs. If you need money in the near future for a laptop, car insurance, or emergency expenses, investing it in something volatile may be a bad idea. Compound growth is powerful, but only if the money can stay invested long enough to ride out downturns.

As the gap widens over time in [Figure 1], notice what future planning really means: deciding which money can wait. The longer your timeline, the more useful compound growth becomes.

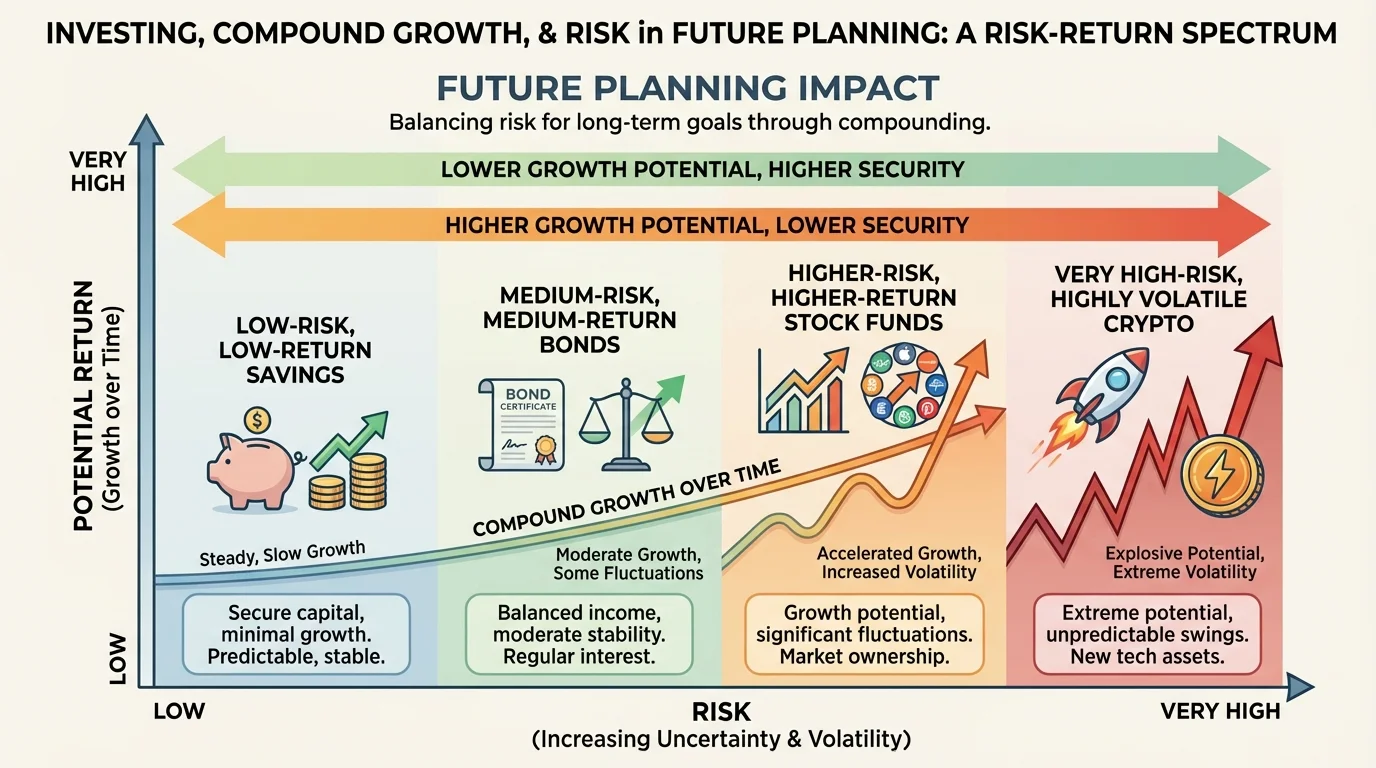

Every money choice sits somewhere on a spectrum, as [Figure 2] illustrates. In general, lower-risk choices tend to offer lower potential returns, while higher-return possibilities usually come with more uncertainty. This relationship is often called the risk-return tradeoff.

For example, a savings account is usually low risk. Your money stays stable, and you can access it fairly easily. But the growth is often limited. A diversified stock index fund has more short-term ups and downs, but over long periods it may offer higher growth. Cryptocurrency can rise quickly, but it can also crash quickly, making it a poor place for money you cannot afford to lose.

Risk is not just about losing everything. It can also mean your money is unavailable when you need it, your returns are lower than inflation, or the investment is so volatile that you sell in fear at the worst time. Practical planning means understanding the kind of risk you are taking, not just asking whether something is "safe" or "unsafe."

Another useful term is volatility. Volatility means how much and how quickly an investment's value moves up and down. High volatility can be stressful because your balance may drop sharply even if the long-term trend may still be positive.

This is why emotional behavior matters. If you put money into a risky investment and then panic when it drops by 15%, you might sell at a loss. Later, if the market recovers, you miss the rebound. A good plan protects you from making emotional decisions under pressure.

Not all risk is bad

Some risk is necessary if you want your money to outgrow inflation over long periods. The goal is not to avoid all risk. The goal is to take the right amount of risk for your timeline, needs, and comfort level. Smart risk is chosen deliberately. Reckless risk is taken without understanding the downsides.

The risk spectrum in [Figure 2] also shows why copying someone else's investment choice can be a mistake. Their goals, timeline, and ability to handle losses may be very different from yours.

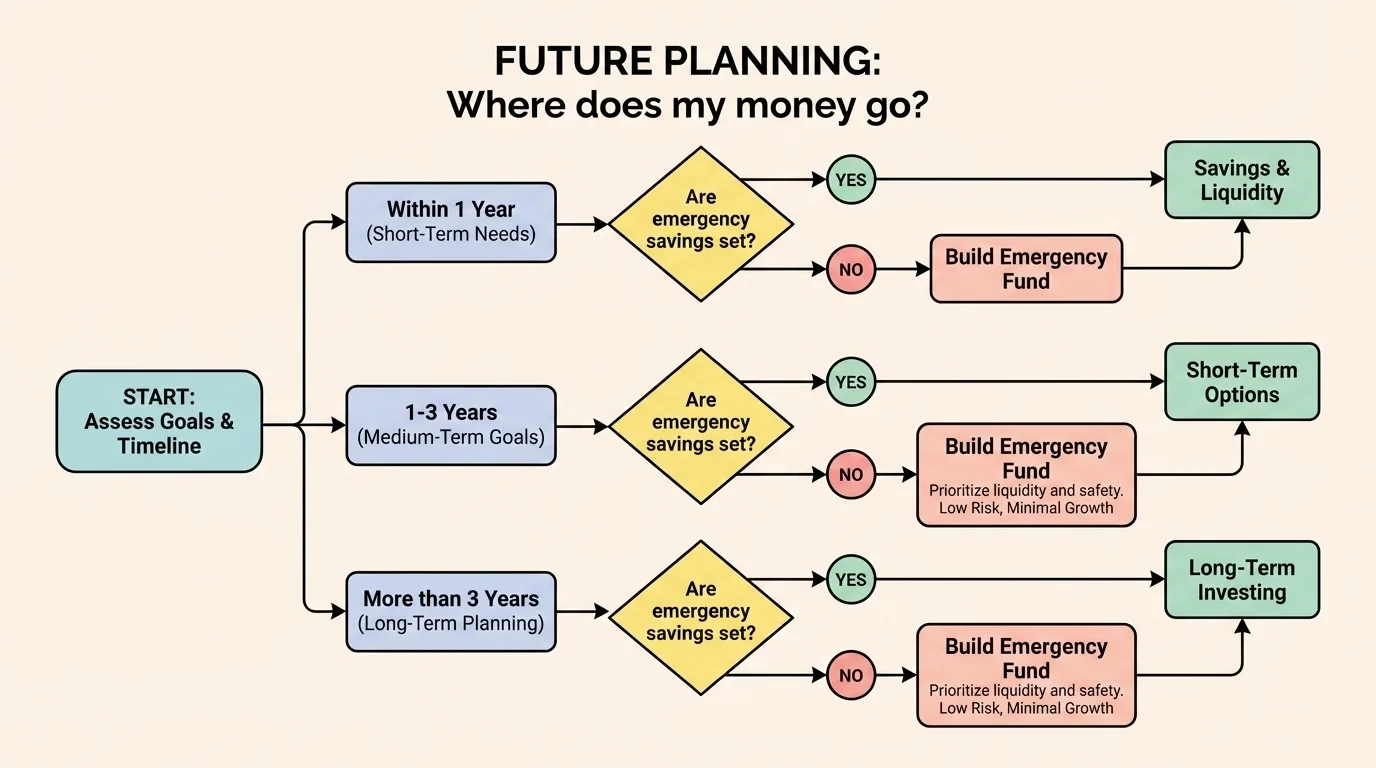

[Figure 3] The best place for your money depends on what that money is for. A practical way to decide is to sort your goals by timeline. This decision path works like a set of checkpoints, helping you separate emergency money, short-term savings, and long-term investing.

If you need the money in less than a year, safety and liquidity usually matter most. That money often belongs in cash or a savings account. If you need it in one to five years, you may still want lower-risk options, depending on how flexible the goal is. If you do not need the money for many years, investing may make more sense because you have time to recover from short-term drops.

Think about a few real-life examples. Money for a concert next month should not be in a volatile investment. Money for a car in two years might need a cautious approach. Money for retirement, which is decades away, can usually handle more short-term market movement because the time horizon is so long.

This is also where an emergency fund matters. Before taking major investing risk, it is wise to have some money set aside for unexpected expenses. Without emergency savings, you might be forced to sell investments at a bad time to cover a sudden need.

| Goal | Time horizon | Priority | Likely fit |

|---|---|---|---|

| Phone repair or urgent bill | Immediate | Fast access | Cash or savings |

| Vacation next summer | Less than 1 year | Protect principal | Savings |

| Used car purchase | 1 to 3 years | Stability with some growth | Usually lower-risk options |

| Retirement | Decades | Long-term growth | Diversified investing |

Table 1. A comparison of financial goals, timelines, and money choices that often fit each situation.

When you use the decision process in [Figure 3], you stop asking, "What is the best investment?" and start asking, "What is the best choice for this goal?" That is a much smarter question.

Many bad money decisions happen because something sounds exciting, urgent, or easy. A video might promise fast returns. A friend may talk about a "guaranteed" opportunity. A post may show only winners and never losses. Before you put money anywhere, slow down and evaluate it carefully.

Step 1: Ask what the investment actually is. If you cannot clearly explain how it works, you should not buy it. "Everyone is doing it" is not a real reason.

Step 2: Ask how the investment makes money. Does it grow because a business earns profits? Does it pay interest? Does it depend entirely on someone else paying more later? If the answer is unclear, be careful.

Step 3: Check fees. Fees may look small, but over time they can eat into growth. If an account charges 1% to 2% every year, that can take a noticeable bite out of long-term returns.

Step 4: Ask about access. Can you get your money out when needed? Is there a penalty for withdrawal? Is the value likely to drop right when you need the cash?

Step 5: Compare the claim with reality. High return with low risk sounds great, but in many cases it is a warning sign. If someone promises easy, guaranteed gains, be skeptical.

Quick decision check

You have $600 from work and gifts. You want some of it for a summer trip and some for the future.

Step 1: Separate by purpose.

Keep the trip money in savings if you will need it soon.

Step 2: Protect against surprises.

Set aside part of the remainder as emergency money.

Step 3: Invest only the money with a longer timeline.

If you will not need the rest for several years, that portion may be appropriate for a diversified investment option.

This is better than putting the full $600 into one risky trend and hoping nothing goes wrong before summer.

One more warning: beware of scams built on urgency. Pressure to "act now," secret strategies, and guaranteed returns are major red flags. Real investing is usually slower and more boring than hype videos make it look. Boring can be good when it is stable and intentional.

One common mistake is waiting for the "perfect" time to start. Many people think they need a lot of money, a perfect market moment, or expert-level knowledge. In reality, starting small and learning gradually is often better than doing nothing.

Another mistake is putting short-term money into long-term investments. If your rent, insurance, or planned purchase depends on that money soon, market swings become dangerous. This is not because investing is bad; it is because the timeline is wrong.

A third mistake is chasing trends. If an investment is popular online, that does not mean it is wise for you. Hype usually focuses on the upside, not the full risk. The farther right you move on the risk scale we saw in [Figure 2], the more important self-control becomes.

"Do not save what is left after spending, but spend what is left after saving."

— Often attributed to Warren Buffett

Smart habits are usually simple. Save consistently. Invest regularly if the goal is long-term. Keep an emergency cushion. Diversify instead of betting everything on one idea. Ignore pressure to get rich fast. Review whether your choices still match your goals.

Consistency matters more than intensity. Investing $25 or $50 regularly can build discipline and experience. The habit of making deliberate money choices now can shape much bigger decisions later when the numbers are larger.

You do not need a complicated system to begin. If you have job income, allowance, side-gig money, or gift money, you can create a simple structure.

First, list your goals by timeline: immediate, within a year, within five years, and long-term. Second, give each dollar a role. Third, keep short-term money safe and liquid. Fourth, consider investing only money that has time to grow. Fifth, review your plan when your life changes.

For example, if you earn $200 in a month, you might put $100 toward short-term needs, $50 into emergency savings, and $50 toward long-term investing. The exact split depends on your life, but the idea is intentional planning instead of random spending.

Money decisions are rarely just about math. They are also about behavior. A plan only works if you can stick to it when markets drop, friends brag about fast gains, or you feel tempted to spend everything immediately.

As your goals change, your strategy should change too. A college payment due soon should be treated differently from retirement savings. The same person may need low-risk choices for one goal and higher-growth investments for another. Future planning is flexible, but it should never be careless.

If you remember only one principle, let it be this: choose based on purpose. Time affects growth. Risk affects outcomes. Your plan should connect the two.