Have you ever had money in your pocket one day and then wondered, just a few days later, where it all went? That happens to a lot of people, including adults. Money can disappear quickly when you spend without a plan. A budget is not about never having fun. It is about telling your money where to go so you can enjoy some now, save some for later, and still reach the things that matter most to you.

When you get allowance, gift money, or cash for helping with jobs at home or in your community, you make choices. Maybe you want a snack, a game add-on, sports gear, art supplies, or money saved for something bigger. The skill that helps with all of those choices is budgeting. Good budgeting helps you stay in control. Poor budgeting can leave you frustrated, short on cash, or unable to buy something important later.

Income is money that comes in. For a sixth grader, that might be allowance, birthday money, holiday money, or money earned from age-appropriate tasks like helping a neighbor rake leaves. Expenses are the costs you pay when you buy something. Saving means setting aside some money now so you can use it later.

Budget means a plan for your money. It shows how much money you have, how much you expect to spend, and how much you want to save.

Need means something important or necessary. Want means something you would like but do not have to have right away.

A budget can be very simple. You do not need fancy apps or difficult math. You only need three basic questions: How much money do I have? What do I need or want to pay for? How much should I save for later? If you can answer those questions honestly, you can build a useful money plan.

One important truth is that budgeting involves choices. If you have $10 and spend all of it on one thing, then you have $0 left for anything else. If you spend $4 and save $6, you still have money working for your future. Budgeting is really the skill of choosing on purpose instead of choosing by accident.

Before you make a plan, you need to know what money you usually receive. Some students get the same allowance every week. Others get money only once in a while. Some may earn small amounts by helping family members or neighbors. When your income changes from week to week, budgeting becomes even more important.

Start by writing down the money you receive in a normal month. For example, if you get $8 each week, then in four weeks you receive:

\[8 \times 4 = 32\]

That means you can plan around $32 for the month. If your money is irregular, estimate carefully. If one week you get $5 and another week you get $10, do not build your budget as if you always get the highest amount. It is safer to plan based on the amount you are most likely to receive.

Many money problems start not because people never had money, but because they guessed wrong about how much was coming in and spent too fast.

It also helps to separate money by purpose. If your aunt gives you $20 specifically for a book or a hobby item, treat that money differently from your regular allowance. When money has a purpose, your budget should respect that purpose.

A very useful beginner strategy is to split your money into three parts: spend, save, and share or give. The categories work together as shown in [Figure 1], and they help you avoid putting every dollar into one place. You might not use exactly the same amounts every time, but the system keeps your money balanced.

Here is one simple example. Suppose you receive $20. You might choose to spend half, save a little less than half, and share a small part. One possible plan is:

\[20 = 10 + 8 + 2\]

That means $10 for spending now, $8 for saving, and $2 for sharing, donating, or using to help someone else. Another student might choose a different split, such as:

\[20 = 8 + 10 + 2\]

If they have a big goal, they may save more and spend less. The best budget is the one that fits your real life and helps you reach your goals.

You can use actual jars, envelopes, a notebook, or a simple notes app. The tool matters less than the habit. What matters is that every time money comes in, you decide where it goes before you spend it.

Try This: The next time you receive money, pause for two minutes before spending any of it. Put each part into a labeled category right away. That one small pause can stop a lot of impulse spending.

Why categories help

Money feels easier to manage when it has a job. If all your cash is mixed together, it is easy to spend your savings by mistake. Categories protect your priorities. Your spending money is for now, and your savings money is for later.

As your amounts change, you can still use the same idea we saw in [Figure 1]. If you get $12 one week instead of $20, you still divide it into categories. A budget is flexible. The plan changes when the amount changes, but the habit stays the same.

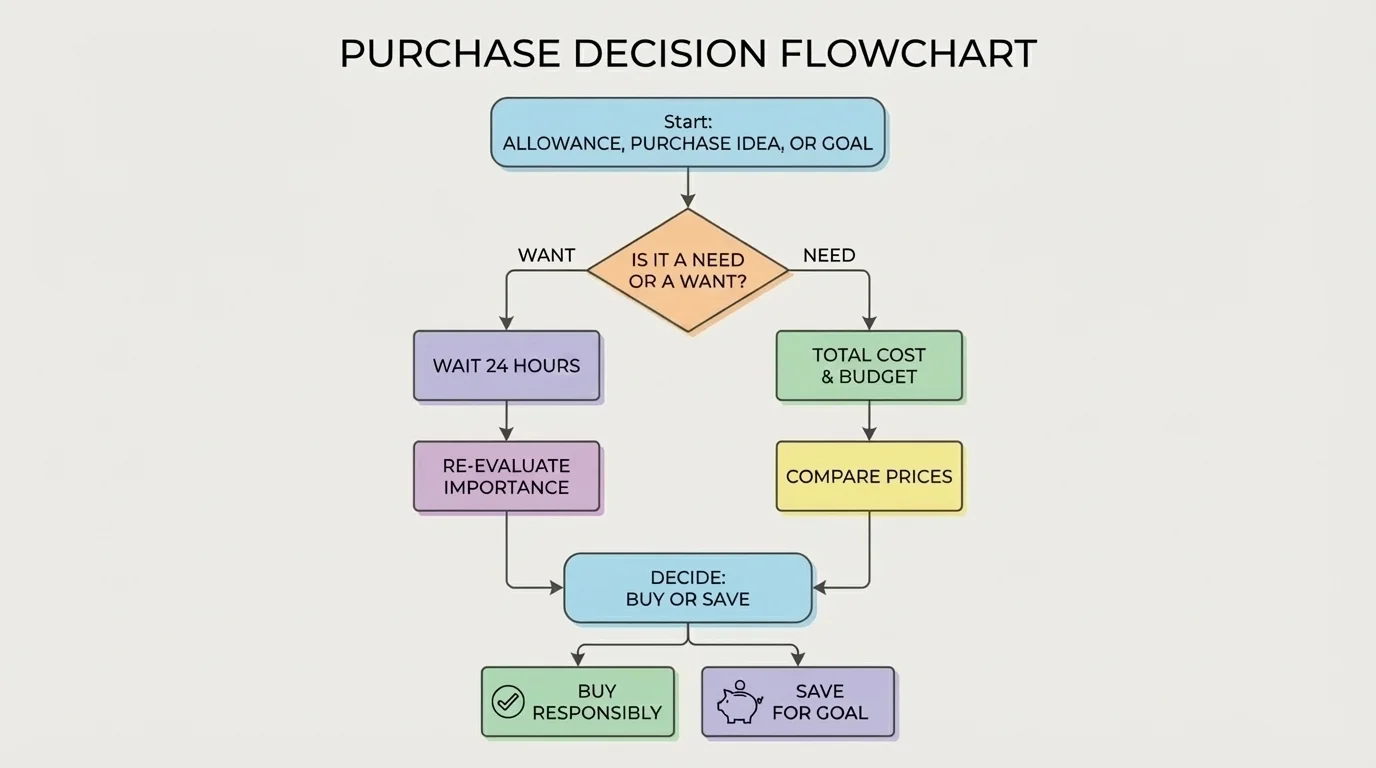

[Figure 2] Buying something may seem simple, but smart buyers use a process. This matters a lot when shopping online, where it is easy to click quickly and forget about taxes, shipping, or extra fees.

The decision steps show how to slow down, check the real cost, and decide whether to buy now or wait. Before you buy, ask yourself these questions: Is this a need or a want? How much does it cost in total? Do I already have enough money in my spending category? Will buying this slow down an important goal? Can I compare prices first?

One of the biggest budgeting mistakes is looking only at the price tag and not the total cost. For example, a craft kit might cost $14 online, but there may also be $3 shipping and $1 tax. The total is:

\[14 + 3 + 1 = 18\]

If you only planned for $14, you are short by $4. That is why careful buyers always check the total before deciding.

Another strong strategy is to use a waiting rule to prevent impulse buying: if it is a want and not urgent, wait a day before purchasing. A lot of wants feel very important in the moment and much less important later. Waiting protects your budget.

Comparing prices is also a smart move. The same item can cost different amounts in different stores or online shops. If one water bottle costs $12 and another similar one costs $9, the difference is $3. Saving $3 might not sound huge, but if you do that often, those small savings build up.

| Question | Why it matters |

|---|---|

| Need or want? | Helps you decide if the purchase should happen now or later. |

| Total cost? | Prevents surprise charges like tax or shipping. |

| Enough budgeted money? | Keeps you from using savings by accident. |

| Can you compare prices? | Helps you get better value for your money. |

| Can you wait? | Reduces impulse buying and regret. |

Table 1. Questions to ask before making a purchase and how each question protects your budget.

Being a smart consumer does not mean never buying fun things. It means buying them in a way that matches your plan. If your budget says you can afford it and it does not damage an important goal, then you can enjoy the purchase with much less stress.

[Figure 3] Saving gets easier when your money has a target. A financial goal is something you want to use your money for in the future. A visual tracker keeps the goal clear, and it helps you notice progress instead of feeling like saving takes forever.

A visual tracker shows one way to track progress toward a goal. Goals can be short-term, like saving for a $15 book or a $25 game accessory, or long-term, like saving $60 for headphones or $100 for a special project. Bigger goals usually require patience and planning.

To build a savings plan, follow these steps. First, name the exact goal. Second, write the exact cost. Third, decide how much you can save each week. Fourth, figure out how long it will take.

For example, if your goal is $60 and you save $10 each week, then the number of weeks is:

\[60 \div 10 = 6\]

That means you can reach the goal in 6 weeks. Breaking a big amount into small steps makes it feel possible.

Sometimes you will need to choose between a small purchase now and a bigger goal later. This is called a trade-off. If you spend $12 from your savings for snacks and small items, and your goal was $60, then you now still need:

\[60 - 12 = 48\]

That may delay your goal. Trade-offs are normal, but you should notice them clearly. When you understand the trade-off, you are in control.

"A budget is telling your money where to go instead of wondering where it went."

— Common personal finance saying

The tracker in [Figure 3] also reminds you that progress counts even when the amount seems small. Saving $2, then $4, then $6 does not look huge at first, but steady saving builds momentum. Many goals are reached through small repeated actions, not one giant payment.

Now let's look at realistic situations you might actually face.

Example 1: Weekly allowance budget

You get $15 this week and want to divide it into spending, saving, and sharing.

Step 1: Pick your categories.

Suppose you choose $7 to spend, $6 to save, and $2 to share.

Step 2: Check that the parts match the total.

\[7 + 6 + 2 = 15\]

Step 3: Put the money into those categories right away.

This keeps you from accidentally spending your savings.

This budget works because every dollar has a purpose.

This kind of plan is especially useful if you usually spend quickly. Once your saving money is separated, it becomes harder to use it without thinking.

Example 2: Can you afford a purchase?

You want a game skin that costs $9, and tax adds $1. You have $8 in your spending category.

Step 1: Find the total cost.

\(9 + 1 = 10\)

Step 2: Compare the total cost to your spending money.

\(10 - 8 = 2\)

Step 3: Decide wisely.

You are short by $2, so buying now would break your budget unless you wait and save more or choose not to buy.

The smart decision is to wait instead of taking money from savings without a plan.

Notice how this example connects to the decision process from [Figure 2]. You check the total cost first, then compare it to your budgeted amount, then decide whether to buy, wait, or skip it.

Example 3: Reaching a bigger goal

You want headphones that cost $48. You can save $6 each week.

Step 1: Write the goal and weekly saving amount.

Goal: $48. Weekly saving: $6.

Step 2: Divide the total goal by the weekly amount.

\[48 \div 6 = 8\]

Step 3: Interpret the answer.

It will take 8 weeks to reach the goal if you stay on track.

This shows how a big cost becomes manageable when you break it into smaller pieces.

If that feels too long, you have choices. You might save more each week, look for a less expensive version, or decide the goal is not worth it right now. Budgeting is not just about numbers. It is about matching your choices to what matters most.

A budget works best when you keep track of it. You do not need anything complicated. A small notebook, spreadsheet, or notes app is enough. Write down money that comes in and money that goes out. This is called a transaction record.

For example, if you start the week with $12 in spending money and buy a snack for $3 and stickers for $2, then the amount left is:

\[12 - 3 - 2 = 7\]

If you forget to track those purchases, you may think you still have more money than you really do. That can lead to overspending and disappointment at checkout.

Subtracting what you spend from what you started with tells you how much money is left. This simple skill is one of the most important parts of everyday money management.

Another strong habit is checking your balance before you shop, especially online. If your plan says you have $5 available, then that is your limit unless you intentionally change your budget. Guessing leads to mistakes. Checking leads to control.

It is also okay to talk with a parent, guardian, or trusted adult about your money plan. They may help you think through goals, compare prices, or avoid scams. Asking for advice is not weakness. It is smart money behavior.

Sometimes your budget will not go perfectly. Maybe you expected $10 this week and received only $5. Maybe the price of the item you wanted increased. Maybe you forgot about shipping. That does not mean you failed. It means your plan needs an update.

Here is how to adjust: first, look at your new total money. Second, protect the most important category, especially if you have a strong goal. Third, reduce or delay less important spending. Fourth, rewrite your plan clearly.

Suppose you planned to save $8 this week, but you only received $6 total. You might decide to save $4 and spend $2 instead. The point is not to keep the old plan no matter what. The point is to make a new plan that fits the real situation.

Flexible budgeting

A good budget is strong, but not stiff. It gives your money direction while still allowing you to respond when life changes. Flexible budgeting helps you avoid giving up just because one week did not go as expected.

This is another reason budgeting is powerful. Without a plan, changes feel confusing. With a plan, changes become a problem you can solve.

You do not need to wait until you are older to become skilled with money. The habits you build now can help you for years. If you learn to separate spending and saving now, future money choices become easier.

Try This: Write one short-term goal and one long-term goal today. Add the cost of each goal and decide how much you can save each week.

Try This: For one week, track every purchase you make, even very small ones. At the end of the week, look for patterns. Are you spending mostly on wants? Are small purchases adding up?

Try This: Before your next purchase, use a 24-hour waiting rule if the item is not urgent. You may still decide to buy it, but the waiting time gives your brain space to think instead of react.

Money management is not about being perfect. It is about being aware, honest, and intentional. Every time you plan before spending, compare the total cost, or save toward a goal, you are building real-life financial strength.