A student loan can shape your future long after graduation. Two people can borrow the same amount for college and end up with very different financial lives: one builds savings, buys a car, and keeps a strong credit score, while the other struggles with late payments and watches the balance grow. The difference is often not just how much they borrowed, but how well they understood repayment before signing the paperwork.

Paying for education is closely connected to career preparation and lifetime earning potential. A certificate, trade program, community college degree, or four-year degree can increase income opportunities, but borrowing for that education means part of future income is already committed. If your first job pays $38,000 a year and your student loan payment is $400 each month, that loan affects your budget, housing choices, transportation, and ability to save. If your first job pays $62,000 a year, the same payment may feel much more manageable.

That is why student loans should never be viewed as "free college now, worry later." A loan is a legal agreement. The money can open doors, but repayment becomes part of your financial future. Thinking ahead helps you compare schools, majors, training programs, and expected starting salaries more carefully.

Education as an investment

Education often increases earning potential, but like any investment, its value depends on cost, results, and timing. Borrowing can make sense when the education leads to stronger career opportunities, but excessive borrowing can reduce the financial benefits of that education for years. A smart decision compares likely income after training with the size of the debt required to get there.

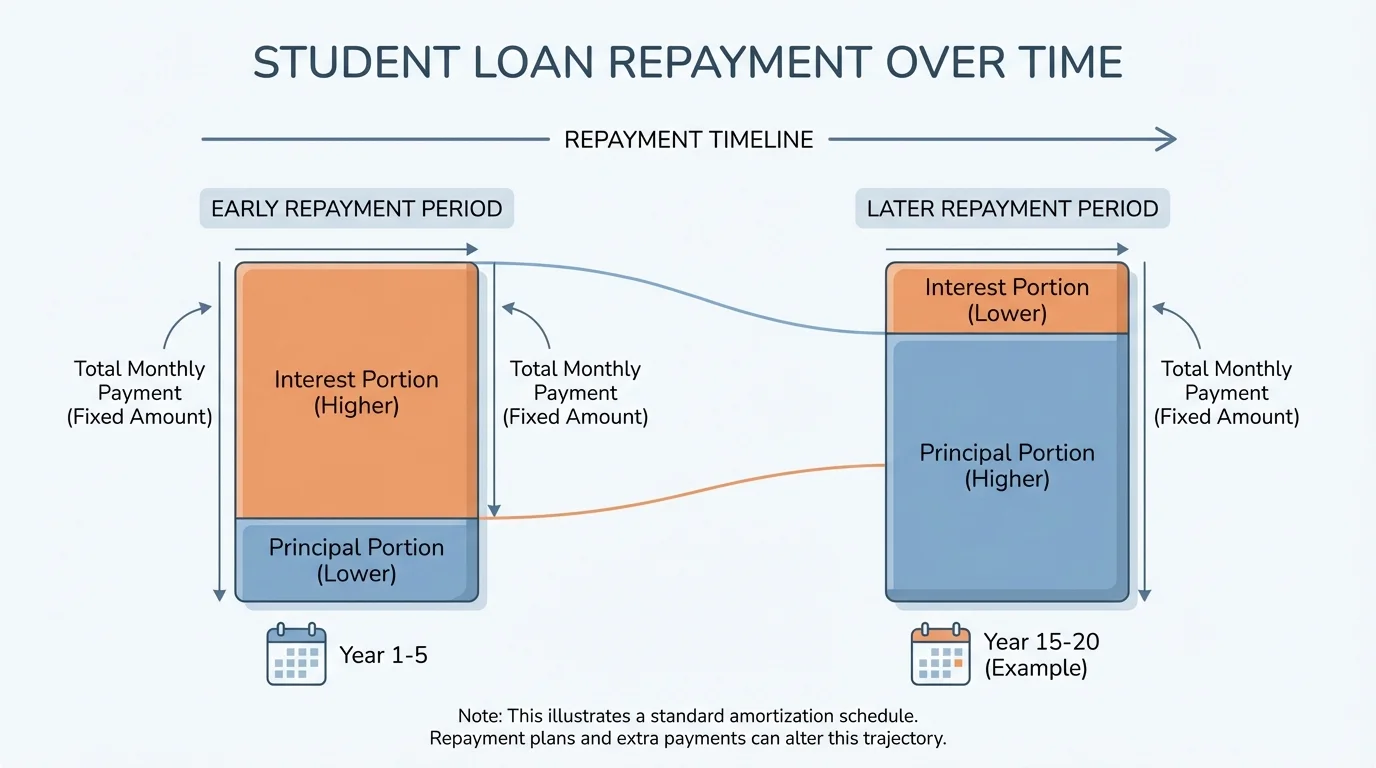

[Figure 1] Students sometimes focus only on the amount borrowed and ignore the repayment structure. Yet the structure matters. A loan with a smaller monthly payment may look safer at first, but if it lasts much longer, the borrower may pay thousands more in interest over time.

When you borrow, the original amount is called the principal. The lender also charges interest, which is the cost of borrowing money. The company that sends bills and manages your account is often a loan servicer. Many student loans also include a grace period, a short time after leaving school before payments are required.

Another important idea is amortization. Amortization means the loan is repaid through regular payments over time. Early payments usually cover more interest and less principal. Later payments usually cover less interest and more principal. This pattern helps explain why making only minimum payments for a long period can become expensive.

Suppose a student borrows $20,000 at an annual interest rate of 5% on a 10-year repayment plan. A simplified monthly interest rate is \(\dfrac{0.05}{12} \approx 0.00417\) per month. Even without calculating the exact payment formula, you can see that interest is added again and again over many months. The longer repayment lasts, the more total interest the borrower pays.

Some federal loans are subsidized, which means the government pays certain interest charges during specific periods, such as while an eligible student is in school. Other loans are unsubsidized, meaning interest begins building more immediately. This difference can change the balance a borrower faces after graduation.

Principal is the amount originally borrowed. Interest is the cost charged for borrowing. A grace period is a temporary time after leaving school before payments begin. Amortization is the process of repaying a loan through scheduled payments over time.

Understanding how payments are divided helps you see why extra payments toward principal can reduce total interest. Even a small extra amount paid consistently can shorten repayment.

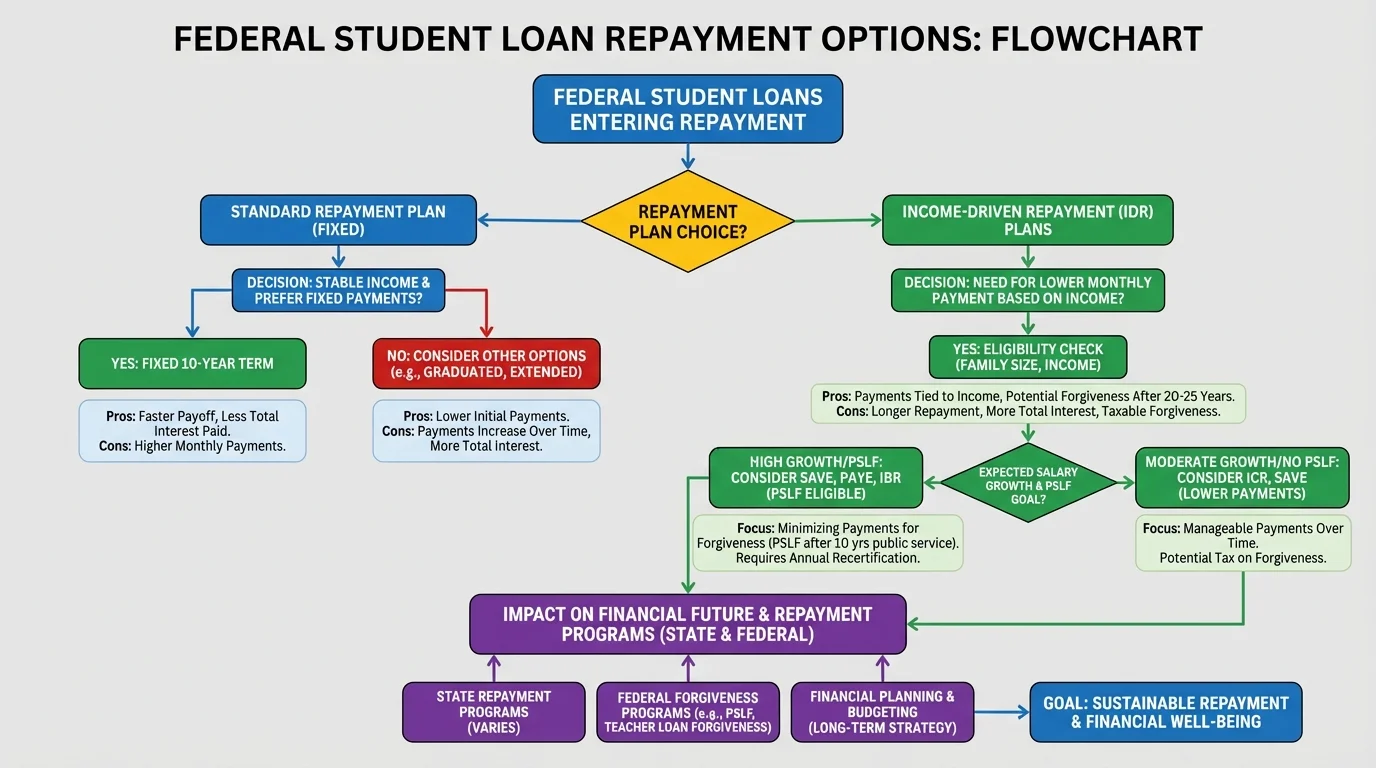

[Figure 2] Federal student loans generally offer more repayment flexibility than private loans, and choosing among plans works almost like a decision tree. The best plan depends on your income, how stable your job is, whether you expect raises, and whether you may qualify for forgiveness programs.

The standard repayment plan usually spreads payments over about 10 years. Because repayment is faster than in some other plans, monthly payments are often higher, but the total amount paid is usually lower. This plan is often the least expensive overall if the borrower can afford the monthly amount.

The graduated repayment plan starts with lower payments that increase over time. This can help a new graduate who expects earnings to rise as their career progresses. However, because the loan may stay outstanding longer or principal is reduced more slowly early on, total interest can be higher.

The extended repayment plan stretches payments over a longer period, such as up to 25 years for eligible borrowers. This lowers the monthly payment but often increases the total amount repaid.

Income-driven repayment plans connect the monthly payment to the borrower's income and family size. These plans can make payments more affordable, especially for borrowers with low early-career earnings. In some cases, the monthly payment may be very low. But a lower monthly payment does not automatically mean a cheaper loan, because repayment may last much longer and interest may continue to accumulate.

Federal repayment plans often allow borrowers to change plans if life changes. A borrower who loses a job, returns to school, or enters public service may need a different payment structure later. This flexibility is one reason federal loans are usually considered less risky than private loans.

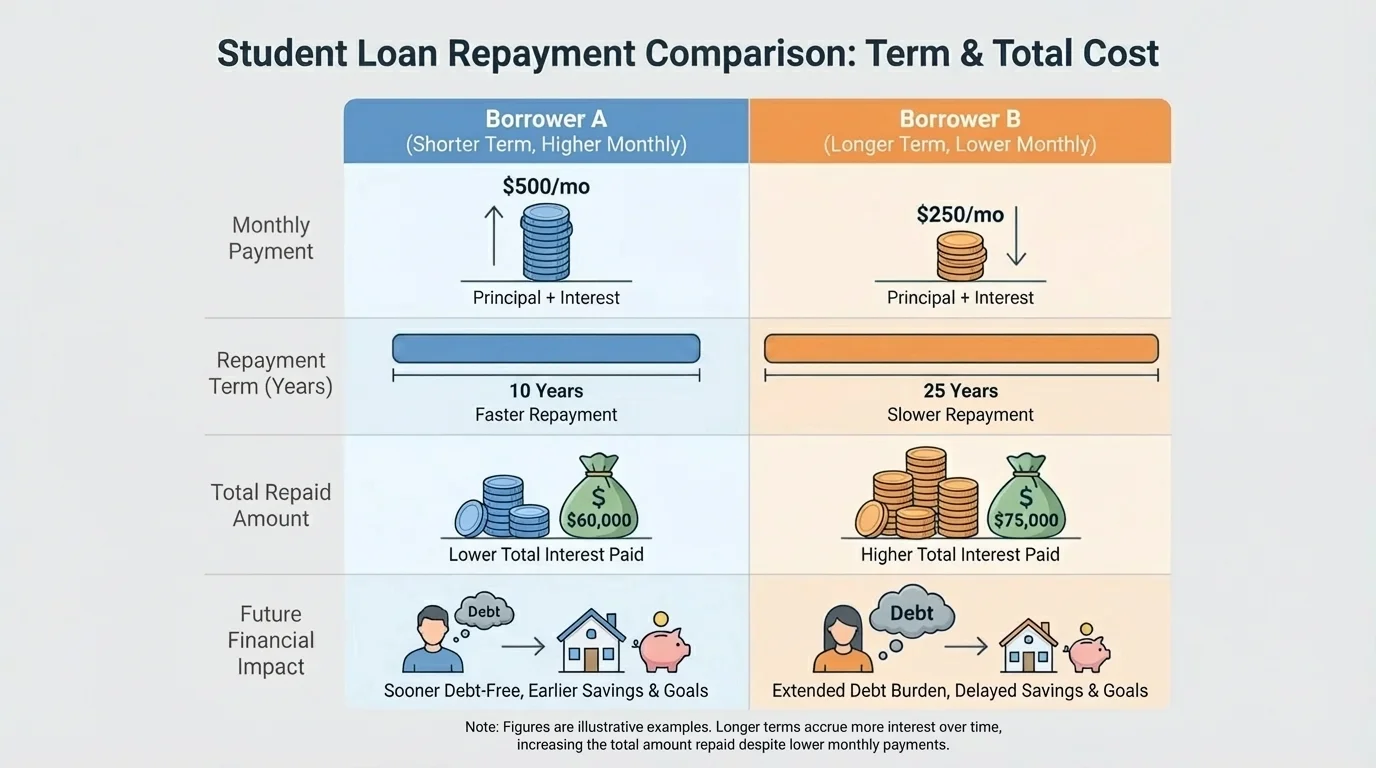

Comparing two repayment choices

A borrower owes $24,000. Under one plan, the monthly payment is $255 for 10 years. Under another, the monthly payment is $170 for 20 years.

Step 1: Find the total paid under the 10-year plan.

There are \(10 \times 12 = 120\) months, so the total paid is \(255 \times 120 = 30,600\).

The borrower repays $30,600 in all.

Step 2: Find the total paid under the 20-year plan.

There are \(20 \times 12 = 240\) months, so the total paid is \(170 \times 240 = 40,800\).

The borrower repays $40,800 in all.

Step 3: Compare the extra cost.

\[40,800 - 30,600 = 10,200\]

The lower monthly payment costs $10,200 more over time.

This example shows a common trade-off: lower monthly payments can protect your short-term budget, but they often increase long-term cost.

Later, when comparing career paths, a borrower may choose a lower payment plan at first to stay financially stable and then switch plans or make extra payments after income rises.

Private student loans come from banks, credit unions, or other lenders. Their rules are set by the lender, not by federal student aid policy. Interest rates may be fixed or variable, and repayment protections are often more limited.

A variable interest rate can change over time. That means a payment that fits your budget today may rise later. Private lenders may also require a cosigner, especially for young borrowers with little credit history. Missing payments can hurt both the borrower's credit and the cosigner's credit.

Private loans may offer fewer options for income-driven repayment, deferment, or forgiveness. Because of that, many financial experts suggest using federal loans first if borrowing is necessary. Private loans can still be useful in some situations, but they require especially careful reading of the terms.

Many borrowers focus on the interest rate alone, but loan flexibility matters too. A slightly lower private rate may still be riskier than a federal loan if the private lender offers fewer hardship protections.

Some borrowers later choose refinancing, which means replacing an old loan with a new one, usually to get a different interest rate or repayment term. Refinancing federal loans into private loans can remove federal protections, so that choice should be made very carefully.

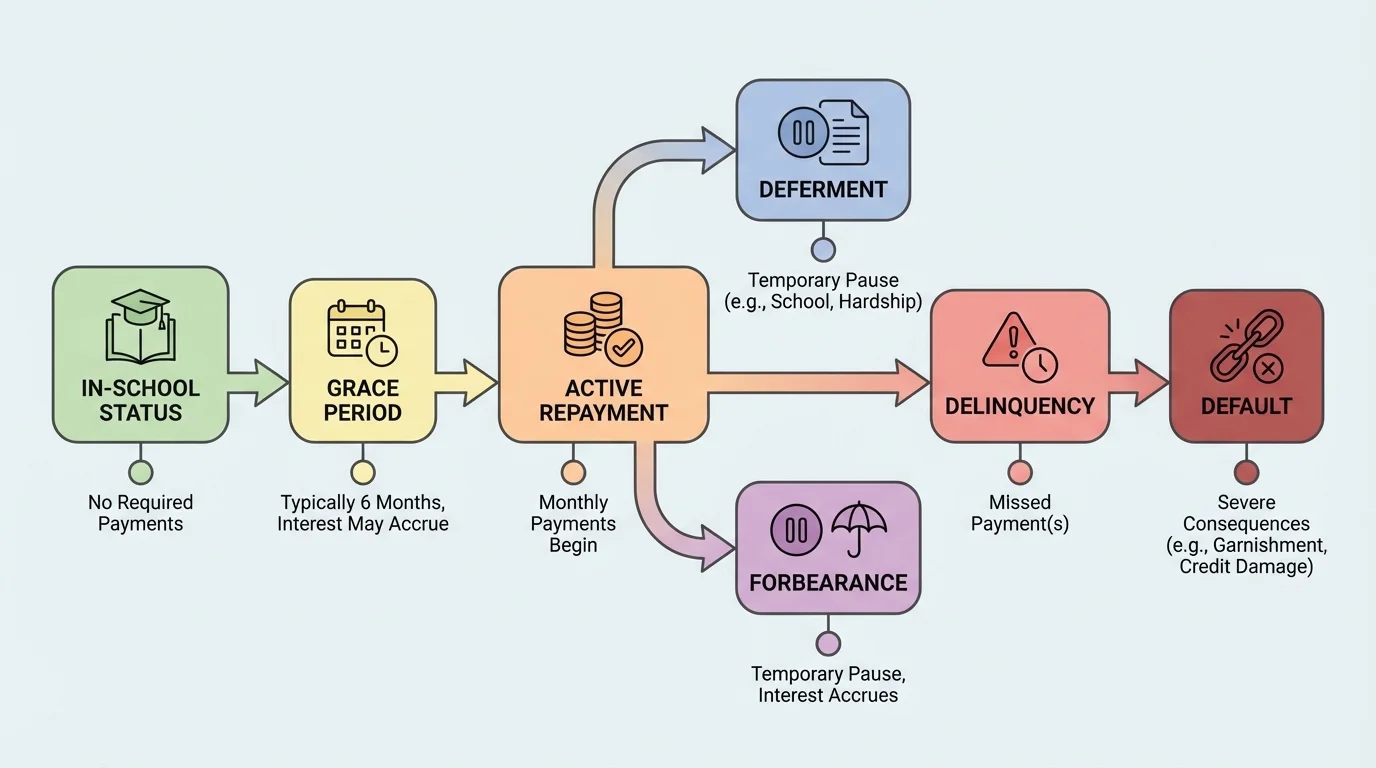

[Figure 3] Student loan repayment is not just one event after graduation. It moves through stages over time, and each stage has its own rules, deadlines, and consequences.

Many federal loans require that a student be enrolled at least half-time to receive certain in-school benefits. After leaving school or dropping below half-time enrollment, the grace period begins for eligible loans. When the grace period ends, required payments start unless another approved status applies.

If a borrower cannot make payments for a valid reason, they may request deferment or forbearance. Deferment is a temporary pause, and for some loans, certain interest charges may be limited during that time. Forbearance is also a temporary pause or reduction, but interest often continues to build.

Interest that is added to the loan balance is called capitalization. For example, if $1,200 of unpaid interest is capitalized on an $18,000 loan, the new balance becomes \(18,000 + 1,200 = 19,200\). Now future interest may be charged on $19,200 instead of $18,000, making the loan more expensive.

When payments are late, the account can become delinquent. If the borrower remains far behind for too long, the loan may enter default. Default can seriously damage credit, lead to collection fees, and make future borrowing harder. In some cases, wages or tax refunds may be taken to repay the debt.

Strong communication with the loan servicer matters. Borrowers who contact the servicer early often have more options than borrowers who ignore bills until the problem grows. There are several stages at which action can prevent a much worse outcome.

Credit reflects how reliably a person handles borrowed money. Late payments, default, and collections can lower a credit score, making apartments, car loans, insurance rates, and even some jobs harder to secure.

Requirements also include paperwork. Borrowers in income-driven plans may need to recertify income regularly. Missing deadlines can cause the monthly payment to jump unexpectedly.

Some repayment programs are designed to reduce debt for borrowers in certain careers or public service roles. These programs can influence career choices, especially for students considering teaching, nursing, medicine, law, social work, military service, or government work.

One major federal program is Public Service Loan Forgiveness. Under this program, eligible borrowers working full-time for qualifying government or nonprofit employers may have remaining federal loan balances forgiven after making a required number of qualifying payments under an eligible repayment plan. The rules are detailed, so borrowers must track employment and payment records carefully.

Teachers may qualify for federal teacher-related forgiveness programs if they work in eligible schools or subject areas. Some states also offer loan repayment assistance for teachers in shortage areas, such as math, science, or special education. States may provide assistance to health professionals who agree to work in rural or underserved communities.

Many states create targeted programs because they want trained workers in high-need fields. For example, a state may help repay part of a nurse's or doctor's loans if that person agrees to serve in a community with limited access to healthcare. This creates a link between education, workforce needs, and public policy.

How forgiveness changes financial planning

Forgiveness programs can lower the long-term cost of education, but they also come with rules. Borrowers may need specific job types, payment plans, or years of service. Depending on the program, changing employers too early or using the wrong repayment plan can reduce or eliminate eligibility. A borrower should never assume forgiveness will happen automatically.

Income-driven repayment plans may also include eventual forgiveness after a long repayment period if a balance remains. However, borrowers should understand that lower monthly payments can still mean more total interest before forgiveness occurs, and program rules can change over time.

The most important question is not only "Can I make the payment next month?" It is also "What will this debt do to my choices over the next 5, 10, or 20 years?" The trade-off between affordability now and total cost later appears clearly here.

A common way to think about loan burden is to compare monthly debt with monthly income. If a graduate brings home about $2,600 each month and owes $450 in student loans, then the loan uses a significant share of take-home pay. The fraction is \(\dfrac{450}{2,600} \approx 0.173\), which is about \(17.3\%\) of monthly take-home pay. That limits room for rent, food, transportation, emergencies, and savings.

Monthly payment as part of a budget

A graduate earns $3,200 per month after taxes and has a student loan payment of $320.

Step 1: Write the fraction of income used for the payment.

\[\frac{320}{3,200}\]

Step 2: Convert to a decimal.

\[\frac{320}{3,200} = 0.10\]

Step 3: Convert to a percent.

\(0.10 = 10\%\)

The payment uses 10% of monthly take-home pay.

This may be manageable for some budgets, but if rent or transportation costs are high, even 10% can feel tight.

[Figure 4] Student loans also create opportunity cost. Money used for loan payments cannot be used for something else, such as emergency savings, investing, moving for a better job, or starting a business. If a borrower pays $300 each month for 10 years, that is \(300 \times 12 \times 10 = 36,000\) that cannot be directed elsewhere during that period.

The "cheaper-feeling" payment is not always the cheaper loan. Lower monthly bills can support short-term survival, but they may delay saving for goals like a car, a home, or retirement.

Effect of extra payments

A borrower has a required payment of $210 each month but chooses to pay $260 instead.

Step 1: Find the extra amount paid each month.

\[260 - 210 = 50\]

Step 2: Find the extra amount paid in one year.

\[50 \times 12 = 600\]

Step 3: Interpret the result.

An extra $600 per year goes toward reducing the balance faster. This can lower future interest and shorten the repayment period, especially because principal falls more quickly.

Even modest extra payments can make a noticeable difference over time.

Career choice matters here too. A student entering a high-paying field may be able to repay faster and reduce interest. A student entering a lower-paying but socially important field may rely more on income-driven repayment or service-based forgiveness. Neither path is automatically better; the key is understanding the relationship between income, debt, and long-term goals.

Before borrowing, compare total school cost, likely starting salary, graduation rate, and job placement data. Borrow only what is necessary. Grants, scholarships, work-study, part-time work, community college transfer plans, and living at home for part of college can reduce total debt.

After borrowing, read every notice, know who your servicer is, and keep records. If your address, school status, or job changes, update your account. If repayment feels difficult, contact the servicer early rather than missing payments.

Students should also watch for scams. Real loan servicers and federal aid programs do not rely on sensational promises like "instant forgiveness" in exchange for a large upfront fee. If someone asks for payment to unlock a program that should already be available through official channels, that is a warning sign.

"The safest student loan is the one you fully understand before you borrow."

Thinking carefully about repayment does not mean avoiding education. It means treating education as a major financial decision tied to your career path, income, and future freedom. The smartest borrowers are not simply the ones who borrow the least; they are the ones who match their borrowing, repayment strategy, and career planning in a realistic way.