A lot of money stress does not come from having no money at all. It comes from having money come in, watching it disappear, and then realizing too late that something important is due. A financial plan helps you avoid that feeling. It gives your money a job before it slips away on random purchases, subscriptions, delivery fees, or impulse spending.

If you are 16, your financial life may already be more real than people assume. You might earn money from a part-time job, freelance work, pet sitting, content editing, reselling items, or help with a family business. You may pay for gas, a phone plan, clothes, streaming services, school supplies, hobbies, gifts, or food when you are out with friends. At the same time, you may be thinking about bigger goals like a car, training after high school, college costs, moving out, or building savings. That is exactly why financial planning matters now, not "someday."

A financial plan is a practical system for deciding how to use your money so that your current needs are covered while you also move toward future goals. It is not just a budget on paper. It is a set of choices about what matters most, what can wait, and how to prepare for problems before they become emergencies.

When you plan well, you are more likely to pay for essentials on time, avoid panic when surprise expenses happen, and make progress toward goals that used to feel too expensive. When you do not plan, small spending can quietly block important priorities. For example, spending $18 on food delivery three times a week may not seem huge, but over four weeks that becomes $216. In three months, that is $648. That amount could cover part of a laptop, emergency savings, course fees, or car maintenance.

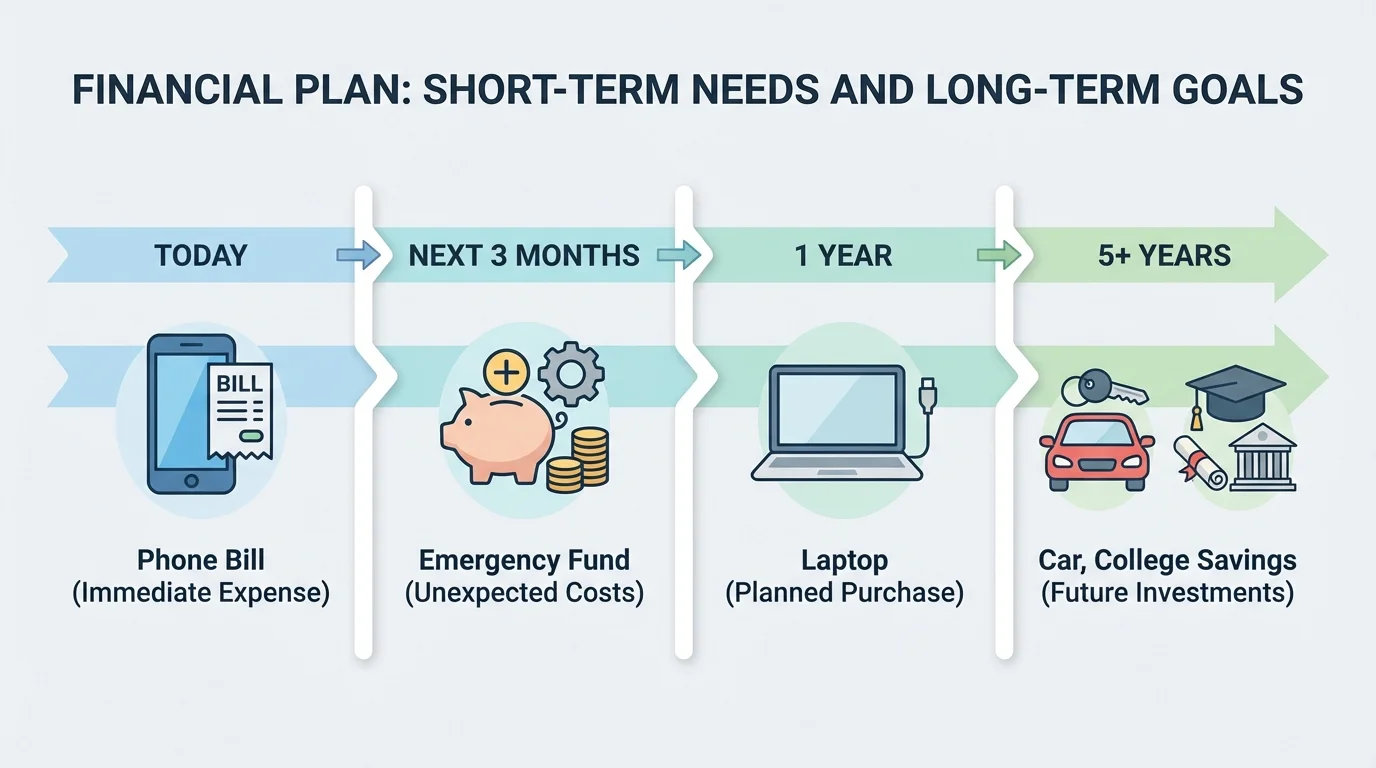

Short-term needs are expenses you must handle soon, usually within days or weeks, such as transportation, a phone bill, hygiene items, or required supplies.

Short-term goals are planned savings targets you want to reach within about a year, such as a concert ticket, new headphones, a gaming upgrade, or holiday gifts.

Long-term goals are bigger financial targets that usually take more than a year, such as college costs, a car, moving out, or retirement savings.

The point is not to stop enjoying your money. The point is to make sure your money reflects your priorities instead of your impulses.

Financial planning gets much easier when you separate money decisions by time horizon, as [Figure 1] shows. If everything feels equally important, you will probably either overspend in the present or feel overwhelmed by the future. Breaking goals into time frames helps you decide what must be handled now, what you can save for over the next few months, and what requires a longer strategy.

For example, replacing worn-out shoes for work may be a short-term need. Saving for a new tablet over the next six months is a short-term goal. Saving for a car down payment over two years is a long-term goal. Paying for streaming services is usually not a need, even if it feels normal. That does not mean you can never spend on entertainment. It means entertainment should not crowd out essentials or important goals.

A useful question is: What happens if I do not pay or save for this? If the consequence is immediate and serious, it is probably a need. If the consequence is disappointment but not danger, it is probably a want or a goal. Another useful question is: When will I need this money? That answer tells you whether to keep it in spending money, a short-term savings fund, or a long-term savings plan.

As you keep planning, return to the time-horizon idea from [Figure 1]. One reason people struggle with money is that they use today's cash to solve today's feelings, then forget that next month and next year are already on the way.

Before you can build a plan, you need a realistic picture of your money. Start with net income, which is the money you actually get to use after taxes or deductions. If your paycheck says $250 but only $221 hits your account, plan with $221, not $250.

Next, list your expenses in categories. Fixed costs stay mostly the same, such as a monthly phone payment or subscription. Variable expenses change from week to week, like snacks, gas, entertainment, and personal care items. Irregular expenses do not happen every week or every month, but they still count. These might include birthday gifts, sports fees, replacing headphones, annual subscriptions, or holiday shopping.

Irregular expenses are where many plans fail. People say, "I forgot that was coming," when really the cost was predictable, just not monthly. A strong financial plan includes these future expenses before they arrive.

Your plan starts with awareness, not restriction. If you do not know where your money goes, you cannot control it. Tracking your money for even two to four weeks often reveals patterns fast: repeated convenience purchases, automatic renewals, or "small" spending that adds up. Once you see the pattern, you can decide what stays, what shrinks, and what gets redirected toward goals.

A quick way to organize your money is to write down four things: money coming in, bills and needs, flexible spending, and savings goals. You can use a notes app, spreadsheet, budgeting app, or paper tracker. The tool matters less than being honest and consistent.

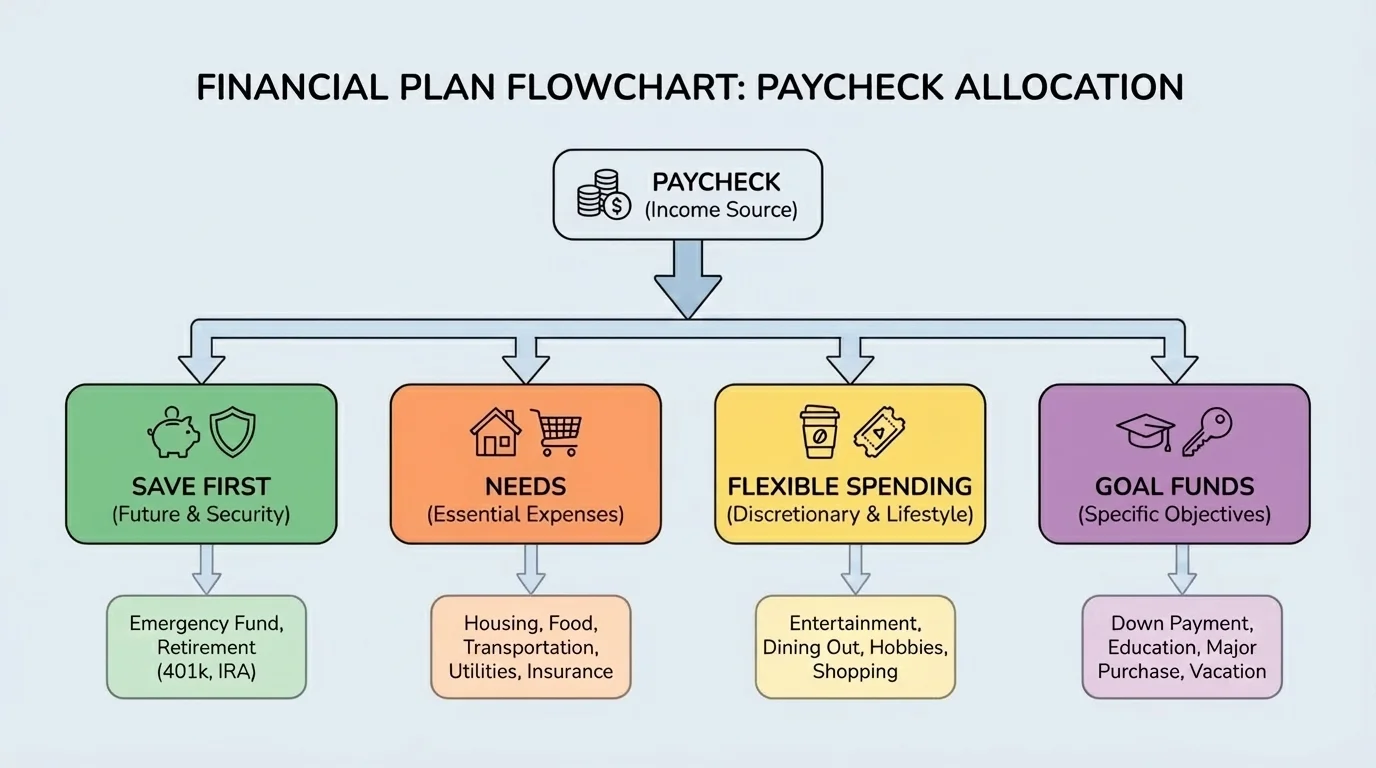

The easiest financial plan is one that tells every dollar where to go, and [Figure 2] illustrates a simple version you can actually use. You do not need a complicated system. You need a repeatable one. A good starter method is to divide your money into four parts: save first, pay needs, allow flexible spending, and fund goals.

Here is a practical order to follow. Step 1: set aside savings right away, even if it is small. Step 2: cover required expenses. Step 3: choose a limit for optional spending. Step 4: send the rest to specific goals. This keeps your plan from becoming "save whatever is left," because usually very little is left.

Suppose you bring in $300 this month. You might decide on a plan like this: $30 to emergency savings, $90 for transportation and your phone, $80 for flexible spending, and $100 toward a larger goal. The math is simple: \(30 + 90 + 80 + 100 = 300\). If your income changes, the categories can change too, but the structure stays useful.

This is where opportunity cost matters. Opportunity cost means what you give up when you choose one use for your money instead of another. If you spend $60 on a game release, that same $60 cannot help with your emergency fund, shoes for work, or your car savings. The purchase may still be worth it to you, but you should see the trade-off clearly.

Try to make your spending plan realistic. If you give yourself $0 for fun, the plan may look perfect but fail fast. A better plan includes some enjoyable spending without letting it take over.

One of the smartest early goals is a small emergency fund. This is money set aside for urgent, unexpected expenses: replacing a lost charger you need for schoolwork, paying for a ride when transportation falls through, helping with a small medical cost, or covering a sudden work-related expense.

Your first emergency goal does not need to be huge. Even $100 to $300 can make a real difference. The purpose is to stop surprise costs from wrecking your entire plan or pushing you to borrow money. Later, you can build it larger.

Small emergency savings often matter more at first than chasing a big goal. A single unexpected expense can force you to spend money meant for something else, which sets off a chain reaction of missed goals and stress.

If you have irregular income, an emergency buffer becomes even more important. Some months may be strong, while others are slower. Saving during better weeks helps protect you during weaker ones.

Short-term goals work best when you turn them into monthly targets. If you want something in the future, divide the total cost by the number of months until you need it. This creates a clear saving amount instead of a vague wish.

For example, suppose you want $240 for holiday gifts in six months. Divide the cost by the timeline: \(240 \div 6 = 40\). That means saving $40 each month. If you wait until the last month, the same goal suddenly feels stressful. If you start early, it becomes manageable.

This approach is often called a sinking fund: money you set aside little by little for a specific future expense. Sinking funds are useful for gifts, clothes, subscriptions, sports fees, tech upgrades, and travel.

Worked example: saving for a laptop

You want a laptop that costs $720 in nine months.

Step 1: Identify the target amount and timeline.

The target is $720 and the timeline is 9 months.

Step 2: Divide the total by the number of months.

\(720 \div 9 = 80\)

Step 3: Turn that into a monthly rule.

Save $80 each month, or about \(80 \div 4 = 20\) per week if that matches your pay schedule better.

The goal becomes much easier when you break it into regular pieces instead of thinking about the full $720 all at once.

If the monthly amount is too high, you still have options: choose a less expensive version, extend the timeline, increase income, or cut another expense. A financial plan is not about forcing impossible numbers. It is about adjusting until the plan fits real life.

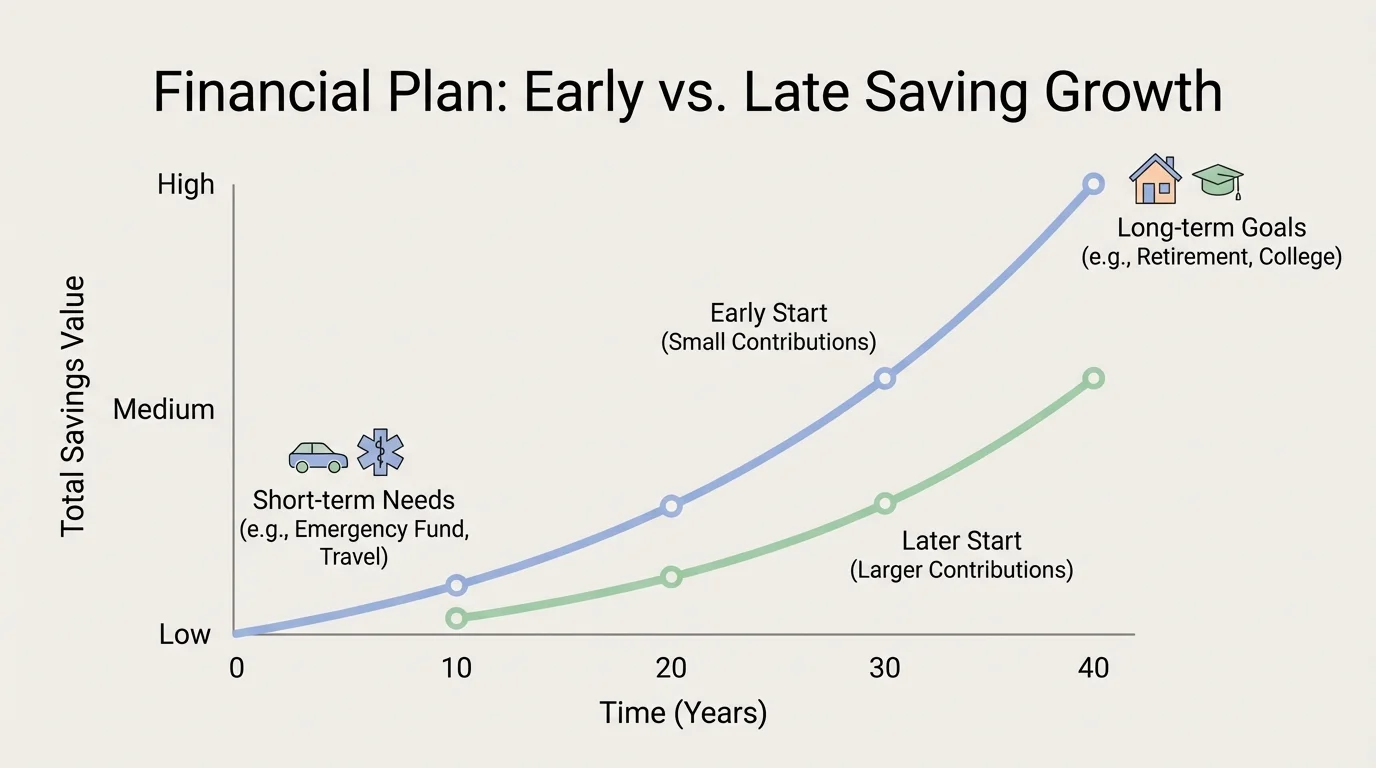

Long-term goals can feel far away, but time is one of the most powerful tools in money growth, as [Figure 3] illustrates. Starting early matters because small amounts saved regularly have more time to build. Even if your amounts are modest now, the habit is valuable.

Long-term goals for someone your age might include college or training costs, a used car, moving expenses, starting independent living, or eventually compound growth through investing. Compound growth means your money grows, and then the growth itself can also grow over time. You do not need to become an investor today to understand the idea. The main takeaway is simple: earlier is usually better.

Suppose one person saves $25 a month starting now, while another waits two years to start saving the same amount. The earlier saver has more months working in their favor. The difference is not just the amount saved; it is the time available for growth and habit-building.

Long-term planning also means estimating larger costs honestly. A car is not just the purchase price. It may include gas, insurance, registration, maintenance, and repairs. Living on your own is not just rent. It may include utilities, groceries, internet, transportation, and basic household supplies. Thinking ahead prevents expensive surprises.

The idea shown earlier in [Figure 3] also applies to non-investing goals. Starting a car fund or education fund early lowers the monthly pressure later. Time can reduce stress just as much as it increases savings.

A financial plan only works if your daily choices support it. That does not mean every purchase must be "serious." It means purchases should be intentional.

One strong habit is the pause rule. For non-essential spending, wait before buying. For a small purchase, wait at least a day. For a larger one, wait several days. During that time, ask yourself whether the item solves a real problem, how often you will use it, and what goal that money could support instead.

Another strong habit is comparison shopping. Check total cost, not just sticker price. A cheaper item with poor quality may need replacing faster. A monthly payment can also be misleading. Paying $20 a month sounds easier than paying $180 once, but over time subscriptions and installment plans can crowd your budget.

"Do not save what is left after spending; spend what is left after saving."

— Warren Buffett

Be careful with debt, especially buy-now-pay-later offers, credit products, or borrowing from friends. These can make current spending feel easier while making future money tighter. Owing money limits your choices later, which is the opposite of what a good plan should do.

Your financial plan should not stay frozen. Income changes. Priorities change. Prices change. You might get more work hours, lose a side gig, need new equipment, or decide that one goal matters more than another. Reviewing your plan regularly keeps it useful.

A simple monthly review works well. Check how much came in, how much you spent, whether you met your savings targets, and what surprised you. Then adjust. If you overspent on one category, do not just feel bad about it. Figure out why. Was the limit unrealistic? Did you forget an irregular expense? Did a habit like online impulse buying throw you off?

| Question to Ask | Why It Matters | Action You Can Take |

|---|---|---|

| Did I cover my needs first? | Essentials protect your stability. | Move required expenses to the top of your plan. |

| Did I save anything? | Saving builds security and progress. | Automate or transfer savings first. |

| What category went over? | Overspending shows where the plan needs work. | Lower spending triggers or raise the category realistically. |

| What expense is coming soon? | Predictable costs should not feel like surprises. | Create or add to a sinking fund. |

| Do my goals still matter? | Plans should match your real priorities. | Re-rank goals and redirect money if needed. |

Table 1. Monthly questions that help you review and improve a financial plan.

Reviewing does not mean you failed. It means you are managing your money like a real system.

Here is a realistic example. Suppose Maya earns about $480 this month from part-time work and online freelance tasks. She needs to pay $60 for her phone, $70 for transportation, and about $40 for personal care and school-related items. She wants to build an emergency fund, save for a $300 tablet in five months, and still have some spending money.

Worked example: building a monthly plan

Step 1: Start with total available money.

Maya's available money is $480.

Step 2: List needs first.

Phone: $60, transportation: $70, personal care and supplies: $40.

Total needs: \(60 + 70 + 40 = 170\)

Step 3: Add emergency savings.

She puts $50 into her emergency fund.

Step 4: Calculate the tablet sinking fund.

Tablet cost is $300 over 5 months, so \(300 \div 5 = 60\). She saves $60 this month.

Step 5: Find the remaining flexible spending money.

\(480 - 170 - 50 - 60 = 200\)

Maya now knows that $200 is the maximum available for optional spending, extra savings, gifts, entertainment, clothes, or eating out. If that feels too high, she can assign part of it to another goal instead of leaving it unplanned.

This example matters because it shows that planning is not only for people with large incomes. It works with modest amounts too. The goal is not perfection. The goal is direction.

One common mistake is planning with money you expect to earn rather than money you already have or can reliably predict. If your shifts are not guaranteed, build your plan around a lower estimate. Then if you earn more, you can save the extra.

Another mistake is forgetting irregular costs. A third is keeping goals too vague, like "save more" or "spend less." Vague goals are hard to follow. Specific goals are better: save $25 a week, keep entertainment under $40 this month, or put $15 from every paycheck into an emergency fund.

People also get stuck comparing themselves to others. Someone on social media may seem to buy everything easily, but you do not see their debt, family support, stress, or lack of savings. Your financial plan should match your life and your priorities, not somebody else's feed.

Finally, do not confuse a setback with failure. If one month goes badly, restart. A strong money habit is not "never making mistakes." It is noticing the mistake, correcting it, and continuing.

Try this: pick one short-term need, one short-term goal, and one long-term goal today. Write the amount each one needs, the deadline, and where the money will come from. Then decide the first transfer or saving amount you can make this week, even if it is small. A financial plan becomes real when it turns into action.