Some of the biggest adult decisions do not feel dramatic in the moment. They look like replying to an email, showing up on time, comparing two job offers, deciding whether you can afford to move, or remembering to renew a document before it expires. Future planning is not just about having a dream. It is about turning your choices today into a life that is more stable, flexible, and genuinely yours.

At your age, the shift toward adulthood is already happening. You may be thinking about work, training, college, independent living, transportation, healthcare, finances, or how much responsibility you want to take on right away. Good planning does not guarantee a perfect outcome, but it gives you something powerful: direction. When you know what matters to you and what your next step is, decisions become less overwhelming.

Future planning is the process of thinking ahead, setting priorities, and preparing for decisions, responsibilities, and changes before they become urgent.

Transition is a period of change from one stage of life to another, such as moving from high school into work, training, college, or independent living.

Responsibility means being accountable for your choices, commitments, and the effects they have on you and other people.

Future planning matters because adulthood brings more freedom, but freedom comes with consequences. If you plan well, you usually gain more options. If you ignore planning, small problems can stack up fast. Missing one payment can hurt your credit. Ignoring an email can cost you an opportunity. Taking on too many commitments can damage your health, your performance, and your relationships.

You are likely making decisions that affect the next few months and the next few years at the same time. A part-time job might help you save for transportation. A certification program might lead to income sooner than a four-year degree. Staying at home for one more year might help you build savings, while moving out right away might give you independence but create financial pressure.

Planning is not about predicting every detail. It is about reducing avoidable stress. When you think ahead, you can ask better questions: What will this cost? How much time will it take? What responsibilities come with this choice? What happens if my first plan changes?

Many adult money problems do not start with low income alone. They often begin with unclear planning, missed deadlines, and commitments that looked manageable one week at a time but were not sustainable over several months.

That is why future planning is tied to responsibility and community. Your choices affect other people too. If you agree to work a shift, join a project, share rent, care for a family member, or volunteer in your community, other people may be counting on you. Planning helps you be dependable, not just ambitious.

Some decisions are big and obvious, like whether to attend college, start full-time work, join the military, begin an apprenticeship, or take a gap year. Others are quieter but still important: whether to get a checking account, how to build transportation access, whether to sign a contract, or how to manage your online reputation when employers and programs may look you up.

One useful way to prepare is to sort upcoming decisions into categories. This keeps your mind from treating every issue as one giant problem.

| Decision Area | Common Questions | Risk if You Do Not Plan |

|---|---|---|

| Education and training | What path fits your goals, strengths, and budget? | Debt, wasted time, low motivation |

| Employment | What job gives income, experience, and growth? | Burnout, unstable schedule, poor fit |

| Money | Can you afford your current lifestyle and future goals? | Overdrafts, unpaid bills, dependence |

| Housing | Will you live at home, with roommates, or independently? | Unsafe lease choices, unaffordable rent |

| Health | How will you handle appointments, sleep, food, and stress? | Declining performance and well-being |

| Relationships and community | Who supports you, and what boundaries do you need? | Isolation, conflict, poor decisions under pressure |

Table 1. Major decision areas that often shape the transition into adulthood.

Notice that these areas connect. A job choice affects sleep, money, and time. Housing affects transportation and food costs. A training program affects your schedule and your stress level. Adult decisions rarely stay in one category.

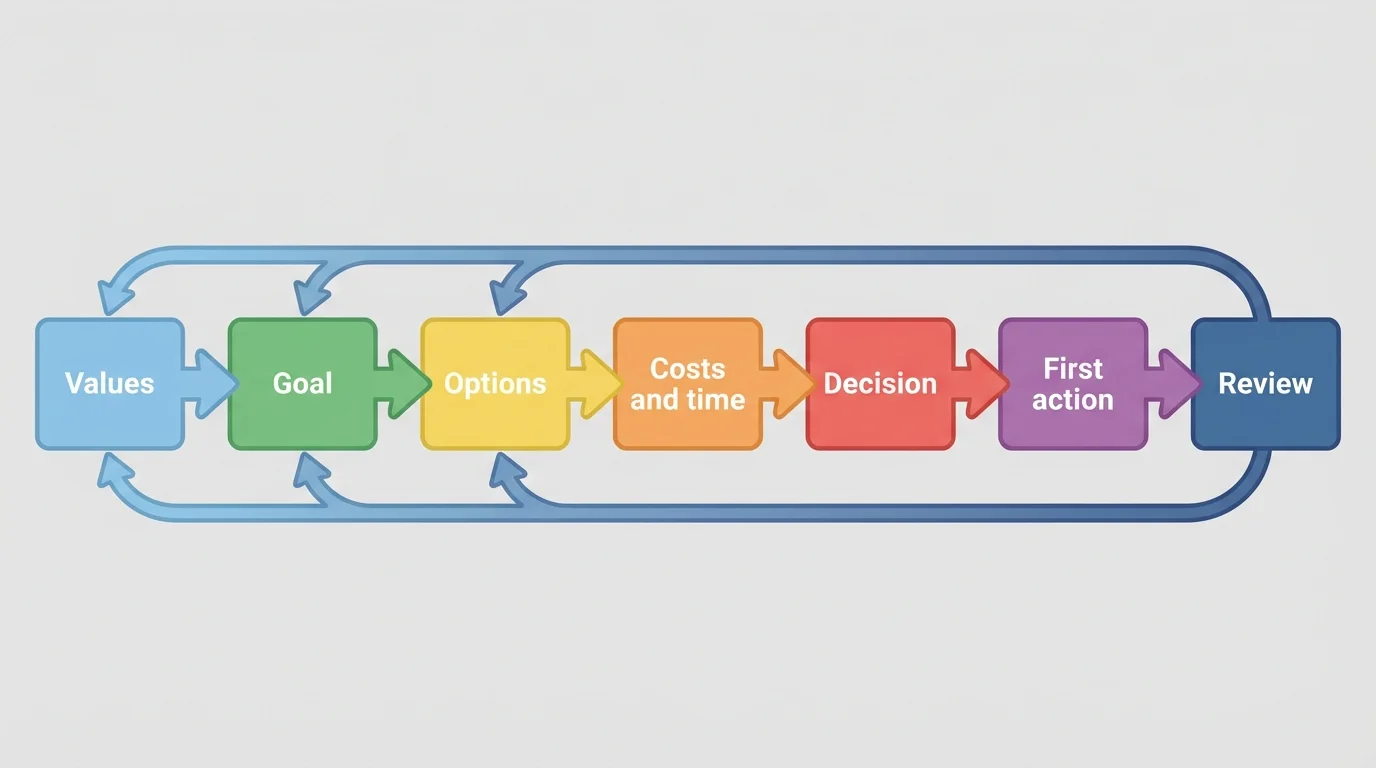

A useful decision-making framework helps you avoid choosing based only on emotion, pressure, or urgency. [Figure 1] shows a process that starts with what matters to you and moves toward action and review. That matters because a plan is not finished when you make a choice; it only works if you follow through and check whether it is actually working.

Step 1: Identify your values. Ask yourself what matters most right now. Income? Stability? Flexibility? Education? Mental health? Family responsibilities? A decision that looks good on paper may still be wrong if it conflicts with your priorities.

Step 2: Define the goal clearly. "I want to do well" is too vague. "I want to save $2,400 in 12 months for a used car down payment" is clearer. "I want to complete a certificate by next spring" is clearer than "I should probably study something."

Step 3: List your options. Try for at least three. When people are stressed, they often act as if they only have two choices. For example: work full-time now, attend community college while working part-time, or take a short certification program and reassess later.

Step 4: Estimate costs, time, and responsibilities. If a program costs $6,000 and you can contribute $250 each month, then covering the full amount yourself would take \(6000 \div 250 = 24\) months, not counting other expenses. That does not automatically make it a bad choice, but it changes your timeline.

Step 5: Choose your next action, not just your final dream. A strong first action might be updating your resume, booking a campus tour, comparing financial aid packages, or setting up automatic savings.

Step 6: Review and adjust. Plans are not promises to never change. If new information appears, adjusting is responsible, not weak. Later in your planning, the flow in [Figure 1] still applies: values guide the decision, and review keeps you from drifting.

Case study: Choosing between two paths after graduation

You are deciding between a warehouse job that starts immediately and a medical assistant training program that begins in three months.

Step 1: Name your priorities.

You need steady income soon, but you also want a path that can grow into a career.

Step 2: Compare short-term and long-term effects.

The warehouse job pays now, while the training program delays income but may increase future earning potential.

Step 3: Calculate one practical issue.

If the training program costs $3,200 and you have $800 saved, you still need $2,400. Saving $300 per month means \(2400 \div 300 = 8\) months to cover that amount on your own.

Step 4: Create a blended plan.

You might take the warehouse job temporarily, build savings, and apply for the next training cycle instead of treating the choice as all-or-nothing.

The best decision is not always the fastest option or the most impressive-sounding one. It is the one that fits your real situation and your future direction.

Planning also protects you from pressure. Friends, relatives, and social media may make certain paths look obvious. But a choice is only strong if you understand its costs and responsibilities for your life.

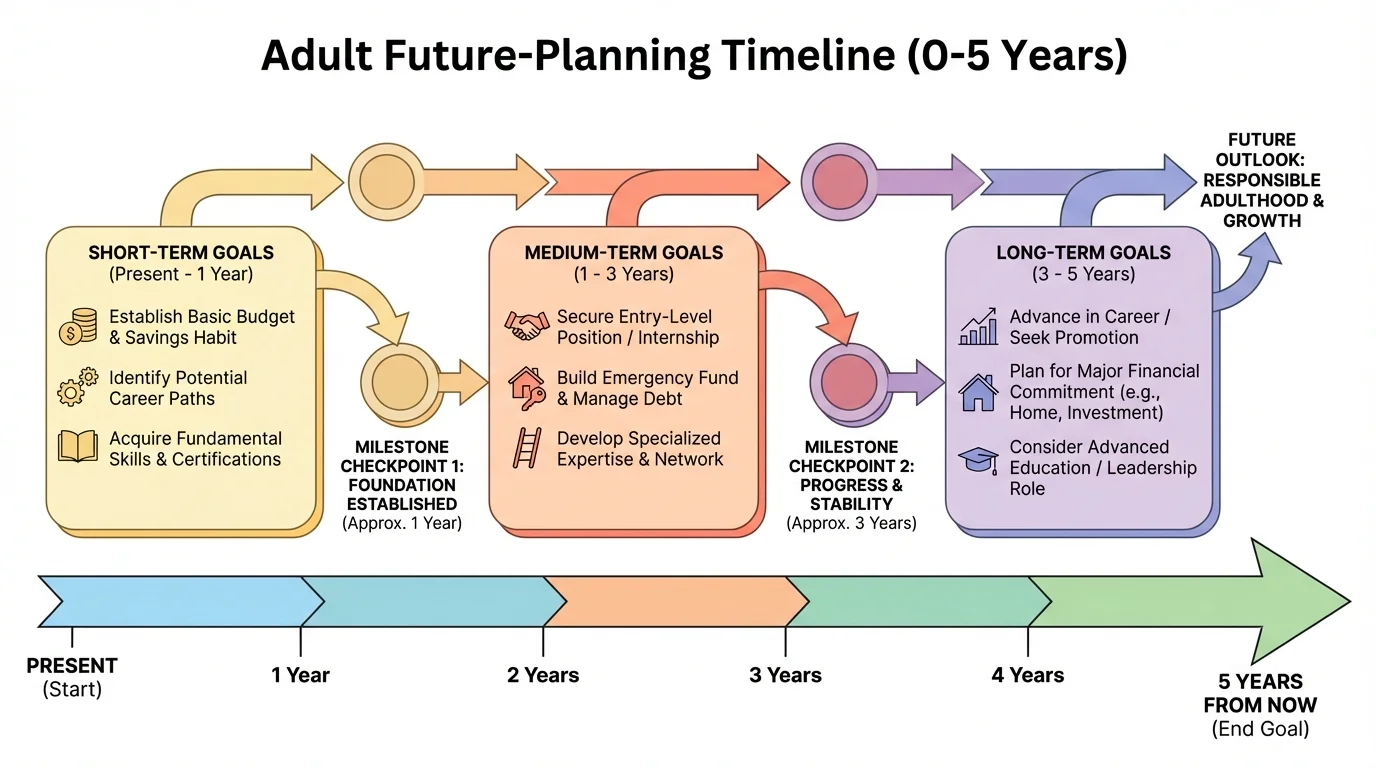

[Figure 2] shows how goals are useful when they connect different time horizons. A short-term goal should support a medium-term goal, and a medium-term goal should support a long-term direction. Without that connection, people stay busy but do not move forward.

Use three levels of goals. Short-term goals usually cover the next days, weeks, or few months. Medium-term goals often cover the next year or two. Long-term goals look several years ahead. You do not need your entire life mapped out, but you do need a direction strong enough to guide your next decisions.

A helpful way to test a goal is to ask whether it is specific, measurable, realistic, and connected to a deadline. "Save money" is weak. "Save $1,200 in six months by setting aside $50 per week" is stronger because it tells you exactly what to do.

Milestones matter because large goals can feel intimidating. If your long-term goal is to live independently, your milestones might include building an emergency fund, learning to budget, getting reliable transportation, increasing work hours, and researching housing costs. Each milestone makes the future less abstract.

It also helps to build a contingency plan. This is your backup plan if the first path changes. For example, if you do not get accepted into your first-choice program, your backup might be taking prerequisite courses, working part-time, and reapplying. A backup plan is not negative thinking. It is realistic thinking.

Why backup plans reduce stress

Stress often rises when a person treats one outcome as the only acceptable outcome. A backup plan keeps disappointment from turning into panic. It protects momentum. If one door closes, you already know your next move.

A goal should challenge you, but it should not ignore your actual resources. If you currently work 15 hours a week and care for siblings in the evening, a plan that assumes unlimited free time will collapse. Good planning is honest. It respects your energy, your schedule, and your responsibilities.

That honesty also prevents shame. If a plan fails because it was unrealistic, the answer is usually not "try harder." The answer is "plan smarter." The timeline in [Figure 2] works because each stage has checkpoints, not because everything happens perfectly.

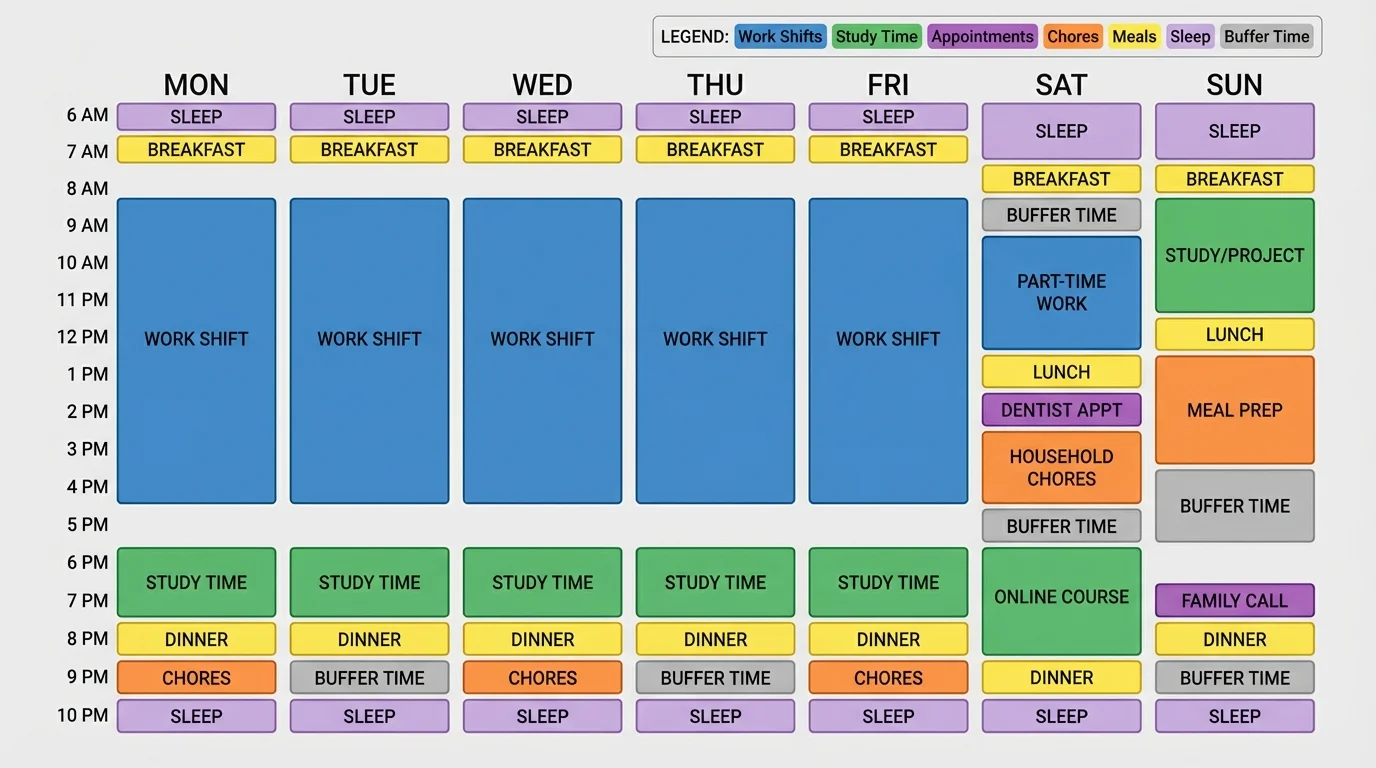

Adult life often feels less like one giant test and more like managing a series of repeating responsibilities. [Figure 3] highlights this balance. The key challenge is not only what you want to do. It is how you handle your limited time, energy, and money from week to week. Overcommitting in one area usually creates problems somewhere else.

Start by tracking your responsibilities in five categories: money, time, communication, health, and follow-through. If one category is weak, your whole plan can wobble. For example, you might have enough money for a class, but if you never check email and miss registration deadlines, the opportunity still disappears.

Time budgeting is one of the most practical skills you can build. A week has \(24 \times 7 = 168\) hours. That sounds like a lot until you subtract sleep, work, family responsibilities, commuting, meals, chores, and personal care. Planning your week on purpose helps you see what is actually available.

For example, if you sleep about \(8\) hours per night, that uses \(8 \times 7 = 56\) hours. If you work \(20\) hours and spend \(10\) hours on coursework, you are already at \(56 + 20 + 10 = 86\) hours before adding meals, chores, transportation, and downtime. This is why responsible planning includes buffer time. If every hour is spoken for, one problem can derail your week.

Money responsibilities work the same way. Before agreeing to a payment plan, membership, subscription, or lease, know the total monthly impact. If your income is $1,400 per month and your fixed expenses are $950, then you have $450 left before savings, emergencies, and flexible spending. If you casually add a $90 payment, a $35 subscription, and a $60 service plan, your remaining amount becomes \(450 - 90 - 35 - 60 = 265\). Small commitments become serious quickly.

Practical weekly responsibility check

Step 1: List all non-negotiables.

Include work shifts, assignment deadlines, appointments, family duties, and transportation needs.

Step 2: Add maintenance tasks.

Include laundry, meal prep, cleaning, exercise, and document checks.

Step 3: Leave buffer time.

Protect at least a few open blocks each week for delays, extra errands, or rest.

Step 4: Review every Sunday evening or Monday morning.

Look ahead before the week gets busy, not after problems appear.

This kind of routine is simple, but it builds reliability fast.

Communication is another responsibility people underestimate. Responding professionally, asking clarifying questions, and confirming important details can prevent major problems. If you are unsure about a shift, fee, deadline, or form, ask early. Silence often creates bigger consequences than asking a basic question.

Some choices have longer-lasting consequences, so they deserve slower thinking. These include signing a lease, taking on debt, accepting a job with unclear expectations, quitting a job without a transition plan, lending money you cannot afford to lose, or agreeing to responsibilities that exceed your capacity.

In these moments, use a pause-and-check method. First, identify the decision. Second, ask what commitment it creates. Third, ask what it costs in money, time, stress, and opportunity. Fourth, ask what happens if things go wrong. Fifth, decide whether you need advice before saying yes.

"Not deciding is still a decision."

— Practical life principle

This matters because avoidance has consequences too. If you do not compare job offers, you may accept poor conditions by default. If you do not read a contract, you may agree to fees you did not expect. If you ignore health appointments, the problem may become harder and more expensive to handle later.

Try to separate urgency from importance. Some things feel urgent because other people want an answer now. That does not always mean they are good choices. A legitimate opportunity can usually survive a reasonable request like, "I'd like until tomorrow to review the details."

Case study: Can you afford to move out?

Step 1: Estimate monthly income.

Suppose your take-home income is $1,800 per month.

Step 2: Add likely fixed costs.

Rent is $700, utilities are $120, phone is $55, transportation is $180, groceries are $250, and insurance is $140. Total fixed costs are \(700 + 120 + 55 + 180 + 250 + 140 = 1,445\).

Step 3: Compare what remains.

You would have \(1800 - 1445 = 355\) left for savings, emergencies, toiletries, medical costs, clothing, and everything else.

Step 4: Judge stability, not just possibility.

If your hours change often, $355 may not be enough margin. The move might be possible on paper but unstable in real life.

Good planning asks not only, "Can I do this?" but also, "Can I do this consistently without constant crisis?"

High-stakes choices are also where your opportunity cost matters. Opportunity cost is what you give up when you choose one path over another. Taking a full-time job may give you income now but reduce time for training. Choosing school full-time may increase future options but reduce immediate earnings. Strong planning means acknowledging both sides.

Planning does not mean doing everything alone. One sign of maturity is knowing when to ask for guidance. A support system might include family, mentors, supervisors, older friends, counselors, advisors, coaches, faith leaders, or community organizations. The goal is not to let others make every decision for you. The goal is to gather useful information and perspective.

It helps to know what kind of support you need. Sometimes you need emotional support: someone to help you calm down and think clearly. Sometimes you need practical support: help comparing financial aid, editing a resume, understanding a bill, or finding local services.

You already use planning skills in everyday life when you meet deadlines, compare prices, prepare for events, or organize your week. Adult future planning builds on those same habits; the stakes are just higher, and the consequences last longer.

Community matters because independence does not mean isolation. Reliable adults ask questions, use resources, and maintain relationships. If you are entering a new environment, learn where support exists before you are in crisis. Save important phone numbers, know how to access healthcare, understand your transportation options, and keep copies of key documents.

Your reputation is part of your future too. The way you communicate online, meet commitments, and treat people can shape references, recommendations, and opportunities. Being respectful, honest, and dependable is not only the right thing to do; it is also practical.

You do not need a perfect five-year plan by tomorrow. What you do need is a workable next-year plan. Start with one page or one digital note and divide it into categories: money, work, education or training, health, relationships, and life skills. Under each category, write one goal, one action for this month, and one possible obstacle.

Then create a realistic rhythm. Review your goals once a month. Check your schedule once a week. Check deadlines and messages daily. Review spending every few days if money is tight. Small reviews prevent large messes.

Try This: Choose one adult decision you expect to face in the next six months. Write down your goal, your options, the likely costs, the responsibilities involved, and one backup plan. Then talk it through with a trusted adult or mentor.

Try This: Build a mini emergency cushion, even if it starts small. Saving $20 per week leads to \(20 \times 52 = 1,040\) dollars in a year. A modest cushion can protect you from turning every surprise into a crisis.

Try This: Audit your week honestly. Where are you losing time, money, or energy? One repeated issue, like sleeping too little or forgetting deadlines, can quietly weaken every other goal.

The purpose of future planning is not to control every outcome. It is to make better decisions, handle transitions with less chaos, and grow into responsibilities with intention. Adulthood becomes more manageable when you stop treating important choices as random and start treating them as plannable parts of your life.