Have you ever had enough money to buy a small treat today, but also wanted something bigger later? That one choice tells a big story about money. Every time you earn, save, or spend, you move a little closer to a goal or a little farther away from it. Learning how these choices work together can help you feel more confident and more in control of your money.

A financial goal is something you want to do with money. Maybe you want to buy a book, save for sports equipment, get art supplies, or have money ready for a family outing. Financial goals help you make decisions instead of just using money as soon as you get it.

When you make smart money choices, your money has a job. Instead of disappearing quickly, it helps you do something important. If you do not think about your choices, you might spend all your money on little things and then not have enough for something that matters more to you.

Financial goal means a plan for what you want your money to help you do. A goal can be short-term, which means you can reach it soon, or long-term, which means it takes more time and patience.

A short-term goal might be saving $12 for a new puzzle. A long-term goal might be saving $60 for a scooter accessory or a special camp activity. Both are good goals. The difference is mostly how much money you need and how long it takes to save it.

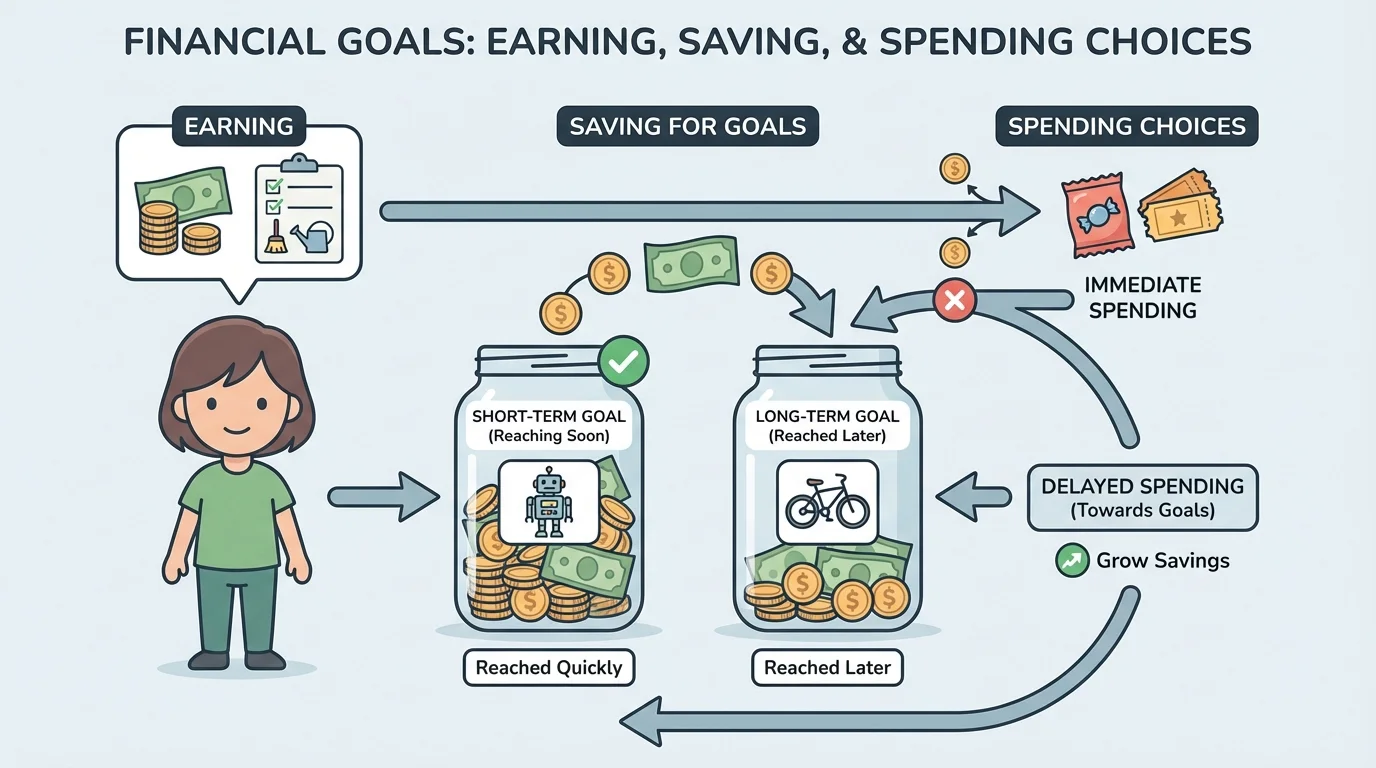

Goals work best when they are clear. As [Figure 1] shows, some goals are closer and some are farther away. If you know the cost and have a plan, your goal stops feeling like a wish and starts feeling possible.

For example, if you want a $20 craft kit and you already have $8, you need $12 more. That means your money plan is about the difference: \(20 - 8 = 12\). Knowing that number helps you decide what to do next.

Goals can also change. Maybe you planned to save for one thing, but later decide something else is more important. That is okay. Good money management is not about being perfect. It is about thinking before you act.

It also helps to choose goals that are realistic. If your goal is very large, you can break it into smaller parts. Saving the first $10 feels easier than thinking about the whole amount at once.

Earning money means getting money in a way that is agreed on, such as through an allowance, helping with extra chores, doing a small job, selling something you made with permission, or receiving money as a gift. Not every family handles money the same way, but many children begin learning money skills by managing a small amount of money of their own.

When you earn money, you create choices. If you earn $5, you can spend all $5, save all $5, or split it into parts. If you earn more money over time, you may reach your goal faster. For example, if you save $3 each week, in \(4\) weeks you would save \(3 + 3 + 3 + 3 = 12\), which is $12.

Earning money can teach responsibility. If you know that money comes from effort, time, or patience, you may think more carefully before spending it. That does not mean you can never enjoy your money. It means you understand that every dollar has value.

Example: How earning changes a goal

Maya wants a $24 science kit. She already has $6.

Step 1: Find how much more she needs.

\(24 - 6 = 18\)

Step 2: Decide how much she can earn or save each week.

If Maya can add $3 each week, she saves $3, then $6, then $9, and keeps going.

Step 3: Find how many weeks it will take.

\(18 \div 3 = 6\)

Maya can reach her goal in 6 weeks if she saves $3 each week.

The more steady your earning is, the easier it is to make a plan. A small amount earned regularly can be more helpful than getting a random amount and spending it right away.

Saving means keeping money now so you can use it later. Saving is one of the strongest tools for reaching a financial goal because it protects your money from disappearing on quick purchases.

Saving does not always mean huge amounts. Even small amounts matter. If you save $2 from one week and $4 from the next week, you now have $6 because \(2 + 4 = 6\). Small steps can lead to big results over time.

You can save in different places, such as a labeled jar, envelope, or savings account with help from a trusted adult. The important part is that your saved money is separated from the money you plan to spend now. That separation helps you stay focused.

Why saving works

Saving gives your future self a chance. When you do not spend all your money right away, you keep options open. You may be able to buy something important, handle a surprise expense, or reach a bigger goal that would be impossible if you used every dollar immediately.

Sometimes saving feels hard because waiting is hard. You may see something fun online or in a store and want it right away. But waiting can help you decide whether you really want it. Often, a day or two later, the item does not feel as important.

This is why people sometimes say to "pay yourself first." For a child, that can mean putting part of your money into savings before you start thinking about spending the rest.

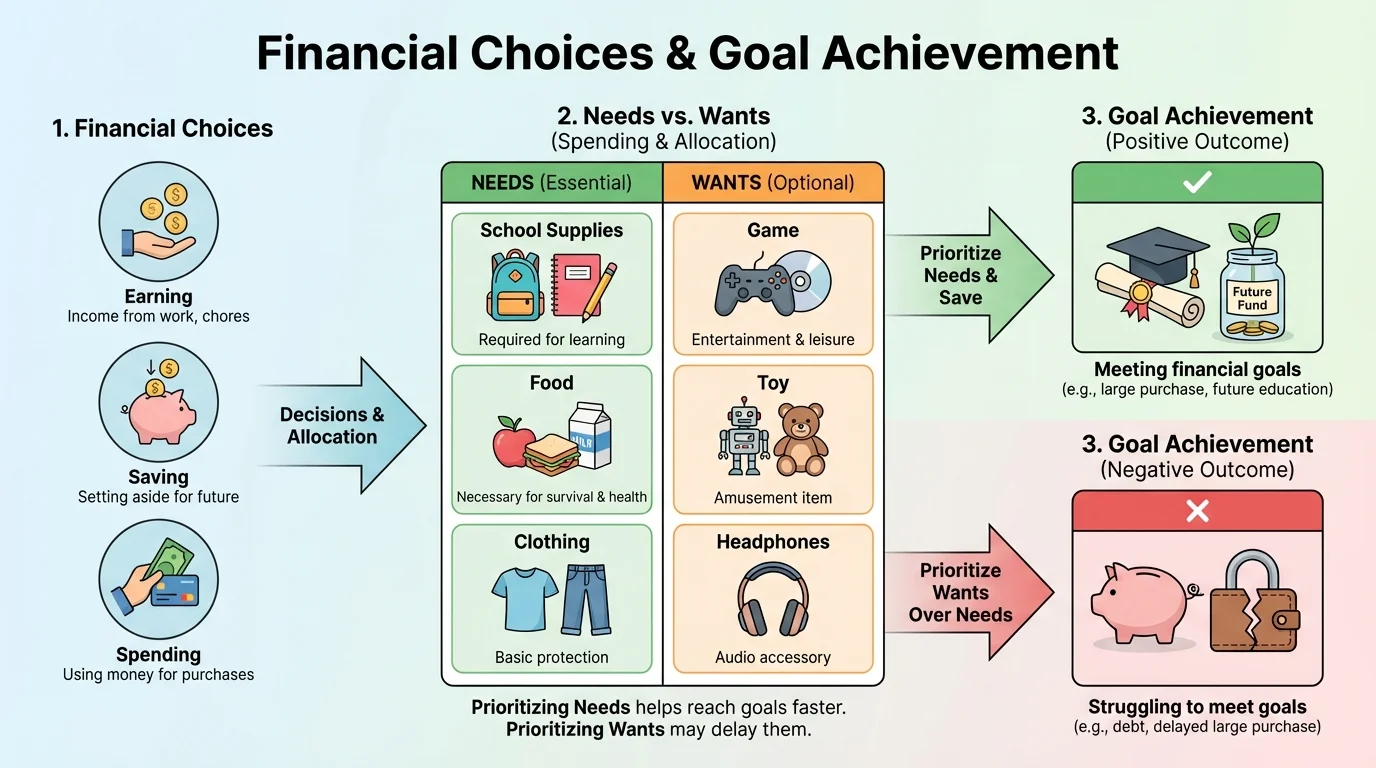

Spending means using money to buy something. Spending is not bad. In fact, money is meant to be used. The key is to spend in ways that match your goals. As [Figure 2] explains, some spending choices matter more than others because some things are needs and some are wants.

A need is something important for daily living, health, learning, or safety. A want is something you would like to have but do not need in order to be okay. Children often spend money on wants, and that is normal, but it is smart to notice the difference before buying.

Another important idea is opportunity cost. Opportunity cost is what you give up when you choose one thing instead of another. If you spend $10 on a game add-on today, you might give up the chance to save that $10 toward headphones you wanted next month.

Suppose you have $15. You can buy a small toy for $15, or you can keep the $15 and add it to your savings for a $30 item. If you buy the toy now, your savings do not grow. If you save the money, you are choosing the larger goal over the smaller one.

Before spending, ask yourself a few simple questions. Do I need this now? Do I already have something like it? Will buying this make it harder to reach my goal? Am I buying because I planned to, or just because it looks exciting right now?

These questions are especially useful for online shopping. Pictures, videos, and ads are designed to make items look amazing. A smart shopper slows down, checks the price, and thinks first.

Stores and apps often try to make quick buying feel easy. That is why waiting a little while before purchasing can help you make a better decision.

Later, when you compare a new purchase to your bigger goal, it still helps to sort your choices instead of reacting fast.

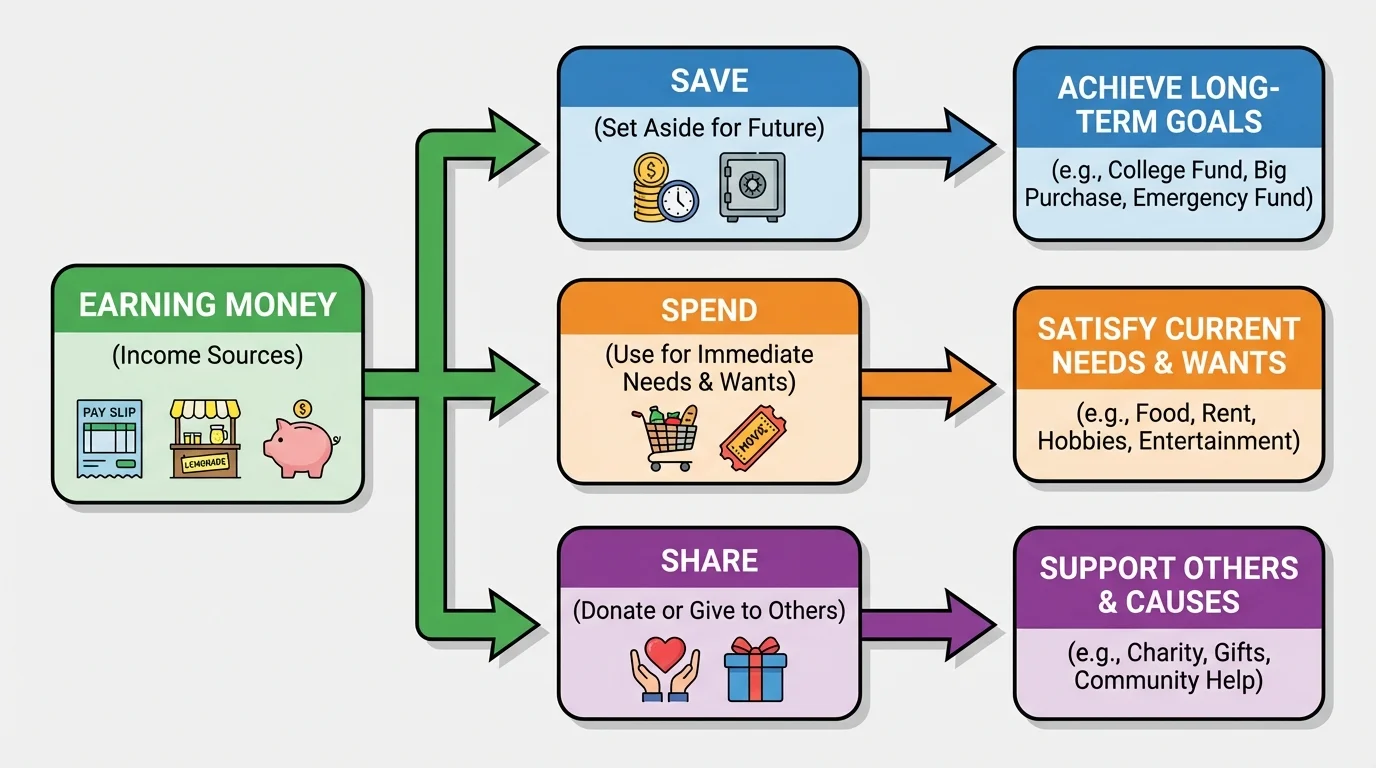

Money choices are connected, not separate. As [Figure 3] shows, money usually starts with earning or receiving it, and then you choose where it goes. You might save some, spend some, and sometimes share some. Each choice changes how quickly you can reach your goal.

Think of your money like water pouring into cups. One cup is for saving, one is for spending, and one might be for giving. If all the water goes into spending, the saving cup stays empty. If some goes into saving every time, the saving cup slowly fills up.

Let's say Jordan gets $10. Jordan decides to save $6 and spend $4. The saving part is larger, so Jordan reaches a goal faster. But if Jordan spends $9 and saves $1, the goal will take much longer.

Here is the idea using simple numbers. If a goal costs $25 and you save $5 each time you get money, it takes \(25 \div 5 = 5\) saving times. But if you save only $1 each time, it takes \(25 \div 1 = 25\) saving times. Your choices affect the speed of progress.

| Choice | Money Received | Saved | Spent | Result |

|---|---|---|---|---|

| Plan A | $10 | $6 | $4 | Goal grows faster |

| Plan B | $10 | $3 | $7 | Goal grows slowly |

| Plan C | $10 | $0 | $10 | No progress toward goal |

Table 1. A comparison of how different saving and spending choices change progress toward a goal.

This is why even a simple plan matters. You do not need lots of money to make good choices. You need a goal, a plan, and the habit of thinking ahead.

You can make a money plan in just a few steps. First, choose one goal. Be specific. "I want something fun" is too broad. "I want a $18 sketchbook set" is clearer.

Second, find out how much the item costs and how much money you already have. If the item is $18 and you already have $7, then you still need \(18 - 7 = 11\), which is $11.

Third, decide how much you can save each time you get money. If you can save $2 each week, you can estimate the time. Since \(11 \div 2 = 5.5\), it will take about \(6\) weeks because you cannot save half a week in this plan.

Example: A simple savings plan

Leo wants a $16 soccer ball pump and has $4.

Step 1: Find the missing amount.

\(16 - 4 = 12\)

Step 2: Choose a saving amount.

Leo decides to save $3 each time he gets money.

Step 3: Estimate the number of times needed.

\(12 \div 3 = 4\)

Leo needs 4 times receiving money to reach his goal.

Fourth, track your progress. You can make a chart on paper or in a notes app. Every time you add money, write the new total. Watching the total grow can keep you motivated.

Fifth, check your plan if something changes. If the price goes up, you may need more time. If you get birthday money, you may reach your goal sooner. Plans can be adjusted.

Let's look at everyday situations. Suppose you have $8 and want to buy a digital sticker pack for $8. At the same time, you are saving for a $20 board game. If you spend the $8 now, your board game goal stays at $20 away. If you save the $8, then only \(20 - 8 = 12\) is left.

Here is another situation. You get $15 as a gift. You decide to spend $5 on a snack and save $10 for a backpack accessory. That is a balanced choice. You enjoyed some money now and still made progress toward your goal.

Now think about a poor choice. You planned to save for a concert ticket for a community event, but each week you spent a little money on tiny items in an app. None of the purchases seemed big, but together they added up. If you spent $3 each week for \(4\) weeks, that is \(3 \times 4 = 12\), which is $12. Small spending can quietly block a bigger goal.

Example: Tiny purchases add up

Sara buys small items online for $2 each time. She does this 5 times.

Step 1: Count the repeated spending.

\(2 + 2 + 2 + 2 + 2 = 10\)

Step 2: Use multiplication to check.

\(2 \times 5 = 10\)

Step 3: Connect it to the goal.

If Sara was saving for something that cost $10, those small purchases used the whole amount.

Even small spending choices can have a big effect on financial goals.

Real life is full of trade-offs. That is why planning ahead is powerful. When you know what matters most, it becomes easier to say yes to some things and no to others.

Good money habits do not happen in one day. They grow over time. One strong habit is saving part of your money every time you receive it. Another good habit is waiting before buying something that was not in your plan.

A helpful habit is talking with a trusted adult before making a bigger purchase. They may help you compare prices, think about quality, or decide if the item is really worth it. Sometimes a lower price on one website is not a better deal if the item is poor quality or if extra costs are added later.

Another habit is celebrating progress, not just the finish line. If your goal is $30 and you have saved $15, you are halfway there because \(15 \div 30 = 0.5\), which means half. Noticing progress can keep you encouraged.

"When you tell your money where to go, you are in charge of your choices."

Remember, every earning choice, saving choice, and spending choice sends your money in a direction. You do not need to be rich to make smart decisions. You only need to be thoughtful, patient, and consistent.

When you look back at [Figure 3], you can see why a plan works so well: money comes in, and then your choices shape what happens next. That is the heart of financial literacy.