Many adults are not struggling because they never earned money. They are struggling because they made money decisions that committed their future paycheck before it even arrived. That is what credit and debt can do: they can either help you build a stable future or quietly make that future more expensive.

If you are 14, you may not have a credit card, car loan, or student loan yet. But you are already close enough to these choices that understanding them matters. In just a few years, you may want a mobile phone plan, a car, an apartment, college, training, or emergency cash. Knowing how borrowing works now helps you avoid costly mistakes later.

Financial stability means your money situation is strong enough that you can pay your bills, handle emergencies, and make plans without constant stress. It does not mean being rich. It means being in control. Credit and debt affect that control because borrowed money always comes with responsibility.

When people use borrowing carefully, it can help them do useful things they cannot pay for all at once. When people borrow carelessly, they can end up owing more than they expected, falling behind on payments, and losing future choices. A person with too much debt may have trouble qualifying for housing, saving for emergencies, or saying yes to opportunities.

Credit is the ability to borrow money now and pay it back later.

Debt is money you owe.

Borrowing is the act of taking money, or receiving something now, with a promise to repay it later.

Interest is the extra money a lender charges for letting you borrow.

Minimum payment is the smallest amount you are allowed to pay on a debt each month.

These ideas show up in real life more often than many teens expect. A credit card lets someone buy now and pay later. A car loan spreads the cost of a vehicle across years. A student loan pays for education now but must be repaid in the future. Even a "buy now, pay later" app is a form of borrowing.

When you use credit, a person or company called a lender gives you access to money, or pays for a purchase on your behalf, with the expectation that you will repay it. If you repay it on time, that can help your financial record. If you do not, it can hurt you for a long time.

The amount you still owe is your debt. Some debt has one fixed amount and a clear end date, like a car loan. Other debt can keep changing, like a credit card balance. The more you owe, the more of your future income is already spoken for.

That is the key issue: borrowing brings future money into the present, but repayment pushes present problems into the future. Sometimes that trade is worth it. Sometimes it is not.

Good borrowing versus harmful borrowing

Borrowing is not automatically bad. It can be useful when it helps you get something important, when you fully understand the cost, and when the payment fits safely into your budget. Borrowing becomes harmful when it is used for things you cannot really afford, when the terms are confusing, or when repayment depends on "hoping things work out."

A practical way to think about borrowing is this: Will this choice make life easier later, or harder later? A smart loan may help you pay for reliable transportation to get to work. A reckless loan may trap you in high payments that block saving and create stress.

Helpful borrowing usually has three features. First, the reason is important, not just impulsive. Second, the total cost is understood. Third, the payment leaves room for other needs like food, transportation, savings, and emergencies.

Harmful borrowing often starts small. Someone says, "It is only $30 a month," but ignores the fact that several small monthly payments add up. If one person has a phone payment of $30, a streaming subscription of $12, a gaming subscription of $10, and a buy-now-pay-later payment of $25, that is already $77 each month. In a year, that becomes \(77 \times 12 = 924\), so $77 a month turns into $924 a year.

That example matters because future financial stability is often damaged by habits, not just by giant mistakes. A few unmanaged debts can reduce the money available for savings, emergencies, and goals.

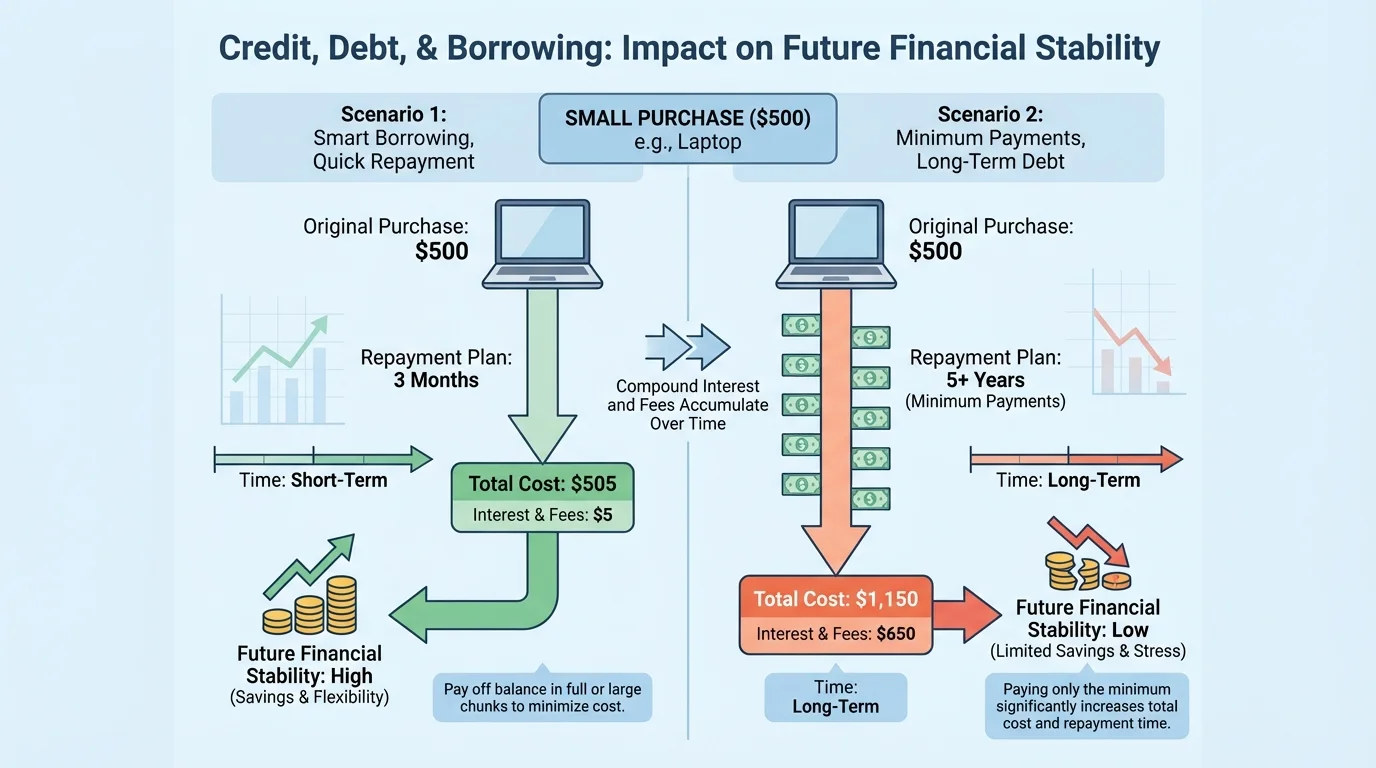

Debt can turn a simple purchase into a much more expensive one, as [Figure 1] shows when a balance is repaid slowly instead of quickly. The price tag in the store is not always the true price if you are borrowing to buy it.

Here is a simple example. Suppose someone buys headphones for $120 using borrowed money. If there is no interest and they pay it off right away, the cost stays $120. But if interest and fees are added, the total can become much higher. If the lender charges $15 in fees and $25 in interest over time, the total paid becomes \(120 + 15 + 25 = 160\). A $120 item has now cost $160.

Minimum payments can be especially dangerous because they create the feeling that everything is fine while the debt lasts much longer. Paying the minimum may keep the account open, but it often means interest keeps growing month after month.

Late payments make things worse. A late fee adds another charge, and the missed payment may be reported to credit bureaus. That means one mistake can hurt in two ways: you pay more money now, and your financial reputation may weaken later.

If a person regularly carries balances and pays late, debt starts acting like a weight on every future decision. Money that could have gone to savings, hobbies, travel, or emergencies now goes toward old purchases.

Case study: Two different choices

Jordan and Alex both want a $300 tablet.

Step 1: Jordan waits and saves.

Jordan saves $50 per month for 6 months. The calculation is \(50 \times 6 = 300\). Jordan buys the tablet for $300 and owes nothing afterward.

Step 2: Alex borrows and pays slowly.

Alex buys the same tablet right away using credit. Over time, Alex pays $300 for the tablet, $36 in interest, and a $20 late fee. The total is \(300 + 36 + 20 = 356\).

Step 3: Compare the outcomes.

Alex gets the tablet sooner, but the extra cost is \(356 - 300 = 56\). That $56 could have gone into savings instead.

The faster choice felt easier at first, but it cost more and reduced future flexibility.

That is why borrowing should always be measured by total cost, not just by whether the first payment seems manageable.

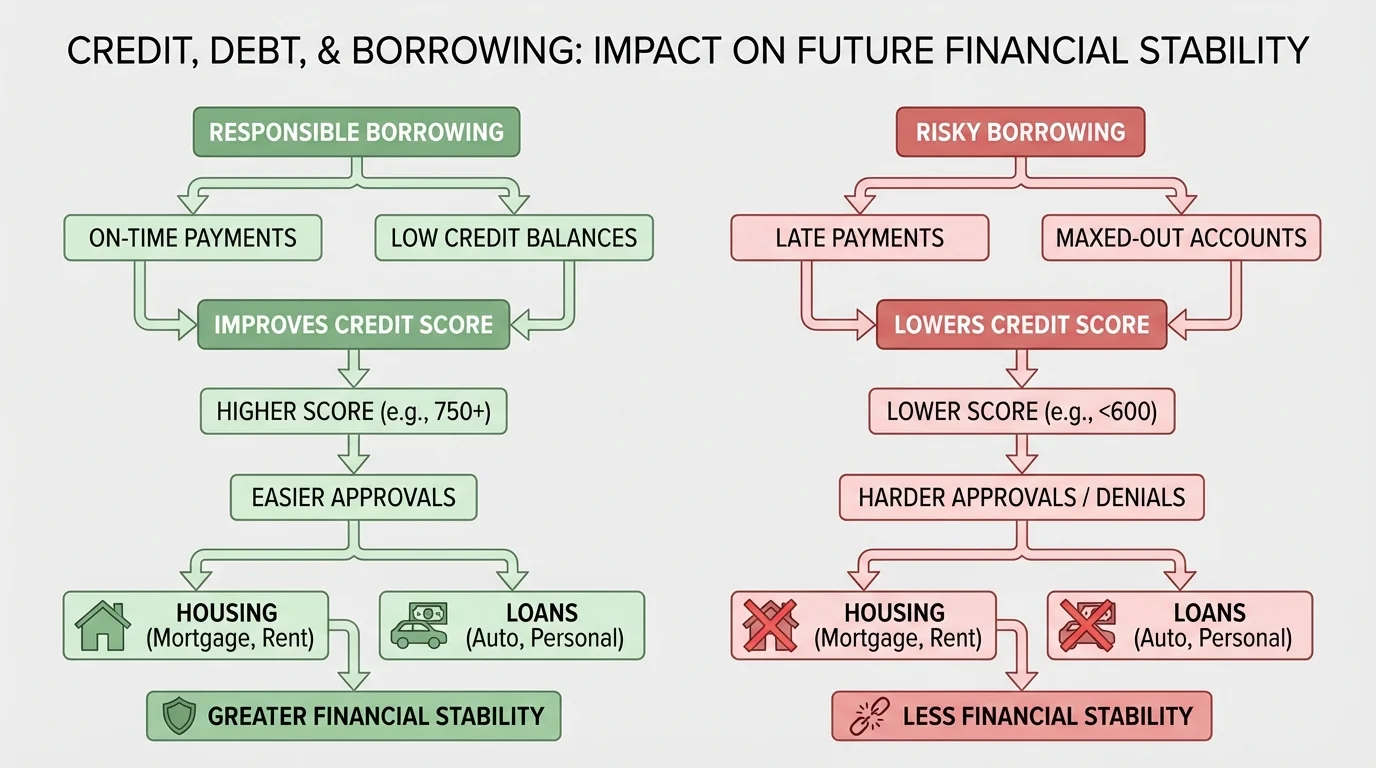

A credit score acts like a financial reputation, and [Figure 2] illustrates how everyday payment habits can push that reputation up or down. Lenders, landlords, and sometimes insurers or employers in certain places may use it as one signal of how reliable someone is with money.

A higher score often comes from habits like paying on time, keeping debt levels lower, and avoiding too many missed payments. A lower score can result from late payments, accounts sent to collections, or using too much available credit.

Why does this matter for stability? Because a strong score can make future borrowing cheaper and easier. A weak score can mean higher interest rates, denied applications, larger deposits, or fewer choices. Two people might want the same car, but the one with stronger credit may pay less over time because the loan terms are better.

Think of it this way: your credit history can follow you into adult life before you feel fully ready for adult responsibilities. As seen earlier in [Figure 1], slow repayment and late fees make debt more expensive. They can also damage the record that future lenders look at.

Even if you are not building a credit history yet, you can still learn the habits that support one later: paying on time, reading terms carefully, and not agreeing to payments you cannot handle.

Many people focus only on whether they can get approved for credit, but the bigger question is whether the terms are affordable. Being approved does not automatically mean a loan is a smart choice.

Approval is not the same as safety. Some lenders make money when borrowers stay in debt longer, especially if fees and interest keep adding up.

Unhealthy debt often shows up through patterns. A person may borrow to cover basic needs every month, make only minimum payments, avoid checking account balances because it feels stressful, or keep opening new accounts to handle older debts.

Another warning sign is losing room in the budget. If most of a paycheck is already committed to past borrowing, there is little flexibility for emergencies. That increases the chance of needing even more debt later.

Emotional signs matter too. Constant money stress, shame, hiding purchases, or arguing with family about bills can be signals that debt is becoming a problem rather than a tool.

| Sign | What It Might Mean | Why It Affects Stability |

|---|---|---|

| Only paying minimums | Debt may last a long time | More interest is paid over time |

| Missing due dates | Payments are not manageable | Fees and credit damage can follow |

| Borrowing for essentials | Income may not cover basic needs | Debt can grow just to maintain daily life |

| Using new debt to pay old debt | The situation may be spiraling | Future income becomes more restricted |

Table 1. Common warning signs that borrowing is hurting financial stability instead of helping it.

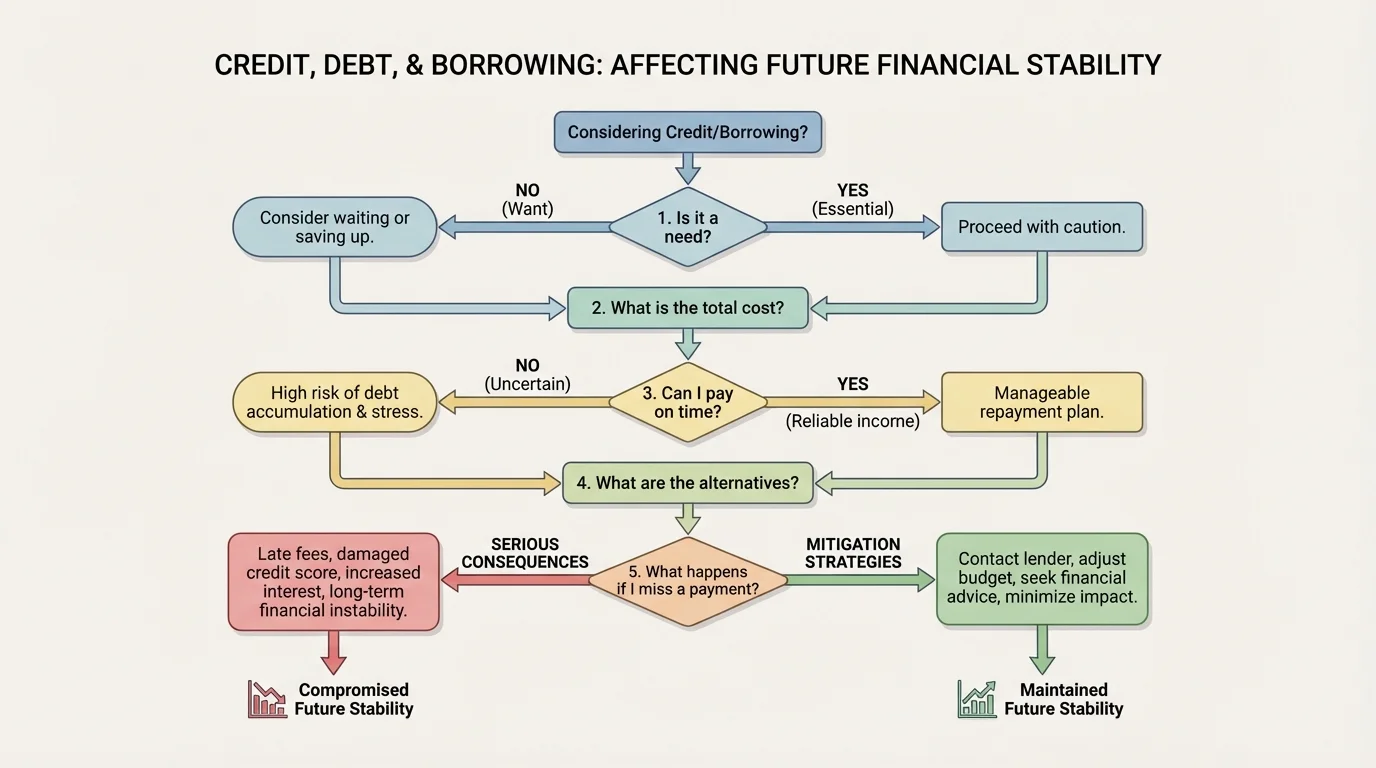

Before borrowing, it helps to slow down and ask a sequence of clear questions. [Figure 3] presents this as a simple decision path you can remember. This is one of the best ways to protect your future self from pressure, impulse, or confusing sales tactics.

Use this checklist before saying yes to any loan, payment plan, or app-based installment offer.

Step 1: Ask whether the item is a need or a want. Borrowing for an emergency repair is different from borrowing for something fun but optional.

Step 2: Ask for the total cost, not just the monthly payment. If a deal says $25 a month for 12 months, calculate the full amount: \(25 \times 12 = 300\). Then check whether fees or interest raise that number even more.

Step 3: Ask whether you could still make the payment if something went wrong, such as fewer work hours, a surprise expense, or a delayed paycheck.

Step 4: Look for alternatives. Could you wait and save? Buy used? Choose a cheaper version? Borrow from a trusted family member with clear terms? Skip the purchase entirely?

Step 5: Read what happens if you miss a payment. If the answer includes late fees, penalty interest, account closure, collections, or damage to your credit record, take that seriously.

Quick decision example

You want a $240 gaming device accessory package offered as $20 per month for 12 months.

Step 1: Calculate the visible total.

The total cost over 12 months is \(20 \times 12 = 240\).

Step 2: Add possible extra costs.

If there is a $15 setup fee, the total becomes \(240 + 15 = 255\).

Step 3: Compare with saving.

If you save $40 per month, you reach $240 in \(240 \div 40 = 6\) months. Waiting cuts the time in half compared with the payment plan and avoids the fee.

Sometimes the smartest borrowing decision is choosing not to borrow.

Later, when you face real financial offers, the same logic still applies. The checklist in [Figure 3] works for phones, furniture, cars, and education choices.

Phone upgrade: A new phone may look affordable because the ad highlights a small monthly payment. But if the payment is locked in for years, your future budget becomes less flexible. If the phone is a want rather than a need, waiting may protect your stability.

Buy now, pay later: These plans can feel harmless because the payments are split into smaller chunks. The risk is that several small plans at once become easy to lose track of. Missing one due date can trigger fees or account problems.

Car loan: A reliable car can support work, family responsibilities, and independence. But buying more car than you can afford can squeeze your monthly budget for years. Insurance, gas, repairs, and registration also matter, not just the loan payment.

Student loan: Education can increase future opportunity, but student borrowing still needs careful thought. A useful question is whether the training or degree is likely to support the income needed to repay the loan reasonably.

Borrowing from friends or family: This may avoid formal interest, but it can create relationship stress. Clear terms, honest communication, and a repayment plan matter. Money problems can quickly become trust problems.

"If you have to borrow for it, you are also buying the repayment."

That idea is simple but powerful. You are never only choosing the item itself. You are choosing the future payments attached to it.

The best protection starts before debt ever appears. Build the habit of comparing prices, delaying impulse buys, and asking yourself whether a purchase still feels worth it after a few days. Time is often a great filter for emotional spending.

Start practicing with the money you already manage. If you get an allowance, gift money, or income from small jobs, try dividing it into categories: spending, saving, and future goals. Even a simple plan builds decision-making skills.

A small emergency fund can make a huge difference. If you save even $10 at a time, you begin creating a buffer. That buffer reduces the need to borrow when something unexpected happens.

Learn to read the fine print. Watch for words like interest rate, late fee, annual fee, introductory offer, and penalty. Some deals look cheap at first because the expensive part is hidden in the details.

Keep your commitments realistic. It is better to say no to a payment plan than to say yes and struggle for months. Financial stability grows when your choices leave space for change, emergencies, and goals.

Every money choice affects future choices. When you save, you create options. When you borrow wisely, you may solve a real problem. When you borrow carelessly, you reduce your future freedom.

You do not need to fear credit. You need to respect it. Used carefully, it can be a tool. Used carelessly, it can turn future income into repayment for past decisions.