Have you ever wanted something special and then realized it costs more than the money in your pocket? That happens to everyone. A new game, a book series, art supplies, or a gift for someone you love may cost more than you have right now. The exciting part is that math can help you make a plan. When you use money carefully, you are not just waiting for your goal to happen. You are building a path to it.

A personal financial goal is something you want to do with money. Your goal might be to save enough to buy a scooter helmet, a soccer ball, or a small science kit. A good goal is clear. Instead of saying, "I want more money," you can say, "I want to save $24 for a sketchbook set."

When a goal is clear, it becomes easier to plan. You can ask helpful questions such as: How much money do I need? How much do I already have? How much more do I need? How long will it take? These questions lead to arithmetic, and arithmetic helps turn wishing into planning.

Personal financial goal means a money target you want to reach. Savings means money you keep and do not spend right away. A plan is a set of steps you follow to reach the goal.

People use money plans in everyday life. Families save for trips, schools save for events, and children save for items they care about. Learning how to make a simple plan now is a smart life skill.

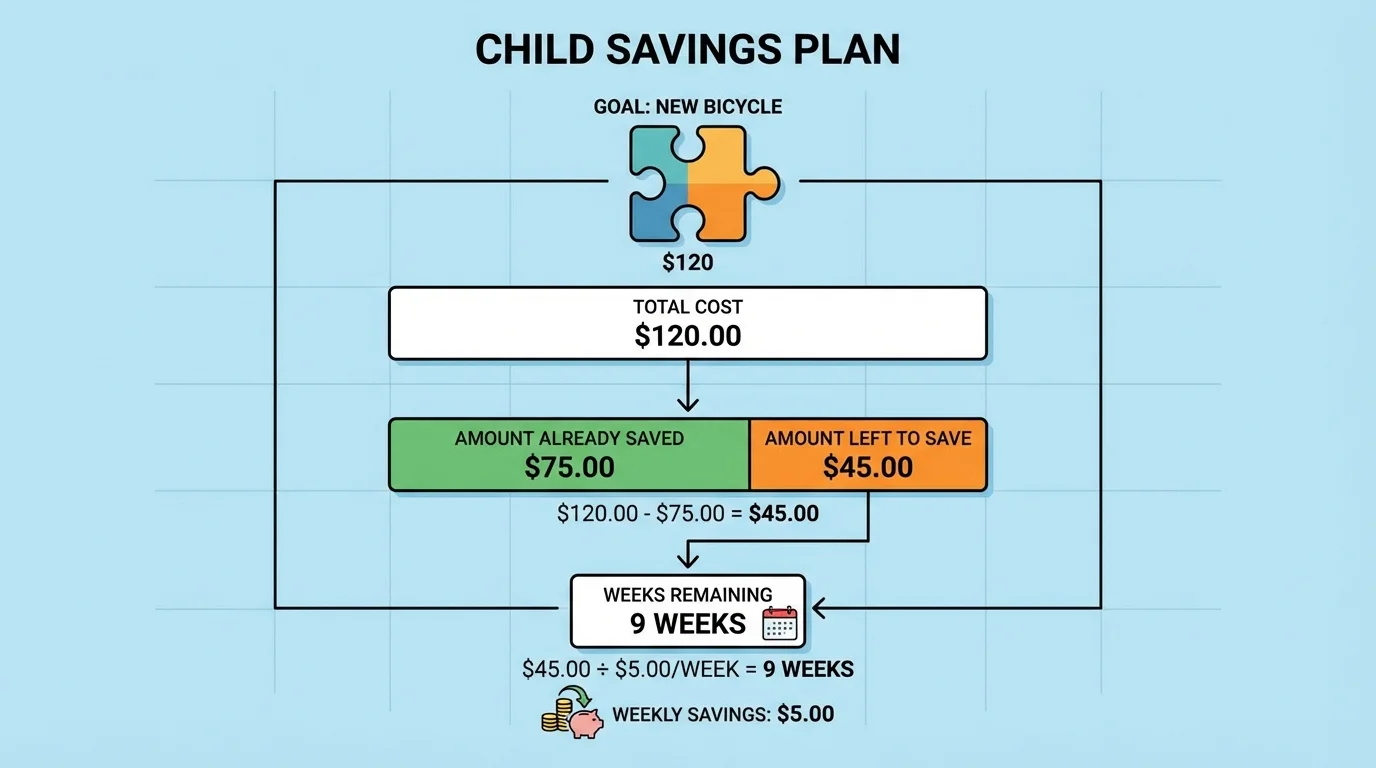

A financial goal has several parts, as [Figure 1] shows. First, there is the item or activity you want. Second, there is the total cost. Third, there is the amount you already have. Fourth, there is the amount still needed. Fifth, there is the time you have to save.

Suppose Maya wants a puzzle that costs $18. She already has $5. To find how much more she needs, she uses subtraction: \(18 - 5 = 13\). Maya still needs $13. Now she can make a plan for saving that $13.

If Maya wants the puzzle in \(13\) weeks, she can save $1 each week. If she wants it sooner, she may need to save more each week. This is why a goal is not only about the total money. It is also about time.

Some goals are short-term, like saving for a book in a few weeks. Some are longer-term, like saving for a bigger toy over several months. A shorter time often means saving a larger amount each week. A longer time often means saving a smaller amount each week.

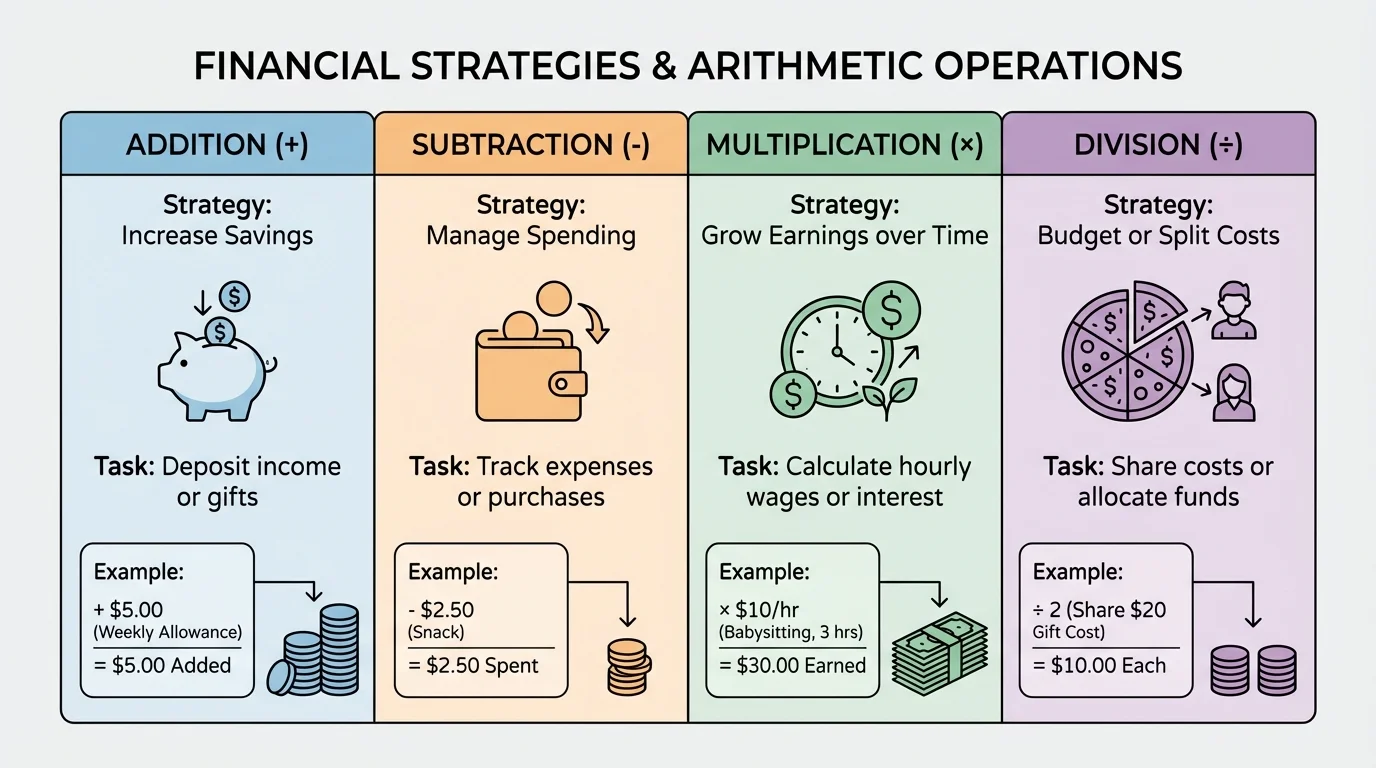

Each arithmetic operation helps answer a different money question, as [Figure 2] explains. You use addition to find how much money you have in all. You use subtraction to find how much money is left to save. You use multiplication when the same amount is saved again and again. You use division to split a total amount into equal weekly or daily parts.

Here are four useful questions and the operation that matches each one:

For example, if you save $2 one week and $3 the next week, addition gives \(2 + 3 = 5\). If your goal is $15 and you have $5, subtraction gives \(15 - 5 = 10\). If you save $4 each week for \(3\) weeks, multiplication gives \(4 \times 3 = 12\). If you need $12 in \(4\) weeks, division gives \(12 \div 4 = 3\).

You already know how to add, subtract, multiply, and divide whole numbers. In money problems, those same skills help you make smart choices. The difference is that now the numbers represent real savings goals.

Sometimes a plan uses more than one operation. You might subtract to find the amount left, then divide to find the weekly savings amount. Or you might multiply your weekly savings by the number of weeks, then add money you already had at the start.

One simple strategy is to save the same amount again and again. This works well when you get money on a regular schedule, such as each week. Because the amount repeats, multiplication is very helpful.

Suppose Jordan saves $3 each week. After \(4\) weeks, Jordan has saved \(3 \times 4 = 12\). After \(6\) weeks, Jordan has saved \(3 \times 6 = 18\). Repeated saving makes a pattern that is easy to track.

This strategy is useful because it is predictable. If you know your weekly savings amount, you can estimate how long your plan will take. As you saw earlier in [Figure 2], multiplication helps when equal amounts repeat.

Another strategy is to start with the money you already have. Then subtract that amount from the total cost. This tells you the missing amount.

Suppose Elena wants markers that cost $14, and she already has $6. The missing amount is \(14 - 6 = 8\). Now Elena knows she needs $8 more. If she saves $2 each week, she can check how long it will take: \(8 \div 2 = 4\). Elena can reach her goal in \(4\) weeks.

This kind of planning is helpful because many people do not start at zero. They may have birthday money, earnings from chores, or leftover money from another week.

Saving even small amounts can make a big difference over time. Four weeks of saving $2 each week gives \(2 \times 4 = 8\), and eight dollars may be enough to finish a goal that once seemed far away.

Starting with what you already have can make a goal feel closer and more possible.

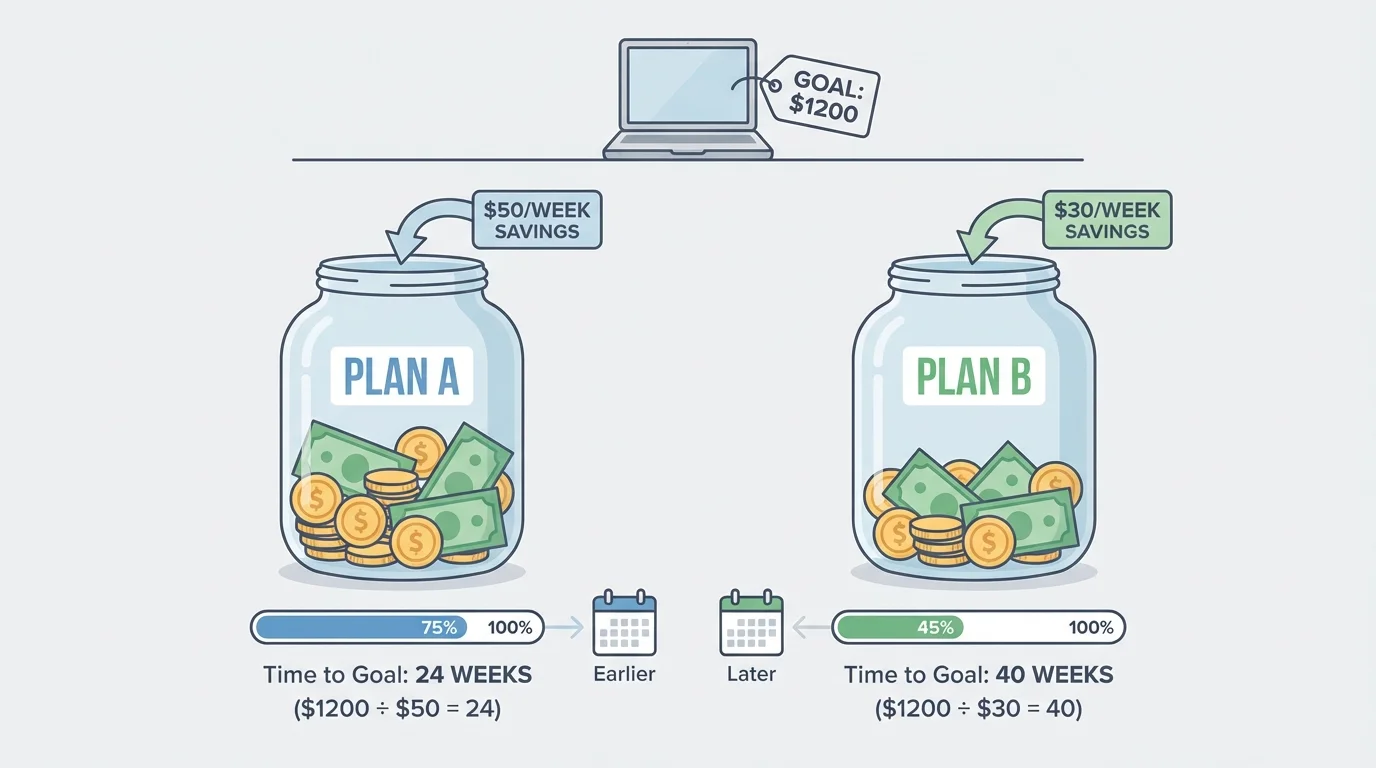

Sometimes there is more than one way to reach the same goal, and [Figure 3] compares this idea clearly. You can save a small amount for more weeks, or a larger amount for fewer weeks. Both plans may work, but one may fit your situation better.

Suppose a game costs $20. Plan A is to save $2 each week. Then the number of weeks is \(20 \div 2 = 10\). Plan B is to save $4 each week. Then the number of weeks is \(20 \div 4 = 5\). Both plans reach $20, but Plan B is faster.

Choosing the best plan depends on what is realistic. If saving $4 each week is too hard, then Plan A may be the better choice. A strong money plan is not just quick. It also needs to be manageable.

Comparing plans helps you become flexible. Later, if you earn extra money or need to spend some money, you can change your plan and still keep moving toward the same goal.

Now let's model several savings plans step by step.

Worked example 1

A notebook set costs $16. Amir has $7 already. How much more money does Amir need?

Step 1: Identify the total cost and the amount already saved.

Total cost: $16. Saved already: $7.

Step 2: Subtract to find the missing amount.

\(16 - 7 = 9\)

Step 3: State the answer clearly.

Amir needs $9 more.

Answer: \(9\) more dollars are needed.

This example uses subtraction because we know the total goal and part of the amount has already been saved.

Worked example 2

Lina wants a jump rope that costs $15. She plans to save $3 each week. How many weeks will it take?

Step 1: Write the total needed and the amount saved each week.

Total goal: $15. Weekly savings: $3.

Step 2: Divide the total by the weekly savings.

\(15 \div 3 = 5\)

Step 3: Explain the result.

Lina will need \(5\) weeks.

Answer: Lina reaches the goal in \(5\) weeks.

This example uses division because the total amount is being split into equal weekly savings parts.

Worked example 3

Noah saves $2 each week for \(6\) weeks and already has $1. Will he have enough money to buy a toy that costs $13?

Step 1: Find how much Noah saves over \(6\) weeks.

\(2 \times 6 = 12\)

Step 2: Add the money he already has.

\(12 + 1 = 13\)

Step 3: Compare with the cost of the toy.

The toy costs $13, and Noah will have $13.

Answer: Yes, Noah will have exactly enough money.

This example combines multiplication and addition. Many real money plans use more than one operation.

Worked example 4

Sofia wants an art pen set that costs $21. She has $9. She wants to buy it in \(4\) weeks. How much should she save each week?

Step 1: Find the amount still needed.

\(21 - 9 = 12\)

Step 2: Divide by the number of weeks.

\(12 \div 4 = 3\)

Step 3: State the plan.

Sofia should save $3 each week.

Answer: Weekly savings should be \(3\) dollars.

Notice that this example first finds the missing amount and then finds the equal weekly savings amount. That is a common two-step strategy in personal financial planning.

A table can help you compare savings goals quickly. It organizes the total cost, money already saved, amount still needed, and possible weekly savings plans.

| Goal | Total Cost | Saved Now | Still Needed | Weekly Savings | Weeks Needed |

|---|---|---|---|---|---|

| Book | $12 | $4 | \(12 - 4 = 8\) | $2 | \(8 \div 2 = 4\) |

| Ball | $18 | $6 | \(18 - 6 = 12\) | $3 | \(12 \div 3 = 4\) |

| Craft kit | $20 | $8 | \(20 - 8 = 12\) | $4 | \(12 \div 4 = 3\) |

| Puzzle | $15 | $3 | \(15 - 3 = 12\) | $2 | \(12 \div 2 = 6\) |

Table 1. A comparison of different savings goals, the amount already saved, the amount still needed, and the number of weeks required.

Tables make patterns easier to see. For example, the ball and the book both take \(4\) weeks in the plans shown, even though the total costs are different. That happens because the weekly savings amounts are also different.

Good plans need good habits. One important habit is keeping track of your budget. A budget is a simple plan for how money will be used. For a third grader, that may mean deciding how much to save, how much to spend, and how much to keep for later.

Another habit is telling the difference between a need and a want. A need is something important, like school supplies. A want is something you would like to have, like a new toy. When you are working toward a goal, choosing not to spend on small wants can help your savings grow.

Why tracking progress works

When you check your savings often, you can see how close you are to your goal. This helps you stay motivated and make changes early if needed. If your plan says you should have $10 after \(5\) weeks, and you only have $8, you know right away that you need to adjust your savings.

Writing your progress down can help too. You might record that after week \(1\), you saved $2; after week \(2\), you saved another $2, so the total is \(2 + 2 = 4\). A running total shows growth over time.

Sometimes life changes your plan. Maybe you get extra money as a gift. Maybe you spend part of your savings on something important. Math helps you adjust without giving up.

Suppose your goal is $25. You had saved $10, and then you received $5 more. Now your total saved is \(10 + 5 = 15\). The new amount left is \(25 - 15 = 10\). If you save $2 each week after that, you need \(10 \div 2 = 5\) more weeks.

Or suppose you had $14 saved for a $20 goal, but then spent $3. Your new savings amount is \(14 - 3 = 11\). Now the amount left is \(20 - 11 = 9\). If you save $3 each week, you need \(9 \div 3 = 3\) more weeks. The goal is still possible. The plan simply changes.

Being flexible is one reason comparing choices matters, just as [Figure 3] shows with different ways to reach the same total. A plan is useful because it can be updated when your money changes.

"A goal without a plan is just a wish."

— Common saying

Money planning is really about making choices with numbers. When you know the total cost, the amount you have, and the time you want to reach the goal, arithmetic gives you powerful tools. Addition shows what you have in all. Subtraction shows what is left. Multiplication shows repeated saving. Division shows equal parts over time.

As you continue learning, you will see that these same operations help with many real-world decisions. They help people save, compare options, and solve problems in smart ways. The best part is that even simple arithmetic can help you reach something meaningful to you.