A jobs report, one inflation number, or one interest-rate decision can move billions of dollars in a single afternoon. That may sound dramatic, but it reveals something important: financial markets are always trying to answer one question—what is likely to happen next? Prices rise and fall not only because of what is happening now, but because investors are constantly guessing how businesses, consumers, and governments will behave in the future.

A financial market is a place where people and institutions buy and sell financial assets such as stocks, bonds, currencies, and commodities. A stock gives partial ownership in a company. A bond is a loan made to a government or corporation. These assets have prices, and those prices change when buyers and sellers disagree about value, risk, and future profits.

Investors react to several big forces at once: overall economic conditions, interest rates, government policy, company performance, and new information. If investors expect stronger profits, they may bid stock prices higher. If they fear a recession, they may sell risky assets and move money into safer ones. In finance, expectations matter just as much as current facts.

One useful way to think about market reactions is by using a basic return formula. If an investment starts at price \(P_1\) and ends at price \(P_2\), then its price return is

\[\textrm{Return} = \frac{P_2 - P_1}{P_1}\]

If a stock rises from $50 to $55, then the return is \(\dfrac{55 - 50}{50} = \dfrac{5}{50} = 0.10\), or \(10\%\). Markets move because investors keep changing their estimates of what \(P_2\) should be in the future.

Market reaction is the change in prices, trading volume, or investor behavior after a shift in economic conditions, policy, or information. Risk is the chance that an investment's actual return will differ from what an investor expected, including the possibility of losing money.

Some reactions are immediate and emotional, while others develop more slowly. A surprise war, banking crisis, or natural disaster can trigger sudden selling. A long period of rising wages and steady consumer spending may support stock prices over many months. This is why understanding the business cycle is so important.

[Figure 1] The business cycle is the recurring pattern of economic expansion and slowdown through different stages. Economies do not grow in a perfectly straight line. Instead, they move through periods of stronger output and hiring, then periods of weaker spending and production.

The main phases are expansion, peak, contraction, and trough. During an expansion, production rises, employment improves, and consumers spend more. At a peak, growth is still high but may begin to overheat. During contraction, spending and business activity slow down. If the decline is deep and lasts long enough, the economy may enter a recession. A trough is the low point before recovery begins.

Different assets often react differently during each phase. In an expansion, company sales and profits often improve, so stock prices may rise. During contraction or recession, investors may fear weaker profits, causing stock prices to fall. Bonds can become more attractive in downturns because many investors want steadier income and lower risk.

This pattern is not guaranteed. Markets sometimes begin rising before the economy fully recovers because investors expect better conditions ahead. In other words, markets are forward-looking. If investors believe a recession is almost over, stock prices may climb even while unemployment is still high.

Commodities also react to the cycle. Oil and industrial metals often rise when factories are busy and transportation demand is strong. During slower periods, demand may drop, which can push prices lower. Cash becomes more appealing when investors want safety or expect better buying opportunities later.

Why markets often move before the economy does

Market prices are based on expectations about future earnings, inflation, and interest rates. Because investors try to predict what comes next, stock indexes may fall before a recession officially starts and may recover before the recession officially ends.

A simple example makes this clearer. Suppose investors expect a company to earn $10 million next year. If recession fears reduce that estimate to $7 million, the company's stock may fall today, even though the earnings decline has not happened yet. Expectations change prices before the full economic effects appear.

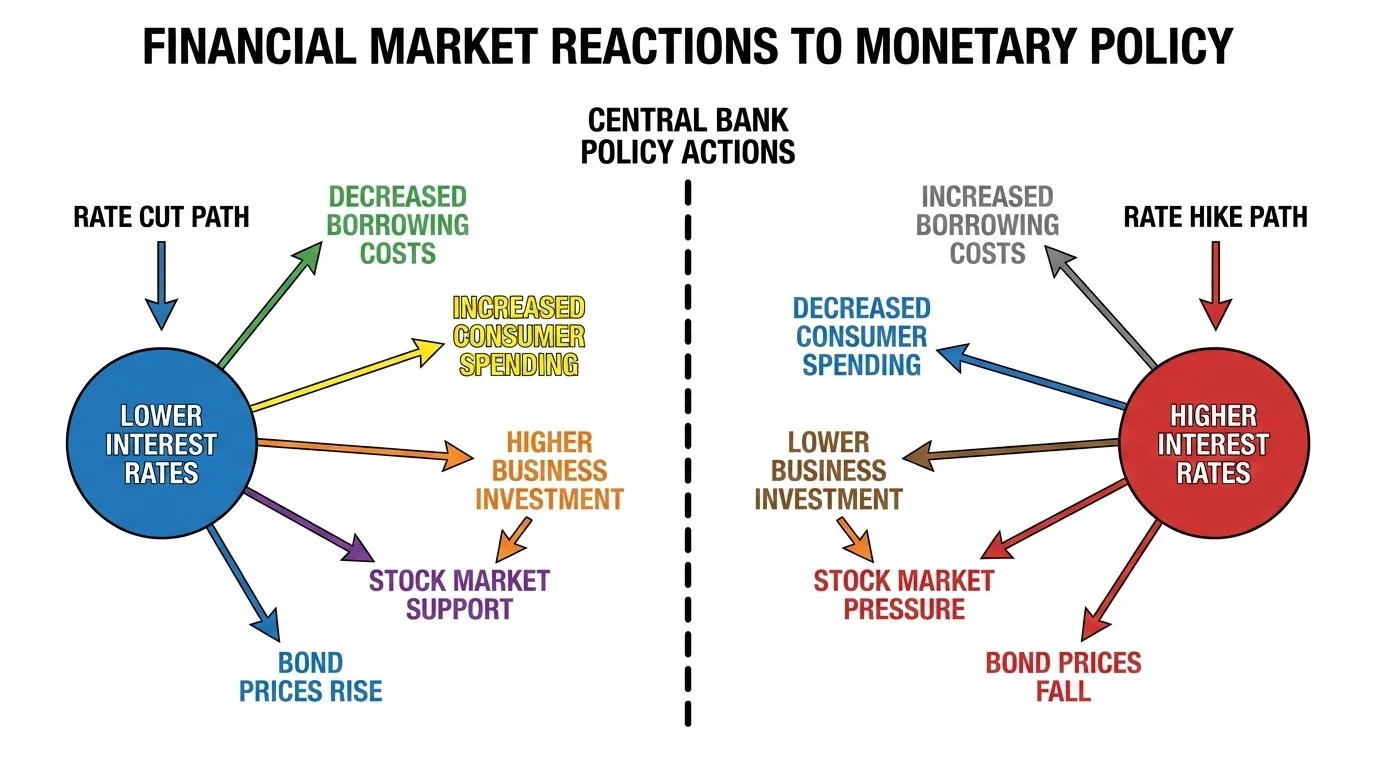

[Figure 2] Monetary policy influences borrowing, spending, saving, and investing across the economy. In the United States, the Federal Reserve is the central bank that helps manage inflation and employment partly by influencing interest rates.

When the central bank lowers interest rates, borrowing becomes cheaper. Consumers may take more car loans or mortgages, and businesses may borrow more to expand. Lower rates can support stock prices because cheaper borrowing can raise profits and because investors may move money out of low-yield savings and into stocks.

When the central bank raises rates, the opposite pressure often appears. Loans become more expensive, which can slow consumer spending and business investment. Higher rates may reduce stock prices, especially for fast-growing companies whose expected profits are far in the future. Investors may also find newly issued bonds more attractive because they offer higher yields.

Bond prices and interest rates usually move in opposite directions. If existing bonds pay a lower fixed rate than new bonds, investors will pay less for the old bonds. This inverse relationship is one of the most important ideas in finance:

\[\textrm{Bond prices} \uparrow \Rightarrow \textrm{yields} \downarrow, \qquad \textrm{Bond prices} \downarrow \Rightarrow \textrm{yields} \uparrow\]

For example, imagine a bond paying $30 each year on a face value of $1,000. If market interest rates are about \(3\%\), that bond is attractive. But if new bonds begin paying \(5\%\), investors will demand a lower price for the old bond. Markets react quickly because investors compare all available returns.

Monetary policy also affects inflation. If inflation is high, the central bank may raise rates to cool spending. That can hurt some stock sectors in the short run, but investors may welcome it if they believe inflation will finally come under control. Later, when inflation starts falling, markets may rise because investors expect future rate cuts. One policy tool influences households, firms, bonds, and stocks through connected channels.

Numerical example: how a rate change affects a simple investment choice

An investor is choosing between a savings account and a stock. The savings account interest rate rises from \(2\%\) to \(4\%\). The stock is expected to return \(6\%\), but with much higher risk.

Step 1: Compare the gap in expected return.

Before the rate increase, the gap is \(6\% - 2\% = 4\%\).

Step 2: Recalculate after the rate increase.

After the rate increase, the gap is \(6\% - 4\% = 2\%\).

Step 3: Interpret the market effect.

The extra reward for taking stock-market risk shrinks from \(4\%\) to \(2\%\). Some investors may shift money away from stocks and toward safer savings or bonds.

This helps explain why rising rates can put pressure on stock prices.

Exchange rates can react too. Higher interest rates in one country may attract foreign investors seeking better returns, which can strengthen that country's currency. A stronger currency can make imported goods cheaper but can make exports more expensive for foreign buyers. That, in turn, affects company profits and stock prices.

Fiscal policy refers to government decisions about spending and taxation. Unlike monetary policy, which is mainly handled by a central bank, fiscal policy is shaped by elected leaders and legislatures. It can boost or slow economic activity, and markets pay close attention to those choices.

If the government increases spending on roads, energy systems, or defense, companies in those industries may gain contracts and revenue. Their stock prices may rise because investors expect stronger future profits. If the government cuts taxes, households may have more disposable income to spend, and businesses may keep more of their earnings.

On the other hand, lower taxes or higher spending can increase the budget deficit if the government spends more than it collects in revenue. Investors may worry that higher government borrowing will push interest rates up over time. If they expect more inflation or heavier debt burdens, some asset prices may fall even while the economy gets a short-term boost.

Fiscal policy can also target specific groups. Subsidies for clean energy may help solar or battery companies. New taxes on tobacco, imports, or corporate profits may reduce expected earnings in certain industries. Markets are not reacting only to whether policy is "good" or "bad"; they are reacting to who gains, who loses, and what the long-term effects might be.

| Policy action | Possible short-term market reaction | Possible longer-term concern |

|---|---|---|

| Higher government spending | Boost to sectors receiving contracts | Higher deficits or inflation |

| Tax cuts for households | More consumer spending | More government borrowing |

| Corporate tax increase | Pressure on profits and stock prices | Could fund public investment |

| Reduced public spending | Slower growth in affected sectors | Lower deficits |

Table 1. Examples of how different fiscal policy actions can influence markets in the short term and long term.

Markets sometimes react positively to a tax increase or a spending cut if investors believe it will reduce inflation or make government finances more stable. A policy that seems negative at first glance can still raise asset prices if expectations improve.

That is why market reaction depends on context. The same policy can produce different results in different times. A large spending program during a recession may help growth, but the same program during a period of already high inflation may worry investors.

Every trading day, markets absorb an enormous amount of new information: company earnings, unemployment data, inflation reports, technological breakthroughs, weather shocks, elections, and international conflict. A market expectation is what investors as a group already think is likely to happen. Prices often react most strongly when reality differs from that expectation.

For example, suppose analysts expect inflation to be \(3.0\%\), but the actual report shows \(3.8\%\). Even if \(3.8\%\) sounds only slightly higher, markets may react sharply because that surprise suggests higher interest rates may continue. In contrast, if inflation comes in exactly as expected, the market may barely move because the news was already "priced in."

The same principle applies to company earnings. A company can report large profits and still see its stock fall if investors expected even more. Another company can report a small loss and see its stock rise if the loss is smaller than feared. Markets compare actual outcomes with prior expectations, not with emotions or headlines alone.

Case study: reacting to an earnings surprise

A company's stock trades at $80. Investors expected earnings per share of \(2.50\), but the company reports \(3.10\).

Step 1: Measure the earnings surprise.

The difference is \(3.10 - 2.50 = 0.60\).

Step 2: Find the percentage surprise.

\[\frac{0.60}{2.50} = 0.24 = 24\%\]

Step 3: Interpret the result.

A positive surprise of \(24\%\) may lead investors to expect stronger future profits, which can push the stock price higher.

The size of the reaction still depends on whether investors believe the strong result will continue.

Information spreads quickly because of technology. Professional investors use data feeds and algorithms that react in fractions of a second. Individual investors can see price changes on a phone. Speed makes markets efficient in some ways, but it also means rumors and fear can spread fast. Short-term volatility does not always reflect long-term value.

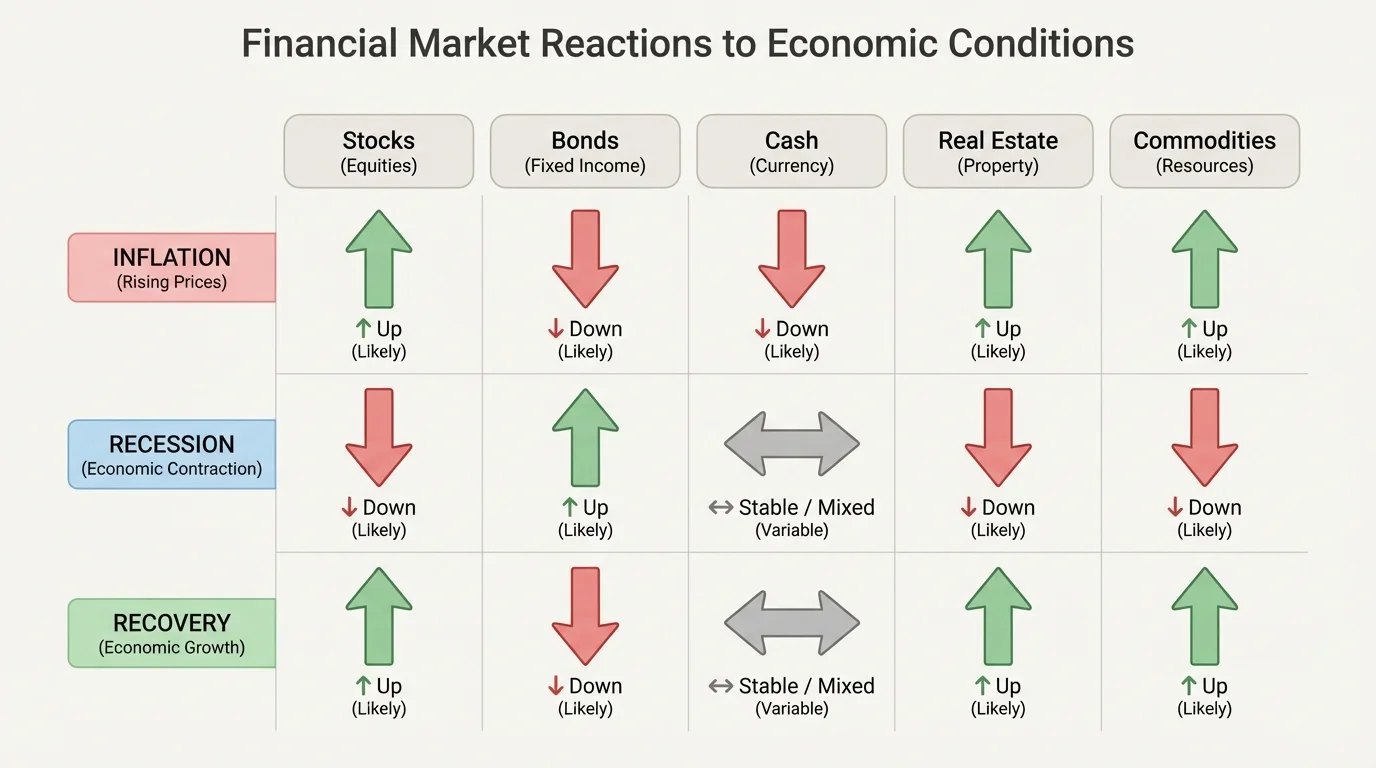

[Figure 3] No single asset performs best in every environment. That is one reason diversification matters. A diversification strategy means spreading money across different types of investments instead of betting everything on one company, one industry, or one asset class.

Stocks usually offer higher long-term growth potential, but they can be volatile. Bonds often provide income and may hold value better during economic stress. Cash is stable but usually grows slowly. Real estate can benefit from rent income and property appreciation, though it can be hurt by high interest rates. Commodities, such as oil or gold, may react strongly to inflation, war, or supply disruptions.

Because assets react differently, combining them can reduce overall risk. If one investment falls, another may stay stable or rise. Diversification does not eliminate losses, but it can make an investment plan more resilient. This helps explain why investors with long-term goals usually avoid putting all their money into a single asset.

Consider a simple portfolio with \(60\%\) in stocks and \(40\%\) in bonds. If stocks fall by \(10\%\) and bonds rise by \(3\%\), the portfolio return is

\[0.60(-10\%) + 0.40(3\%) = -6\% + 1.2\% = -4.8\%\]

The portfolio still loses value, but less than an all-stock portfolio would. This is the practical logic behind diversification.

Worked example: comparing a concentrated investment with a diversified one

Student A puts all savings into one technology stock. Student B spreads savings across a stock fund, a bond fund, and cash.

Step 1: Assume the technology stock falls by \(25\%\).

Student A's investment return is simply \(-25\%\).

Step 2: Assume Student B holds \(50\%\) in a stock fund, \(30\%\) in a bond fund, and \(20\%\) in cash.

If the stock fund falls by \(12\%\), the bond fund rises by \(4\%\), and cash earns \(1\%\), then the portfolio return is \(0.50(-12\%) + 0.30(4\%) + 0.20(1\%)\).

Step 3: Calculate the result.

\[ -6\% + 1.2\% + 0.2\% = -4.6\% \]

Student B still loses money, but the loss is far smaller because the portfolio is diversified.

Understanding market reactions is not just for economists or traders. It matters for personal financial decisions. A student saving for college in \(2\) years should not invest exactly like someone saving for retirement in \(40\) years. Time horizon, goals, and risk tolerance shape what kind of investment strategy makes sense.

Suppose one person needs money soon for tuition. Because short-term market drops can be damaging, that student might keep more money in cash, certificates of deposit, or short-term bonds. Another student saving for retirement may accept more stock-market risk because there is time to recover from downturns and benefit from long-term growth.

Investors also need to match market knowledge with self-knowledge. If a person panics and sells every time markets drop \(5\%\), that person may need a more conservative portfolio. A diversified strategy should be compatible with personal goals, not based on hype, fear, or trends on social media.

Earlier financial literacy topics about saving, budgeting, and goal-setting still matter here. Investing comes after understanding how much money you can commit, when you will need it, and how much uncertainty you can handle without making impulsive decisions.

A smart investor asks practical questions: What is my goal? When will I need the money? How much loss could I handle emotionally and financially? Am I diversified across asset types? These questions matter more than trying to predict every market headline.

It is easy to oversimplify market reactions. Students often hear statements like "stocks fell because of inflation" or "bonds rose because the government passed a bill." Sometimes those statements are partly true, but markets usually react to many forces at once. Prices reflect a mix of current facts, forecasts, fears, and competing interpretations.

Another mistake is assuming that one day's market move proves a long-term trend. Markets can overreact in the short run. A company's stock may drop after disappointing news and recover later if the business remains strong. A rally may fade if investor optimism was excessive.

That is why long-term investing usually focuses on discipline rather than prediction. Diversification, regular contributions, and patience can matter more than guessing the next rate move or news headline. Financial markets are important signals, but they are not crystal balls.

"The stock market is a device for transferring money from the impatient to the patient."

— Warren Buffett

Seen this way, market reactions become easier to understand. Economic conditions shape profits and risk. Monetary policy changes borrowing costs and interest rates. Fiscal policy changes spending, taxes, and government borrowing. New information changes expectations. Different assets respond in different ways, which is exactly why diversified investing is so valuable for personal financial goals.