A single event can change a person's finances in minutes: a phone gets stolen, a driver causes a crash, a worker gets injured and misses weeks of pay, or someone opens a credit card account using stolen personal information. What makes personal finance challenging is not just earning money, but protecting it. Strong financial decision-making includes preparing for problems before they happen.

In personal finance, risk means the chance that an event will cause financial loss. Some losses are small, like replacing a broken pair of headphones. Others can be severe, such as hospital bills, a house fire, or months without income after an injury. Consumers cannot eliminate all uncertainty, but they can choose strategies to manage it.

Many financial risks fall into a few major categories. A person may face loss of income from unemployment, illness, disability, or death of a wage earner. They may face loss or damage to property such as a car, laptop, apartment, or home. They may face health-related costs from accidents, chronic illness, or emergency treatment. They may also face fraud, especially identity theft, where someone steals personal information to open accounts, make purchases, or access money.

Financial risk is the possibility that an event or decision will lead to money loss or extra expense. Risk management is the process of deciding how to deal with that possibility before the loss occurs.

Good risk management is not about being afraid of everything. It is about matching the right strategy to the size and likelihood of a loss. A rational consumer asks two key questions: How likely is the loss? and How damaging would it be if it happened? A scratched backpack and a totaled car do not deserve the same response.

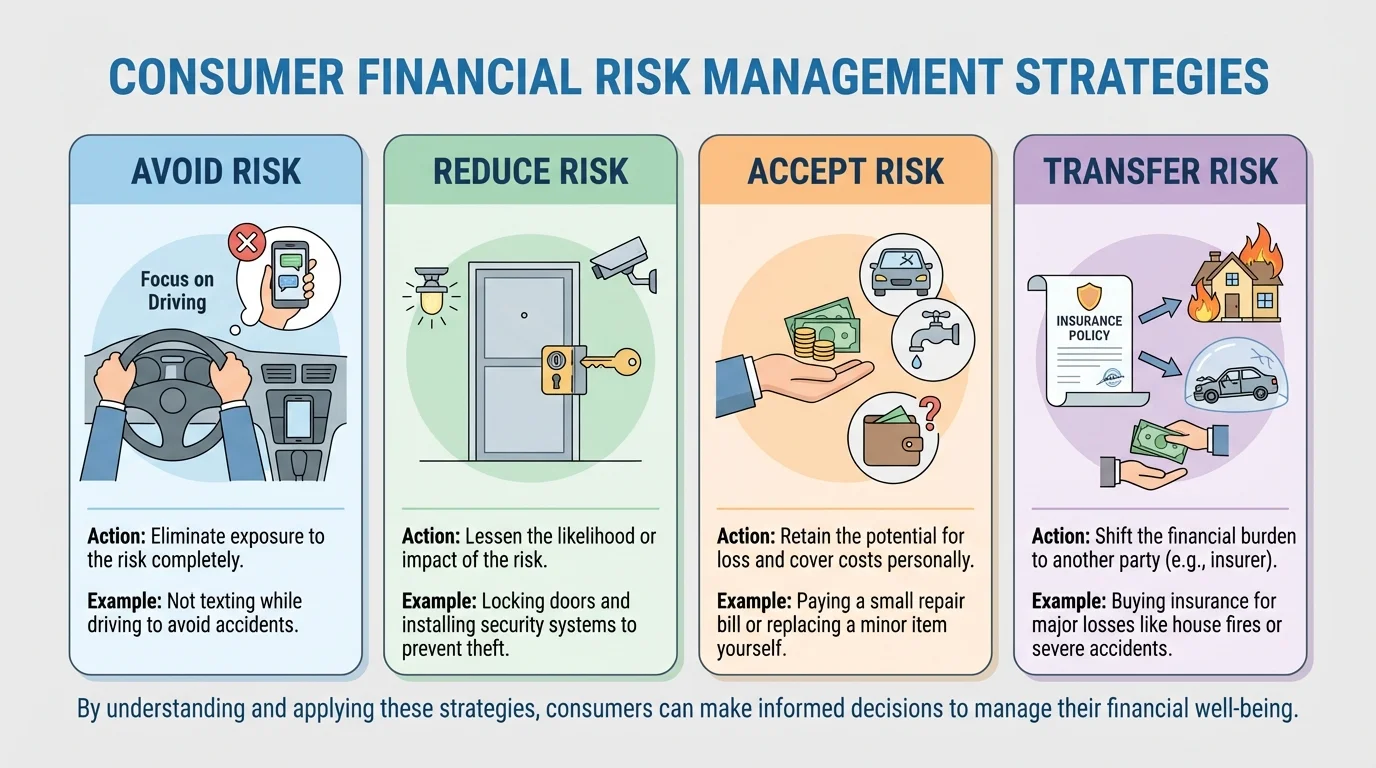

Consumers usually respond to financial risk in four basic ways, as shown in [Figure 1]: they can avoid the risk, reduce the risk, accept the risk, or transfer the risk to another party through insurance or another agreement. These strategies are not identical, and good decisions often combine more than one.

To avoid risk means choosing not to do something that creates danger. To reduce risk means lowering either the chance of a loss or the size of the loss. To accept risk means deciding to pay for a possible loss yourself if it occurs. To transfer risk means shifting much of the financial burden to an insurer in exchange for a cost.

These four responses are easiest to understand through examples. A student may avoid the risk of overdraft fees by not using a debit card without checking the account balance. That same student may reduce the risk of identity fraud by using strong passwords and two-factor authentication. They may accept the risk of replacing a cheap pair of earbuds on their own. They may transfer the risk of major car accident costs by buying auto insurance.

Avoiding risk is the most complete form of protection because it removes exposure to a particular danger. If you never post your banking password online, you avoid that specific chance of theft. If you never drive without a license or insurance, you avoid legal and financial consequences tied to that decision.

Consumers avoid risk when they refuse suspicious job offers, avoid high-interest payday loans, decline to share personal information with unknown callers, or choose not to drive after drinking. They also avoid financial risk when they read contracts before signing and walk away from deals that seem unclear or dishonest. Avoiding risk often requires patience and self-control because the risky choice may seem faster, more exciting, or more convenient.

However, not every risk can or should be avoided. If a person avoided all risk, they might never drive, rent an apartment, apply for college, use online banking, or take a job. The challenge is deciding which risks are unnecessary and which are part of normal life. Avoiding obvious, preventable risks is wise; avoiding every possible uncertainty is unrealistic.

Many successful financial decisions feel boring in the moment. Ignoring a scam text, reading the fine print, or refusing an impulsive purchase rarely feels dramatic, but these actions can prevent losses that take months to repair.

Avoidance works best when the risk is both unnecessary and potentially harmful. For example, if a website asks for a Social Security number even though the service does not require one, leaving the site is a smart form of risk avoidance. There is little reward and significant danger.

Reducing risk means taking steps that make a loss less likely or less severe. This is one of the most common strategies because many daily risks cannot be removed completely. You may need to drive, use the internet, or live in a place where storms are possible. In those cases, reducing risk is practical.

Consumers reduce property risk by locking doors, installing smoke detectors, maintaining cars, using surge protectors, and storing valuable documents safely. They reduce health-related financial risk by exercising, wearing seat belts, getting preventive care, and following safety rules at work or in sports. They reduce income risk by building job skills, maintaining savings, and having an emergency fund.

An emergency fund is one of the strongest examples of reducing risk. If a person has their hours reduced at work or faces an unexpected car repair, savings can prevent the problem from turning into debt. A common recommendation is to save several months of essential expenses, though the exact amount depends on the person's situation.

Consumers also reduce digital risk by freezing credit when necessary, checking bank statements, shredding sensitive documents, updating software, and using strong passwords. These habits do not make fraud impossible, but they lower the chance that thieves will succeed or go undetected for long.

Reducing probability versus reducing impact

Some actions lower the chance of a loss, while others lower the size of the loss if it occurs. Installing a home security system lowers the probability of burglary. Keeping copies of important records and maintaining savings lowers the impact if a burglary or other emergency still happens. Effective risk management often uses both kinds of protection.

Reducing risk also includes understanding costs. Suppose a driver can spend $300 per year on safer tires that lower the chance of an accident and also reduce wear. Even if no crash occurs, the purchase may still be worthwhile because the smaller cost helps prevent a potentially much larger loss. Risk reduction often means paying a smaller amount now to avoid a larger amount later.

As the comparison in [Figure 1] shows, reducing risk differs from avoiding it. Locking a bike reduces the chance of theft, but not riding the bike in a high-crime area at all would be avoidance. Both may be sensible depending on the situation.

Accepting risk does not mean being careless. It means recognizing that some losses are small enough that paying for them yourself makes more sense than buying protection. People do this all the time, often without noticing it. Many consumers do not insure inexpensive items such as a low-cost phone case, school supplies, or small kitchen tools.

This approach is sometimes described as choosing to self-insure against minor losses. Instead of paying regular premiums for every small problem, the consumer keeps enough savings to cover manageable costs. If replacing a $20 item would not seriously damage a budget, accepting that risk may be reasonable.

Still, accepted risk should be chosen carefully. A person who says, "I'll just pay for it myself," needs to be sure the possible loss really is affordable. Accepting the risk of a chipped phone screen is very different from accepting the risk of a major surgery bill or a lawsuit after a car crash. One is inconvenient; the other can cause long-term financial harm.

Consumers should think about frequency and severity. Small losses that happen rarely may be fine to accept. Large losses, even if unlikely, are often too dangerous to leave unprotected. That is why people often accept the risk of buying school supplies out of pocket but transfer the risk of a house fire through insurance.

Case study: Accept or insure?

Jordan owns a bike worth $150 and is offered a special insurance plan for $12 per month.

Step 1: Find the yearly cost of insurance.

The premium would be $12 each month, so the annual cost is $144.

Step 2: Compare the annual cost to the value of the item.

Paying $144 each year to protect a bike worth $150 is almost the same as buying a replacement bike.

Step 3: Evaluate the better strategy.

If Jordan can afford to replace the bike, accepting the risk and saving money may be more sensible than buying the policy.

This does not mean insurance is bad. It means the size of the possible loss matters.

Accepting risk becomes dangerous when consumers underestimate costs, overestimate their savings, or ignore low-probability but catastrophic events. Wise acceptance requires honest budgeting, not wishful thinking.

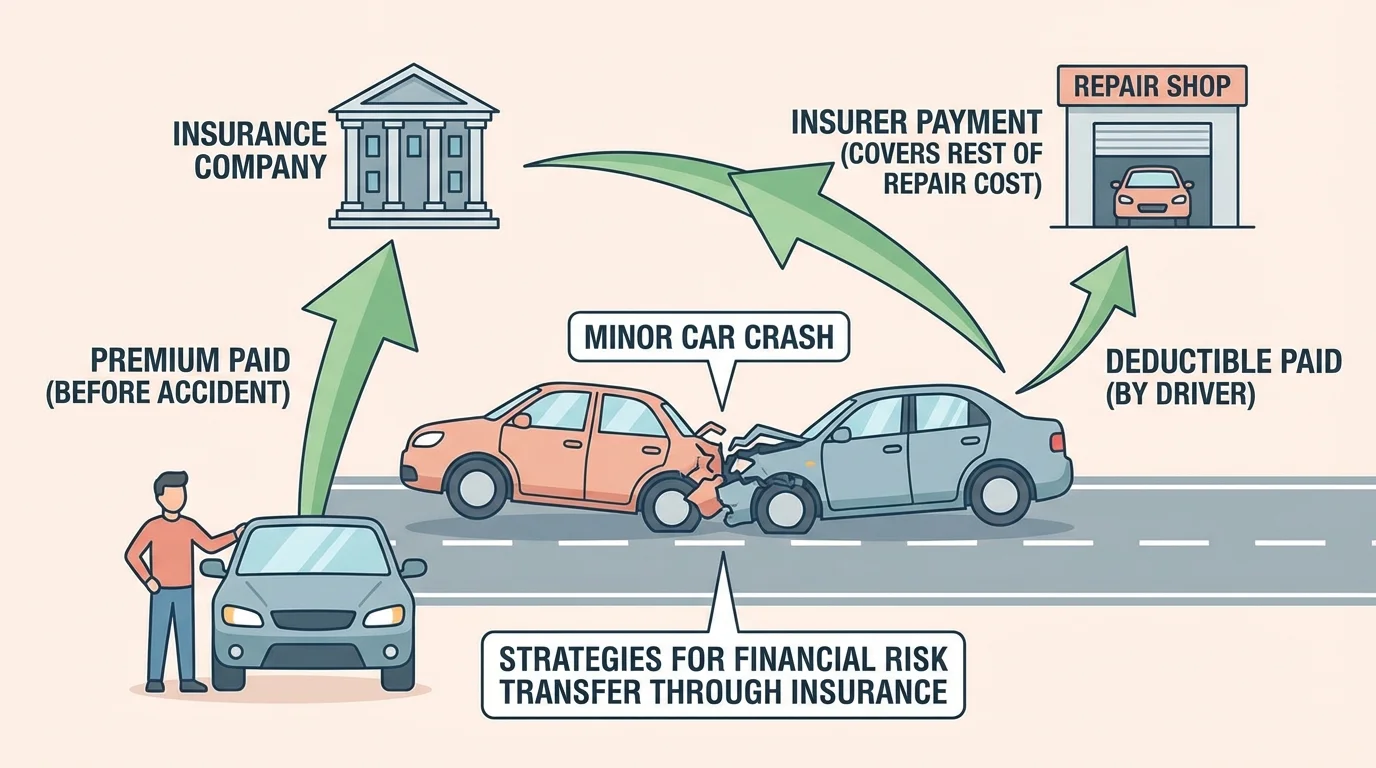

Insurance is one of the most powerful tools in personal finance because it transfers much of the financial cost of a covered loss from the consumer to an insurance company. The danger itself does not disappear. Cars can still crash and people can still get sick. What changes is who pays most of the bill after the event.

When someone buys insurance, they pay a premium, which is the amount paid for coverage. Many policies also include a deductible, which is the amount the policyholder must pay before the insurer pays the covered remainder. Policies also have coverage limits, which are maximum amounts the insurer will pay, and exclusions, which are situations the policy does not cover.

Suppose a driver has collision insurance with a $500 deductible and causes covered damage of $3,000 to their own car. The driver pays the first $500, and the insurer pays the remaining $2,500. In a simple form, the insurer payment is the covered loss minus the deductible: \(3{,}000 - 500 = 2{,}500\). This sharing of cost is one reason insurance works best for large losses rather than tiny expenses.

As [Figure 2] illustrates, different types of insurance protect against different risks. Health insurance helps pay medical costs. Auto insurance protects against losses from car accidents and may be required by law. Renters insurance and homeowners insurance protect personal property and housing-related losses. Disability insurance helps replace income if a person cannot work because of illness or injury. Life insurance supports dependents after a wage earner dies.

Insurance is especially important for losses that are unlikely but financially devastating. Most teenagers cannot pay a $50,000 hospital bill or a major liability claim from savings. Paying smaller premiums over time can protect against losses far beyond what most households could handle alone.

Not all insurance policies are equally useful. Some offer strong protection against major risk, while others mainly cover small inconveniences at high cost. Consumers should look closely at monthly premium cost, deductible amount, exclusions, reimbursement rules, and whether the policy duplicates protection they already have.

| Type of risk | Possible strategy | Why it may fit |

|---|---|---|

| Minor phone accessory breaks | Accept | The loss is small and often affordable out of pocket. |

| House fire | Transfer | The loss can be extremely large and difficult to pay without insurance. |

| Identity fraud | Avoid and reduce | Safe digital habits can prevent or limit damage. |

| Job interruption | Reduce and transfer | Savings reduce short-term pressure; disability or other coverage may help in some cases. |

Table 1. Examples of how different risks often match different management strategies.

Later, when weighing choices in [Figure 2], it becomes clear that insurance is not "free money." Consumers pay for protection ahead of time through premiums, and they still may share costs through deductibles and uncovered losses. The value of insurance comes from protection against losses that would otherwise be overwhelming.

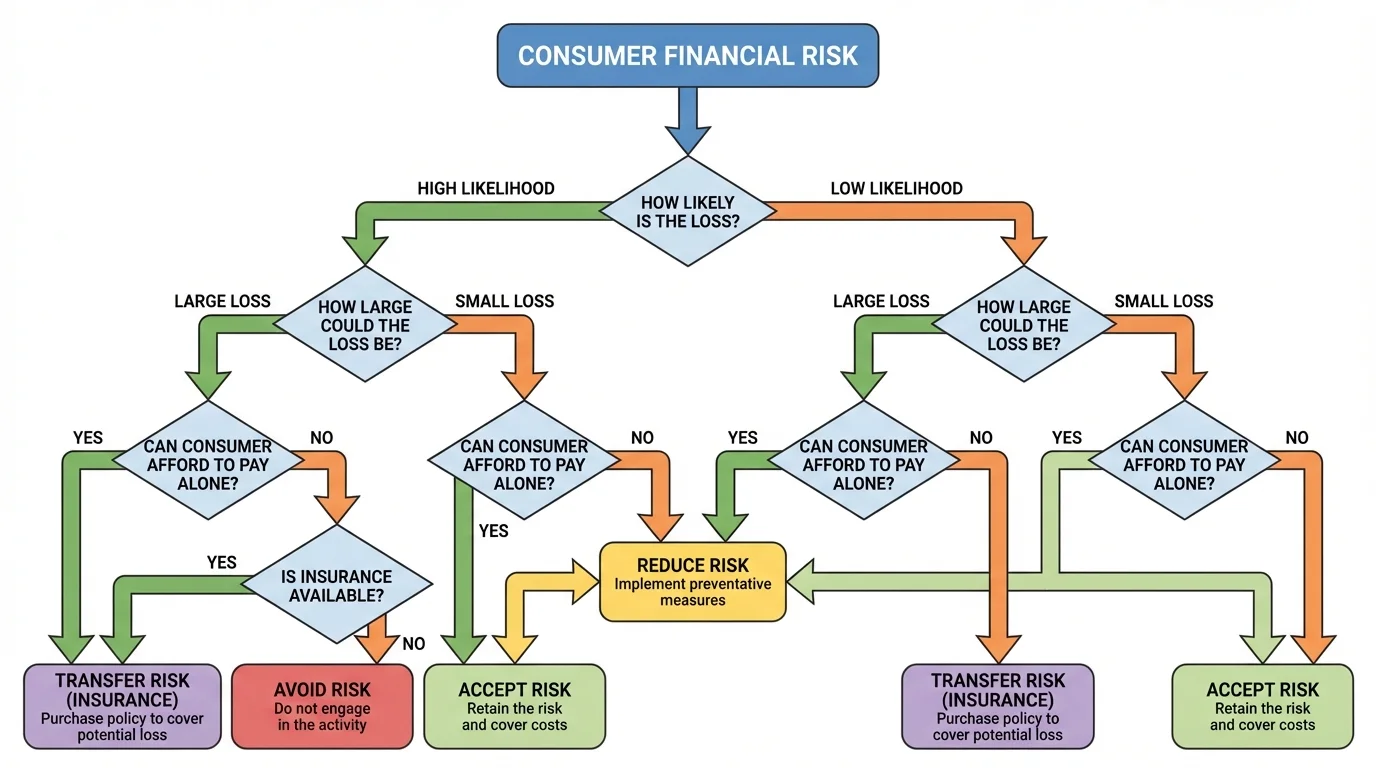

As [Figure 3] shows, consumers can evaluate risk systematically by following a useful decision process. First, estimate how likely the event is. Second, estimate how expensive the loss would be. Third, ask whether the loss would seriously harm your finances if you had to pay it yourself. Fourth, compare the cost of protection to the benefit of that protection.

If the activity is unnecessary and the risk is significant, avoidance may be best. If the risk is part of everyday life but can be lowered, reduction is often appropriate. If the loss is small and manageable, acceptance may work. If the loss could be catastrophic, transferring it through insurance is often the smartest choice.

Consider three situations. First, a student is tempted to click a link in a suspicious email claiming they won a prize. The best strategy is avoidance: do not click. Second, a family uses smoke alarms, keeps savings, and locks doors. That is reduction. Third, a renter chooses insurance for belongings because replacing everything after a fire would be impossible from current savings. That is transfer. In each case, the strategy matches the level and type of risk.

Sometimes consumers combine strategies. A driver transfers risk with auto insurance, reduces risk by driving carefully, and avoids risk by never driving under the influence. If the deductible is small enough to handle, they may also accept a limited part of the loss. Real financial decisions are often layered rather than single-choice.

Opportunity cost still matters in risk management. Money spent on premiums, security devices, or emergency savings cannot be spent elsewhere, so consumers must weigh whether the protection is worth that tradeoff.

The decision flow in [Figure 3] also helps explain why two people may make different choices. A high-income adult with large savings may accept a loss that would be impossible for another household to cover. Personal circumstances affect what counts as affordable risk.

Smart consumers read policy details carefully. They compare deductibles, exclusions, copays, claim procedures, and total yearly costs, not just the monthly premium. A policy with a low premium but very high deductible may leave a consumer underprotected when a loss occurs.

They also watch for warning signs of fraud. Insurance scams, fake warranties, and identity protection offers can make consumers pay for weak or fake coverage. Verifying that a company is licensed, reading independent reviews, and asking questions before signing are basic consumer protections.

Another smart habit is reviewing risk over time. A person's needs change when they start driving, move into an apartment, begin working full time, or support family members. The best strategy for a middle school student is not the same as the best strategy for a working adult with dependents. Risk management should change as financial responsibilities change.

"Insurance is not meant to make people richer after a loss. It is meant to keep a loss from ruining them."

Strong risk management protects both current income and future goals. A person who avoids scams, reduces preventable dangers, accepts only manageable losses, and transfers catastrophic losses through insurance is more likely to stay on track with savings, education, housing, and career plans.