Have you ever wanted something so much that you counted the days until you could get it? Maybe it was a new book, an art set, a game, or a soccer ball. Wanting something is the easy part. The tricky part is making a financial plan so you can actually buy it. A good plan turns a big wish into small, clear steps.

Money plans are important because money is limited. Most people cannot buy everything they want right away. That means they must choose, save, and wait. Learning how to plan for money now helps you make smart choices later too.

A short-term financial goal is something you want to pay for in the near future. "Short-term" means it does not take years. It might take a few days, a few weeks, or a few months. "Financial" means it has to do with money.

Examples of short-term financial goals for a third grader might include buying a $12 storybook, saving $18 for a class T-shirt, or collecting $25 for a small toy or game. These are goals because they give your money a purpose.

Some things are needs, like food, a home, and clothes. Other things are wants, like extra toys or treats. Many short-term goals are wants. That does not make them bad. It just means we should plan carefully before spending money on them.

Financial goal means something you want to use money for in the future.

Short-term means happening soon, usually within a short amount of time.

Save means to keep money now so you can use it later.

When you choose a goal, it helps to be specific. "I want something fun" is not a strong goal. "I want to save $20 for a sketch pad and markers by the end of next month" is much better because it tells exactly what, how much, and when.

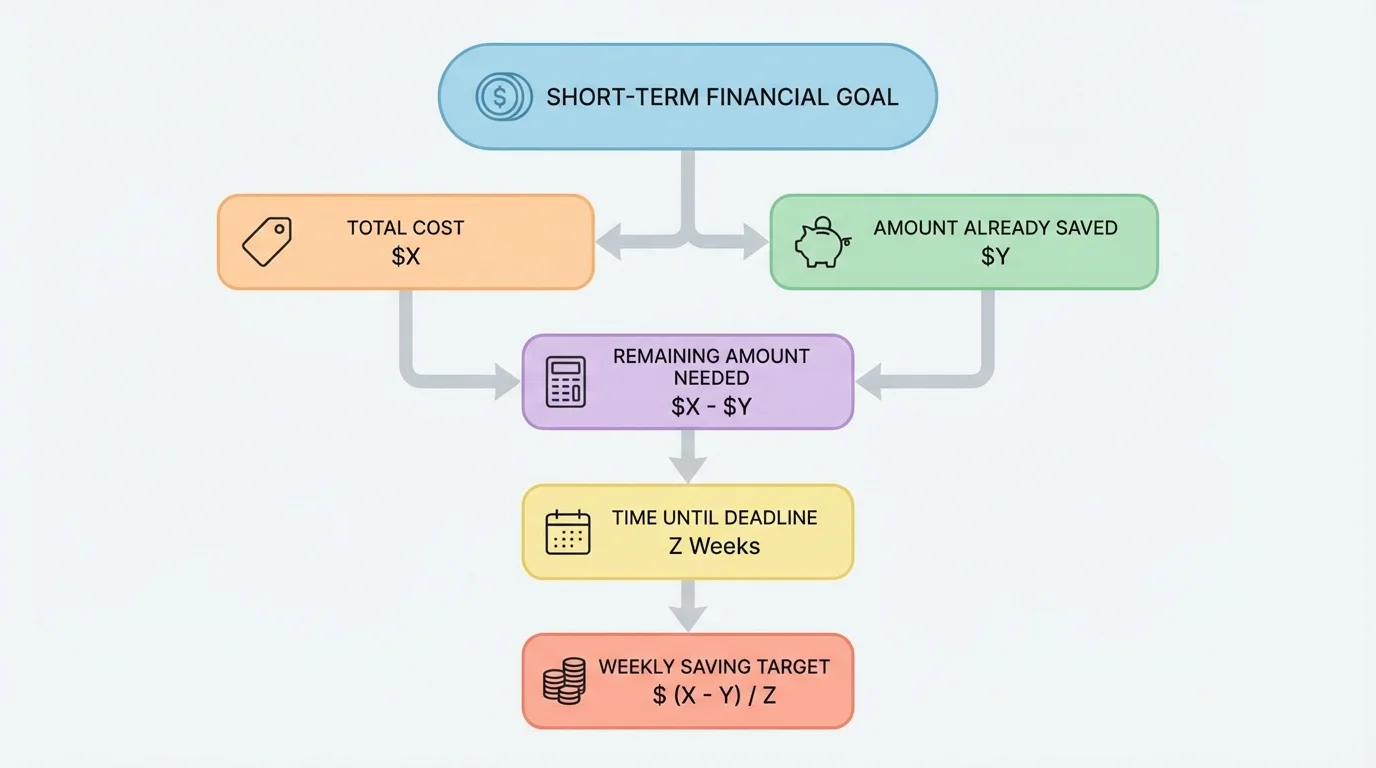

A simple financial plan has a few important parts, and [Figure 1] shows how they connect in order. First, name the goal. Next, find the cost. Then, think about how much money you already have. After that, decide how much time you have. Last, figure out how much money you need to save each week or each time you get money.

These parts work together. If the cost is high, you may need more time or bigger savings. If you already have some money, your job becomes easier. A plan helps you see the whole picture instead of guessing.

Suppose Maya wants a puzzle that costs $16. She already has $4. She needs to find how much more money she must save. She subtracts the money she has from the total cost: \(16 - 4 = 12\). Maya still needs $12.

Now suppose Maya wants the puzzle in 4 weeks. She can divide the amount she still needs by the number of weeks: \(12 \div 4 = 3\). She needs to save $3 each week. That is a clear and useful plan.

Big goals become small steps

Many money goals seem hard at first because the total cost looks large. A plan breaks the total into smaller parts. Saving $3 each week feels easier than thinking only about $12 all at once. This is one reason planning works so well.

Knowing the cost matters too. Sometimes people guess the price and do not save enough. Smart planners check the real price first. They may look at a store tag, a website with an adult, or a class paper that tells the amount needed.

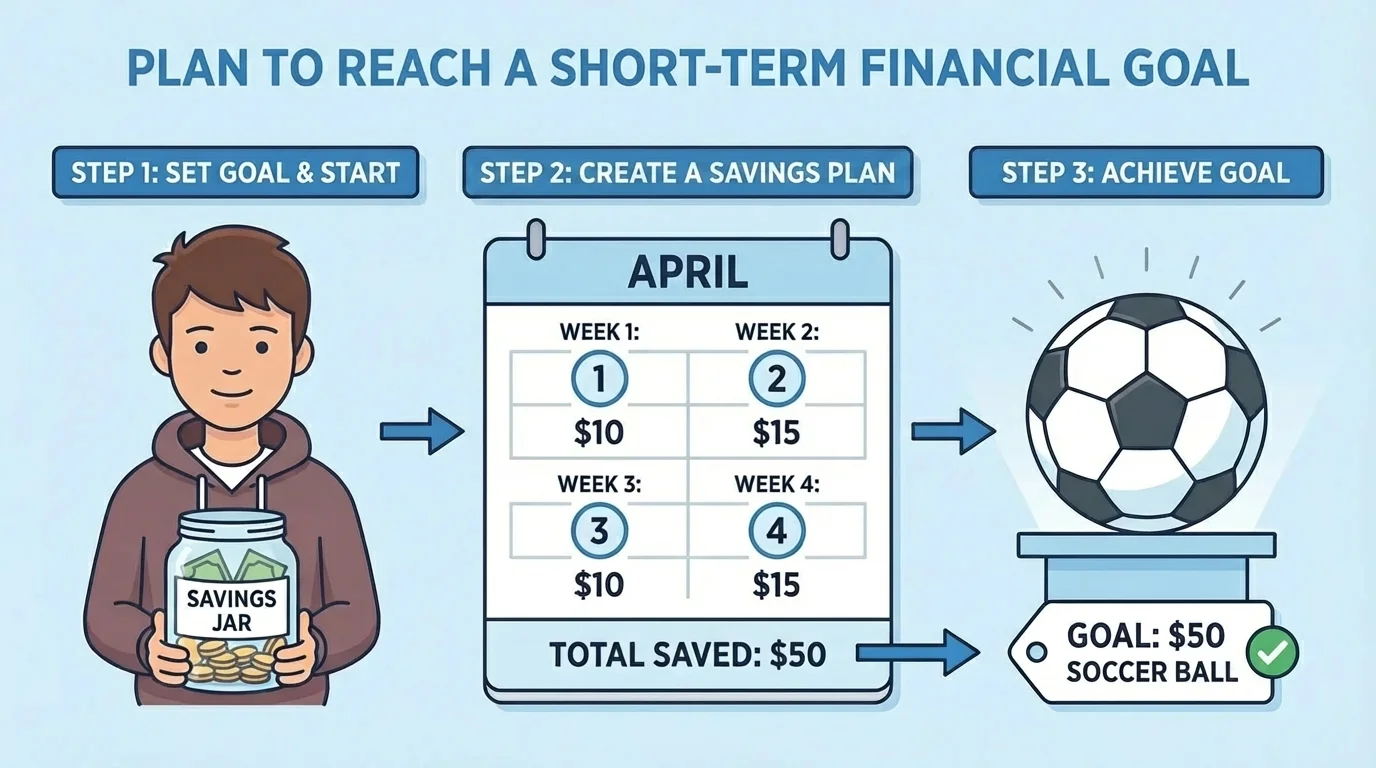

Reaching a goal is easier when you follow steps, and [Figure 2] illustrates how one goal can be divided into small savings jobs on a calendar. You do not have to do everything at once. You just need to know what to do first, next, and after that.

Step 1: Choose one goal. Pick something clear and real, such as "I want to buy a $15 craft kit."

Step 2: Write the total cost. You need to know exactly how much money is required.

Step 3: Write how much money you already have. Maybe you already saved some coins or dollars.

Step 4: Subtract to find how much more you need. If the craft kit costs $15 and you already have $6, then \(15 - 6 = 9\). You still need $9.

Step 5: Choose a time to reach the goal. Maybe you want it in 3 weeks.

Step 6: Divide the amount you still need by the number of weeks or chances to save. If you need $9 in 3 weeks, then \(9 \div 3 = 3\). You need to save $3 each week.

Step 7: Decide where the money will come from. You might save part of your allowance, birthday money, or money earned for chores at home.

Step 8: Track your progress. Each time you save, mark it on a chart, calendar, or paper. Small check marks can lead to a big success.

A plan can change if needed. If you save less one week, you can look at your plan again and make a new one. Maybe you need one more week, or maybe you decide to save a little extra the next time. That is not failure. That is a smart adjustment.

As we see again in [Figure 1], every step connects to the next one. If the cost changes, the weekly savings may change too. Plans are meant to guide you, not trap you.

Let's look at several examples of students making short-term money plans.

Example 1: Saving for a book

Jalen wants a book that costs $10. He already has $2. He wants to buy it in 4 weeks.

Step 1: Find how much more money Jalen needs.

Subtract the amount he has from the total cost: \(10 - 2 = 8\).

Step 2: Find how much to save each week.

Divide the amount still needed by 4 weeks: \(8 \div 4 = 2\).

Jalen should save $2 each week.

This plan is simple because the goal, the amount already saved, and the time are all clear.

Example 2: Saving for art supplies

Sofia wants markers and paper that cost $21. She already has $9. She wants them in 4 weeks.

Step 1: Find how much more she needs.

Subtract: \(21 - 9 = 12\).

Step 2: Divide by the number of weeks.

\(12 \div 4 = 3\).

Sofia needs to save $3 each week.

If Sofia saves $4 one week, then the next week may be easier. Plans are helpful, but they do not have to be exactly the same every time.

Example 3: Saving for a ball

Luis wants a ball that costs $24. He has $6 already and wants to buy it in 6 weeks.

Step 1: Find the amount still needed.

\(24 - 6 = 18\).

Step 2: Divide by the number of weeks.

\(18 \div 6 = 3\).

Luis should save $3 each week.

Notice something interesting: Sofia and Luis have different goals, but both save $3 each week. The total cost is not the only thing that matters. The amount already saved and the time also matter.

Small amounts can add up faster than many people expect. Saving $1 again and again may seem tiny, but after 10 times, you have $10.

Sometimes a division problem does not come out evenly. For example, if a toy costs $14, you have $2, and you want it in 3 weeks, then \(14 - 2 = 12\), and \(12 \div 3 = 4\). That works evenly. But if you needed $10 in 3 weeks, \(10 \div 3\) would not be a whole number. In a case like that, you could plan to save $4 each week for 3 weeks so you have enough. Saving a little extra is often smart.

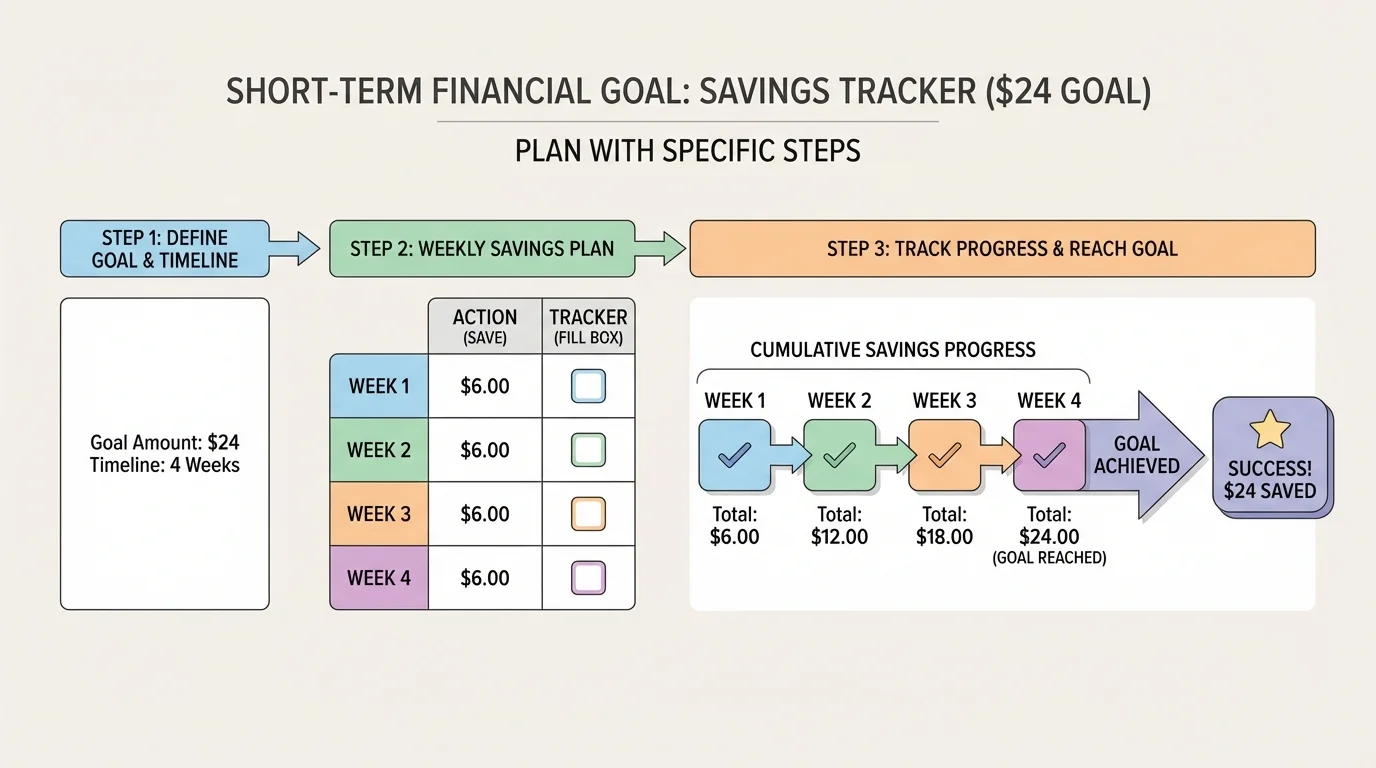

Good plans need good choices, and [Figure 3] shows how a savings tracker helps you watch your progress fill up little by little. One strong choice is to save first. That means when you get money, you put some aside for your goal before spending on something else.

Another strong choice is to spend less on smaller wants while you are working on a goal. If you buy candy or stickers every time you get money, it may take longer to reach your goal. Waiting can help you get something more important later.

Tracking your progress is also helpful. You can use a jar, envelope, chart, or notebook. When you see the amount growing, it can help you stay excited and focused.

You can also compare prices. If one store sells the same item for less money, your goal may become easier. For example, if a game costs $20 at one place and $18 at another, the cheaper price saves $2. That changes your plan in a good way.

Sometimes your plan must change because something unexpected happens. Maybe you thought you could save $3 this week, but you only saved $2. You can fix the plan by checking how much is left and dividing again. This is another reason a tracker is useful, just like the one in [Figure 3]. It helps you see what still needs to be done.

You already know how to add, subtract, and divide. Those same math skills help you make money plans. Subtraction tells how much more you need. Division tells how much to save each week or each time you receive money.

Planning also helps you make decisions. If the weekly amount is too high, you have choices. You might choose a cheaper item, take more time, or save more often. A strong plan is realistic, which means it matches what you can truly do.

Nia wants to buy a small science kit for $30. She has saved $12 in her piggy bank. She hopes to buy it in 6 weeks before a school break. First, she finds the amount she still needs: \(30 - 12 = 18\). Then she divides by the number of weeks: \(18 \div 6 = 3\). Nia decides to save $3 each week.

She writes her plan on paper: goal, total cost, money already saved, amount still needed, number of weeks, and weekly savings. This is exactly the kind of organized thinking shown earlier in [Figure 1]. Because she can see each part clearly, she knows what to do next.

In week 1, Nia saves $3. In week 2, she saves $4 because she helps wash the car. In week 3, she saves only $2. She checks her tracker and sees that she is still close to her goal. The picture of filling boxes, like the one in [Figure 3], matches what is happening with her own plan.

By breaking the goal into smaller actions, Nia avoids feeling overwhelmed. That is the same idea we saw in [Figure 2]: one big goal becomes a series of smaller jobs. At the end of 6 weeks, Nia reaches her goal because she kept checking, saving, and adjusting.

Some habits make almost every money goal easier. One habit is budgeting. A budget is a simple plan for how money will be used. Even a child can use basic budget ideas by deciding, "I will save part and spend part."

Another helpful habit is patience. Sometimes waiting is hard. But waiting gives your money time to grow. When you save toward a goal instead of spending right away, you are practicing self-control.

It also helps to be honest about what you can do. If you usually get $2 each week, a plan that says you will save $6 each week may not be realistic. A smaller goal or a longer timeline may work better.

Adults often use these same planning steps for bigger goals. They may save for a bike, a trip, a phone, or something for their home. The numbers are larger, but the idea is the same: know the cost, know the time, and make a plan.

"A goal without a plan is only a wish."

— Common saying

When you plan your money, you are being thoughtful, responsible, and prepared. You are telling your money where to go instead of wondering where it went. That is a powerful skill.