You might earn $15 per hour, work several hours, and still get a paycheck that feels smaller than your quick mental estimate. That is not necessarily a mistake. It is one of the first big money lessons of adult life: the amount you earn and the amount you actually keep are not the same. If you do not understand why money is removed from your pay, it becomes easy to overspend, miss errors, or feel confused about where your money went.

Learning how taxes, paychecks, and deductions work gives you real control. Whether you get a part-time job, summer job, freelance income, or your first full-time job later on, you need to know how to read what you are paid, what was taken out, and what reaches your bank account. This is not just paperwork. It affects how much you can save, spend, and plan for goals like a phone bill, gas, clothes, entertainment, or college expenses.

When people first start working, they often multiply hours by hourly pay and assume that number is theirs to spend. That estimate usually gives gross pay, which is the total amount earned before money is taken out. Your actual spending money is your net pay, which is what remains after taxes and other deductions are removed.

Gross pay is the total money you earn before deductions. Net pay is the amount you actually receive after deductions. Deductions are amounts subtracted from your earnings, such as taxes, insurance, or retirement contributions.

For example, if you earn $16 per hour and work 20 hours, your gross pay is

\[16 \times 20 = 320\]

Your gross pay is $320. But your paycheck will usually be lower because taxes are withheld, and sometimes other deductions are too. If $48 total is taken out, then your net pay is

\[320 - 48 = 272\]

That means the money you can actually use is $272, not $320. This difference matters. If you plan your spending based on gross pay, you can run short fast.

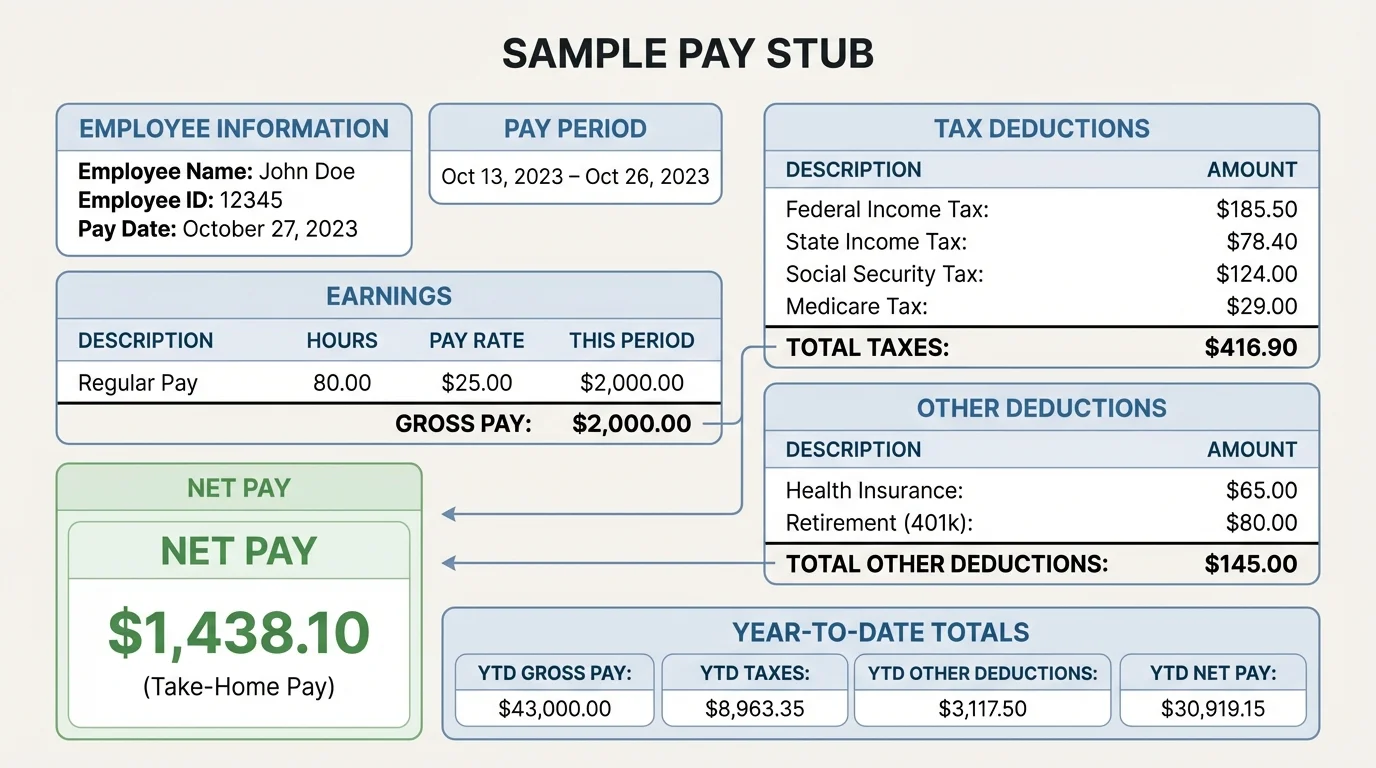

A paycheck usually comes with a pay stub, which breaks one payment into parts, as [Figure 1] shows. Even if you are paid by direct deposit and never receive a paper check, you can usually view this information online through your employer's payroll system.

Some common parts of a pay stub include your pay period, hours worked, pay rate, gross pay, each deduction, and final net pay. It may also show year-to-date (YTD) totals, which track how much you have earned and how much has been deducted since the beginning of the year.

If you are paid hourly, your paycheck depends on how many hours you worked. If you are paid a salary, your paycheck is usually more predictable because your yearly pay is divided across pay periods. For example, a salary of $36,000 paid twice a month leads to 24 paychecks per year, so each gross paycheck would be

\[36000 \div 24 = 1500\]

That is gross pay, not take-home pay.

Pay frequency also matters. You might be paid weekly, every two weeks, twice a month, or monthly. The same annual income can feel different depending on the schedule. A biweekly paycheck can look larger than a weekly one, but you are also waiting longer between payments.

Another important term is overtime. Overtime usually means extra pay for certain hours worked beyond a standard amount, often at a higher rate. If your job qualifies and you work extra hours, your gross pay rises. But because taxes and deductions may also rise, your net pay increases by less than the full gross increase.

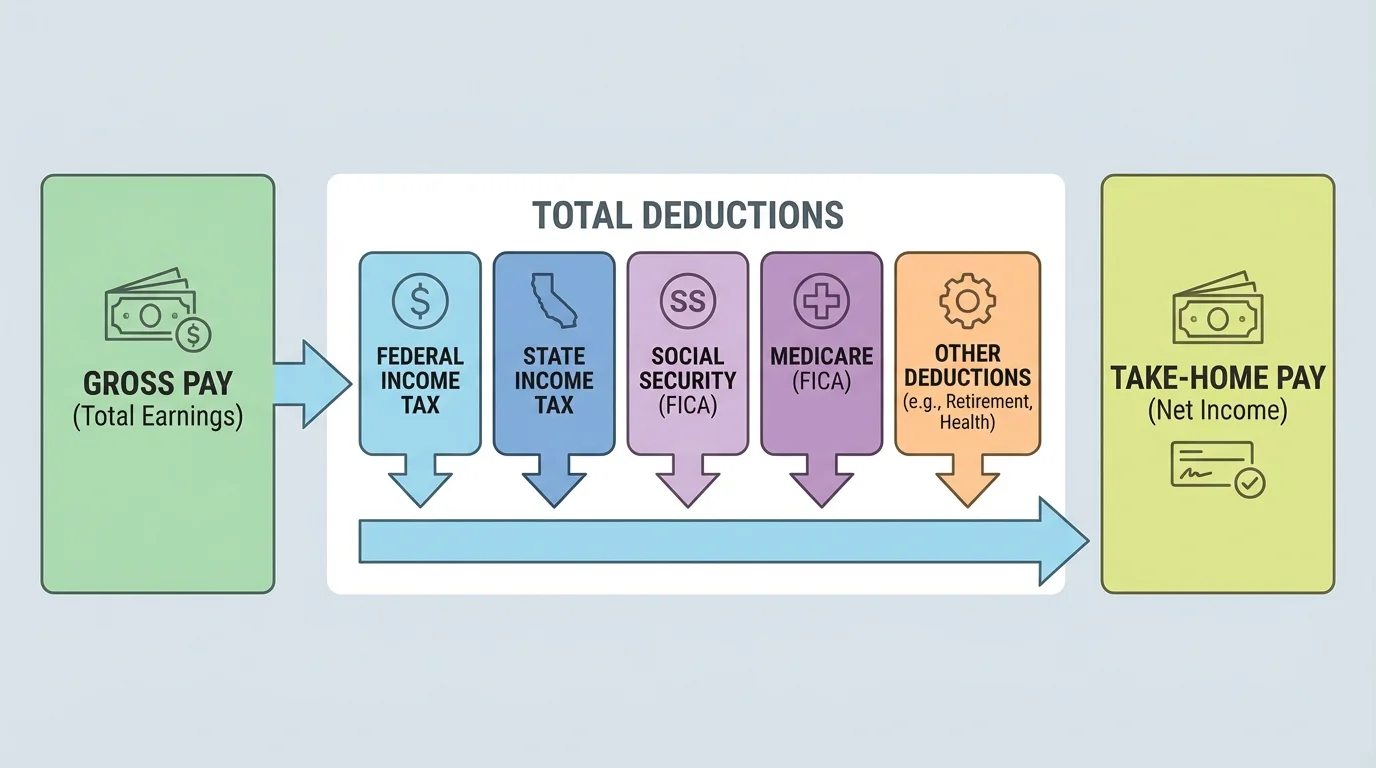

Before money reaches you, several required deductions may come out of your earnings, as [Figure 2] illustrates. These are often called withholding because your employer holds back part of your earnings and sends it to the government for you.

Why withholding exists

Most workers do not wait until the end of the year to pay all taxes at once. Instead, employers withhold estimated amounts from each paycheck. This spreads tax payments across the year and lowers the chance that a worker suddenly owes a large amount later.

Federal income tax helps fund national government services. The amount withheld depends on things such as your income level and the tax information you submit when you start a job.

State income tax exists in many states, though not all. If your state has one, it may also be withheld from each paycheck. Some local areas have local income taxes too.

Social Security tax helps fund benefits for retired workers and some others. Medicare tax helps fund parts of the health insurance system for older adults and certain eligible people. These two are often grouped as payroll taxes.

Here is a simple view of common paycheck deductions:

| Deduction | What it is for | Usually required? |

|---|---|---|

| Federal income tax | National government programs and services | Usually yes |

| State income tax | State government programs and services | Depends on state |

| Social Security | Retirement and related benefits | Usually yes |

| Medicare | Health coverage support for eligible groups | Usually yes |

| Local tax | City or local government services | Depends on location |

Table 1. Common taxes that may appear as paycheck deductions.

These taxes are one reason your paycheck is lower than your gross earnings. Later, when you budget, your real number is always net pay. As you saw earlier in [Figure 1], the pay stub separates gross earnings from the amounts taken out.

A common misunderstanding is thinking, "If more tax is withheld, I lost that money forever." What actually matters is whether the total tax paid across the year matches what you owe. In some cases, too much is withheld and you may get a tax refund later. In other cases, too little is withheld and you may owe money. A refund is not free bonus money; it usually means you paid too much during the year.

Not every deduction is a tax. Some are optional, and some depend on your job. For example, an employer may offer health insurance, dental insurance, vision insurance, or a retirement savings plan. If you sign up, money can be deducted from each paycheck to help cover those costs.

Some workers also choose direct deductions for things like union dues, charitable donations, or savings accounts. These are often called voluntary deductions because the worker chooses them.

There are also less common deductions, such as a garnishment. A garnishment is a court-ordered deduction, often connected to unpaid debt or other legal obligations. This is one example of how money decisions can affect future income in a very real way.

Small deductions can feel harmless because each one seems minor, but several small deductions added together can reduce a paycheck by a noticeable amount over time.

That is why it is smart to know which deductions are required and which ones you chose. Required taxes are part of working. Optional deductions should match your actual priorities and budget.

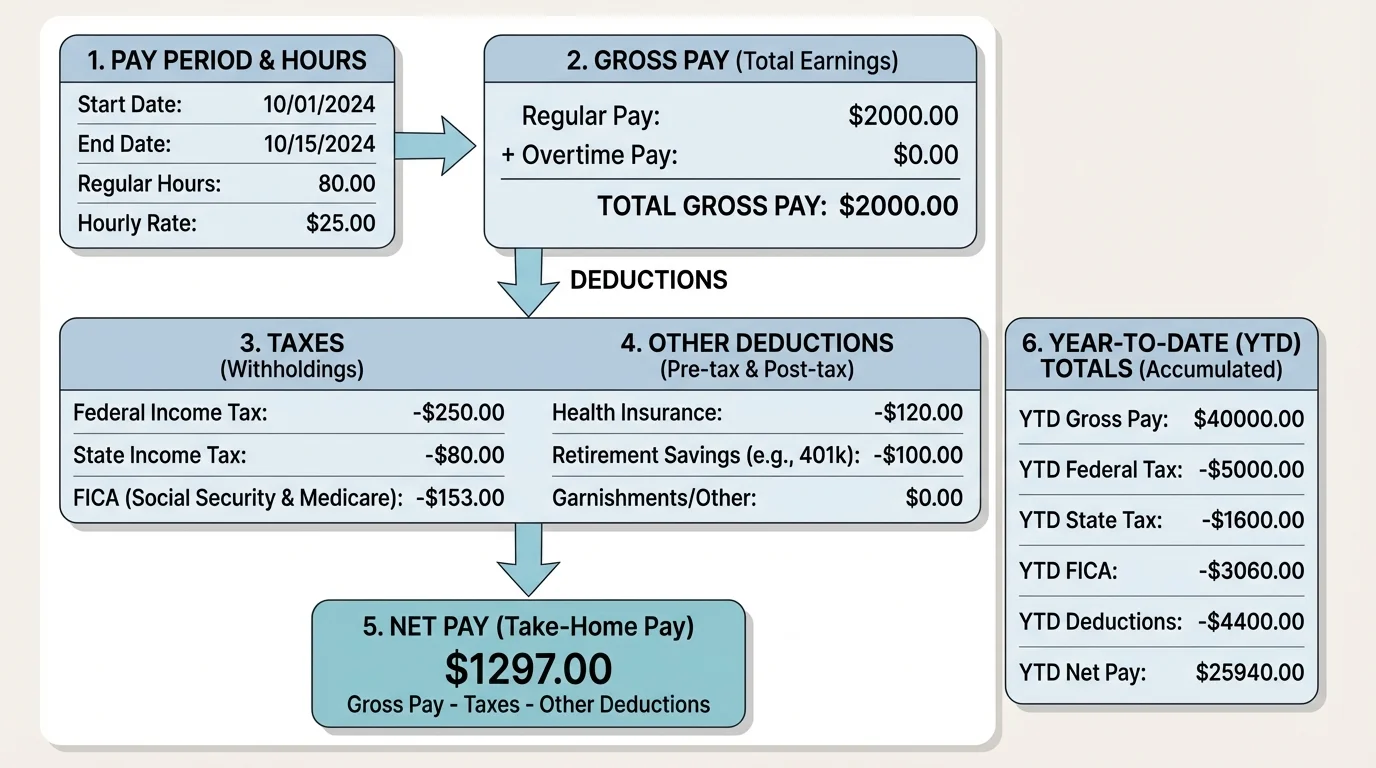

[Figure 3] shows a helpful way to read a pay stub in a consistent order. Instead of staring at all the numbers at once, move through it like a checklist.

Step 1: Check the pay period. Make sure the dates match the time you actually worked.

Step 2: Check hours and pay rate. If you are hourly, confirm that the number of hours and your hourly rate are correct.

Step 3: Find gross pay. This tells you what you earned before deductions.

Step 4: Review each tax withheld. Look for federal, state, Social Security, Medicare, and any local tax.

Step 5: Review other deductions. Check for insurance, retirement, or any other selected deductions.

Step 6: Find net pay. This is your real take-home amount.

Step 7: Scan the YTD totals. These help you track the bigger picture across the year.

Using this order can help you notice errors faster and understand how each part of the paycheck connects to the final amount you receive.

If something seems wrong, do not ignore it. Mistakes can happen with hours, rates, or deductions. It is easier to fix a payroll issue quickly than months later. Save your pay stubs digitally or in a folder so you can compare them over time.

Checking an hourly paycheck

A student works 18 hours at $14 per hour during one weekly pay period. Taxes and other deductions total $37.

Step 1: Calculate gross pay.

\[18 \times 14 = 252\]

Step 2: Subtract total deductions.

\[252 - 37 = 215\]

The worker's net pay is $215. That is the number to use for spending and saving decisions.

Using a system like this lowers stress. You do not need to memorize every tax rule. You do need to know how to locate the important numbers and notice when something does not add up.

Seeing the numbers in realistic situations helps make this feel less abstract. The goal is not advanced math. The goal is learning how your earnings turn into usable money.

Example 1: Part-time weekend job

A worker earns $15 per hour and works 12 hours. Federal tax withheld is $12, state tax is $5, and payroll taxes total $14.

Step 1: Find gross pay.

\[15 \times 12 = 180\]

Step 2: Add deductions.

\[12 + 5 + 14 = 31\]

Step 3: Find net pay.

\[180 - 31 = 149\]

The worker earned $180 gross but can actually use $149.

If that worker expected to have the full $180 available, they might overspend by $31. That is why understanding deductions protects your budget.

Example 2: Same hours, extra voluntary deduction

Suppose the same worker also chooses a $10 savings deduction through work.

Step 1: Start with the previous total deductions of $31.

Step 2: Add the new deduction.

\[31 + 10 = 41\]

Step 3: Recalculate net pay.

\[180 - 41 = 139\]

Now the paycheck amount is $139, but $10 has been moved into savings. Lower take-home pay is not always bad if the deduction supports your goals.

This is an important adulting idea: a smaller paycheck is not always worse. If part of your money is going into savings, retirement, or insurance, you may be building stability even though your spendable cash is lower.

Example 3: Overtime changes the picture

A worker earns $16 per hour for 20 regular hours and 4 overtime hours at $24 per hour. Total deductions are $62.

Step 1: Calculate regular pay.

\[16 \times 20 = 320\]

Step 2: Calculate overtime pay.

\[24 \times 4 = 96\]

Step 3: Add for gross pay.

\[320 + 96 = 416\]

Step 4: Subtract deductions.

\[416 - 62 = 354\]

The worker takes home $354. Working more hours increased net pay, but not by the full $96 because deductions also increased.

As shown earlier in [Figure 2], extra earnings pass through the same system of taxes and deductions before becoming take-home pay.

The most useful budgeting mistake to avoid is planning around gross pay. Your bills and spending come out of net pay, not from the larger number listed before deductions. If your average weekly net pay is $215, then your budget should be built around that amount.

For example, suppose your weekly net pay is $215. You decide to divide it this way: $60 for savings, $40 for transportation, $30 for entertainment, $25 for food, and $60 for personal spending or future expenses. The total is

\[60 + 40 + 30 + 25 + 60 = 215\]

That plan works because it uses real take-home pay. If you had used a gross amount of $252 instead, you would be budgeting money you never actually received.

When money is limited, every category competes with the others. A realistic budget starts with the amount available after required deductions, then assigns that money on purpose.

Taxes and deductions also affect short-term choices. If you pick up an extra shift, your take-home pay goes up, but not dollar for dollar. If you sign up for insurance or a savings deduction, your current spending money goes down, but your protection or savings may go up. Good decisions depend on knowing the tradeoff.

The reading process from [Figure 3] helps here too. Once you can quickly spot gross pay, deductions, and net pay, you can make smarter choices about accepting shifts, setting savings goals, or deciding what you can really afford.

When you start a job, fill out hiring forms carefully. Tax forms help determine how much is withheld from your paycheck. If the information is wrong, your withholding may be off too.

Keep records. Save pay stubs, W-2 forms, and any tax documents you receive. You do not need to become a tax expert right away, but you do need a basic paper trail. If something is incorrect, your records help you prove it.

Review every paycheck, especially early on. Check your hours, rate, deductions, and net pay. Do not assume computers never make mistakes. A few minutes of checking can protect hours of work.

"It is not enough to earn money. You also need to understand where it goes."

Another smart habit is separating spending money from savings money right away. When your paycheck arrives, decide what part is for current use and what part is for future goals. This keeps net pay from disappearing without a plan.

Your income will not always stay the same. You may work more hours during summer, fewer during exam weeks, or earn extra money from side jobs. Bonuses, overtime, and inconsistent hours can all change your gross pay and your withholding.

If you do gig work or freelance jobs, taxes may not be withheld automatically. That means you could receive more money upfront but still owe taxes later. In that situation, setting money aside yourself is important. Otherwise, the money can feel like it is all yours when it really is not.

A raise can also be misunderstood. If your hourly pay increases from $14 to $15 and you work 20 hours, your gross pay changes from

\[14 \times 20 = 280\]

to

\[15 \times 20 = 300\]

Your gross pay rises by $20, but your net pay will rise by less than $20 if withholding and other deductions also increase. The raise still helps, but the full increase does not all become spending money.

This is why strong money management depends on looking past the headline number. Bigger gross income usually helps, but what matters for everyday life is how much actually lands in your account after everything is taken out.